A spokesman for the Ministry of Finance has declared there is no housing bubble:

“We don’t believe we’re in a bubble,” Bank of Canada Governor Stephen Poloz said in testimony Tuesday to the House of Commons Standing Committee on Finance. He said Canada’s long-running boom in the housing market hasn’t been underpinned by the kind of rampant speculative buying that is the hallmark of an asset bubble.

“Our housing construction has stayed very much in line with our estimates of demographic demand,” he said. “There’s no excess.”

This despite the central bank’s own estimate, published last December in its Financial System Review, that Canada’s housing market is overpriced by between 10 and 30 per cent.

Mr. Poloz indicated that he believes the overvaluation is not a symptom of runaway prices and widespread investor speculation, but rather of ongoing strength in consumer demand spurred by historically low interest rates – rates that were cut by the central bank in order to keep consumer demand buoyant to support Canada’s economy during the Great Recession.

A few months ago I received an eMail from a Concerned Investor:

This is not likely to happen but if the BOC 5 year rate fell to minus 2% or lower and some of these insanely priced resets at less than 200 basis points aren’t called ( and by the way probably never will) would the buyer be obliged to pay the issuer the difference ?

… and I answered with a reference to a PrefBlog comment that addressed a question regarding a negative GOC-5 yield.

We are now seeing some real life examples in European markets:

Negative interest rates are an odd fish in the world of finance given that they basically wreak havoc on a central tenet of investing; that investors will be compensated in some way for, you know, investing in things.

Bloomberg’s Alastair Marsh reports today on POPYM 2007-2 A3G, a 2007 securitization deal that bundled together loans made to small businesses in Spain. Trustees for the bonds appear to be halting coupon payments to the debt’s investors after a benchmark interest rate to which the deal is tied turned negative in recent days.

…

While this particular Spanish securitization, put together by Banco Popular, does have a legal clause that stops coupons from turning negative, it’s highly unlikely that all banks which created such bond deals would have anticipated an era of negative rates. In other words, it’s not entirely clear how such securitized debt will react to a sub-zero world.

For what it’s worth, Danish mortgage lender Nykredit said last month that it would fix coupon rates on its own floating-rate bonds to zero if benchmark interest rates turn negative.

Negative yields! On a protracted basis! Ha-ha! That’s as ridiculous an idea as thinking there could ever be a significant decline in US national real-estate prices!

I noted a broadly based retail trend towards low-cost funds and ETFs on April 24. One impediment to such a trend in Canada has just been addressed:

Exchange-traded funds will now be more readily available to investors as an industry solution announced Tuesday will provide mutual fund advisers direction on how to sell ETFs.

Unlike mutual funds, ETFs are sold on an exchange. Currently, mutual fund licensed representatives can trade in exchange-traded funds that meet the definition of a mutual fund under securities legislation. This includes the majority of ETFs in the marketplace.

The problem for the majority of mutual fund advisers is that they do not have access to an exchange in order to settle the trade.

The Canadian ETF Association (CEFTA), along with the Federation of Mutual Fund Dealers (FMFD), announced mutual fund dealers would soon be able to provide advisers access to an exchange through a partnership with custody and trade execution provider National Bank Correspondent Network (NBCN). The solution was announced at the FMFD conference earlier Tuesday.

Of course, there’s a very good chance that the fees on fee-based accounts will (i) exceed the savings generated by the migration and/or (ii) dissuade unsophisticated investors from the notion, but we’ll just have to see how everything shakes out.

Treasury yields rose significantly today:

Treasury 10-year yields reached 2 percent for the first time in a month as the Federal Reserve began a two-day policy meeting and investors were lured away by higher-yielding corporate debt.

U.S. government debt dropped for a second day as Fed policy makers gathered in Washington to debate whether growth is strong enough to raise borrowing costs for the first time since 2006, with economists forecasting a September move. Oracle Corp. and Amgen Inc. are raising money in the bond market, weighing down Treasuries as underwriters hedged bets on interest rates.

…

Yields on 10-year note yields rose eight basis points, or 0.08 percentage point, to 2 percent as of 5 p.m. New York time, according to Bloomberg Bond Trader data. The price of the benchmark 2 percent security due in February 2025 fell 23/32, or $7.19 per $1,000 face value, to 99 31/32.

It’s the first time yields have touched 2 percent since March 26, along with the highest close since March 17 and biggest increase since March 6. Yields are still down from the 2014 close of 2.17 percent.

Treasury five-year note yields added six basis points to 1.40 percent.

In a very encouraging sign, we see an investment firm hiring traders:

Canyon Partners co-Chief Executive Officer Josh Friedman says his credit investment firm has added traders from Wall Street as banks exit market making.

“Wall Street has lots of traders who are available because they’re not allowed to take positions,” Friedman said in a Bloomberg Television interview with Stephanie Ruhle Monday at the Milken Institute Global Conference in Beverly Hills, California. “If we’re interested in buying a security, we want to make sure we have very high talent level on the trading desk to be able to go out and source those securities at cheap prices.”

…

“It’s hard to move large blocks of debt and we’ll find that the people who actually buy it are not intermediaries, but they’ll be end consumers who are not leveraged,” he said. “It means there will be other types of opportunities to make money.”

A “handful or maybe two handfuls” of other credit firms are taking similar action, said Friedman.

And finally, here’s an alternative investment I could wrap myself around:

A U.K. brewer is offering investors an alternative to record-low interest rates at home and negative bond yields in the euro area: bottles of its own craft beer.

Innis & Gunn Brewing Co. Ltd., which is based in Edinburgh, is offering beer coupons in place of interest payments on a 3 million-pound ($4.6 million) notes issue. It’s just the latest small company to embrace crowdfunding to raise cash.

The brewer will use the proceeds of the four-year sale to fund the construction of a new site. The notes offer gross annual interest of 7.25 percent for investments starting at 500 pounds. Investors opting to be paid in beer will receive the equivalent of 9 percent interest a year, the company said.

It was a violently mixed day for the Canadian preferred share market, with PerpetualDiscounts off 20bp, FixedResets up 36bp and DeemedRetractibles gaining 2bp. The Performance Highlights table is lengthy, with ENB, TRP and BAM issues again prominent. Volume was on the high side of average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

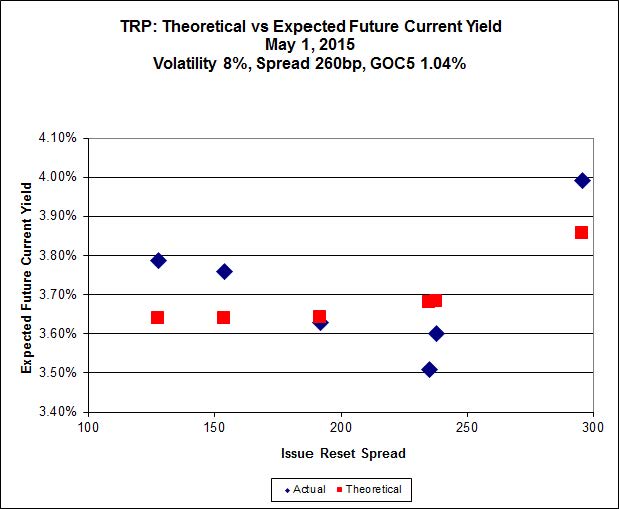

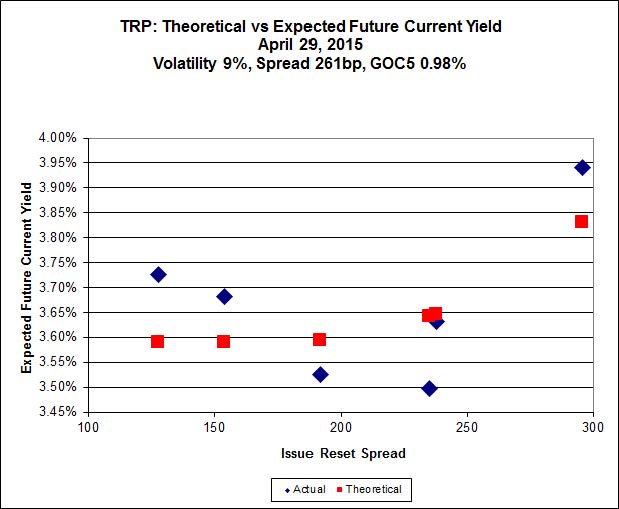

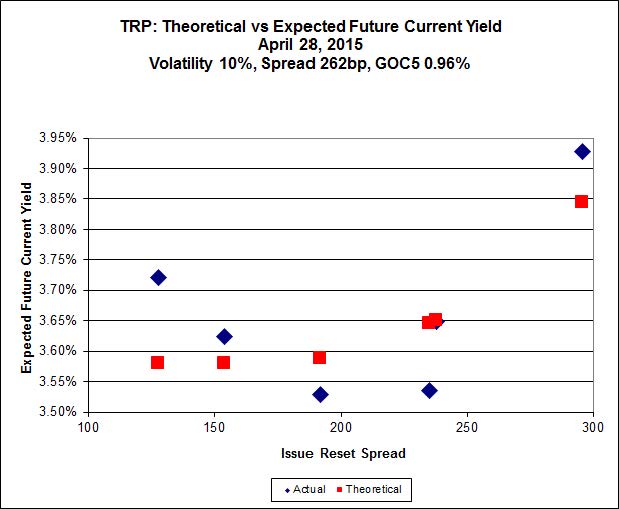

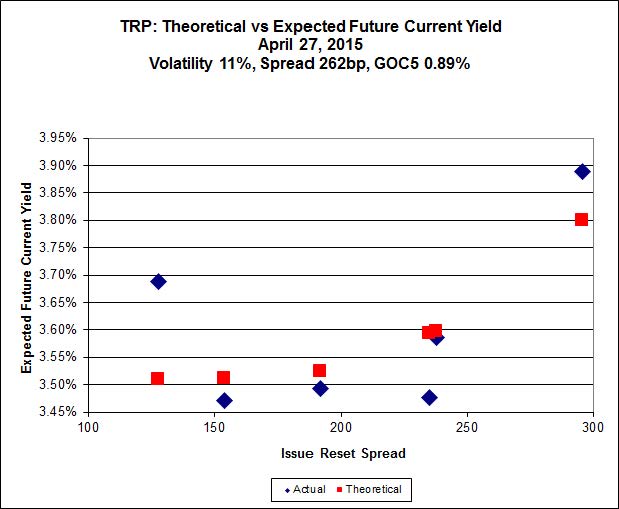

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 23.41 to be $0.71 rich, while TRP.PR.B, resetting 2015-6-30 at +128, is $0.59 cheap at its bid price of 15.05.

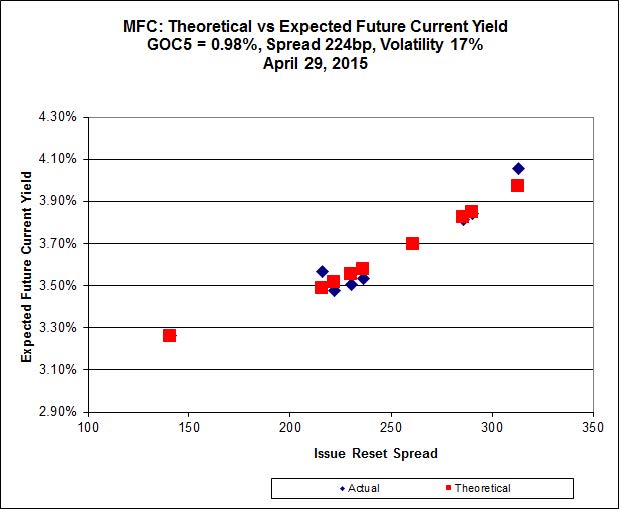

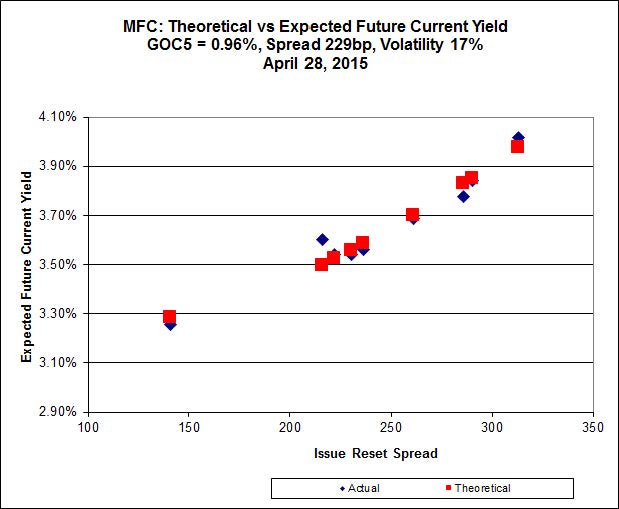

Click for Big

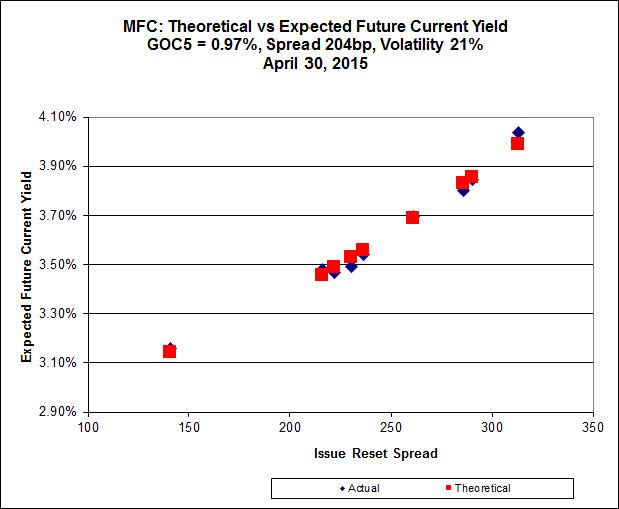

Click for BigAnother excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.I, resetting at +286 on 2017-9-19, bid at 25.28 to be $0.34 rich, while MFC.PR.L, resetting at +216bp on 2019-6-19, is bid at 21.66 to be $0.64 cheap.

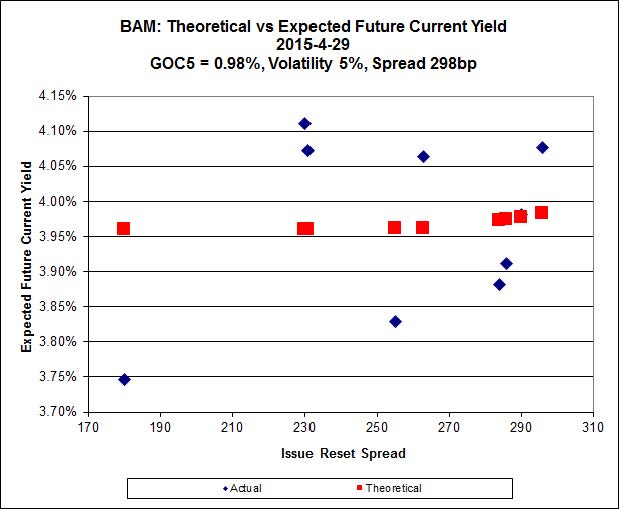

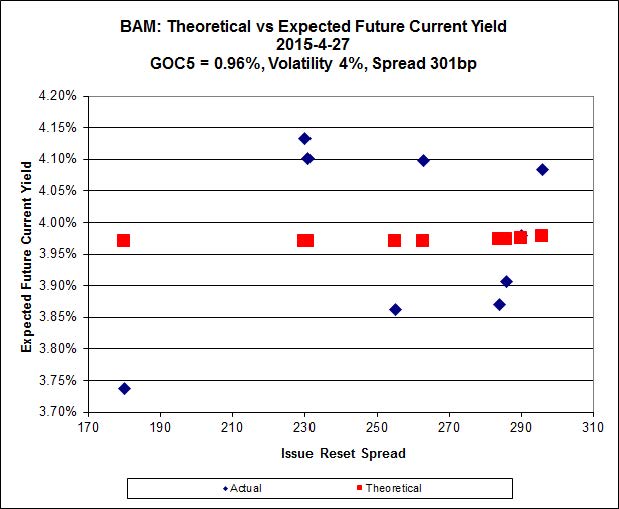

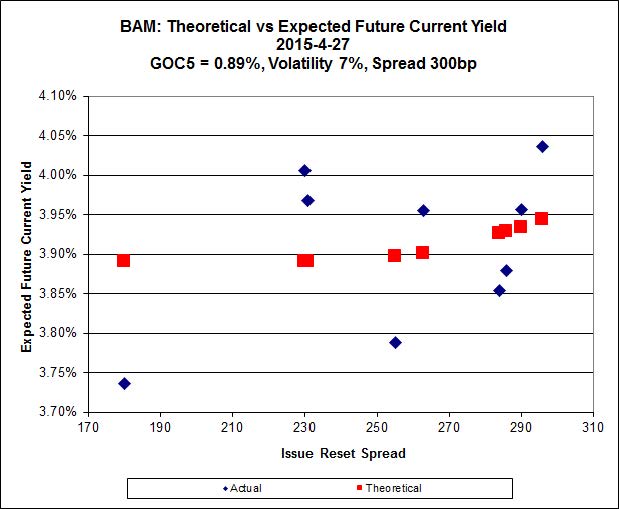

Click for Big

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 19.72 to be $0.81 cheap. BAM.PR.X, resetting at +180bp 2017-6-30 is bid at 28.46 and appears to be $1.08 rich.

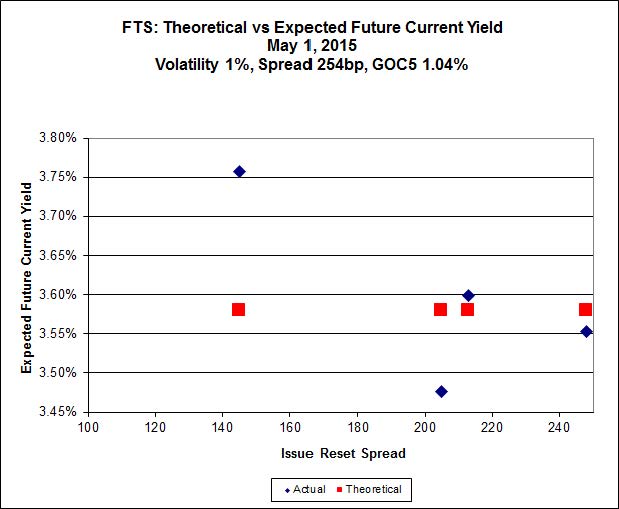

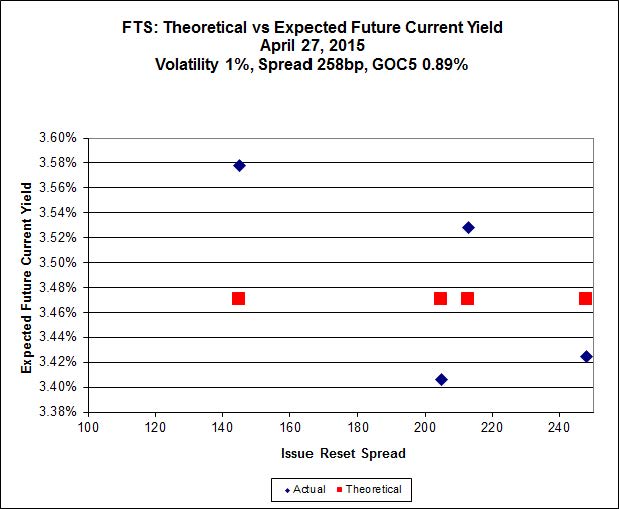

Click for Big

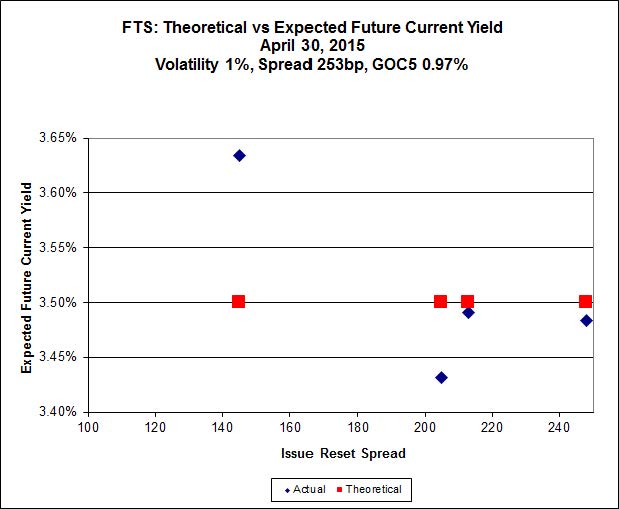

Click for BigFTS.PR.H, with a spread of +145bp, and bid at 16.15, looks $0.77 cheap and resets 2015-6-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 24.61 and is $0.45 rich.

It’s nice to see FTS.PR.M replace FTS.PR.K as most expensive of the series. I think this is the first change in either extremity for as long as I’ve been producing these daily Implied Volatility reports.

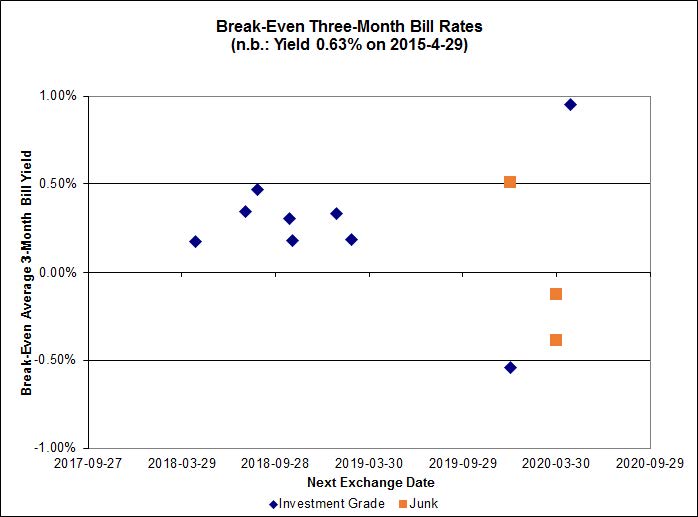

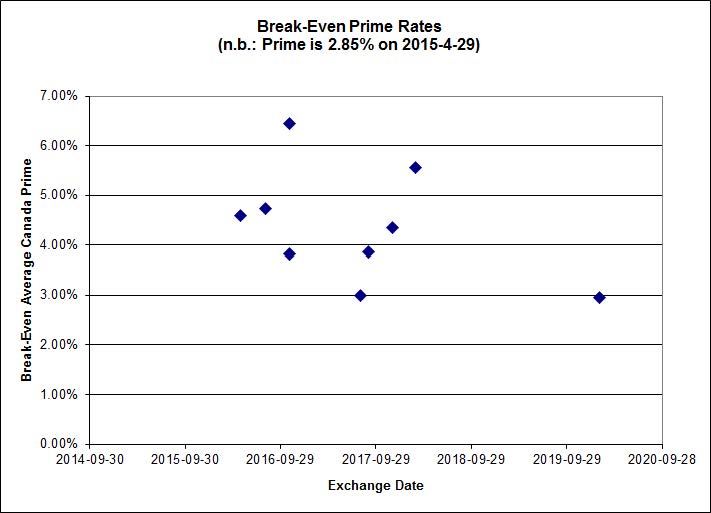

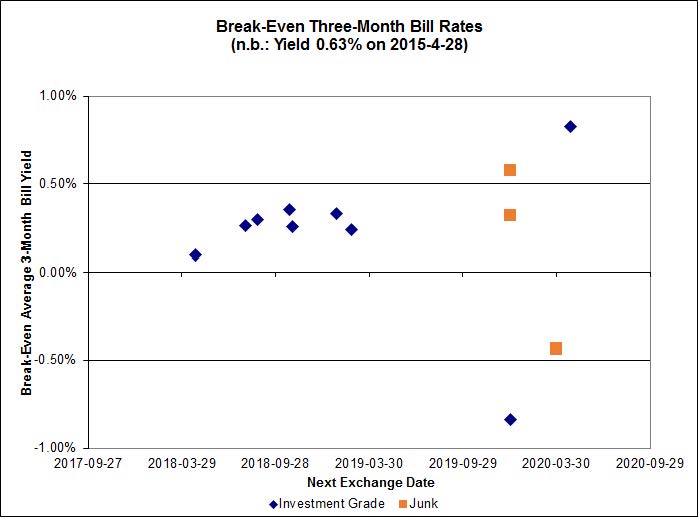

Click for Big

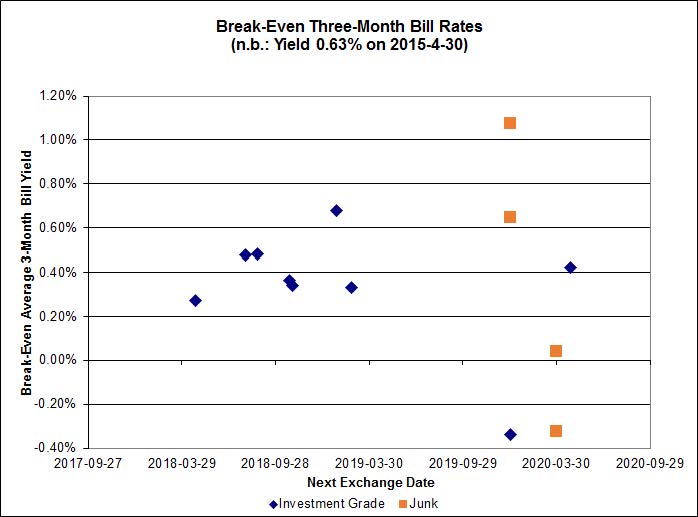

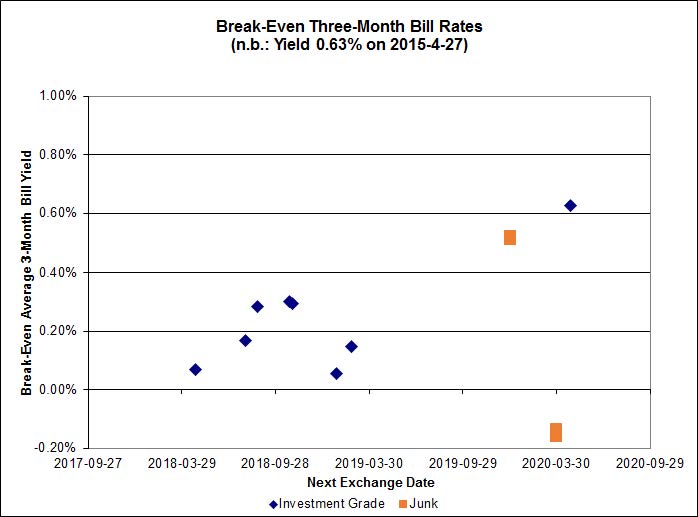

Click for BigInvestment-grade pairs now predict an average over the next five years of about 0.25%, but TRP.PR.A / TRP.PR.F is an outlier at -0.84% and the new BNS.PR.Y / BNS.PR.D pair is at +0.83%. The DC.PR.B / DC.PR.D pair retains its customary outlier status, with a breakeven rate of -1.58%.

Click for Big

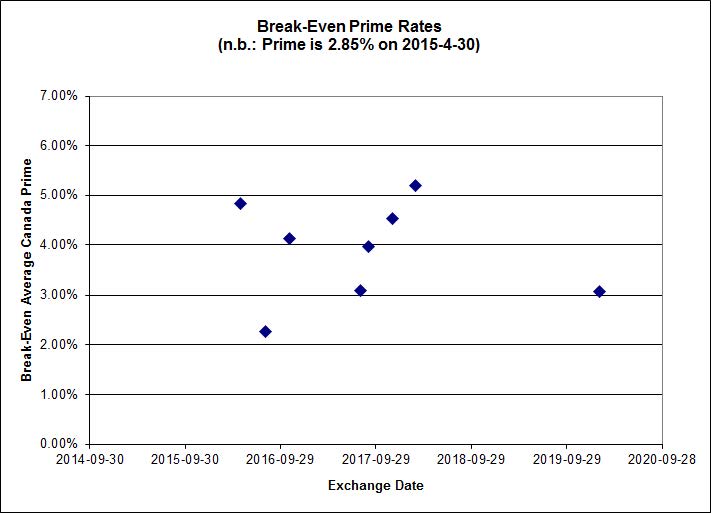

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.5883 % |

2,177.7 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.5883 % |

3,807.6 |

| Floater |

3.33 % |

3.52 % |

55,671 |

18.46 |

4 |

0.5883 % |

2,315.1 |

| OpRet |

4.42 % |

-4.21 % |

40,163 |

0.09 |

2 |

0.0197 % |

2,765.3 |

| SplitShare |

4.57 % |

4.58 % |

69,159 |

3.38 |

3 |

0.1069 % |

3,225.0 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0197 % |

2,528.6 |

| Perpetual-Premium |

5.32 % |

4.23 % |

70,073 |

0.50 |

25 |

0.1538 % |

2,519.8 |

| Perpetual-Discount |

5.14 % |

5.29 % |

139,041 |

14.96 |

9 |

-0.2032 % |

2,777.5 |

| FixedReset |

4.49 % |

3.81 % |

288,512 |

16.36 |

86 |

0.3569 % |

2,362.3 |

| Deemed-Retractible |

4.92 % |

2.63 % |

112,597 |

0.32 |

36 |

0.0199 % |

2,646.6 |

| FloatingReset |

2.52 % |

3.11 % |

73,163 |

6.22 |

9 |

0.2398 % |

2,309.1 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| BAM.PF.B |

FixedReset |

-1.57 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 21.62

Evaluated at bid price : 21.90

Bid-YTW : 4.18 % |

| ENB.PR.H |

FixedReset |

-1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 18.05

Evaluated at bid price : 18.05

Bid-YTW : 4.48 % |

| TRP.PR.C |

FixedReset |

-1.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 17.25

Evaluated at bid price : 17.25

Bid-YTW : 3.61 % |

| FTS.PR.H |

FixedReset |

-1.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 16.15

Evaluated at bid price : 16.15

Bid-YTW : 3.66 % |

| BAM.PR.T |

FixedReset |

-1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 19.93

Evaluated at bid price : 19.93

Bid-YTW : 4.21 % |

| BAM.PR.K |

Floater |

1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 14.04

Evaluated at bid price : 14.04

Bid-YTW : 3.58 % |

| MFC.PR.F |

FixedReset |

1.11 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.20

Bid-YTW : 6.41 % |

| ENB.PF.A |

FixedReset |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 21.35

Evaluated at bid price : 21.35

Bid-YTW : 4.46 % |

| BAM.PF.F |

FixedReset |

1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.01

Evaluated at bid price : 24.45

Bid-YTW : 3.93 % |

| PWF.PR.T |

FixedReset |

1.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.26

Evaluated at bid price : 24.95

Bid-YTW : 3.32 % |

| ENB.PR.Y |

FixedReset |

1.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 19.45

Evaluated at bid price : 19.45

Bid-YTW : 4.48 % |

| BAM.PF.A |

FixedReset |

1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.03

Evaluated at bid price : 24.25

Bid-YTW : 3.97 % |

| ELF.PR.H |

Perpetual-Premium |

1.25 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-04-17

Maturity Price : 25.00

Evaluated at bid price : 25.82

Bid-YTW : 4.92 % |

| VNR.PR.A |

FixedReset |

1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.16

Evaluated at bid price : 24.21

Bid-YTW : 3.84 % |

| TRP.PR.A |

FixedReset |

1.44 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 20.40

Evaluated at bid price : 20.40

Bid-YTW : 3.59 % |

| BNS.PR.Z |

FixedReset |

1.44 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.51

Bid-YTW : 4.12 % |

| BAM.PF.G |

FixedReset |

1.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 22.99

Evaluated at bid price : 24.55

Bid-YTW : 3.92 % |

| BNS.PR.D |

FloatingReset |

1.64 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.26

Bid-YTW : 3.40 % |

| HSE.PR.C |

FixedReset |

1.66 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.00

Evaluated at bid price : 24.50

Bid-YTW : 4.15 % |

| ENB.PR.B |

FixedReset |

1.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 19.15

Evaluated at bid price : 19.15

Bid-YTW : 4.46 % |

| IFC.PR.A |

FixedReset |

1.76 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.20

Bid-YTW : 5.76 % |

| MFC.PR.K |

FixedReset |

2.05 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.45

Bid-YTW : 4.76 % |

| TRP.PR.B |

FixedReset |

2.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 15.05

Evaluated at bid price : 15.05

Bid-YTW : 3.62 % |

| ENB.PR.J |

FixedReset |

2.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 21.26

Evaluated at bid price : 21.26

Bid-YTW : 4.35 % |

| BAM.PR.X |

FixedReset |

2.56 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 18.46

Evaluated at bid price : 18.46

Bid-YTW : 3.95 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| ENB.PR.D |

FixedReset |

470,488 |

TD crossed two blocks of 230,000 each, both at 19.56.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 19.50

Evaluated at bid price : 19.50

Bid-YTW : 4.38 % |

| HSE.PR.A |

FixedReset |

85,051 |

RBC crossed 25,000 at 16.10.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 16.05

Evaluated at bid price : 16.05

Bid-YTW : 4.23 % |

| ENB.PR.F |

FixedReset |

83,952 |

TD crossed 25,000 at 19.80, then another 25,000 at 19.77. Desjardns crossed 20,000 at 19.64.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 19.70

Evaluated at bid price : 19.70

Bid-YTW : 4.50 % |

| TD.PF.E |

FixedReset |

82,980 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.12

Evaluated at bid price : 24.97

Bid-YTW : 3.62 % |

| TRP.PR.B |

FixedReset |

73,846 |

TD crossed 61,100 at 14.83.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 15.05

Evaluated at bid price : 15.05

Bid-YTW : 3.62 % |

| PWF.PR.P |

FixedReset |

62,000 |

Scotia crossed blocks of 13,900 and 15,000, both at 17.68. TD crossed 14,000 at the same price.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 17.75

Evaluated at bid price : 17.75

Bid-YTW : 3.63 % |

| There were 38 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| BAM.PF.A |

FixedReset |

Quote: 24.25 – 25.00

Spot Rate : 0.7500

Average : 0.4540

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.03

Evaluated at bid price : 24.25

Bid-YTW : 3.97 % |

| SLF.PR.H |

FixedReset |

Quote: 21.30 – 21.80

Spot Rate : 0.5000

Average : 0.3446

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.30

Bid-YTW : 5.19 % |

| GWO.PR.F |

Deemed-Retractible |

Quote: 25.55 – 25.95

Spot Rate : 0.4000

Average : 0.2732

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2015-05-28

Maturity Price : 25.00

Evaluated at bid price : 25.55

Bid-YTW : -14.76 % |

| CU.PR.G |

Perpetual-Discount |

Quote: 23.16 – 23.52

Spot Rate : 0.3600

Average : 0.2409

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 22.86

Evaluated at bid price : 23.16

Bid-YTW : 4.92 % |

| BAM.PF.E |

FixedReset |

Quote: 22.72 – 23.35

Spot Rate : 0.6300

Average : 0.5364

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 22.12

Evaluated at bid price : 22.72

Bid-YTW : 4.03 % |

| FTS.PR.M |

FixedReset |

Quote: 24.61 – 24.98

Spot Rate : 0.3700

Average : 0.2840

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-04-28

Maturity Price : 23.05

Evaluated at bid price : 24.61

Bid-YTW : 3.51 % |