TransAlta Corporation has announced:

that its Board of Directors has approved a transaction pursuant to which all the currently outstanding first preferred shares in the capital of the Corporation are proposed to be exchanged for shares in a single new series of cumulative redeemable minimum rate reset first preferred shares, series 1, in the capital of the Corporation (the “New Preferred Shares”) pursuant to a plan of arrangement (the “Arrangement”). The terms of the New Preferred Shares will be substantially the same as the terms of the existing first preferred shares with the exception of an adjustment to the reset spread to 5.29%, a change to December 31, 2021 for the next reset date, and the addition of a minimum reset coupon rate of 6.5%.

The Corporation currently has four series of cumulative redeemable rate reset first preferred shares outstanding, being the series A shares, series C shares, series E shares and series G shares, and one series of cumulative redeemable floating rate first preferred shares outstanding, being the series B shares (collectively, the “Existing Preferred Shares”). Pursuant to the Arrangement, the outstanding Existing Preferred Shares will be exchanged for New Preferred Shares at an exchange ratio specific to each series of Existing Preferred Shares.

The Arrangement is expected to provide several benefits to holders of Existing Preferred Shares including:

- dividend volatility will be minimized as a result of the downside protection provided under the terms of the New Preferred Shares, which will include a “minimum floor” mechanism pursuant to which holders of the New Preferred Shares will have certainty that the reset coupon rate will be no lower than 6.50%;

- the dividends to be paid to holders of the New Preferred Shares are expected to be greater than the current dividends received by holders of the Existing Preferred Shares over the initial five-year reset period based on current interest rate levels;

- trading liquidity is expected to be enhanced, as the consolidation of the Existing Preferred Shares into one series of New Preferred Shares is expected to provide holders of New Preferred Shares with more flexibility and depth in the market to buy and sell such New Preferred Shares; and

- the exchange of Existing Preferred Shares for New Preferred Shares will constitute an automatic tax deferred exchange for Canadian income tax purposes. The Arrangement will, however, provide holders of Existing Preferred Shares with an option, at their election, to have the exchange occur in a manner which may allow a shareholder to realize a capital gain or a capital loss for Canadian income tax purposes.

The Arrangement is also expected to benefit TransAlta by:

reducing the Corporation’s notional capital balance of preferred shares by approximately $300 million, which strengthens the balance sheet and improves certain financial ratios; and

- providing future preferred share issuance capacity based on the equity treatment guidelines of the Corporation’s credit rating agencies.

Pursuant to the Arrangement, (i) holders of series A shares will receive 0.503 of a New Preferred Share; (ii) holders of series B shares will receive 0.550 of a New Preferred Share; (iii) holders of series C shares will receive 0.705 of a New Preferred Share; (iv) holders of series E shares will receive 0.790 of a New Preferred Share; and (v) holders of series G shares will receive 0.820 of a New Preferred Share. The New Preferred Shares will pay fixed cumulative dividends of $1.625 per share per annum, yielding 6.5% per annum, payable on the last business day of March, June, September and December of each year, as and when declared by the Board of Directors of TransAlta. The dividend rate will be reset on December 31, 2021 and every five years thereafter at a rate equal to the sum of the then five-year Government of Canada bond yield and 5.29%, provided that, in any event, such calculated rate shall not be less than 6.50%. The New Preferred Shares will be redeemable by TransAlta, at its option, on December 31, 2021 and on December 31 in every fifth year thereafter.

The Corporation will deliver an information circular, describing the proposed Arrangement in greater detail, to holders of Existing Preferred Shares entitled to vote in connection with the Arrangement, with a view to completing the Arrangement in the first quarter of 2017. Holders of Existing Preferred Shares are encouraged to review the information circular as it includes important information pertaining to the Arrangement.

The closing of the Arrangement will be subject to various conditions to be set out in the information circular, including: (i) the approval of not less than two-thirds of the votes cast in person or by proxy at a special meeting of holders of each series of Existing Preferred Shares; (ii) approval of the Arrangement by the Court of Queen’s Bench of Alberta; and (iii) any required regulatory approvals, including the listing of the New Preferred Shares on the Toronto Stock Exchange.

PricewaterhouseCoopers LLP has provided its fairness opinion that the Arrangement is fair, from a financial point of view, to holders of each series of Existing Preferred Shares. Based on the fairness opinion and after consulting with its financial and legal advisors, among other considerations, the Board of Directors of the Corporation (i) has unanimously determined that the Arrangement is in the best interests of the Corporation; (ii) has unanimously determined that the Arrangement is fair to the holders of each series of Existing Preferred Shares; and (iii) recommends that holders of each series of Existing Preferred Shares vote in favour of the Arrangement. In connection with the Arrangement, CIBC World Markets Inc. acted as the financial advisor to the Corporation and Norton Rose Fulbright Canada LLP acted as legal counsel to the Corporation.

DBRS has assigned the new issue a provisional Pfd-3 Trend-Negative rating.

The market seemed to like the proposed exchange, with TA preferred issues jumping in price:

| Ticker |

Bid

12/16 |

Bid

12/19 |

Change |

Implied

New Issue

Price |

| TA.PR.D |

11.91 |

12.26 |

+2.94% |

24.37 |

| TA.PR.E |

11.40 |

13.00 |

+14.04% |

23.63 |

| TA.PR.F |

15.59 |

17.05 |

+9.36% |

24.18 |

| TA.PR.H |

16.97 |

19.07 |

+12.37% |

24.14 |

| TA.PR.J |

18.07 |

19.70 |

+9.02% |

24.02 |

So it looks as if prices instantly adjusted on the day to reflect a $25 trading price for the new issue, less a deal-risk discount of about 4%. So far, this is normal and unobjectionable.

The objectionable part of this plan becomes clear once we start looking at the Implied Volatility of the FixedResets. One thing is very clear: given the higher coupon on the new issue, it may be expected to trade at a much higher price than the issues it replaces – regardless of the exact level, it will also be clear that there is therefore much less potential upside (if spreads narrow), if any, before the issue gets called, while the downside (if spreads should widen) is more or less the same. Normally, as is formally explained by the theory of Implied Volatility, the reduced chance of an upside win is offset by a higher yield, which will result in increased income if spreads remain stagnant.

This deal takes away that upside, without compensation.

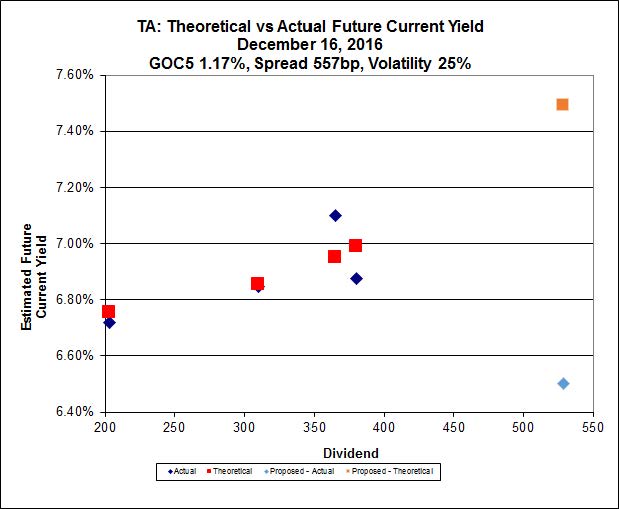

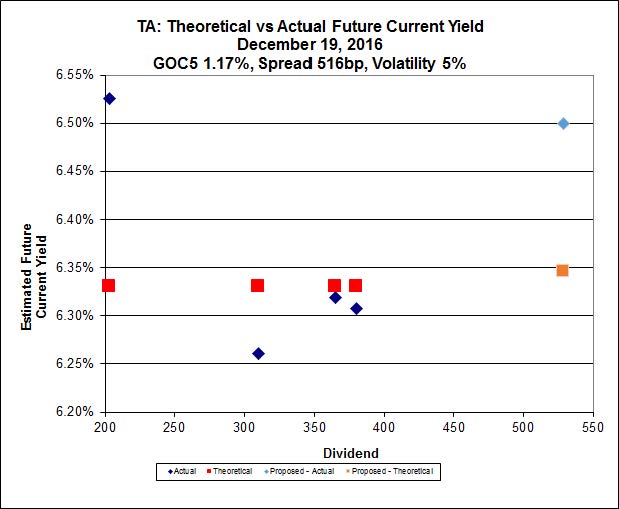

For instance lets look at the Implied Volatility of the TA series of FixedResets as of last Friday:

Click for Big

Click for BigThe curve has been fit using the four extant FixedReset issues only (TA.PR.E is a FloatingReset). We can see that in order to be consistent with four extant issues, the new issue should yield about 7.5%, whereas in fact it only yields about 6.5%. In this model, the fair price for the new issue is about 21.69 and purchasers of the TA shares at the new level are going to be awfully disappointed.

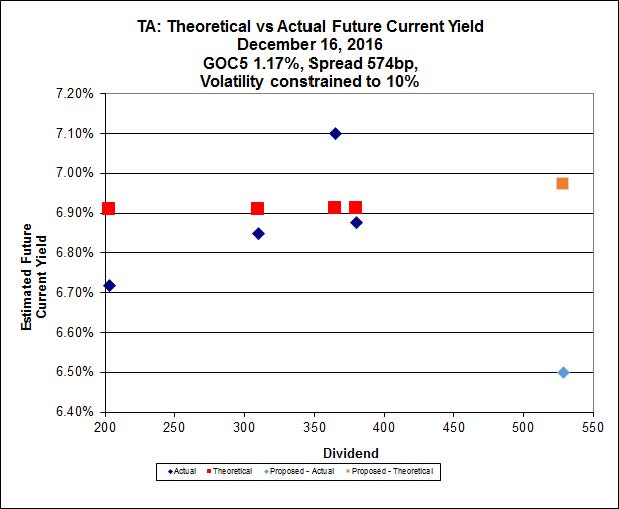

It may certainly be objected that the derived level of Implied Volatility in the above analysis is unwarrantably high at 25% and I have certainly not been shy about stating in the past that I consider a reasonable value to be in the high single digits. So let’s re-run the analysis, constraining Implied Volatility to be 10%. We get:

Click for Big

Click for BigEven with this constraint, we see that in order to be consistent with Friday’s closing bids for the extant issues the new issue should offer a yield of just under 7.0% – compared to the 6.5% actually offered – which in turn implies that the free trading price of the new issue is predicted to be about 23.30 … again, purchasers of the TA shares at the new level are going to be disappointed.

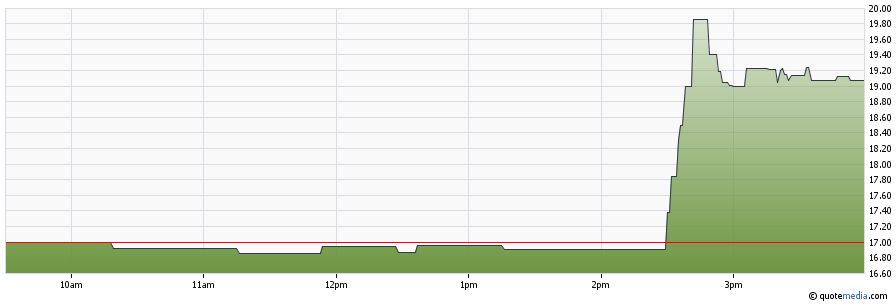

Finally, we can look at the Implied Volatility analysis with end of day prices. Obviously, as shown in the table above, there was a very large move in the prices of these issues. This happened very quickly as illustrated in the day’s chart for TA.PR.H:

Click for Big

Click for Big… and the day’s action has changed the Implied Volatility analysis to:

Click for Big

Click for BigIt is only in this analysis that we may conclude that the new issue is well-priced, as the theoretical yield for consistency is only 6.35% compared to the actual offer of 6.50%.

All of this analysis leads to the conclusion that this is a rotten deal for the preferred shareholders, so rotten that we may call it a sleazy attempt by the company to pull the wool over the eyes of unsophisticated retail investors. As the company admits, they look forward to:

reducing the Corporation’s notional capital balance of preferred shares by approximately $300 million

That $300-million is money that currently can potentially be earned by the current shareholders with price increases on the extant issues; price increases that could result from an increase in the GOC-5 yield, or from straightforward spread narrowing. The company is giving up nothing – NOTHING! – in order to capture this entire amount for themselves.

But, whimpers the incompetent dork from PriceWaterhouseCoopers who signed his name to the fairness opinion, we are giving up something!

the dividends to be paid to holders of the New Preferred Shares are expected to be greater than the current dividends received by holders of the Existing Preferred Shares over the initial five-year reset period based on current interest rate levels.

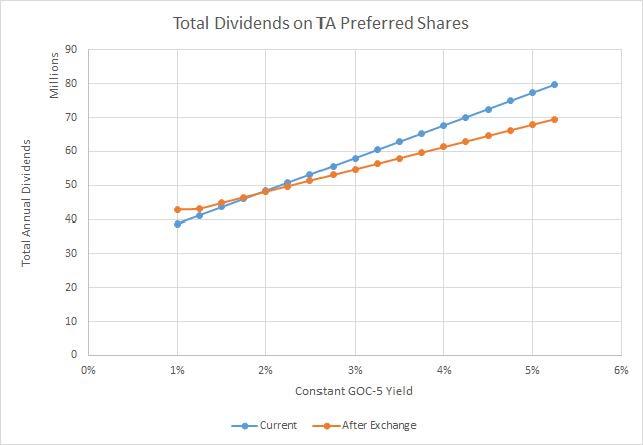

Sure, based on current interest rate levels. But my vast experience in fixed income has led me to the arcane knowledge that interest rate levels do not always remain constant – however convenient it might be for analysis to assume that they do – and that we should at least be aware of what happens in various scenarios. So with the aid of a handy xlsx MS-Excel spreadsheet we can draw a graph of what will happen if the GOC-5 yield changes:

Click for Big

Click for BigYes, that’s right: preferred shareholders will get a little extra income after the Exchange for as long as the GOC-5 yield is under 2%. Once they rise above that, though, the Exchange makes them worse off. There is no compensation in this deal for the reduction of potential income in the event that yields rise. Whether yields rise in the future is a matter of opinion, snivel the directors who claim this is fair to shareholders … but with the North American economy beginning to show signs of life, it will be very hard to find takers for bets they’ll remain constant when these bets are presented straightforwardly and honestly.

So, to put things in a nutshell, Transalta wants to eliminate (more or less) potential capital gains should spreads narrow in the future, and reduce potential income increases should GOC-5 yields increase in the future; all this for a very, very tiny increase in current income. Hell, why not send them the deed to your house and car, while you’re at it?

This is a shitty deal for shareholders. Vote No. I will note that as a matter of practicalities, the idea of selling into this stupidly inflated market and becoming indifferent to how this abusive deal turns out is also quite attractive.

Update, 2016-12-24 I was perplexed by a comment on Financial Wisdom Forum:

More on the TransAlta exchange.

http://business.financialpost.com/news/ … picks=true

FWIW, I am quite satisfied with the offer because I’m a trader and am more than happy to bail on these PF-3 issues because I really believe that one would have to be wearing super sized rose coloured glasses to think that they would someday trade or be redeemed at par, especially with a company like TA that has slashed the dividend on the common to 4 cents/quarter.

The case for the “No” vote does not depend on the hope that the shares will “someday trade or be redeemed at par”, and demonstrating this should actually make the argument more clear for those who have difficulty with the concept of Implied Volatility.

Let us examine the specific case of TA.PR.D; the following analysis framework may be applied to the other series with changes in numbers.

TA.PR.D:

- pays $0.67725 p.a. until the next Exchange Date

- will reset to GOC-5 + 203bp (paid on par value of $25) on each Exchange Date

- This is equal to (25 * GOC-5) + (25 * 203bp)

- which is equal to (25 * GOC-5) + $0.5075

- may be redeemed at $25 on each Exchange Date

- Exchange Dates are 2021-3-31 and every five years thereafter

The company proposes to exchange each share of this for 0.503 of a New Preferred Share; each New Preferred Share will

- Pay 6.50% of $25.00 = 1.625 until the next Exchange Date

- will reset to GOC-5 + 529bp (paid on par value of $25) on each Exchange Date

- may be redeemed at $25 on each Exchange Date

- Exchange Dates are 2021-12-31 and every five years thereafter

The fact that holders will be getting only 0.503 New Preferred Shares for each share of TA.PR.D makes the changes a little more complex for many investors, so as a thought experiment, let’s design a Notional Share which we will assume will be offered 1 for 1 for TA.PR.D, with the new holdings, in total, having exactly the same characteristics as the proposed new holdings of the New Preferred Shares.

A Notional Preferred Share:

- pays $0.817375 until the next Exchange Date

- will reset to 0.503 (GOC-5 + 529bp) * 25 on each Exchange Date

- This is equal to (0.503 * 25 * GOC-5) + (0.503 * 25 * 529bp)

- which is equal to 12.575 * GOC-5 + $0.6652175

- subject to a minimum rate of $0.817375

- may be redeemed at $12.575 on each Exchange Date

- Exchange Dates are 2021-12-31 and every five years thereafter

So when we compare the currently held TA.PR.D to the Notional Share we see that:

- The Notional Share will pay an extra $0.14 annually for each of the next five years (approximately), for a total of $0.70.

- The redemption price will drop from $25 to $12.575

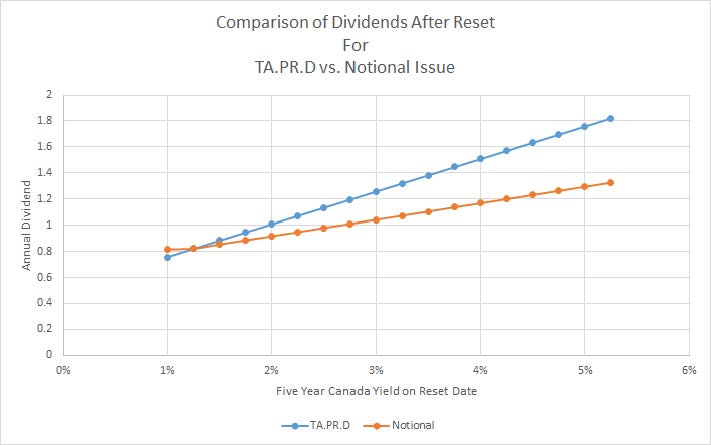

- The dividends after the next Exchange Date (if it is left outstanding) will depend on the GOC-5 yield, as indicated on the following chart

Click for Big

Click for BigThe big problem, of course, is the change in redemption price – holders lose out on a lot of potential capital gains if the market improves, either through increases in the GOC-5 yield (which should increase the trading price of the preferreds) or through a narrowing of spreads (which may occur because the market improves, or TA’s credit improves, or both). In addition, we see that increases in the GOC-5 rate greatly improve the dividend payout from TA.PR.D and the much higher redemption price means these potential increases will not be called away unless for a gigantic premium over the current price.