Bonds got crushed today:

U.S. Treasury yields hit their highest in around a year on Friday, two days after the government sold 30-year bonds at the highest yield since 2007, as traders anticipated the Federal Reserve would be forced to hike rates to rein in inflationary pressures stemming from energy shocks. Major global stock indexes were down between 1% and 2%, a day after the S&P 500 and Nasdaq hit new highs.

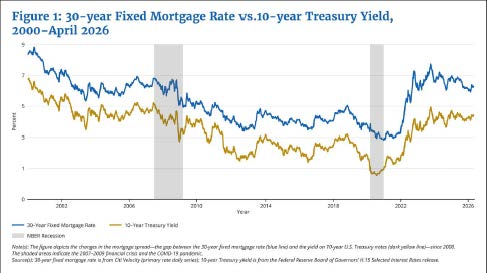

The global move higher in bond yields extended into Canada, where both the five- and 10-year yields reached two-year highs, and were up more than 10 basis points. The moves suggest there will be more upward pressure on GIC and fixed mortgage rates in Canada in the days ahead.

…

Though the bond rout was sweeping the globe, many of the drivers were at least partly local in nature. UK gilt yields surged again, hitting their highest in decades, as pressure mounts on Prime Minister Keir Starmer to resign over his Labour Party’s hefty losses in local elections, and as challengers emerge.

Yields across the euro zone jumped, while Japanese bond yields hit record highs following a red-hot wholesale inflation reading this week that investors believe is likely to lead to rate increases from the Bank of Japan.

Italian 10-year bonds were among the worst performers, with yields up 11 basis points to around 3.89%, bringing the rise for the week to 16 bps, while benchmark German Bund yields rose almost 7 bps to around 3.12%, up 11 bps this week.

Equities noticed:

All three major U.S. stock indexes as well as Canada’s TSX veered sharply lower, each shedding more than 1% as a jump in benchmark Treasury yields, reflecting surging energy prices and concerns about long-term inflation, offered an attractive alternative to higher-risk equities.

Despite the selloff, the S&P 500 logged its seventh straight weekly gain, its longest since a nine-week streak ended in December 2023.

The S&P/TSX Composite Index, Nasdaq and the Dow fell on the week, with the Nasdaq snapping a six-week winning streak.

…

The odds of the Fed hiking interest rates by 25 basis points in December are approaching 40%, up from 13.6% a week ago, according to CME Group’s FedWatch tool.

The Dow Jones Industrial Average fell 537.29 points, or 1.07%, to 49,526.17, the S&P 500 lost 92.74 points, or 1.24%, to 7,408.50 and the Nasdaq Composite lost 410.08 points, or 1.54%, to 26,225.15.

The Toronto Stock Exchange’s S&P/TSX composite index ended down 434.92 points, or 1.3%, at 33,833.35, marking its lowest closing level since May 5. For the week, the index lost 0.7%.

The Canadian 5-year bond yield, a key driver of Canadian mortgage rates, was up 11.6 basis points at 3.351%, its highest closing yield since July 2024.

What a timely date for the Bank of Canada Staff analytical paper 2026-18 Distributing Sovereign Debt in a Rising Debt Environment: Outcomes from Canada’s 2024 Debt Distribution Framework Review by William Bradley and Jeffrey Gao to come out!

This paper documents Canada’s recent review of its sovereign debt distribution framework (DDF). Informed by a context of record-high debt issuance since the previous DDF review, along with comparisons with sovereign peers and insights from market participants, the review identified an important need to broaden Canada’s dealer base internationally to support a larger and more diverse set of investors. As a result, reforms to Canada’s DDF were recommended in 2024 and implemented in 2025. Key changes included revised dealer requirements to attract new international institutions to the non-Primary Dealer Government Securities Distributor (non-PD GSD) class, as well as simplification of auction rules, an increase in non-competitive bidding limits, and the introduction of a new reopening facility for off-the-run bonds.

… and further …

While the GoC and its peers have been issuing significantly more debt, the size of the dealer base has not kept pace.Between 2013 and 2024, the number of Canada’s primary dealers (PDs)—the firms committed to purchasing government securities at auctions and providing liquidity in the market—declined from 12 to 10. This reduction is due to several factors. In addition to dealers consolidating the number of jurisdictions in which they operate, banking regulations introduced after the 2008 financial crisis, such as Basel III and its Leverage Ratio, have strained balance sheets of the larger, bank-owned dealers and reduced the profitability of GoC bond trading.

This trend is common across many advanced economies (OECD 2025).

It is important to note that profits from trading GoC securities are not the only incentive for PDs to participate in primary and secondary GoC markets. Being a regular GoC dealer and liquidity provider is a prerequisite for members of syndicates for Canadian dollar (CAD) issuers and building ancillary customer relationships, which is how PDs generate most of their profits. Still, the declining returns from direct GoC securities activity have negatively affected the balance of dealer benefits and obligations, while also making it harder for new dealers to enter the market.

…

Rising hedge fund participation in sovereign debt markets is a global phenomenon. Epp and Gao (2025) find that, while GoC bond auctions have continued to be well-covered amid the increase to Canada’s debt stock, this can mostly be explained by the corresponding rise in hedge fund allocations—from about 5% to 40% over the past 10 years. The increased presence of hedge funds at auctions has heightened competition for government bonds, which in turn has helped keep Canada’s cost of funding low even as the volume of debt issuance has grown. With the dealer base experiencing limited growth, hedge funds have also assumed a greater role in secondary market intermediation, thereby contributing to market liquidity in normal periods (Sandhu and Vala 2023).

However, higher hedge fund participation brings certain risks. These firms, particularly international ones, tend to have higher attrition rates and less organic commitment to the Canadian market, making them more likely to exit abruptly. Their strategies often involve significant leverage through the repurchase (repo) market, which could pose financial stability risks (Bank of Canada 2024). During periods of market stress, such as the COVID-19 crisis, their trading activity may exacerbate one-sided markets, amplifying volatility—as observed by Sandhu and Vala (2023). With the share of dealer and real money investor participation at auctions declining, any decline or stagnation in hedge fund activity could quickly lead to noticeable deterioration in auction performance.

…

While all other sovereigns consulted have at least half their dealers based internationally, Canada has only one non-domestic dealer. This limited number of international dealers could mean greater exposure to a domestic shock and may constrain the development of Canada’s international client base—considerations that have become more important in an environment of higher debt issuance.

One factor limiting international dealer participation has been the requirement that all dealers be resident in Canada. Together with the requirement for CIRO membership, this has been cited as a significant hurdle for many prospective international dealers. Only two other DMOs consulted—both substantially larger than Canada—also impose an explicit requirement to be resident in their country.

… but, of course, if international dealers are allowed in, profits at Canadian dealers (effectively, Canadian banks) will decline. We can’t have that, not in our version of State Capitalism!

Another mortgage fund has run into liquidity problems:

Mortgage Company of Canada Inc. has temporarily halted redemptions for its residential lending fund as homeowners struggle to make their monthly loan payments amid the country’s housing downturn.

For more than a decade, the alternative mortgage lender has provided loans to homeowners in the Toronto region, which is one of Canada’s priciest real estate markets and an area where mortgage delinquencies have been rising faster than in the rest of the country.

…

Because of what it called adverse conditions, Mortgage Company said it has decided to temporarily halt redemptions and monthly distributions, and it will not allow investors to invest more.

…

Because MICs lend to borrowers who typically have a spottier credit history, their portfolios have a higher share of delinquencies, which is when a borrower misses a payment by at least 90 days.

Mortgage investment entities had a delinquency rate of 1.96 per cent in the third quarter of 2025, according to federal housing agency Canada Mortgage and Housing Corp. In comparison, chartered banks had a delinquency rate of 0.24 per cent in the same period.

CMHC said that, overall, mortgage investment entities have a higher exposure to Toronto, which may partially explain their worsening delinquency rate.

Mortgage Company did not disclose its delinquency rate in the investor notice or on its website.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.1210 % |

2,535.5 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.1210 % |

4,807.7 |

| Floater |

5.66 % |

5.86 % |

45,159 |

14.08 |

3 |

-0.1210 % |

2,770.7 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.1415 % |

3,657.8 |

| SplitShare |

4.76 % |

4.70 % |

51,075 |

2.81 |

5 |

-0.1415 % |

4,368.2 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.1415 % |

3,408.2 |

| Perpetual-Premium |

5.77 % |

5.30 % |

56,041 |

0.08 |

3 |

-0.1057 % |

3,046.1 |

| Perpetual-Discount |

5.63 % |

5.70 % |

53,829 |

14.32 |

30 |

-0.6967 % |

3,345.0 |

| FixedReset Disc |

5.64 % |

5.84 % |

101,095 |

13.91 |

24 |

-0.9913 % |

3,306.2 |

| Insurance Straight |

5.48 % |

5.57 % |

52,292 |

14.43 |

22 |

-0.1937 % |

3,290.4 |

| FloatingReset |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.9913 % |

3,933.1 |

| FixedReset Prem |

5.98 % |

4.53 % |

87,851 |

2.30 |

24 |

-0.2307 % |

2,655.4 |

| FixedReset Bank Non |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.9913 % |

3,379.6 |

| FixedReset Ins Non |

5.06 % |

5.27 % |

69,644 |

14.44 |

14 |

-0.0235 % |

3,265.6 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| ENB.PF.E |

FixedReset Disc |

-2.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.34

Evaluated at bid price : 23.00

Bid-YTW : 6.17 % |

| IFC.PR.M |

Perpetual-Discount |

-1.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 24.27

Evaluated at bid price : 24.65

Bid-YTW : 5.64 % |

| ENB.PR.J |

FixedReset Disc |

-1.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.95

Evaluated at bid price : 23.89

Bid-YTW : 5.99 % |

| ENB.PR.H |

FixedReset Disc |

-1.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.86

Evaluated at bid price : 23.56

Bid-YTW : 5.68 % |

| PWF.PR.Z |

Perpetual-Discount |

-1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.33

Evaluated at bid price : 22.60

Bid-YTW : 5.74 % |

| CU.PR.J |

Perpetual-Discount |

-1.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 21.13

Evaluated at bid price : 21.13

Bid-YTW : 5.64 % |

| BN.PR.N |

Perpetual-Discount |

-1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 20.57

Evaluated at bid price : 20.57

Bid-YTW : 5.86 % |

| PWF.PR.F |

Perpetual-Discount |

-1.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.90

Evaluated at bid price : 23.17

Bid-YTW : 5.71 % |

| PWF.PR.S |

Perpetual-Discount |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 21.36

Evaluated at bid price : 21.36

Bid-YTW : 5.67 % |

| POW.PR.B |

Perpetual-Discount |

-1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 23.57

Evaluated at bid price : 23.84

Bid-YTW : 5.67 % |

| POW.PR.D |

Perpetual-Discount |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.19

Evaluated at bid price : 22.47

Bid-YTW : 5.62 % |

| PWF.PR.L |

Perpetual-Discount |

-1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.18

Evaluated at bid price : 22.46

Bid-YTW : 5.72 % |

| GWO.PR.S |

Insurance Straight |

-1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 23.16

Evaluated at bid price : 23.46

Bid-YTW : 5.66 % |

| CU.PR.D |

Perpetual-Discount |

1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 21.67

Evaluated at bid price : 21.92

Bid-YTW : 5.59 % |

| GWO.PR.H |

Insurance Straight |

1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 21.65

Evaluated at bid price : 21.90

Bid-YTW : 5.61 % |

| MFC.PR.K |

FixedReset Ins Non |

1.35 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2028-09-19

Maturity Price : 25.00

Evaluated at bid price : 26.30

Bid-YTW : 4.46 % |

| ENB.PR.A |

Perpetual-Discount |

1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 24.50

Evaluated at bid price : 24.75

Bid-YTW : 5.56 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BN.PF.I |

FixedReset Prem |

198,900 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2027-03-31

Maturity Price : 25.00

Evaluated at bid price : 25.45

Bid-YTW : 4.08 % |

| CU.PR.H |

Perpetual-Discount |

70,000 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 23.60

Evaluated at bid price : 23.87

Bid-YTW : 5.50 % |

| MFC.PR.L |

FixedReset Ins Non |

50,200 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 23.52

Evaluated at bid price : 25.46

Bid-YTW : 5.26 % |

| POW.PR.D |

Perpetual-Discount |

49,200 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.19

Evaluated at bid price : 22.47

Bid-YTW : 5.62 % |

| FTS.PR.M |

FixedReset Prem |

48,570 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2029-12-01

Maturity Price : 25.00

Evaluated at bid price : 25.21

Bid-YTW : 5.18 % |

| CU.PR.C |

FixedReset Disc |

28,156 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2027-06-01

Maturity Price : 25.00

Evaluated at bid price : 25.00

Bid-YTW : 4.99 % |

| There were 11 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. |

| Issue |

Index |

Quote Data and Yield Notes |

| ENB.PF.E |

FixedReset Disc |

Quote: 23.00 – 23.60

Spot Rate : 0.6000

Average : 0.3727

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.34

Evaluated at bid price : 23.00

Bid-YTW : 6.17 % |

| GWO.PR.I |

Insurance Straight |

Quote: 20.85 – 21.55

Spot Rate : 0.7000

Average : 0.4769

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 20.85

Evaluated at bid price : 20.85

Bid-YTW : 5.48 % |

| ENB.PR.H |

FixedReset Disc |

Quote: 23.56 – 24.13

Spot Rate : 0.5700

Average : 0.3643

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.86

Evaluated at bid price : 23.56

Bid-YTW : 5.68 % |

| ENB.PR.P |

FixedReset Disc |

Quote: 24.11 – 24.67

Spot Rate : 0.5600

Average : 0.3612

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 23.06

Evaluated at bid price : 24.11

Bid-YTW : 5.85 % |

| BN.PR.T |

FixedReset Disc |

Quote: 22.10 – 23.15

Spot Rate : 1.0500

Average : 0.8567

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 21.68

Evaluated at bid price : 22.10

Bid-YTW : 6.09 % |

| ENB.PR.B |

FixedReset Disc |

Quote: 22.78 – 23.35

Spot Rate : 0.5700

Average : 0.3932

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-05-15

Maturity Price : 22.11

Evaluated at bid price : 22.78

Bid-YTW : 6.02 % |