| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8937 % | 1,623.9 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8937 % | 2,966.5 |

| Floater | 4.73 % | 4.74 % | 62,111 | 15.97 | 3 | -0.8937 % | 1,709.6 |

| OpRet | 4.87 % | 1.35 % | 38,638 | 0.08 | 1 | -0.1191 % | 2,832.4 |

| SplitShare | 4.89 % | 4.99 % | 86,188 | 4.63 | 7 | -0.0409 % | 3,334.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0409 % | 2,601.8 |

| Perpetual-Premium | 5.60 % | -10.42 % | 78,114 | 0.09 | 9 | 0.0478 % | 2,634.5 |

| Perpetual-Discount | 5.39 % | 5.45 % | 103,803 | 14.68 | 28 | -0.0936 % | 2,726.0 |

| FixedReset | 5.24 % | 4.61 % | 154,680 | 7.32 | 88 | -0.7897 % | 1,942.6 |

| Deemed-Retractible | 5.16 % | 5.40 % | 122,550 | 4.91 | 33 | -0.3079 % | 2,682.1 |

| FloatingReset | 3.13 % | 5.09 % | 28,067 | 5.18 | 18 | -0.2027 % | 2,090.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

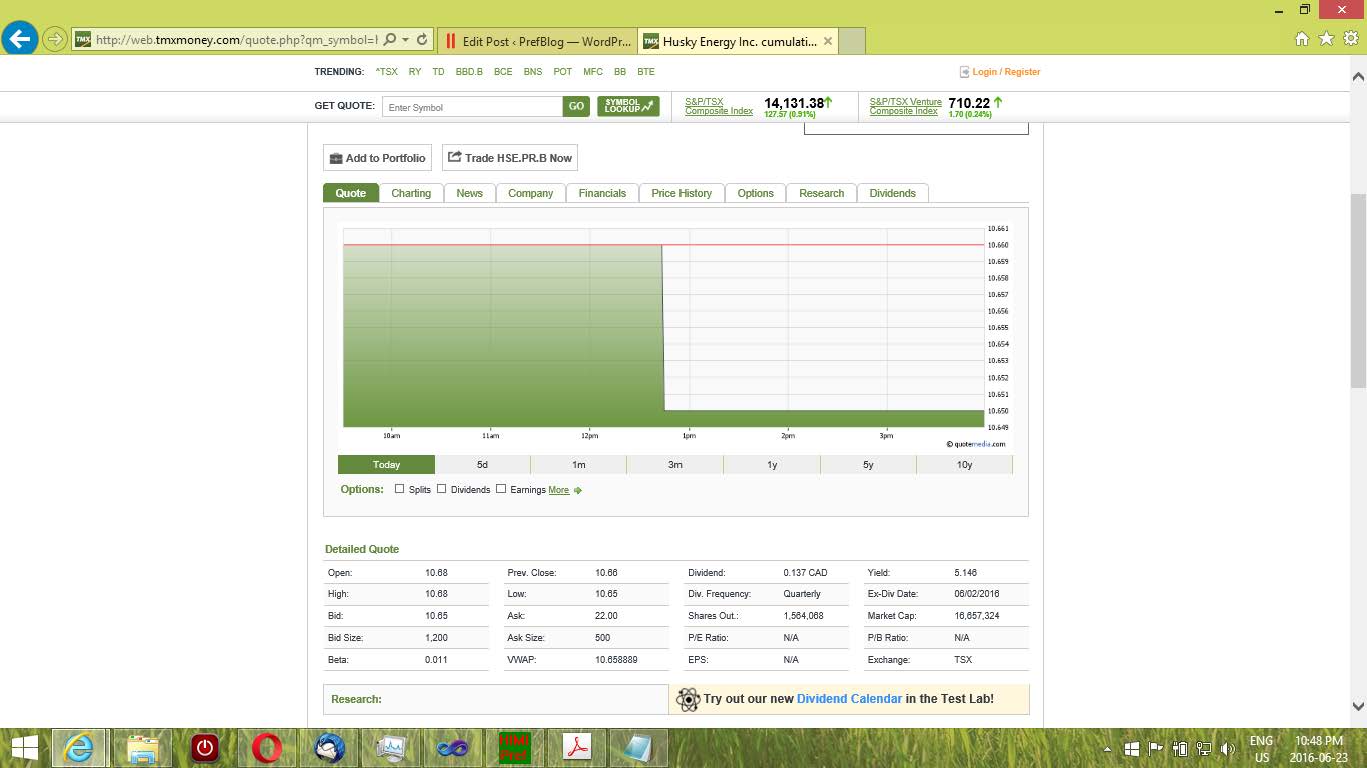

| HSE.PR.B | FloatingReset | -4.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 10.15 Evaluated at bid price : 10.15 Bid-YTW : 5.43 % |

| TRP.PR.C | FixedReset | -2.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 11.65 Evaluated at bid price : 11.65 Bid-YTW : 4.68 % |

| HSE.PR.E | FixedReset | -2.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 5.75 % |

| SLF.PR.H | FixedReset | -2.67 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.31 Bid-YTW : 9.46 % |

| HSE.PR.G | FixedReset | -2.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.47 Evaluated at bid price : 18.47 Bid-YTW : 5.74 % |

| SLF.PR.G | FixedReset | -2.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.00 Bid-YTW : 9.88 % |

| MFC.PR.L | FixedReset | -2.42 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.31 Bid-YTW : 8.33 % |

| MFC.PR.K | FixedReset | -2.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.79 Bid-YTW : 8.64 % |

| SLF.PR.I | FixedReset | -2.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.48 Bid-YTW : 8.39 % |

| MFC.PR.N | FixedReset | -2.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.00 Bid-YTW : 7.93 % |

| MFC.PR.M | FixedReset | -2.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.10 Bid-YTW : 7.91 % |

| TRP.PR.B | FixedReset | -2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 11.05 Evaluated at bid price : 11.05 Bid-YTW : 4.35 % |

| MFC.PR.G | FixedReset | -2.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.49 Bid-YTW : 7.77 % |

| FTS.PR.G | FixedReset | -2.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 16.94 Evaluated at bid price : 16.94 Bid-YTW : 4.22 % |

| FTS.PR.M | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.40 % |

| HSE.PR.A | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 11.02 Evaluated at bid price : 11.02 Bid-YTW : 5.32 % |

| NA.PR.S | FixedReset | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 17.43 Evaluated at bid price : 17.43 Bid-YTW : 4.58 % |

| FTS.PR.J | Perpetual-Discount | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 21.93 Evaluated at bid price : 22.29 Bid-YTW : 5.37 % |

| TRP.PR.F | FloatingReset | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 12.95 Evaluated at bid price : 12.95 Bid-YTW : 4.62 % |

| MFC.PR.F | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.46 Bid-YTW : 10.40 % |

| MFC.PR.J | FixedReset | -1.82 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.37 Bid-YTW : 7.69 % |

| FTS.PR.K | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 17.09 Evaluated at bid price : 17.09 Bid-YTW : 4.15 % |

| MFC.PR.I | FixedReset | -1.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.33 Bid-YTW : 7.21 % |

| FTS.PR.F | Perpetual-Discount | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 22.70 Evaluated at bid price : 22.94 Bid-YTW : 5.39 % |

| CM.PR.O | FixedReset | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.25 % |

| HSE.PR.C | FixedReset | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 16.91 Evaluated at bid price : 16.91 Bid-YTW : 5.77 % |

| SLF.PR.B | Deemed-Retractible | -1.71 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.41 Bid-YTW : 6.42 % |

| CM.PR.Q | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.97 Evaluated at bid price : 18.97 Bid-YTW : 4.50 % |

| CU.PR.C | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 16.56 Evaluated at bid price : 16.56 Bid-YTW : 4.60 % |

| SLF.PR.C | Deemed-Retractible | -1.62 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.71 Bid-YTW : 7.19 % |

| SLF.PR.A | Deemed-Retractible | -1.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.25 Bid-YTW : 6.47 % |

| IAG.PR.G | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.10 Bid-YTW : 8.07 % |

| SLF.PR.D | Deemed-Retractible | -1.52 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.70 Bid-YTW : 7.20 % |

| CM.PR.P | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 4.24 % |

| BMO.PR.S | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.18 Evaluated at bid price : 18.18 Bid-YTW : 4.27 % |

| IFC.PR.C | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.16 Bid-YTW : 8.48 % |

| SLF.PR.E | Deemed-Retractible | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.96 Bid-YTW : 7.07 % |

| IFC.PR.A | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.50 Bid-YTW : 10.27 % |

| GWO.PR.I | Deemed-Retractible | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.20 Bid-YTW : 6.91 % |

| BMO.PR.T | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 17.90 Evaluated at bid price : 17.90 Bid-YTW : 4.22 % |

| BMO.PR.W | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 17.82 Evaluated at bid price : 17.82 Bid-YTW : 4.21 % |

| TD.PF.B | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 4.25 % |

| BAM.PR.T | FixedReset | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-06-27 Maturity Price : 14.82 Evaluated at bid price : 14.82 Bid-YTW : 5.03 % |

| SLF.PR.J | FloatingReset | 1.92 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.75 Bid-YTW : 10.77 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.Q | FixedReset | 120,856 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 26.31 Bid-YTW : 4.44 % |

| BNS.PR.M | Deemed-Retractible | 115,308 | YTW SCENARIO Maturity Type : Call Maturity Date : 2016-07-27 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 0.87 % |

| TRP.PR.J | FixedReset | 105,100 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.88 Bid-YTW : 4.81 % |

| NA.PR.A | FixedReset | 65,236 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-15 Maturity Price : 25.00 Evaluated at bid price : 25.63 Bid-YTW : 4.92 % |

| CCS.PR.C | Deemed-Retractible | 25,610 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.11 Bid-YTW : 6.18 % |

| MFC.PR.G | FixedReset | 18,960 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.49 Bid-YTW : 7.77 % |

| There were 16 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| FTS.PR.I | FloatingReset | Quote: 11.90 – 12.89 Spot Rate : 0.9900 Average : 0.8204 YTW SCENARIO |

| TRP.PR.F | FloatingReset | Quote: 12.95 – 13.50 Spot Rate : 0.5500 Average : 0.4205 YTW SCENARIO |

| PWF.PR.Q | FloatingReset | Quote: 11.50 – 13.00 Spot Rate : 1.5000 Average : 1.3751 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 18.10 – 18.38 Spot Rate : 0.2800 Average : 0.1774 YTW SCENARIO |

| PVS.PR.D | SplitShare | Quote: 23.58 – 23.98 Spot Rate : 0.4000 Average : 0.3063 YTW SCENARIO |

| IFC.PR.A | FixedReset | Quote: 14.50 – 14.80 Spot Rate : 0.3000 Average : 0.2064 YTW SCENARIO |