Interesting news from Peru today:

IShares, the world’s biggest provider of exchange-traded funds, reached an agreement with Peru’s pension funds that will increase the assets of the first Peruvian exchange traded fund in the U.S., according to Gonzalo Presa, a pension fund manager at Lima-based AFP Horizonte.

The Peruvian pension funds, known as AFPs, will swap shares of local companies in exchange for shares in the iShares MSCI All Peru Capped Index Fund, said Presa. BlackRock Inc. agreed to buy Barclays Plc’s global fund unit, including iShares, for $13.5 billion in June.

“We’ll give Barclays shares to build up this ETF,” Presa, who helps manage $3.4 billion as head of local equities at AFP Horizonte, said in a phone interview. “The idea is to issue $300 million in new shares in two, three weeks.”

Presa said it would be “very difficult” for Barclays to acquire the shares in the local market because of the lack of liquidity.

There’s no information given as to whether the pension funds got a sweetheart deal on fees.

I hadn’t known this in advance, but to my astonishment there was no early close of the bond markets today:

“SIFMA’s Board of Directors and membership reassessed the early close policy, recognizing that additional access to the liquidity provided by our members would benefit all market participants. The interconnected, global nature of the fixed income markets and the significant–and nearly round the clock–access to liquidity that many members provide would be enhanced by this change. Since shortened trading days may limit the liquidity window and create possible market risks which could be mitigated with a full functioning fixed income market on days when liquidity could be normal, we have determined eliminating some of the early closes is a better solution,” said Randy Snook, executive vice president at SIFMA. “This step will allow firms of all sizes around the globe to have access to fixed income liquidity on an almost continuous basis on most trading days of the year.”

Early close recommendations will be eliminated for the following holidays:

· Friday before Martin Luther King, Jr. Day

· Friday before President’s Day

· Day before Independence Day

· Friday before Labor Day

· Day before Columbus Day

· Day before Veterans Day

· Day before Thanksgiving

I’ve heard a rumour that this is TARP-related, which may well be true, but I’m glad of it anyway. Ever since I got into this business, I’ve been amazed that the highest paid profession on earth has had a half-day in advance of long weekends. All the B-School Babies will be whining about having to put in a full day’s work, poor things.

The SEC may be preparing a short-selling cosmetic makeover:

Given the climate in Washington, as well as the running suspicion of Wall Street, new rules seem inevitable, analysts say. Mary L. Schapiro, chairwoman of the S.E.C., has said that considering new rules restricting short-selling is a priority. Members of Congress like Barney Frank, the Massachusetts Democrat who heads the House financial services committee, are calling for quick action.

For the moment, the most likely outcome may be for the S.E.C. to reinstate a rule that the commission itself abolished with a unanimous vote in 2007, under its previous chairman, Christopher S. Cox. Known as the uptick rule, it would bar investors from shorting a stock until its price ticks at least a penny above its previous trading price.

But current and former S.E.C. staff members appear to doubt that reinstating the uptick rule would have much of an effect on trading. Some say the change would be merely cosmetic.

…

Sally Miller, a spokesman for the A.B.A., said the member banks thought there was clear link between the market turmoil and the rule change. “All of a sudden subsequent to 2007 they can see all their stocks going haywire,” Ms. Miller said. “It’s cause and effect.”

I wonder what Ms. Miller actually said, in context. She surely can’t be claiming that the most important determinant of bank equity price volatility in the 2007-09 period was the removal of the uptick rule!

Still and all, I wonder what BIS thinks of it. Their annual report contains an argument in favour of short sales as a bubble-controller.

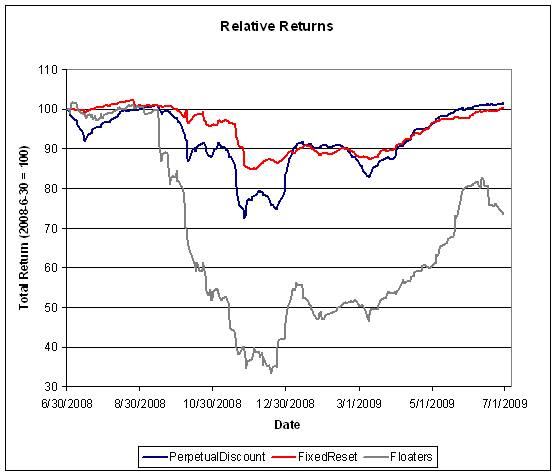

Continued strength in FixedResets brings the yield-to-worst down to 4.55%! Holy smokes, how low can they go?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.6522 % |

1,194.5 |

| FixedFloater |

7.06 % |

5.46 % |

35,241 |

16.37 |

1 |

0.3909 % |

2,137.7 |

| Floater |

3.19 % |

3.68 % |

82,780 |

18.15 |

3 |

0.6522 % |

1,492.2 |

| OpRet |

4.98 % |

3.41 % |

118,629 |

0.88 |

15 |

0.0575 % |

2,209.8 |

| SplitShare |

5.76 % |

6.38 % |

69,320 |

4.19 |

3 |

-0.3160 % |

1,894.9 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0575 % |

2,024.2 |

| Perpetual-Premium |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0938 % |

1,747.3 |

| Perpetual-Discount |

6.31 % |

6.38 % |

161,955 |

13.40 |

71 |

-0.0938 % |

1,609.2 |

| FixedReset |

5.60 % |

4.55 % |

483,655 |

4.34 |

40 |

0.3709 % |

2,040.4 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| W.PR.H |

Perpetual-Discount |

-2.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 20.71

Evaluated at bid price : 20.71

Bid-YTW : 6.68 % |

| ELF.PR.F |

Perpetual-Discount |

-1.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 18.18

Evaluated at bid price : 18.18

Bid-YTW : 7.33 % |

| MFC.PR.A |

OpRet |

-1.50 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2015-12-18

Maturity Price : 25.00

Evaluated at bid price : 24.98

Bid-YTW : 4.16 % |

| PWF.PR.F |

Perpetual-Discount |

-1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 20.06

Evaluated at bid price : 20.06

Bid-YTW : 6.68 % |

| CM.PR.G |

Perpetual-Discount |

-1.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 20.92

Evaluated at bid price : 20.92

Bid-YTW : 6.47 % |

| SLF.PR.A |

Perpetual-Discount |

-1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 17.72

Evaluated at bid price : 17.72

Bid-YTW : 6.76 % |

| BAM.PR.B |

Floater |

-1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 10.74

Evaluated at bid price : 10.74

Bid-YTW : 3.68 % |

| W.PR.J |

Perpetual-Discount |

1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 21.76

Evaluated at bid price : 22.01

Bid-YTW : 6.38 % |

| TD.PR.K |

FixedReset |

1.10 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-08-30

Maturity Price : 25.00

Evaluated at bid price : 27.65

Bid-YTW : 4.33 % |

| BNS.PR.K |

Perpetual-Discount |

1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 20.31

Evaluated at bid price : 20.31

Bid-YTW : 6.03 % |

| BAM.PR.O |

OpRet |

1.19 % |

YTW SCENARIO

Maturity Type : Option Certainty

Maturity Date : 2013-06-30

Maturity Price : 25.00

Evaluated at bid price : 23.88

Bid-YTW : 6.34 % |

| BNS.PR.O |

Perpetual-Discount |

1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 23.62

Evaluated at bid price : 23.80

Bid-YTW : 5.99 % |

| BNS.PR.X |

FixedReset |

1.42 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-25

Maturity Price : 25.00

Evaluated at bid price : 27.80

Bid-YTW : 4.02 % |

| NA.PR.N |

FixedReset |

1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 25.62

Evaluated at bid price : 25.67

Bid-YTW : 4.66 % |

| RY.PR.P |

FixedReset |

1.73 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-03-26

Maturity Price : 25.00

Evaluated at bid price : 27.67

Bid-YTW : 3.96 % |

| TRI.PR.B |

Floater |

2.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 15.55

Evaluated at bid price : 15.55

Bid-YTW : 2.54 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| MFC.PR.E |

FixedReset |

85,595 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-10-19

Maturity Price : 25.00

Evaluated at bid price : 25.30

Bid-YTW : 5.48 % |

| BMO.PR.P |

FixedReset |

81,135 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 23.22

Evaluated at bid price : 25.30

Bid-YTW : 4.90 % |

| SLF.PR.C |

Perpetual-Discount |

67,360 |

Scotia crossed 63,500 at 16.80.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 16.77

Evaluated at bid price : 16.77

Bid-YTW : 6.69 % |

| RY.PR.G |

Perpetual-Discount |

61,780 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 18.26

Evaluated at bid price : 18.26

Bid-YTW : 6.26 % |

| BNS.PR.N |

Perpetual-Discount |

57,359 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-07-02

Maturity Price : 21.39

Evaluated at bid price : 21.71

Bid-YTW : 6.15 % |

| MFC.PR.D |

FixedReset |

51,633 |

National Bank bought two blocks from anonymous, 10,000 and 13,500 shares, both at 27.15.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-07-19

Maturity Price : 25.00

Evaluated at bid price : 27.06

Bid-YTW : 4.85 % |

| There were 37 other index-included issues trading in excess of 10,000 shares. |