Charles Kenny, a Senior Fellow with the Center for Global Development (a quite respectably ranked think-tank) writes a very good piece on Bloomberg about money laundering and regulations thereof:

In the best of cases, anti-money-laundering efforts are likely to do no more than raise the cost of transactions. A system that misses all but a fraction of a percent of criminal financial flows is almost guaranteed to miss terrorism finance in particular, which involves very small sums: The Madrid and London terror bombings cost no more than $10,000 to finance; the Sept. 11 attacks, less than $500,000. That may be one reason why none of the reported money laundering prosecutions to date have involved terror finance.

Though the regulations have limited impact on criminal activities, they still cost money. Tracking illicit money flows requires a considerable bureaucracy. Enforcing the regulations cost an estimated $7 billion in the U.S., and probably far more. Mauritius, a small, middle-income country of just 1.3 million people, has 25 government officials working on FATF implementation. That’s more people than are listed as opticians in the country. Each bank in Mauritius will also have staff tasked with carrying out customer investigations.

Perhaps most insidious, the regulations have disproportionately affected the kinds of business transactions that serve small, poor economies. FATF rules are why Merchants Bank of California cut off money transfers to Somalia last week, the last U.S. financial institution to do so. Between $160 million and $180 million of remittances will be affected by Merchants Bank’s action, but from its point of view, cutting services is the only safe course. It faced immense potential liabilities if it turned out that one of the accounts receiving funds in Somalia was linked to terrorist activity. Yet there’s no evidence any of the remittances were going to fund terror groups; most were being used to support schooling, housing, food, and other living costs for Somalis. The country is one of the poorest in the world and remittances are equal to about one-third of the country’s GDP.

No doubt, Somali expatriates will find other ways to send the money, but they will cost more and are likely to involve less savory financial institutions as intermediaries. Given that, and the link between people losing their livelihoods and terror recruitment, it is all too possible the FATF regulations will give rise to better-funded and larger terrorist groups.

Does anybody else remember 1994? And Orange County’s infamous carry-trades? It will be interesting to see what happens when policy rates rise:

Growth is on a tear, hiring is the strongest in decades and households are the most upbeat since 2011. Yet banks such as Bank of America Corp. keep plowing their burgeoning deposits into U.S. government and related debt — pushing the industry’s holdings past $2 trillion — instead of lending it all out.

Part of the buildup has to do with rules that require banks to hold more high-quality assets in the wake of the worst financial crisis since the Great Depression. But it also reflects how borrowers, particularly among Americans scarred by the housing bust, are still repairing their finances rather than going into debt to splurge on big-ticket items. And that may mean the U.S. recovery isn’t quite as robust as all the upbeat data would suggest.

…

Investing in government bonds is proving to be a profitable move for banks. They’re making over a full percentage point more by purchasing five-year Treasuries instead of leaving the idle cash parked at the Fed, where they earn only 0.25 percent. U.S. commercial banks held $2.83 trillion in cash as of Feb. 11, versus $2.57 trillion at the end of last year.Having cash invested in five-year Treasuries is also netting banks an attractive spread over what they are paying depositors. The yield advantage for the notes over the average deposit rate for the four largest U.S. banks is above the norm over the past decade.

For Bank of America, the spread is about 1.44 percentage points, data compiled by Bloomberg show.

Pension troubles in New Jersey are getting harder to defer:

New Jersey Governor Chris Christie must make a $1.57 billion payment this year to the state pension system, a judge ruled while decrying the failure of the state to address a looming crisis.

…

“Because the state will now make nearly 70 percent less than the statutorily required $2.25 billion payment,” the expectations of workers have been “substantially impaired,” the judge ruled. “In short, the aim of the legislation is not being met.”Jacobson’s ruling contrasts with her decision days before the last fiscal year ended June 30, when Christie said he faced a fiscal emergency. Workers sued then as well, and the judge said Christie acted reasonably in paying $696 million to the pension system to cover current employees while deferring $887 million to help close the gap left by previous governors.

The legislative and executive branches “have now had almost 10 months to find a solution to the pensions crisis for FY 2015,” Jacobson said in the latest ruling.

DBRS has confirmed Fairfax with a stable trend. I have updated the post regarding S&P’s revision to ‘Outlook Negative’.

Preferred share investors rushed to their monitors this morning to see what would happen at the start of a new week:

Click for Big

It was a poor day for the Canadian preferred share market, with PerpetualDiscounts down 3bp, FixedResets losing 67bp and DeemedRetractibles off 2bp. ENB and TRP issues are prominent on the bad side of a suitably lengthy Performance Highlights table. Volume was high, with ENB issues again prominent – it looks like people are getting increasingly nervous about a possible downgrade.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

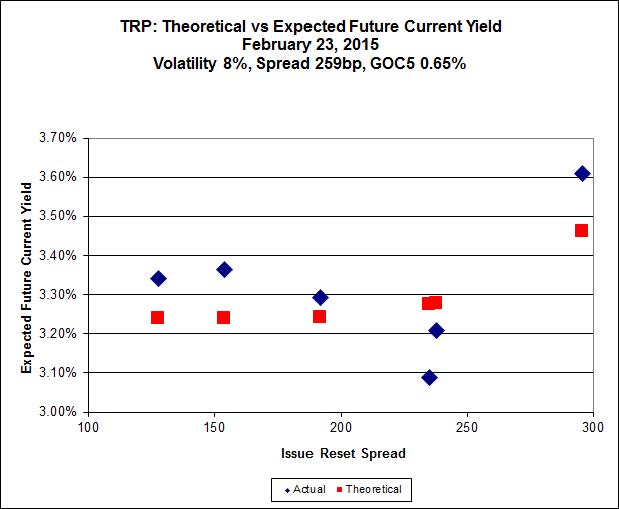

Here’s TRP:

Click for Big

The new issue has caused a large change in the curve-fitting for the TRP series of FixedResets, which is discussed at greater length on the post announcing the new issue. TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.28 to be $1.37 rich, while the new issue, resetting 2020-11-30 at +296, is $1.07 cheap at its issue price of 25.00.

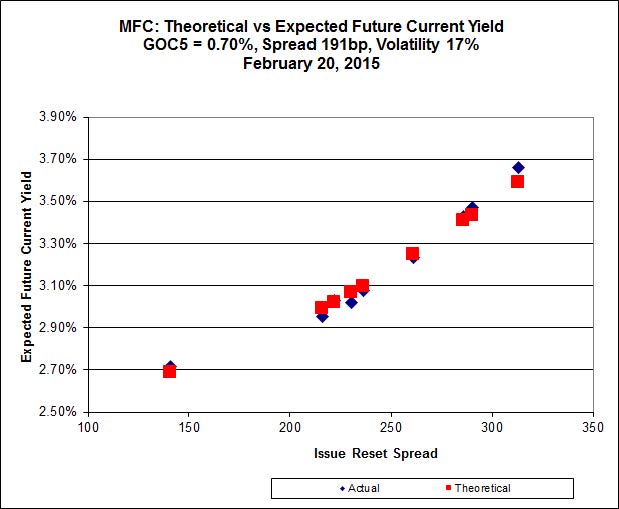

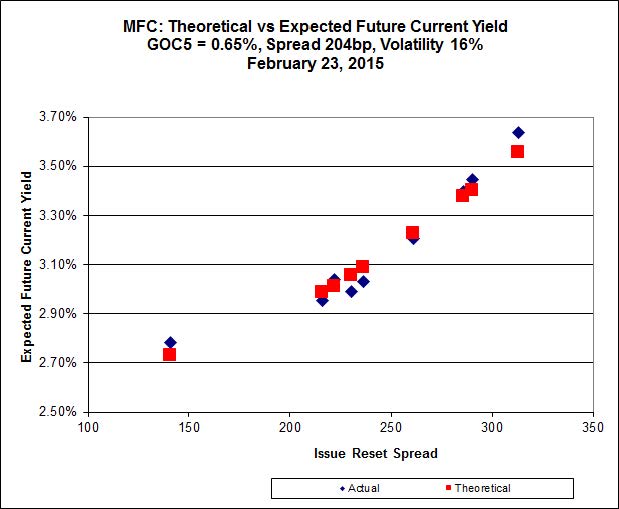

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.N, resetting at +230 on 2020-3-19, bid at 24.68 to be $0.55 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.97 to be $0.62 cheap.

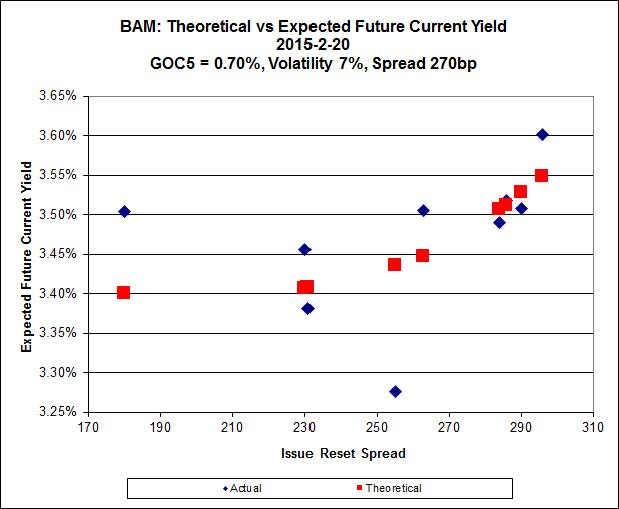

Click for Big

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

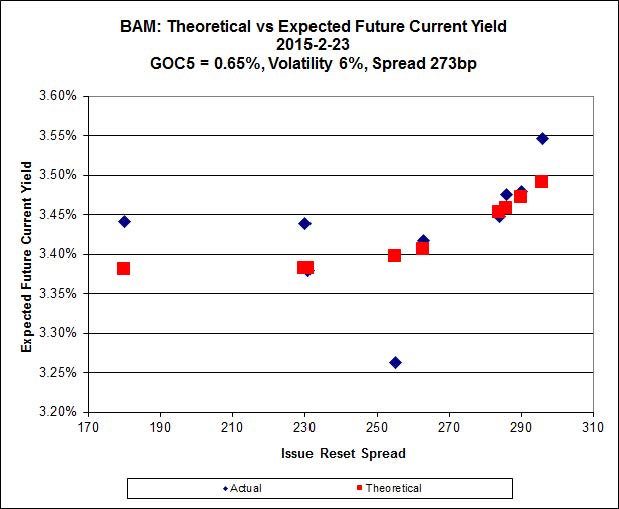

The cheapest issue relative to its peers is BAM.PR.Z, resetting at +296bp on 2017-12-31, bid at 25.45 to be $0.41 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.52 and appears to be $0.97 rich.

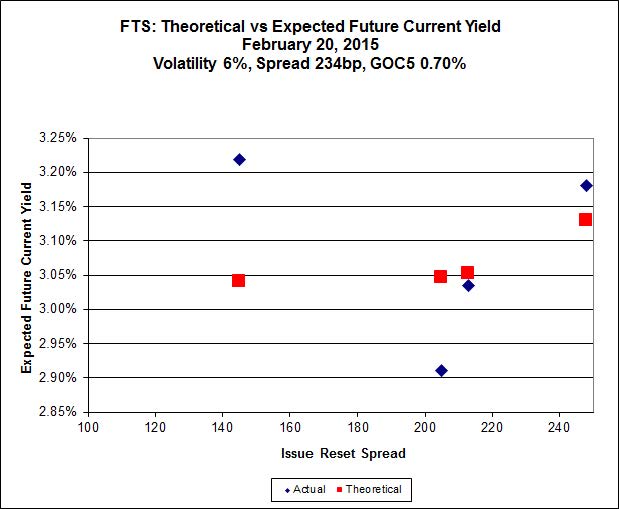

Click for Big

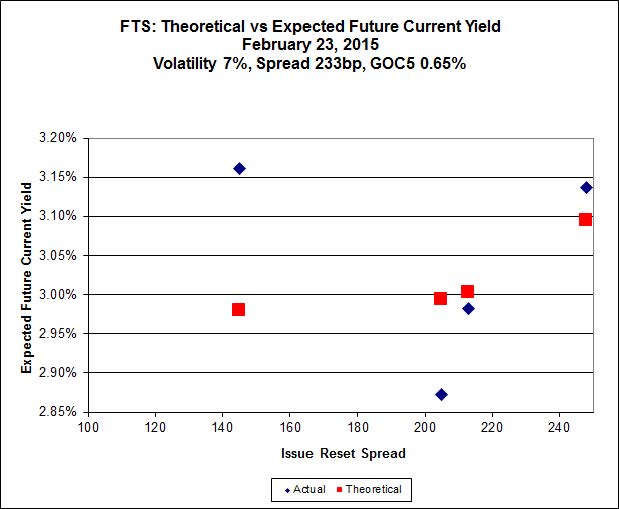

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.61, looks $1.01 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.50 and is $0.96 rich.

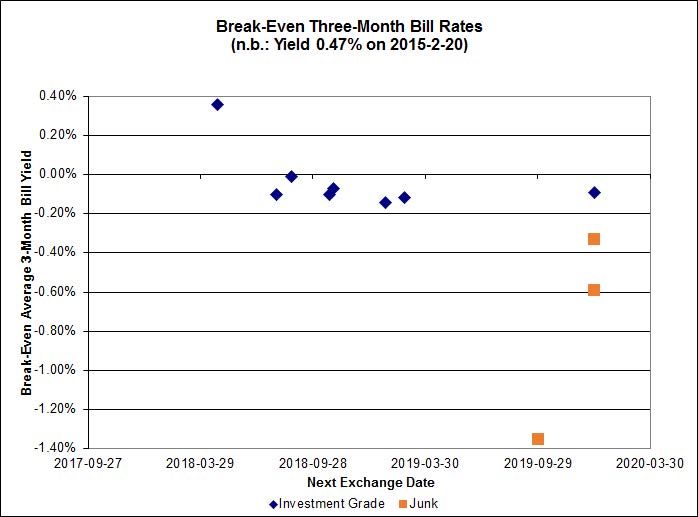

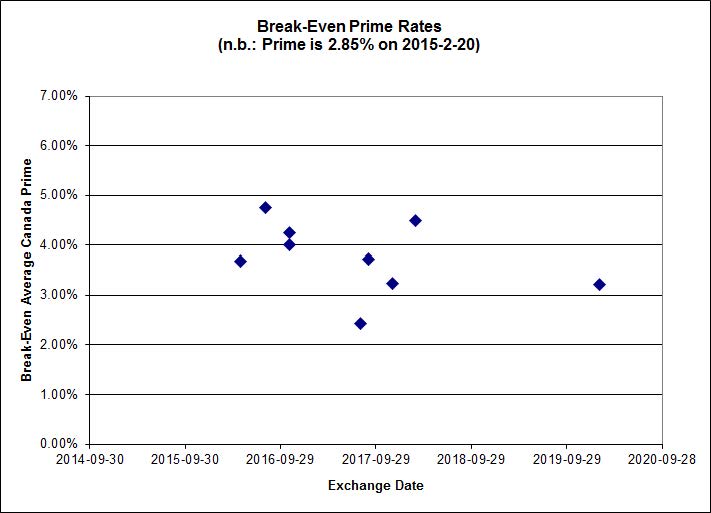

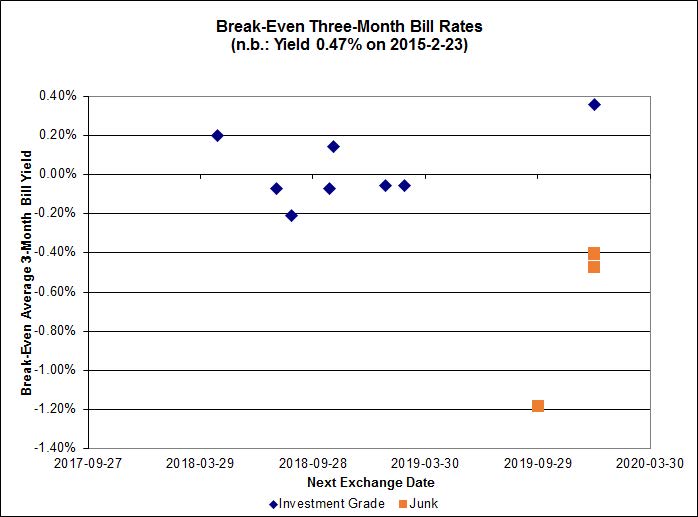

Click for Big

Most of the investment grade break-even rates are scattered around zero.

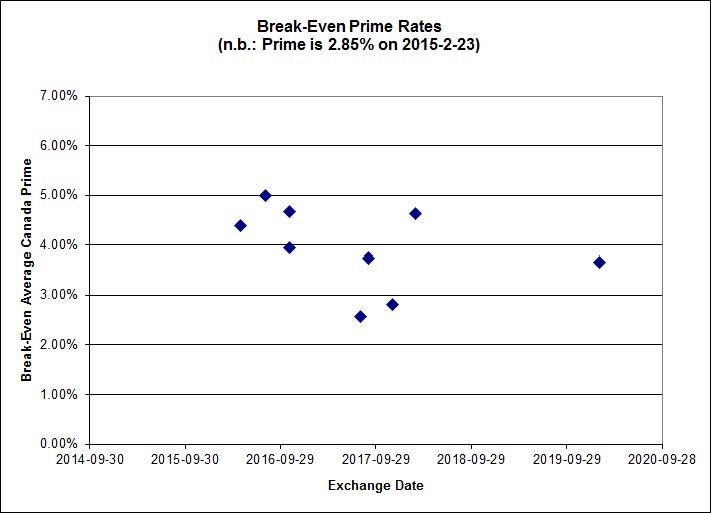

On the other hand, the market’s distaste for product linked to Money Market rates does not extend to prime, as shown by the FixedFloater/RatchetRate pairs:

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.9080 % | 2,366.2 |

| FixedFloater | 4.37 % | 3.52 % | 18,990 | 18.38 | 1 | 0.0000 % | 4,046.5 |

| Floater | 3.05 % | 3.18 % | 67,125 | 19.23 | 4 | -0.9080 % | 2,515.5 |

| OpRet | 4.08 % | 1.99 % | 112,950 | 0.32 | 1 | -0.1722 % | 2,754.9 |

| SplitShare | 4.32 % | 4.62 % | 28,133 | 3.55 | 5 | -1.0670 % | 3,184.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1722 % | 2,519.1 |

| Perpetual-Premium | 5.33 % | 1.52 % | 56,568 | 0.08 | 24 | 0.0327 % | 2,514.6 |

| Perpetual-Discount | 4.95 % | 4.82 % | 115,235 | 15.25 | 10 | -0.0334 % | 2,794.8 |

| FixedReset | 4.45 % | 3.30 % | 206,478 | 16.90 | 79 | -0.6720 % | 2,410.7 |

| Deemed-Retractible | 4.91 % | 0.02 % | 104,901 | 0.10 | 39 | -0.0215 % | 2,650.6 |

| FloatingReset | 2.43 % | 2.86 % | 89,472 | 6.39 | 7 | -0.0308 % | 2,322.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.P | FixedReset | -3.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 18.03 Evaluated at bid price : 18.03 Bid-YTW : 3.26 % |

| ENB.PR.T | FixedReset | -3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 4.25 % |

| PVS.PR.B | SplitShare | -3.80 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.29 Bid-YTW : 5.15 % |

| PWF.PR.A | Floater | -3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 18.26 Evaluated at bid price : 18.26 Bid-YTW : 2.74 % |

| ENB.PR.N | FixedReset | -3.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 20.42 Evaluated at bid price : 20.42 Bid-YTW : 4.22 % |

| MFC.PR.F | FixedReset | -3.34 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.50 Bid-YTW : 5.84 % |

| ENB.PR.P | FixedReset | -3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 4.17 % |

| ENB.PF.C | FixedReset | -3.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 21.84 Evaluated at bid price : 22.30 Bid-YTW : 3.98 % |

| ENB.PR.J | FixedReset | -2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 4.11 % |

| ENB.PF.A | FixedReset | -2.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 21.81 Evaluated at bid price : 22.23 Bid-YTW : 4.00 % |

| TRP.PR.C | FixedReset | -2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 3.53 % |

| TRP.PR.A | FixedReset | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 3.55 % |

| TRP.PR.B | FixedReset | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 14.44 Evaluated at bid price : 14.44 Bid-YTW : 3.44 % |

| ENB.PR.Y | FixedReset | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 4.22 % |

| ENB.PR.F | FixedReset | -1.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 19.28 Evaluated at bid price : 19.28 Bid-YTW : 4.30 % |

| PVS.PR.C | SplitShare | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2017-12-10 Maturity Price : 25.00 Evaluated at bid price : 25.12 Bid-YTW : 4.62 % |

| BAM.PR.T | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 21.52 Evaluated at bid price : 21.90 Bid-YTW : 3.58 % |

| ENB.PR.B | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 4.29 % |

| HSE.PR.A | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 3.61 % |

| ENB.PR.D | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 4.28 % |

| TRP.PR.D | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 22.66 Evaluated at bid price : 23.62 Bid-YTW : 3.36 % |

| PWF.PR.T | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 23.26 Evaluated at bid price : 25.02 Bid-YTW : 3.11 % |

| GWO.PR.G | Deemed-Retractible | -1.25 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-03-25 Maturity Price : 25.00 Evaluated at bid price : 25.35 Bid-YTW : -2.44 % |

| VNR.PR.A | FixedReset | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 23.41 Evaluated at bid price : 24.90 Bid-YTW : 3.51 % |

| BAM.PR.R | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 3.68 % |

| BAM.PF.E | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 22.98 Evaluated at bid price : 24.52 Bid-YTW : 3.49 % |

| HSE.PR.C | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 23.22 Evaluated at bid price : 25.14 Bid-YTW : 3.86 % |

| MFC.PR.K | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.62 Bid-YTW : 3.89 % |

| BAM.PF.B | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 22.85 Evaluated at bid price : 24.00 Bid-YTW : 3.57 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.J | FixedReset | 140,313 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 23.19 Evaluated at bid price : 25.13 Bid-YTW : 3.30 % |

| ENB.PR.T | FixedReset | 63,228 | RBC crossed 33,000 at 19.25. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 4.25 % |

| TD.PR.T | FloatingReset | 60,470 | TD crossed 41,400 at 23.82 and bought 11,500 from Scotia at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.83 Bid-YTW : 2.78 % |

| ENB.PF.C | FixedReset | 40,945 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 21.84 Evaluated at bid price : 22.30 Bid-YTW : 3.98 % |

| TRP.PR.C | FixedReset | 31,658 | RBC crossed 10,000 at 16.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 16.28 Evaluated at bid price : 16.28 Bid-YTW : 3.53 % |

| ENB.PR.F | FixedReset | 28,981 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-02-23 Maturity Price : 19.28 Evaluated at bid price : 19.28 Bid-YTW : 4.30 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PVS.PR.B | SplitShare | Quote: 24.29 – 25.30 Spot Rate : 1.0100 Average : 0.5591 YTW SCENARIO |

| NEW.PR.D | SplitShare | Quote: 32.40 – 33.40 Spot Rate : 1.0000 Average : 0.7593 YTW SCENARIO |

| PWF.PR.A | Floater | Quote: 18.26 – 18.96 Spot Rate : 0.7000 Average : 0.5045 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 23.80 – 24.50 Spot Rate : 0.7000 Average : 0.5105 YTW SCENARIO |

| ENB.PF.A | FixedReset | Quote: 22.23 – 22.72 Spot Rate : 0.4900 Average : 0.3063 YTW SCENARIO |

| GWO.PR.G | Deemed-Retractible | Quote: 25.35 – 25.75 Spot Rate : 0.4000 Average : 0.2751 YTW SCENARIO |