Core consumer prices rose 2.4 percent in March from a year earlier, the most since December 2008, and February retail sales climbed 1.7 percent, Statistics Canada said Friday from Ottawa. Price gains showed up in everything from text messages to fresh meat to cars.

Consumer spending fueled by low interest rates has been among the biggest sources of growth since a recession that started at the end of 2008, with manufacturing and business investment curtailed by weak global demand. Today’s retail figures showed gains in every major category, from a 5.6 percent increase at general merchandise stores to 0.9 percent at automobile dealers.

…

Canada’s currency climbed as much as 0.8 percent to C$1.2088 per U.S. dollar, the strongest since Jan. 21. It was down 0.4 percent at 1:36 p.m. in Toronto. Yields on benchmark government two-year bonds rose 5 basis points to 0.63 percent, the third straight increase.

We are told that it is it is hard to find a virtuous woman? for her price is far above rubies [sic]. Sadly, we are never given the salacious details of Ruby’s pricing, but modern market science allows us to infer that a little bit of liquidity, if you know what I mean, helps a lot:

For colored stones, prices often increase with supply as jewelers acquire enough stock to justify marketing the gems to customers. Take regular emeralds: their value has appreciated 1,000 percent in five years as Harebottle’s Gemfields Plc and peers expanded mines, while marketing campaigns fronted by Hollywood star Mila Kunis gave demand a boost.

Now Harebottle wants to bring the same game to rubies. Gemfields’ Montepuez in Mozambique, estimated to contain as much as 40 percent of the world’s known supply of the deep-red stones, could triple output from the 8 million carats targeted for this year, according to the executive.

The potential rewards are compelling. At its first Singapore auction last December, Gemfields sold high-quality rubies for an average $689 a carat, dwarfing the $66 a carat for comparable emeralds. Production growth is underpinned by rising demand in China, where the color red symbolizes prosperity, health and wealth, making rubies an auspicious investment.

Assiduous Reader HS sends me a couple of links (which is more than most of you have ever done). The first is a mainstream report on ENB preferreds and their credit woes:

Over the past two years, Enbridge has come to the market on eight separate occasions with offerings of rate reset preferred shares. The offerings featured a variety of currencies (US$ or C$), coupons (4 per cent or 4.40 per cent) and spreads above five-year Canada bonds — the yield that serves as the base rate for the prefs. The last issue for $200 million was completed last September.

…

The Canadian restructuring was viewed as positive for Enbridge’s common shareholders – but not its debt holders. In other words, the drop down in assets wasn’t credit-friendly. Indeed, the pref share ratings are under review.The restructuring at Enbridge occurred before the preferred share market was hit by the fallout from an unexpected 25 basis points cut in the bank rate made in January.

He also sends a link for a Schwab piece titled The Bond Investor’s Trilemma: Positioning for a Fed Rate Hike. I usually don’t pass brokerage analysis along – waste of time! – but brokerage work is useful for data and charts. In this case, there are three good charts:

Click for Big

It is interesting that the market is so much more gloomy than the Fed.

Click for Big

Schwab comments:

Market-based measures of inflation expectations have been edging lower lately, along with actual inflation readings.

Click for Big

I’m almost getting tired of beating the drum on corporate bond liquidity … but one more time won’t hurt! Schwab comments:

One outgrowth of the financial crisis and its aftermath has been reduced liquidity in the bond market. Since the financial crisis, many banks have reduced their risk-taking and are not making markets in bonds or holding as many bonds as in the past. Consequently, there are fewer buyers and sellers in the market and if you want to sell a bond, you may have a difficult time finding a buyer at a reasonable price, especially during periods of market volatility.

Rob Carrick wrote a fairly lengthy piece in the Globe titled What investors should know about the recent plunge in preferred shares:

But rate resets have been trouble.

Investors clearly bought them with the expectation that the reset would help them tap into a higher yield down the line. Today, however, some of these shares are headed to a reset at a time when rates are at unexpectedly low levels. It all comes down to this: Five-year Canada bonds had a yield around 0.75 per cent at midweek, compared with about 3 per cent five years ago.

You can see the result of this rate decline in Fortis Inc.’s Series H five-year fixed rate reset shares (FTS.PR.H). They currently pay a dividend that yielded 4.25 per cent when issued at a value of $25 per share. The dividend on these shares will be reset on June 1 to produce a dividend yield of 1.45 percentage points above the five-year Canada bond yield. Based on recent bond yields, these shares would, after reset, have a yield of about 2.2 per cent based on the $25 issue price. In dollar terms, the dividend would fall to 55 cents from the current $1.06.

The shares traded this week in the $15.25 range, which meant their yield based on the current $1.06 dividend was 6.9 per cent. Mr. Nagel calculates their yield after the reset at about 3.6 per cent based on this week’s share price and a dividend of 55 cents. No matter how you look at it, investors are going to get less in dividends after the reset. Now, what should they do about it?

…

Mr. Nagel lays out the decision on whether to choose the floating rate option like this: Do you want a lower yield now in exchange for the opportunity for increases if interest rates rise over the next five years, or would you prefer to lock in 3.6 per cent? The floating rate option could end up being the most rewarding, he argues. If rates do go up in the five years to come, you’ll benefit in the near term rather than having to wait until the next reset date. With floating rate shares, adjustments are made every three months.Another thought from Mr. Nagel is to sell all or part of your rate reset preferred shares and put the money into straight preferreds, which pay a fixed dividend. Straight preferreds have benefited a little bit from lower rates – Desjardins data show they were up 2.5 per cent as a group for the year to April 10, while the preferred share universe was down 8 per cent.

Still another possibility would be to switch from preferred shares to dividend-paying common shares. They’ve had a rough go lately as well, but that’s a matter for a future column.

It appears that Mr. Nagel’s thinking has evolved since his exhortations in January, 2010:

On the other hand, if the bond yield is low and it looks like the shares will be reset, the best bet — available in the vast majority of cases — is to convert to floating rate preferred shares, which are usually pegged to the Government of Canada three-month treasury bills plus the spread.

But now market timing and return chasing is the recommended strategy. Market timing achieves the main objective of the investment industry, which is the generation of excessive commissions.

Dividend Growth Split Corp., proud issuer of DGS.PR.A, has been confirmed at Pfd-3 by DBRS:

DBRS Limited (DBRS) has today confirmed the Preferred Shares rating of Dividend Growth Split Corp. (the Company) at Pfd-3. In December 2007, the Company issued approximately 1.5 million Preferred Shares (at $10 each) and an equal number of Class A Shares (at $15 each). Subsequent to the initial public offering, the Company has completed six follow-on offerings. The total number of Preferred Shares and Class A Shares outstanding currently stands at approximately 18.7 million shares each. The scheduled redemption date for both classes of shares issued is November 28, 2019.

…

The net asset value (NAV) of the Company has been volatile since the last rating confirmation in April 2014. As of April 9, 2015, the downside protection available to the Preferred Shares is approximately 45.2%, down from 46.7% on April 3, 2014. The dividend coverage ratio is approximately 0.99 times. The Pfd-3 rating of the Preferred Shares is based primarily on the downside protection available and the additional protection provided by an asset coverage test, which does not permit any distributions to holders of the Class A Shares if the NAV of the Company falls below $15.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 4bp, FixedResets down 38bp and DeemedRetractibles off 26bp. The Performance Highlights table is predictably dominated by losing FixedResets, but the recent high level of volatility manifests itself in a large number of winners as well – notably a few Enbridge issues. Volume was super-duper very extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

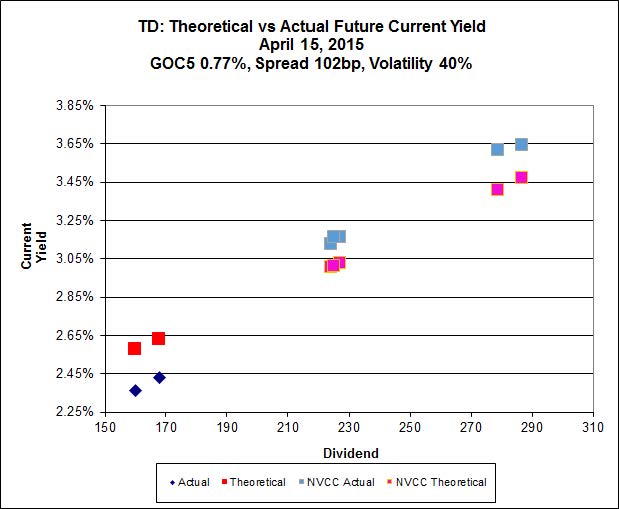

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 22.68 to be $1.85 rich, while TRP.PR.B, resetting 2015-6-30 at +128, is $0.88 cheap at its bid price of 13.68.

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Losses by the lower-spread issues have resulted in a sharp decrease in Implied Volatility, which was 17% yesterday and 19% on March 31.

Most expensive is MFC.PR.I, resetting at +286 on 2017-9-19, bid at 25.15 to be $0.47 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.15 to be $0.46 cheap.

Click for Big

This fit is actually quite good.

The cheapest issue relative to its peers is BAM.PF.A, resetting at +290bp on 2016-9-30, bid at 23.13 to be $0.24 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 23.51 and appears to be $0.51 rich.

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 15.40, looks $1.00 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 21.05 and is $0.35 rich.

Click for Big

Investment-grade pairs (including TRP.PR.A / TRP.PR.F, which is no longer an outlier) now predict an average over the next five years of about 0.28%. The DC.PR.B / DC.PR.D pair is still off the charts and now predicts an average bill rate over the next 4 3/4 years of -1.57%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8391 % | 2,170.8 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.8391 % | 3,795.5 |

| Floater | 3.34 % | 3.53 % | 58,020 | 18.48 | 4 | -1.8391 % | 2,307.7 |

| OpRet | 4.43 % | -2.25 % | 39,277 | 0.12 | 2 | 0.0394 % | 2,763.2 |

| SplitShare | 4.57 % | 4.57 % | 59,598 | 3.41 | 3 | 0.1604 % | 3,225.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0394 % | 2,526.6 |

| Perpetual-Premium | 5.34 % | 1.29 % | 65,141 | 0.08 | 25 | -0.1062 % | 2,513.4 |

| Perpetual-Discount | 5.15 % | 5.10 % | 144,513 | 14.97 | 9 | 0.0380 % | 2,771.9 |

| FixedReset | 4.63 % | 3.83 % | 278,207 | 16.26 | 85 | -0.3848 % | 2,307.6 |

| Deemed-Retractible | 4.91 % | 3.40 % | 109,562 | 0.59 | 36 | -0.2554 % | 2,647.1 |

| FloatingReset | 2.54 % | 2.98 % | 77,994 | 6.25 | 8 | -0.0856 % | 2,342.0 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TD.PF.B | FixedReset | -4.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.21 Evaluated at bid price : 22.82 Bid-YTW : 3.48 % |

| SLF.PR.H | FixedReset | -4.36 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.50 Bid-YTW : 6.18 % |

| TD.PF.C | FixedReset | -3.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.17 Evaluated at bid price : 22.80 Bid-YTW : 3.47 % |

| MFC.PR.F | FixedReset | -3.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.66 Bid-YTW : 7.37 % |

| SLF.PR.I | FixedReset | -3.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.03 Bid-YTW : 4.17 % |

| BAM.PR.B | Floater | -3.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 14.23 Evaluated at bid price : 14.23 Bid-YTW : 3.53 % |

| IAG.PR.G | FixedReset | -3.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.25 Bid-YTW : 4.21 % |

| BAM.PR.C | Floater | -3.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 14.19 Evaluated at bid price : 14.19 Bid-YTW : 3.54 % |

| CIU.PR.C | FixedReset | -3.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 3.57 % |

| MFC.PR.N | FixedReset | -2.59 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.20 Bid-YTW : 4.99 % |

| MFC.PR.J | FixedReset | -2.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.77 Bid-YTW : 4.27 % |

| BAM.PF.E | FixedReset | -2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 21.12 Evaluated at bid price : 21.12 Bid-YTW : 4.30 % |

| IFC.PR.A | FixedReset | -1.79 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.16 Bid-YTW : 6.32 % |

| TD.PF.A | FixedReset | -1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.65 Evaluated at bid price : 23.65 Bid-YTW : 3.32 % |

| NA.PR.W | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.74 Evaluated at bid price : 23.90 Bid-YTW : 3.28 % |

| NA.PR.S | FixedReset | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 23.02 Evaluated at bid price : 24.40 Bid-YTW : 3.32 % |

| MFC.PR.M | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.60 Bid-YTW : 4.84 % |

| BMO.PR.S | FixedReset | -1.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.91 Evaluated at bid price : 24.15 Bid-YTW : 3.34 % |

| PWF.PR.P | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 17.12 Evaluated at bid price : 17.12 Bid-YTW : 3.61 % |

| CM.PR.P | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.72 Evaluated at bid price : 23.85 Bid-YTW : 3.26 % |

| SLF.PR.D | Deemed-Retractible | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.24 Bid-YTW : 5.44 % |

| SLF.PR.C | Deemed-Retractible | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.25 Bid-YTW : 5.44 % |

| SLF.PR.E | Deemed-Retractible | -1.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.40 Bid-YTW : 5.41 % |

| BAM.PR.K | Floater | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 14.11 Evaluated at bid price : 14.11 Bid-YTW : 3.56 % |

| HSE.PR.C | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.56 Evaluated at bid price : 23.49 Bid-YTW : 4.28 % |

| FTS.PR.F | Perpetual-Premium | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 24.18 Evaluated at bid price : 24.46 Bid-YTW : 5.06 % |

| RY.PR.H | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.87 Evaluated at bid price : 24.10 Bid-YTW : 3.28 % |

| TRP.PR.E | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.11 Evaluated at bid price : 22.68 Bid-YTW : 3.69 % |

| SLF.PR.B | Deemed-Retractible | -1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.61 Bid-YTW : 5.06 % |

| RY.PR.Z | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.92 Evaluated at bid price : 24.16 Bid-YTW : 3.24 % |

| CM.PR.O | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 22.78 Evaluated at bid price : 23.90 Bid-YTW : 3.34 % |

| ENB.PR.F | FixedReset | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 18.86 Evaluated at bid price : 18.86 Bid-YTW : 4.58 % |

| MFC.PR.I | FixedReset | 1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.15 Bid-YTW : 3.83 % |

| ENB.PF.G | FixedReset | 1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 4.53 % |

| ENB.PF.C | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 20.37 Evaluated at bid price : 20.37 Bid-YTW : 4.57 % |

| TRP.PR.B | FixedReset | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 13.68 Evaluated at bid price : 13.68 Bid-YTW : 3.79 % |

| MFC.PR.K | FixedReset | 1.44 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.77 Bid-YTW : 5.06 % |

| TRP.PR.C | FixedReset | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 15.75 Evaluated at bid price : 15.75 Bid-YTW : 3.80 % |

| BAM.PR.R | FixedReset | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 19.39 Evaluated at bid price : 19.39 Bid-YTW : 4.18 % |

| ENB.PR.T | FixedReset | 1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 19.62 Evaluated at bid price : 19.62 Bid-YTW : 4.44 % |

| ENB.PR.N | FixedReset | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 19.90 Evaluated at bid price : 19.90 Bid-YTW : 4.51 % |

| ENB.PR.Y | FixedReset | 2.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 18.92 Evaluated at bid price : 18.92 Bid-YTW : 4.50 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.L | Perpetual-Premium | 257,257 | Scotia crossed 125,000 at 24.94. Nesbitt crossed 125,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 24.66 Evaluated at bid price : 24.90 Bid-YTW : 5.13 % |

| MFC.PR.G | FixedReset | 251,476 | TD crossed four blocks: 10,000 shares, 40,000 shares, 139,700 and 50,000, all at 25.00. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.92 Bid-YTW : 3.91 % |

| RY.PR.J | FixedReset | 231,776 | RBC crossed three blocks of 40,000 each, all at 24.95, and bought 13,500 from TD at the same price. Scotia crossed 50,000 at the same price again. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 23.13 Evaluated at bid price : 24.94 Bid-YTW : 3.46 % |

| POW.PR.A | Perpetual-Premium | 184,100 | Scotia crossed 59,300 at 25.35; Nesbitt crossed 60,000 at the same price; TD crossed 60,400 at the same price again. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-05-17 Maturity Price : 25.00 Evaluated at bid price : 25.33 Bid-YTW : -9.76 % |

| TD.PF.D | FixedReset | 136,215 | RBC bought 15,000 from TD at 24.70, then crossed 78,600 at 24.80. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 23.09 Evaluated at bid price : 24.85 Bid-YTW : 3.50 % |

| CM.PR.Q | FixedReset | 100,045 | Scotia crossed blocks of 40,000 and 45,900, both at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-04-17 Maturity Price : 23.06 Evaluated at bid price : 24.75 Bid-YTW : 3.52 % |

| There were 71 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| SLF.PR.I | FixedReset | Quote: 24.03 – 25.00 Spot Rate : 0.9700 Average : 0.5592 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 22.60 – 24.00 Spot Rate : 1.4000 Average : 1.0401 YTW SCENARIO |

| TRP.PR.E | FixedReset | Quote: 22.68 – 23.64 Spot Rate : 0.9600 Average : 0.6056 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 19.50 – 20.50 Spot Rate : 1.0000 Average : 0.6795 YTW SCENARIO |

| TD.PF.B | FixedReset | Quote: 22.82 – 23.55 Spot Rate : 0.7300 Average : 0.4616 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 24.25 – 24.97 Spot Rate : 0.7200 Average : 0.4870 YTW SCENARIO |