Bank of Montreal has announced (although not yet on their website):

it has closed its domestic public offering of Non-Cumulative 5-Year Rate Reset Class B Preferred Shares Series 38 (the “Preferred Shares Series 38”). The offering was underwritten on a bought deal basis by a syndicate of underwriters led by BMO Capital Markets. Bank of Montreal issued 24 million Preferred Shares Series 38 at a price of $25 per share to raise gross proceeds of $600 million.

The Preferred Shares Series 38 were issued under a prospectus supplement dated October 14, 2016, to the Bank’s short form base shelf prospectus dated April 13, 2016. Such shares will commence trading on the Toronto Stock Exchange today under the ticker symbol BMO.PR.B.

BMO.PR.B is a FixedReset, 4.85%+406, NVCC-compliant issue announced October 14. It will be tracked by HIMIPref™ and assigned to the FixedResets subindex.

The issue traded a staggering 4,330,078 shares in a range of 25.69-82 before closing at 25.69-70, 27×87. The volume ranks it sixth in my database (over 1-million records dating back to 1993-12-31), just behind NVA.PR.A (Nova Energy), which traded 4.4-million shares on 1997-3-24 (shortly after issue) and the highest single-issue daily volume since GWO.PR.E, which traded 5.3-million shares on 1999-3-18 (also shortly after issue). So, this is the highest single-issue daily volume so far this century.

Vital statistics are:

| BMO.PR.B | FixedReset | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.69 Bid-YTW : 4.29 % |

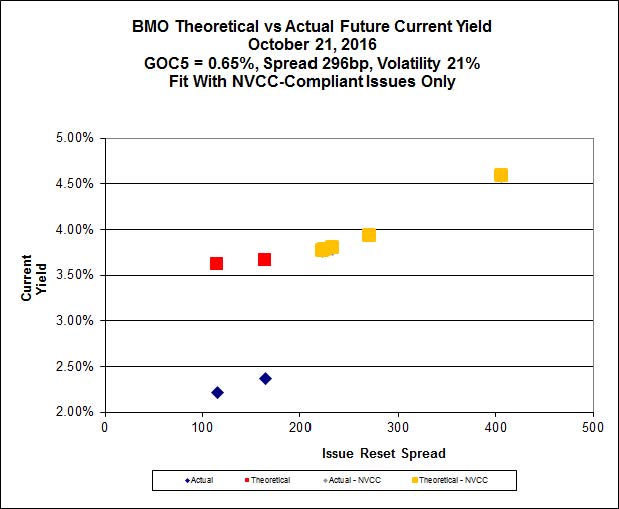

As has often been the case lately, Implied Volatility analysis results in a chart that can be interpreted in two ways:

Click for Big

The curve fits very well, with a very high Implied Volatility. If one takes the view that GOC-5 rates will increase dramatically over the next few years, the low-spread, low-price issues will be preferred (as this will lead to capital gains on these issues, but not the new one since the call provision caps the expected price); if one takes the view that the current GOC yield curve represents the new normal, then the new issue will be preferred (as one will then expect Implied Volatility to decrease, flattening the fitted curve, resulting in capital losses for the low-spread issues).