It’s interesting:

2. Perpetual and Retractible Preferred Shares

3. Corporate Bonds … or Preferred Shares?

4. Interest Bearing Preferreds

5. Why Invest in Preferred Shares?

6. A Brief Introduction to Preferred Shares

John Hull has published an essay titled The Credit Crunch of 2007: What Went Wrong? Why? What Lessons Can Be Learned?:

This paper explains the events leading to the credit crisis that began in 2007 and the products that were created from residential mortgages. It explains the multiple levels of securitization that were involved. It argues that the inappropriate incentives led to a short‐term focus in the decision making of traders and a failure to evaluate the risks being taken. The products that were created lacked transparency with the payoffs from one product depending on the performance of many other products. Market participants relied on the AAA ratings assigned to products without evaluating the models used by rating agencies. The paper considers the steps that can be taken by financial institutions and their regulators to avoid similar crises in the future. It suggests that companies should be required to retain some of the risk in each instrument that is created when credit risk is transferred. The compensation plans within financial institutions should be changed so that they have a longer term focus. Collateralization through either clearinghouses or two‐way collateralization agreements should become mandatory. Risk management should involve more managerial judgment and rely less on the mechanistic application of value‐at‐risk models.

With respect to tranche retention, Dr. Hull argues:

The present crisis might have been less severe if the originators of mortgages (and other assets where credit risk is transferred) were required by regulators to keep, say, 20% of each tranche created. This would have better aligned the interests of originators with the interests of the investors who bought the tranches.

…

The most important reason why originators should have a stake in all the tranches created is that this encourages the originators to make the same lending decisions that the investors would make. Another reason is that the originators often end up as administrators of the mortgages (collecting interest, making foreclosure decisions, etc). It is important that their decisions as administrators are made in the best interests of investors.

…

This idea might have reduced the market excesses during the period leading up to the credit crunch of 2007. However, it should be acknowledged that one of the ironies of the credit crunch is that securitization did not in many instances get the mortgages off the books of originating banks. Often AAA-rated senior tranches created by one part of a bank were bought by other parts of the bank. Because banks were both investors in and originators of mortgages, one might expect a reasonable alignment of the interests of investors and originators. But the part of the bank investing in the mortgages was usually far removed from the part of the bank originating the mortgages and there appears to have been little information flow from one to the other.

Assiduous Readers will not be surprised to learn that I don’t like this idea. In my role as bond trader I have never bought a securitization … I would if the spreads were high enough, but generally spreads are compressed by other buyers.

When I buy a bond, I want to know somebody’s on the hook for it. I like the idea that if the borrower is a day late or a dollar short, I can force an operating company into bankruptcy and cause great anguish and financial ill effects on the deadbeats. Securitizations tend to be highly correllated; while this is claimed to be counterbalanced by the overcollateralization (or tranche subordination, which is simply a formalization of the process) I confess I have a great preference for keeping actual bonds in my bond portfolios.

Tranche retention is simply a methodology whereby securitizations become more bond-like. I object to such blurring of the lines, especially when enforced by governmental regulatory fiat. What I am being told, in a world where such retention is mandated, is that if something has been issued that I – for good reasons or bad – wish to buy and that the security originator wishes to sell, we’ll both go to jail if we consummate the transaction.

I will also point out the logical implications of tranche retention: when I sell 100 shares of SLF.PR.A, I should be forced to retain 20 of them, so that the buyer will know they’re OK. That’s crazy. The buyer should do his own damn homework and make up his own mind.

The world has learned over and over that while regulation is very nice, the only thing that works really well is caveat emptor. I do not want some 20-year old regulator with a college certificate in boxtickingology telling me what I may and may not buy.

Dr. Hull has underemphasized the heart of the matter: one of the ironies of the credit crunch is that securitization did not in many instances get the mortgages off the books of originating banks. Often AAA-rated senior tranches created by one part of a bank were bought by other parts of the bank..

In this context, I will repeat some of Sheila Bair’s testimony to the Crisis Committee:

In the mid-1990s, bank regulators working with the Basel Committee on Banking Supervision (Basel Committee) introduced a new set of capital requirements for trading activities. The new requirements were generally much lower than the requirements for traditional lending under the theory that banks’ trading-book exposures were liquid, marked-to-market, mostly hedged, and could be liquidated at close to their market values within a short interval—for example 10 days.

The market risk rule presented a ripe opportunity for capital arbitrage, as institutions began to hold growing amounts of assets in trading accounts that were not marked-to-market but “marked-to-model.” These assets benefitted from the low capital requirements of the market risk rule, even though they were in some cases so highly complex, opaque and illiquid that they could not be sold quickly without loss. Indeed, in late 2007 and through 2008, large write-downs of assets held in trading accounts weakened the capital positions of some large commercial and investment banks and fueled market fears.

I see the basic problem as one that happens when traders try to be investors. Traders do not typically know a lot about the market – although they can talk a good game – and when they try their hand at actual investing, bad things will happen more often than not. It’s a totally different mindset.

I didn’t make a penny during the tech bubble – never bought any of it. I have numerous friends, however, who made out like bandits and set themselves up for life during those years. The difference between us was not the knowledge that that stuff was garbage … we all knew it was garbage. But I could not sleep at night knowing I had garbage in my portfolio; they were fine with the idea, so long as there was lots of positive chatter and prices kept going up.

A long, long time ago – so long I can’t remember the reference – I read an interview with a big wheel (perhaps the proprietor) of a small NASDAQ trading firm. The interview was interupted when one of his staff burst in with the news that another brokerage (XYZ brokers) wanted to sell a large block of stock (45,000 shares, if I remember correctly) in ABC Company and was willing to do so at a discount to market. So they look at the recent price/volume history, check the news and the deal gets done. When the interview resumed, the interviewer asked “So … what’s ABC Company?”. The trader replied, patienty and wearily: “Its something XYZ wanted to sell 45,000 shares of.”

Now that’s trading!

Despite constant interviews by the media, there is not really much correlation between trading ability and investing ability.

So anyway, I will suggest that when considering a regulatory response to the Credit Crunch, a clearer distinction between trading and investing activities is what’s required. As I have previously suggested, there should be no bright-line between investment banks and vanilla banks; but the difference should be recognized in the capital rules. Investment banks should have low capital requirements for trading inventory and higher ones for investment positions; the reverse for vanilla banks. And for heaven’s sake, make sure that there’s no jiggery-pokery with aging positions on the trading books! Hold it for thirty days, and the capital charge goes up progressively! Start trading too many “investment” positions and you’ll find your investment portfolio reclassified.

As far as bonus deferral is concerned … it’s suitable for investors, not so much for traders. Bonus deferral requires a lot of trust by the employee, trust that is all too often unjustified as exemplified by the Citigroup case discussed January 7 and, here in Canada, by the case of David Berry. The major effect of bonus deferral, I believe, will be to spawn a migration of talent to hedge funds and boutiques.

Dr. Hull suggests:

One idea is the following. At the end of each year a financial institution awards a “bonus accrual” (positive or negative) to each employee reflecting the employee’s contribution to the business. The actual cash bonus received by an employee at the end of a year would be the average bonus accrual over the previous five years or zero, whichever is higher. For the purpose of this calculation, bonus accruals would be set equal to zero for years prior to the employee joining the financial institution (unless the employee manages to negotiate otherwise) and bonuses would not be paid after an employee leaves it. Although not perfect, this type of plan would motivate employees to use a multi-year time horizon when making decisions.

One problem I have with that is vesting. Is the vesting of this bonus iron-clad or not? Is it held by a mutually agreed-upon third party in treasury bills? And what happens if the employee leaves the firm and somebody else starts trading his book? Who takes any future losses then?

Another problem, of course, is trust (assuming the vesting is not iron-clad). When a relationship turns sour – or somebody gets greedy – things can turn nasty in a hurry. It should always be remembered that the purpose of regulation is not to protect anybody. The purpose of regulation is to ensure that everybody is guilty of something.

I have twice been offered jobs with the stupidest incentive scheme in the world. Not only would my bonus be determined by how well the firm did – putting me on the hook for decisions made by people I didn’t even know – but because of deferral, up-front transfers and discretion, I could have worked there for five years and paid them for the privilege. Those negotiations didn’t take long!

Mary Schapiro of the SEC testified to the Crisis Committee. It’s lightweight bureaucratic fluff, especially when compared to Sheila Bair’s testimony, which was a joy to read since it contained actual arguments.

The previously mocked HAMP is looking more sickly by the minute:

About 25 percent of homeowners who received trial loan modifications through President Barack Obama’s main foreclosure prevention plan are failing to keep up with their new reduced payments, the Treasury Department said.

At least 196,000 borrowers have missed some or all of their required payments, according to comments Treasury officials made on a conference call today and calculations from government data. An additional 115,000 homeowners who started trial repayment plans last year have either dropped out or been kicked out of Obama’s Home Affordable Modification Program, the officials said.

…

Turning around the U.S. housing market is one of Obama’s top priorities, Lawrence Summers, the president’s top economic adviser, told reporters yesterday. The administration has put off restructuring federally controlled mortgage-finance companies Fannie Mae and Freddie Mac while they are administering the mortgage- modification program.

PerpetualDiscounts had a nothing day on the Canadian preferred share market, losing a quarter of a beep, but FixedResets bounced back strongly, gaining 13bp. Volume was heavy.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4882 % | 1,709.1 |

| FixedFloater | 5.89 % | 3.95 % | 35,508 | 19.08 | 1 | 1.0959 % | 2,682.3 |

| Floater | 2.30 % | 2.63 % | 109,631 | 20.71 | 3 | 0.4882 % | 2,135.1 |

| OpRet | 4.84 % | -3.74 % | 116,926 | 0.09 | 13 | 0.1034 % | 2,319.8 |

| SplitShare | 6.35 % | -4.00 % | 184,077 | 0.08 | 2 | 0.0219 % | 2,114.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1034 % | 2,121.2 |

| Perpetual-Premium | 5.78 % | 5.63 % | 145,233 | 2.26 | 12 | -0.1286 % | 1,896.2 |

| Perpetual-Discount | 5.73 % | 5.74 % | 178,385 | 14.28 | 63 | -0.0025 % | 1,833.3 |

| FixedReset | 5.40 % | 3.56 % | 329,303 | 3.85 | 42 | 0.1264 % | 2,180.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TD.PR.Y | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-11-30 Maturity Price : 25.00 Evaluated at bid price : 25.66 Bid-YTW : 4.26 % |

| ENB.PR.A | Perpetual-Premium | -1.56 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2010-02-14 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : -0.85 % |

| W.PR.J | Perpetual-Discount | -1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 23.20 Evaluated at bid price : 23.50 Bid-YTW : 5.99 % |

| BAM.PR.B | Floater | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 15.06 Evaluated at bid price : 15.06 Bid-YTW : 2.63 % |

| BAM.PR.G | FixedFloater | 1.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 25.00 Evaluated at bid price : 18.45 Bid-YTW : 3.95 % |

| POW.PR.D | Perpetual-Discount | 1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 21.61 Evaluated at bid price : 21.95 Bid-YTW : 5.72 % |

| GWO.PR.J | FixedReset | 1.57 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-01-30 Maturity Price : 25.00 Evaluated at bid price : 27.74 Bid-YTW : 3.15 % |

| TRP.PR.A | FixedReset | 2.03 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-30 Maturity Price : 25.00 Evaluated at bid price : 26.58 Bid-YTW : 3.28 % |

| HSB.PR.C | Perpetual-Discount | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 23.09 Evaluated at bid price : 23.30 Bid-YTW : 5.51 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.R | FixedReset | 288,715 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 23.19 Evaluated at bid price : 25.30 Bid-YTW : 4.88 % |

| MFC.PR.A | OpRet | 192,570 | RBC crossed 190,000 at 26.75. YTW SCENARIO Maturity Type : Call Maturity Date : 2010-07-19 Maturity Price : 26.25 Evaluated at bid price : 26.50 Bid-YTW : 2.60 % |

| TRP.PR.A | FixedReset | 147,424 | RBC bought 10,000 from Nesbitt at 26.60. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-01-30 Maturity Price : 25.00 Evaluated at bid price : 26.58 Bid-YTW : 3.28 % |

| BAM.PR.P | FixedReset | 96,780 | Nesbitt crossed 68,700 at 27.20. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-10-30 Maturity Price : 25.00 Evaluated at bid price : 27.18 Bid-YTW : 5.04 % |

| SLF.PR.C | Perpetual-Discount | 61,813 | RBC crossed 50,000 at 19.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 19.37 Evaluated at bid price : 19.37 Bid-YTW : 5.80 % |

| IAG.PR.A | Perpetual-Discount | 50,360 | RBC crossed 49,400 at 20.30. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-15 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 5.73 % |

| There were 46 other index-included issues trading in excess of 10,000 shares. | |||

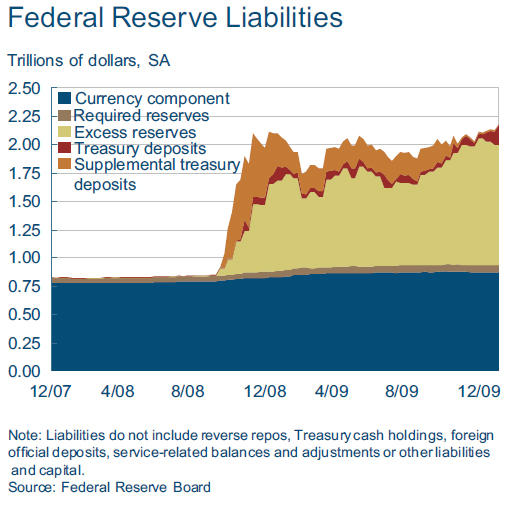

Excess bank reserves at the Fed were last discussed on PrefBlog when reviewing a New York Fed working paper titled Why are banks holding so many excess reserves?.

The Federal Reserve Bank of Cleveland has released the Econotrends, January 2010 with an interesting article by John B. Carlson and John Lindner titled Treasury Deposits and Excess Bank Reserves:

An interesting development on the Federal Reserve’s balance sheet is a decline in excess bank reserves. Th is decline has occurred despite an increase in the overall size of the Fed’s balance sheet. Th e key factor accounting for the decline in excess reserves is a substantial increase in U.S. treasury deposits at the Fed, which were made as a consequence of having issued new debt. When the treasury issues debt to the public and deposits the proceeds at the Fed in its general account, bank reserves decline. In normal times, the treasury typically holds some proceeds in Treasury Tax and Loan accounts at commercial banks, which keeps reserves in the banking system. Th is arrangement helps maintain a steady supply of reserves—a desirable outcome for when the Fed sought to keep the fed funds rate near a target rate.

Following the collapse of Lehman Brothers in September 2008, the Federal Reserve instituted a number of policies that sharply increased bank reserves in excess of required levels. Initially, the Fed sought to absorb most of the new reserves in order to keep the fed funds rate near its target rate. To help in this eff ort, the treasury issued short-term debt at special auctions (called the Supplementary Financing Program or SFP) and placed the proceeds in a new supplemental treasury account at the Federal Reserve. Still, the amount of reserves absorbed could not keep up with the amount of bank reserves that were being created with the Fed’s new credit policies. Subsequently, the fed funds target was lowered to zero, and the immediate need to absorb reserves abated.

In late 2009 the total level of treasury debt approached the limit authorized by Congress. As the SFP issues matured, the SFP deposits were used to redeem them, and excess reserves increased. In December Congress raised the debt ceiling, allowing the treasury to issue new debt. Th is time, the treasury deposited much of the proceeds into its general account with the Fed, which caused the observed decline in excess reserves.

John Hull and Alan White have published a working paper titled The Risk of Tranches Created from Residential Mortgages:

This paper examines, ex-ante, the risk in the tranches of ABSs and ABS CDOs that were created from residential mortgages between 2000 and 2007. Using the criteria of the rating agencies, it tests how wide the AAA tranches can be under different assumptions about the correlation model and recovery rates. It concludes that the AAA ratings assigned to the senior tranches of ABSs were not totally unreasonable. However, the AAA ratings assigned to tranches of Mezz ABS CDOs cannot be justified. The risk of a Mezz ABS CDO tranche depends critically on the correlation between mortgage pools as well as on the correlation model and the thickness of the underlying BBB tranches. The BBB tranches of ABSs cannot be considered equivalent to BBB bonds for the purposes of subsequent securitizations.

This paper won’t be popular amongst the Credit Ratings Agencies Are Evil crowd!

Credit derivatives models often assume that the recovery rate realized when there is a default is constant. This is less than ideal. As the default rate increases, the recovery rate for a particular asset class can be expected to decline. This is because a high default rate leads to more of the assets coming on the market and a reduction in price.

As is now well known, this argument is particularly true for residential mortgages. In a normal market, a recovery rate of about 75% is often assumed for this asset class. If this is assumed to be the recovery rate in all situations, the worst possible loss on a portfolio of residential mortgages given by the model would be 25%, and the 25% to 100% senior tranche of an ABS created from the mortgages could reasonably be assumed to be safe. In fact, recovery rates on mortgages have declined in the high default rate environment experienced since 2007.

The evaluation of ABSs depends on a) the expected default rate, Q, for mortgages in the underlying pool, b) the default correlation, ρ, for mortgages in the pool, and c) the recovery rate, R. Data from the 1999 to 2006 period suggest a value of Q less than 5% assuming an average mortgage life of 5 years. But, as has been mentioned, a different macroeconomic environment could be anticipated over the next few years. It would seem to be more prudent to use an estimate of 10%, or even higher. We will present results for values of Q equal to 5%, 10%, and 20%. The Basel II capital requirements are based on a copula correlation of 0.15 for residential mortgages.6 We will present results for values of ρ between 0.05 and 0.30. As already mentioned, a recovery rate of 75% is often assumed for residential mortgages, but this is probably optimistic in a high default rate environment. We will present results for the situation where the recovery rate is fixed at 75% and for the situation where the recovery rate model in the previous section is used with Rmin=50% and Rmax=100%.

ABS CDOs also depend on the parameter, α. Loosely speaking, this measures the proportion of the default correlation that comes from a factor common to all pools. A value of α close to zero indicates that investors obtain good diversification benefits from the ABS CDO structure. In adverse market conditions some mezzanine tranches can be expected to suffer 100% losses while others incur no losses. However, a value of α close to one indicates that all mezzanine tranches will tend to sink or swim together. We do not know what estimates rating agencies made for α. (Ex post of course, we know that it was high.) We will therefore present results based on a wide range of values for this parameter.

The meat of the matter – at least as far as the CRAs are concerned – is:

Table 2 shows that when a 20% default rate is combined with a high default correlation, and a stochastic recovery rate model, the AAA ratings that were made seem a little high. Also, the ratings are difficult to justify when the most extreme model (double t copula, stochastic recovery rate) is used. But overall the results in Table 2 indicate that the AAA ratings that were assigned were not totally unreasonable.

Very bad things happened to CDOs created from the mezzanine tranches of the structures – and here the CRAs can be faulted:

It should be noted that a CDO created from the triple BBB tranches of ABSs is quite different from a CDO created from BBB bonds. This is true even when the BBB tranches have been chosen so that their probabilities of default and expected losses are consistent with their BBB rating. The reason is that the probability distribution of the loss from a BBB tranche is quite different from the probability distribution of the loss from a BBB bond.

The authors conclude:

Contrary to many of the opinions that have been expressed, the AAA ratings for the senior tranches of ABSs were not unreasonable. The weighted average life of mortgages is about five years. The probability of loss and expected loss of the AAA-rated tranches that were created were similar to or better than those of AAA-rated five-year bonds.

The AAA ratings for Mezz ABS CDOs are much less defensible. Scenarios where all the underlying BBB tranches lose virtually all their principal are sufficiently probable that it is not reasonable to assign a AAA rating to even a quite thin senior tranche. The risks in Mezz ABS CDOs depend critically on a) the width of the underlying BBB tranches, b) the correlation between pools, c) the tail default correlation, and d) the relationship between the recovery rate and the default rate. An important point is that the BBB tranche of an ABS cannot be assumed to be similar to a BBB bond for the purposes of determining the risks in ABS CDO tranches.

In practice Mezz ABS CDOs accounted for about 3% of all mortgage securitizations. Our conclusion is therefore that the vast majority of the AAA ratings assigned to tranches created from mortgages were reasonable, but in a small minority of the cases they cannot be justified.

I think it’s fair to conclude that the problems of the sub-prime crisis were not with the rating agencies or, to a small degree, with investors who plunked down their money. The problem lay in concentration: the banks took the view that if one is good, two is better … and went the way of all those who fail to diversify sufficiently.

Update: For a review of what participants were thinking at the time, see Making sense of the subprime crisis. For more on subprime default experience, see Subprime! Problems forseeable in 2005?. I will admit, though, that what I’m really waiting for is an accounting of realized losses on subprime paper.

Comrade Peace-Price made the punitive taxation of vilified institutions official:

“My commitment is to recover every single dime the American people are owed,” Obama said in a statement released this morning. “My determination to achieve this goal is only heightened when I see reports of massive profits and obscene bonuses at the very firms who owe their continued existence to the American people.”

The levy would be based on bank liabilities and be imposed starting June 30 on companies such as Citigroup Inc., American International Group Inc. and Bank of America Corp. The administration estimates it will raise $90 billion over a minimum of 10 years, said an administration official, who briefed reporters on the condition of anonymity.

As discussed yesterday, the bulk of TARP costs have been for carmakers and individuals, but since when have facts influenced a demagogue?

The SEC has released a Concept Release on Equity Market Structure:

The Securities and Exchange Commission (“Commission”) is conducting a broad review of the current equity market structure. The review includes an evaluation of equity market structure performance in recent years and an assessment of whether market structure rules have kept pace with, among other things, changes in trading technology and practices. To help further its review, the Commission is publishing this concept release to invite public comment on a wide range of market structure issues, including high frequency trading, order routing, market data linkages, and undisplayed, or “dark,” liquidity. The Commission intends to use the public’s comments to help determine whether regulatory initiatives to improve the current equity market structure are needed and, if so, the specific nature of such initiatives.

Meanwhile, the Fed has released a Report to Congress on the Case for a Role for the Federal Reserve in Bank Supervision:

Besides the experience at the Federal Reserve, international developments suggest that a central bank role in supervision can be important. For example, many have suggested that the problems with Northern Rock in the United Kingdom were compounded by a lack of clarity regarding the distribution of powers, responsibilities, and information among the Bank of England, the U.K. Financial Services Authority, and the U.K. Treasury. In response, the Bank of England was given statutory responsibilities in the area of financial stability, its powers to collect information from banks were augmented, and many have called for it to be given increased supervisory authority. In the European Union, a new European Systemic Risk Board is being established under which national central banks and the European Central Bank will play a central role in efforts to protect the financial system from systemic risk. More broadly, in most industrial countries today the central bank has substantial bank supervisory authorities, is responsible for broad financial stability, or both.

There was not a lot of price action in the preferred share market today, at it seems to have found some kind of level after the large gains of early January: PerpetualDiscounts were down 8bp, while FixedResets gained 4bp, on reasonable volume. The day was enlivened by the successful launch of BAM.PR.R.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.5103 % | 1,700.8 |

| FixedFloater | 5.96 % | 4.01 % | 35,621 | 19.01 | 1 | -0.8152 % | 2,653.2 |

| Floater | 2.31 % | 2.65 % | 109,498 | 20.64 | 3 | 0.5103 % | 2,124.7 |

| OpRet | 4.85 % | -0.57 % | 118,176 | 0.09 | 13 | -0.0177 % | 2,317.4 |

| SplitShare | 6.36 % | 0.34 % | 186,248 | 0.08 | 2 | 0.3519 % | 2,113.9 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0177 % | 2,119.0 |

| Perpetual-Premium | 5.78 % | 5.66 % | 142,923 | 2.26 | 12 | 0.0132 % | 1,898.7 |

| Perpetual-Discount | 5.73 % | 5.75 % | 180,123 | 14.26 | 63 | -0.0821 % | 1,833.4 |

| FixedReset | 5.41 % | 3.59 % | 330,911 | 3.85 | 42 | 0.0374 % | 2,177.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| POW.PR.D | Perpetual-Discount | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 21.61 Evaluated at bid price : 21.61 Bid-YTW : 5.83 % |

| W.PR.H | Perpetual-Discount | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 22.57 Evaluated at bid price : 23.24 Bid-YTW : 5.92 % |

| RY.PR.P | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-03-26 Maturity Price : 25.00 Evaluated at bid price : 27.65 Bid-YTW : 3.77 % |

| BAM.PR.B | Floater | 1.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 14.91 Evaluated at bid price : 14.91 Bid-YTW : 2.65 % |

| ELF.PR.G | Perpetual-Discount | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 18.43 Evaluated at bid price : 18.43 Bid-YTW : 6.49 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BAM.PR.R | FixedReset | 614,165 | New issue settled today. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 23.17 Evaluated at bid price : 25.26 Bid-YTW : 4.89 % |

| RY.PR.L | FixedReset | 133,433 | Nesbitt crossed 120,000 at 27.22. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-03-26 Maturity Price : 25.00 Evaluated at bid price : 27.20 Bid-YTW : 3.53 % |

| TD.PR.R | Perpetual-Premium | 74,160 | RBC crossed 72,000 at 24.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 24.54 Evaluated at bid price : 24.76 Bid-YTW : 5.67 % |

| GWO.PR.J | FixedReset | 72,492 | RBC bought two blocks of 25,000 shares and one of 20,100 shares from anonymous, all at 27.34. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-01-30 Maturity Price : 25.00 Evaluated at bid price : 27.31 Bid-YTW : 3.59 % |

| CM.PR.A | OpRet | 56,911 | Desjardins crossed 27,500 at 26.28 and sold 16,500 to Nesbitt at 26.29. I want a commission! YTW SCENARIO Maturity Type : Call Maturity Date : 2010-02-13 Maturity Price : 25.25 Evaluated at bid price : 26.30 Bid-YTW : -42.29 % |

| BNS.PR.P | FixedReset | 45,108 | RBC crossed 24,900 at 26.40. YTW SCENARIO Maturity Type : Call Maturity Date : 2013-05-25 Maturity Price : 25.00 Evaluated at bid price : 26.40 Bid-YTW : 3.17 % |

| There were 35 other index-included issues trading in excess of 10,000 shares. | |||

BAM.PR.R, the new FixedReset 5.40%+230 announced January 5 closed today and was able to close well above par on heavy volume. The issue traded 614,165 shares in a range of 24.95-30 before closing at 25.26-30, 8×61.

Vital statistics are:

| BAM.PR.R | FixedReset | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2040-01-14 Maturity Price : 23.17 Evaluated at bid price : 25.26 Bid-YTW : 4.89 % |

BAM.PR.R is tracked by HIMIPref™. It has been added to the FixedResets subindex.

DBRS has released its Global Methodology for Rating Banks and Banking Organisations that has some snippets of interest for preferred share investors:

DBRS notes that the regulatory focus on Tier 1 capital is evolving with increased focus on core Tier 1 capital that excludes hybrids. We will adjust our methodology in the future to reflect any changes in emphasis or requirements.

…

To assess leverage, another capital measure that we employ is the ratio of Tier 1 capital to tangible assets. This ratio, or a variation of it, is applied to banks in a number of countries. It is generally more constraining than the Basel ratios, as assets are not risk-adjusted, although no adjustment is made for off-balance sheet exposures. We anticipate that there is likely to be pressure for adoption of some variation on this leverage ratio in more countries in the aftermath of the crisis.Taking advantage of the regulatory risk weightings, DBRS considers the ratio of tangible common equity to RWA. Refl ecting DBRS’s preference for equity over hybrids as a cushion for bondholders and other senior creditors, this ratio excludes the hybrid securities that are given full weight by the regulators, up to certain limits.

In the light of Sheila Bair’s testimony to the Crisis Committee, the following extract is interesting:

By their nature, however, these businesses, if poorly run with inadequate risk management, can detract from a bank’s strengths and constrain its ratings. It is worth noting again that while banks had extraordinary losses in their trading businesses in this cycle, most of the losses were concentrated in few business lines, primarily in certain areas of fi xed income, related to origination, structuring and packaging various forms of credit and more complex securities. Risk management of trading activities was predominantly successful in helping banks generate revenues and earnings across many of their trading businesses. The analysis focuses on the trading and other capital markets businesses, but does not ignore other exposures to market risk.

The National Post had an article on preferreds yesterday by Eric Lam And David Pett, Reset preferred shares fill trust gap with all the incisive, hard-hitting reporting that made the National Post what it is today: bankrupt:

John Nagel, vice-president at Desjardins Securities, preferred shares department, and one of the creators of reset preferreds, said the shares give investors much more flexibility.

“The very low interest-rate scenario that we’re in … if rates are a lot higher five or six years from now, there’s the option of going floating or being redeemed. That’s very attractive,” he said.

Flexibility? The redemption option belongs to the issuer. The holder – if not redeemed – has the relatively trivial opportunity to choose between fixed and floating. The flexibility that counts belongs to the issuer.

To date, almost all of the reset preferreds have gained in value from the price they were originally issued. That represents an added bonus for investors who got in early, but it also presents a particular challenge for investors looking to get in on the action now as they may face lower yields and the potential for large capital losses as shares get redeemed on the reset date at par.

Clearly, it’s important to think about the exit strategy right from the beginning.

“When you buy it, assume the worst,” Mr. Nagel said.

“The secret is to look at these six months or nine months ahead of [maturity], and make a decision. If you think they’re going to be redeemed, you should sell.”

Sell to whom? At what price?

If the bond yield has risen substantially, the issuer is likely going to redeem the shares to prevent you from cashing in on the elevated rates.

This part is nonsense. The redemption decision will have everything to do with credit spreads on the market – can they borrow on more attractive terms? – and virtually nothing to do with the absolute value of “bond yield” – assuming that by “bond” they mean five-year Canadas.

On the other hand, if the bond yield is low and it looks like the shares will be reset, the best bet — available in the vast majority of cases — is to convert to floating rate preferred shares, which are usually pegged to the Government of Canada three-month treasury bills plus the spread.

Hopeless nonsense. In a normal environment, a five year bond will outperform treasury bills bought and rolled for a five-year term. Not always, but more often than not.

Investors should remember that while FixedResets can certainly mitigate the effects of a rise in yields, you pay through the nose for that benefit; the bond market, as a whole, ascribes zero value to this benefit. And the credit risk is forever. Should Bad Things happen to Groupe Aeroplan – although it is hard to imagine bad things happening to a company that combines air travel with green stamp savings books – they will not be able to refinance at +375, not redeem, and the prefs will be trading at a big discount.

Sheila Bair of the FDIC has testified to the Financial Crisis Inquiry Commission:

In the 20 years following FIRREA and FDICIA, the shadow banking system grew much more quickly than the traditional banking system, and at the onset of the crisis, it’s been estimated that half of all financial services were conducted in institutions that were not subject to prudential regulation and supervision. Products and practices that originated within the shadow banking system have proven particularly troublesome in this crisis.

…

As a result of their too-big-to-fail status, these firms were funded by the markets at rates that did not reflect the risks these firms were taking.

I don’t think it’s as cut-and-dried as that, unless she’s talking about the GSEs – which she might be. If investors underestimated risk – or estimated it correctly but got caught on the wrong side of a bet – it does not follow that they did so in the expectation of a bail-out.

This growth in risk manifested itself in many ways. Overall, financial institutions were only too eager to originate mortgage loans and securitize them using complex structured debt securities. Investors purchased these securities without a proper risk evaluation, as they outsourced their due diligence obligation to the credit rating agencies.

…

Consumers and businesses had vast access to easy credit, and most investors came to rely exclusively on assessments by a Nationally Recognized Statistical Rating Agency (credit rating agency) as their due diligence. There became little reason for sound underwriting, as the growth of private-label securitizations created an abundance of AAA-rated securities out of poor quality collateral and allowed poorly underwritten loans to be originated and sold into structured debt vehicles. The sale of these loans into securitizations and other off-balance-sheet entities resulted in little or no capital being held to absorb losses from these loans. However, when the markets became troubled, many of the financial institutions that structured these deals were forced to bring these complex securities back onto their books without sufficient capital to absorb the losses. As only the largest financial firms were positioned to engage in these activities, a large amount of the associated risk was concentrated in these few firms.

Much of this is just fashionable slogan-chanting, but it is interesting to see how the rating agency problem is cast: in terms of investors outsourcing their due diligence rather than as evil rating agencies inflating their output. This is an encouraging sign, putting the onus squarely on the investors – in stark contrast to Angelides ill-advised remarks yesterday, which implied that securities firms have a responsibility to sell only products that go up.

The GSEs became highly successful in creating a market for investors to purchase securities backed by the loans originated by banks and thrifts. The market for these mortgage-backed securities (MBSs) grew rapidly as did the GSEs themselves, fueling growth in the supporting financial infrastructure. The success of the GSE market created its own issues. Over the 1990s, the GSEs increased in size as they aggressively purchased and retained the MBSs that they issued. Many argue that the shift of mortgage holdings from banks and thrifts to the GSE-retained portfolios was a consequence of capital arbitrage. GSE capital requirements for holding residential mortgage risk were lower than the regulatory capital requirements that applied to banks and thrifts.

This growth in the infrastructure fed market liquidity and also facilitated the growth of a liquid private-label MBS market, which began claiming market share from the GSEs in the early 2000’s. The private-label MBS (PLMBS) market fed growth in mortgages backed by jumbo, hybrid adjustable-rate, subprime, pay-option and Alt-A mortgages.

…

These mortgage instruments, originated primarily outside of insured depository institutions, fed the housing and credit bubble and triggered the subsequent crisis. In addition, the GSEs – Fannie Mae, Freddie Mac, and the Federal Home Loan banks, were major purchasers of PLMBS.

In conjunction with her deprecation of investor acuity, this is a very interesting observation indeed!

During the 1990s, much of the underlying collateral for private-label MBSs was comprised of prime jumbo mortgages—high quality mortgages with balances in excess of the GSE loan limits. During this period, the securitizing institution would often have to retain the risky tranches of the structure because there was no active investor market for these securities.

…

However, the lack of demand for the high-risk tranches limited the growth of private-label MBSs. In response, the financial industry developed two other investment structures—collateralized debt obligations (CDOs) and structured investment vehicles (SIVs). These structures were critical in creating investor demand for the high-risk tranches of the private-label MBSs and for creating the credit-market excesses that fueled the housing boom.

With these high ratings, MBS, CDO, and SIV securities were readily purchased by institutional investors because they paid higher yields compared to similarly rated securities. In some cases, securities issued by CDOs were included in the collateral pools of new CDOs leading to instruments called CDOs-squared. The end result was that a chain of private-label MBS, CDO and SIV securitizations allowed the origination of large pools of low-quality individual mortgages that, in turn, allowed over-leveraged consumers and investors to purchase over-valued housing. This chain turned toxic loans into highly rated debt securities that were purchased by institutional investors. Ultimately, investors took on exposure to losses in the underlying mortgages that was many times larger than the underlying loan balances. For regulated institutions, the regulatory capital requirements for holding these rated instruments were far lower than for directly holding these toxic loans.

The crisis revealed two fatal problems for CDOs and SIVs. First, the assumptions that generated the presumed diversification benefits in these structures proved to be incorrect. As long as housing prices continued to post healthy gains, the flaws in the risk models used to structure and rate these instruments were not apparent to investors. Second, the use of short-term asset-backed commercial paper funding by SIVs proved to be highly unstable. When it became apparent that subprime mortgage losses would emerge, investors stopped rolling-over SIVs commercial paper. Many SIVs were suddenly unable to meet their short-term funding needs. In turn, the institutions that had sponsored SIVs were forced to support them to avoid catastrophic losses. A fire sale of these assets could have cascaded and caused mark-to-market losses on CDOs and other mortgage-related securities.

OK, so we’ve identified two problems:

Unfortunately, her proposed solution actually exacerbates the problem:

For instance, loan originators and firms that securitize these loans should have to retain some measure of recourse to ensure sound underwriting.

Interestingly:

Looking back, it is clear that the regulatory community did not appreciate the magnitude and scope of the potential risks that were building in the financial system.

For instance, private-label MBSs were originated through mortgage companies and brokers as well as portions of the banking industry. The MBSs were subject to minimum securities disclosure rules that are not designed to evaluate loan underwriting quality. Moreover, those rules did not allow sufficient time or require sufficient information for investors and creditors to perform their own due diligence either initially or during the term of the securitization.

…

Many of the structured finance activities that generated the largest losses were complex and opaque transactions, and they were only undertaken by a relatively few large institutions. Access to detailed information on these activities—the structuring of the transactions, the investors who purchased the securities and other details—was not widely available on a timely basis even within the banking regulatory community.

Repeal Regulation FD!

In the mid-1990s, bank regulators working with the Basel Committee on Banking Supervision (Basel Committee) introduced a new set of capital requirements for trading activities. The new requirements were generally much lower than the requirements for traditional lending under the theory that banks’ trading-book exposures were liquid, marked-to-market, mostly hedged, and could be liquidated at close to their market values within a short interval—for example 10 days.

The market risk rule presented a ripe opportunity for capital arbitrage, as institutions began to hold growing amounts of assets in trading accounts that were not marked-to-market but “marked-to-model.” These assets benefitted from the low capital requirements of the market risk rule, even though they were in some cases so highly complex, opaque and illiquid that they could not be sold quickly without loss. Indeed, in late 2007 and through 2008, large write-downs of assets held in trading accounts weakened the capital positions of some large commercial and investment banks and fueled market fears.

In other words, regulators failed to ensure that the trading book was, in fact, trading and failed to apply a capital surcharge on aged positions.

In 2001, regulators reduced capital requirements for highly rated securities. Specifically, capital requirements for securities rated AA or AAA (or equivalent) by a credit rating agency were reduced by 80 percent for securities backed by most types of collateral and by 60 percent for privately issued securities backed by residential mortgages. For these highly rated securities, capital requirements were $1.60 per $100 of exposure, compared to $8 for most loan types and $4 for most residential mortgages.

Like the market risk rule, this rule change also created important economic incentives that altered financial institution behavior by rewarding the creation of highly rated securities from assets that previously would have been held on balance sheet. For example, as discussed earlier, the production of large volumes of AAA-rated securities backed by subprime and Alt-A mortgages was almost certainly encouraged by the ability of financial institutions holding these securities to receive preferential low capital requirements solely by virtue of their assigned ratings from the credit rating agencies.

In other words, it wasn’t just investors who were outsourcing their due diligence – they were joined by the regulators.

The federal housing GSEs operated with considerably lower capital requirements than those that applied to banks. Low capital requirements encouraged an ongoing migration of residential mortgage credit to these entities and spurred a growing reliance on the originate-to-distribute business models that proved so fragile during the crisis. Not only did the GSEs originate MBSs, they purchased private-label securities for their own portfolio, which helped support the growth in the Alt-A and subprime markets. In 2002, private-label MBSs only represented about 10 percent of their portfolio. This amount grew dramatically and peaked at just over 32 percent in 2005.

Good! A return to the role of the GSEs!

A reserve fund, built from industry assessments, would also provide economic incentives to reduce the size and complexity that makes closing these firms so difficult. One way to address large interconnected institutions is to make it expensive to be one. Industry assessments could be risk-based. Firms engaging in higher risk activities, such as proprietary trading, complex structured finance, and other high-risk activities would pay more.

…

The largest firms that impose the most potential for systemic risk should also be subject to greater oversight, higher capital and liquidity requirements, and other prudential safeguards. Off-balance-sheet assets and conduits, which turned out to be not-so-remote from their parent organizations in the crisis, should be counted and capitalized on the balance sheet.

I like this part, it’s good stuff!

It’s a pity she didn’t develop her attack on the GSEs further: it seems apparent that they were the kings of the too-big-to-fail castle and had very low capital requirements. But, perhaps, she simply wants to lay the groundwork for somebody else to bell the cat.