In recognition of the fact that investors get so much regulatory paper from their brokers that they don’t read it, the Canadian Securities Administrators are requiring the delivery of more paper. I’ll bet a nickel that every year the “Fund Facts” gets enlarged ‘because Granny didn’t know she could lose money if so-and-so went bankrupt’, until about twenty years from now, when new “Fund Briefer Facts” becomes mandated and then lucky buyers get even more mail to throw away without reading. Still, it keeps the regulators busy and Proactively Working In The Best Interest Of Investors, and that’s what counts, right?

Julia Dickson gave a speech in Vancouver lauding financial oligopolies:

One lesson everyone is relearning is the importance of proper consolidated oversight and supervision of financial groups, especially systemically important financial groups. This lesson has arisen in the context of AIG, where the parent holding company was regulated, but not to the extent required of a systemically important group of its size.

Canada is relatively well placed in this regard as there is already considerable consolidated oversight and supervision of the Canadian financial sector. The large securities firms are owned by the big banks, which OSFI oversees, meaning that securities firms must meet the same prudential standards as their parent bank. As well, the general structural model for large financial services groups is that they are headed by a regulated financial institution, which is overseen by OSFI, versus the holding company structure commonly seen in other jurisdictions.

Having a regulated Canadian financial institution at the top of such organizations enhances our ability to understand the risks facing the conglomerate. Further, given OSFI’s regulatory authority at the top level, we can intervene and require action to be taken, no matter where in the group we may have identified potential problems.

As a regulator, you need to have knowledge of the financial status and risk profile of all affiliates within a financial group. Indeed, as demonstrated by the AIG case, small parts of big companies can be hugely problematic.

She did not go so far as to say she wished to see an elimination of the holding company structure for insurers, but she is clearly headed in that direction. It is very disappointing to see such regulatory hostility to the concept of a layered financial system: banks – securities dealers – hedge funds, that can work quite well provided there are clear lines between the layers.

Plain vanilla for everyone! That’s the Canadian way!

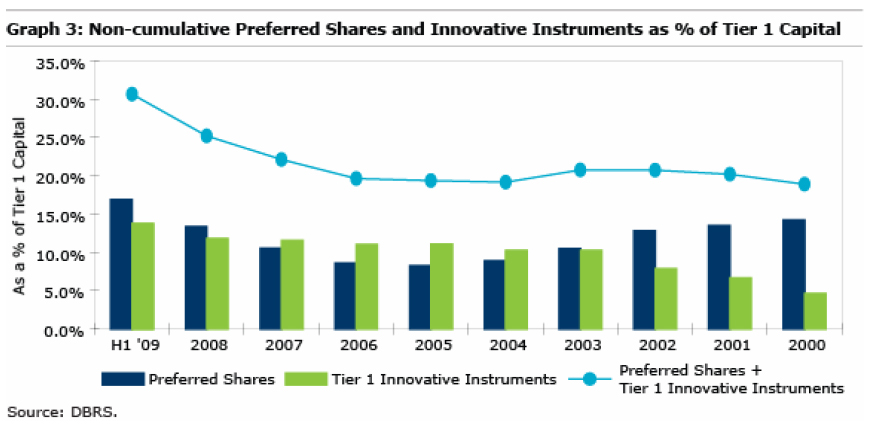

C-EBS has published a consultation paper on implementation of hybrid capital guidelines.

Christopher Whalen, head of International Risk Analytics, had some home-truths for the Senate today:

Trading in credit-default swaps should be banned, Christopher Whalen, managing director of Institutional Risk Analytics in Hawthorne, California, said in prepared testimony for today’s Senate hearing. Regulators are too cozy with the banks in the market to be counted on to make changes, he said.

“The views of the existing financial regulatory agencies, and particularly the Federal Reserve Board and Treasury, should get no consideration from the committee since the view of these agencies are largely duplicative of the views of JPMorgan Chase & Co. and the large OTC dealers,” he said in the remarks.

I can’t find the full text of his testimony, but they will probably be posted soon.

Equities got hit today after the World Bank warned of lower future growth. The only way out of this mess is to hire more regulators:

Global Development Finance 2009: Charting a Global Recovery, warns that the world is entering an era of slower growth that will require tighter and more effective oversight of the financial system.

Perhaps in sympathy, PerpetualDiscounts were off somewhat today; while FixedResets were also down the loss of the latter was negligible. Volume continued high.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8682 % | 1,215.1 |

| FixedFloater | 7.09 % | 5.54 % | 34,558 | 16.26 | 1 | -1.0968 % | 2,126.6 |

| Floater | 3.13 % | 3.44 % | 78,268 | 18.66 | 3 | -0.8682 % | 1,518.0 |

| OpRet | 4.97 % | 3.65 % | 134,539 | 0.10 | 14 | 0.0141 % | 2,193.6 |

| SplitShare | 5.78 % | 6.44 % | 64,042 | 4.22 | 3 | 0.2890 % | 1,886.3 |

| Interest-Bearing | 5.98 % | 7.46 % | 22,779 | 0.51 | 1 | -0.1988 % | 1,995.2 |

| Perpetual-Premium | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3465 % | 1,734.9 |

| Perpetual-Discount | 6.34 % | 6.36 % | 165,003 | 13.40 | 71 | -0.3465 % | 1,597.8 |

| FixedReset | 5.67 % | 4.81 % | 526,037 | 4.35 | 40 | -0.0276 % | 2,011.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PR.K | Floater | -5.34 % | Not a particularly meaningful decline, since only 3,500 shares traded and this was in a range of 11.50-75; the closing quote was 11.00-49, 1×5 after a trade with eight minutes left in the day took out the bid. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 3.58 % |

| MFC.PR.B | Perpetual-Discount | -2.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 18.43 Evaluated at bid price : 18.43 Bid-YTW : 6.36 % |

| BAM.PR.J | OpRet | -2.25 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2018-03-30 Maturity Price : 25.00 Evaluated at bid price : 21.70 Bid-YTW : 7.51 % |

| IAG.PR.C | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-01-30 Maturity Price : 25.00 Evaluated at bid price : 25.57 Bid-YTW : 5.64 % |

| RY.PR.H | Perpetual-Discount | -1.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 23.34 Evaluated at bid price : 23.51 Bid-YTW : 6.08 % |

| SLF.PR.E | Perpetual-Discount | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 16.82 Evaluated at bid price : 16.82 Bid-YTW : 6.73 % |

| IGM.PR.A | OpRet | -1.44 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2009-07-30 Maturity Price : 26.00 Evaluated at bid price : 26.02 Bid-YTW : 3.65 % |

| RY.PR.A | Perpetual-Discount | -1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 6.18 % |

| CU.PR.A | Perpetual-Discount | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 23.31 Evaluated at bid price : 23.60 Bid-YTW : 6.20 % |

| POW.PR.D | Perpetual-Discount | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 19.17 Evaluated at bid price : 19.17 Bid-YTW : 6.54 % |

| SLF.PR.D | Perpetual-Discount | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 16.69 Evaluated at bid price : 16.69 Bid-YTW : 6.71 % |

| CL.PR.B | Perpetual-Discount | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 23.00 Evaluated at bid price : 23.27 Bid-YTW : 6.75 % |

| BAM.PR.G | FixedFloater | -1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 25.00 Evaluated at bid price : 15.33 Bid-YTW : 5.54 % |

| RY.PR.F | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 18.07 Evaluated at bid price : 18.07 Bid-YTW : 6.24 % |

| BMO.PR.J | Perpetual-Discount | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 18.42 Evaluated at bid price : 18.42 Bid-YTW : 6.19 % |

| CM.PR.H | Perpetual-Discount | -1.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 18.81 Evaluated at bid price : 18.81 Bid-YTW : 6.50 % |

| BAM.PR.I | OpRet | 1.23 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2013-12-30 Maturity Price : 25.00 Evaluated at bid price : 24.61 Bid-YTW : 5.91 % |

| BNA.PR.C | SplitShare | 1.27 % | Asset coverage of 1.9-:1 as of May 31 according to the company. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 15.95 Bid-YTW : 10.54 % |

| TRI.PR.B | Floater | 1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 15.25 Evaluated at bid price : 15.25 Bid-YTW : 2.57 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.P | FixedReset | 282,931 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 23.13 Evaluated at bid price : 25.04 Bid-YTW : 5.09 % |

| MFC.PR.E | FixedReset | 86,160 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-19 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 5.50 % |

| TD.PR.O | Perpetual-Discount | 79,131 | National crossed two blocks at 20.04, of 30,000 and 24,000 shares. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 19.96 Evaluated at bid price : 19.96 Bid-YTW : 6.19 % |

| BAM.PR.P | FixedReset | 63,575 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-30 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 6.87 % |

| BMO.PR.L | Perpetual-Discount | 54,550 | Nesbitt crossed 30,000 at 23.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 23.62 Evaluated at bid price : 23.80 Bid-YTW : 6.16 % |

| CM.PR.I | Perpetual-Discount | 51,356 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-06-22 Maturity Price : 18.38 Evaluated at bid price : 18.38 Bid-YTW : 6.51 % |

| There were 43 other index-included issues trading in excess of 10,000 shares. | |||