A paper by Nicholas Labelle, Varya Taylor titled Removal of the Unwinding Provisions in the Automated Clearing Settlement System: A Risk Assessment is interesting:

A default in the Automated Clearing Settlement System (ACSS) occurs when a Direct Clearer is unable to settle its final obligation. In August 2012, the Canadian Payments Association amended the ACSS by-law and rules to repeal the unwinding provisions from the ACSS default framework. Without unwinding, payment items are no longer returned by the defaulter to the other participants as a means of reducing the defaulter’s final obligation. Instead, the other Direct Clearers (survivors) pay only additional settlement obligations to cover the defaulter’s shortfall. To assess the potential exposures of an ACSS default without unwinding, we use simulations to estimate the value of additional settlement obligations for each survivor and compare these exposures to their capital and liquid assets. Results indicate that these exposures are indeed manageable by survivors and, therefore, that the ACSS does not pose systemic risk.

The global economy still looks lousy:

Today’s report from the IMF highlights, in particular, the struggles of the euro zone and the still-uneven recovery in the United States after a brutal winter, as well as the troubles in emerging markets.

In the update to its earlier world economic outlook, released in Mexico City, the IMF now forecasts that Canada’s economy will grow by 2.2 per cent this year, down marginally from its April forecast of 2.3 per cent. It held its 2015 outlook for Canada steady at 2.4 per cent.

Despite the trim, Canada’s economy will be outpaced this year among the G7 nations only by Britain, at 3.2 per cent. Next year, according to the forecast both Britain and the United States will outstrip Canada, at 2.7 per cent and 3 per cent, respectively.

The IMF forecast puts the spotlight on the euro zone, where Germany’s economy is projected to grow by 1.9 per cent this and 1.7 per cent in 2015, France by 0.7 per cent and 1.4 per cent, and Italy, by 0.3 per cent and 1.1 per cent.

Japan will also lag, at 1.6 per cent and 1.1 per cent.

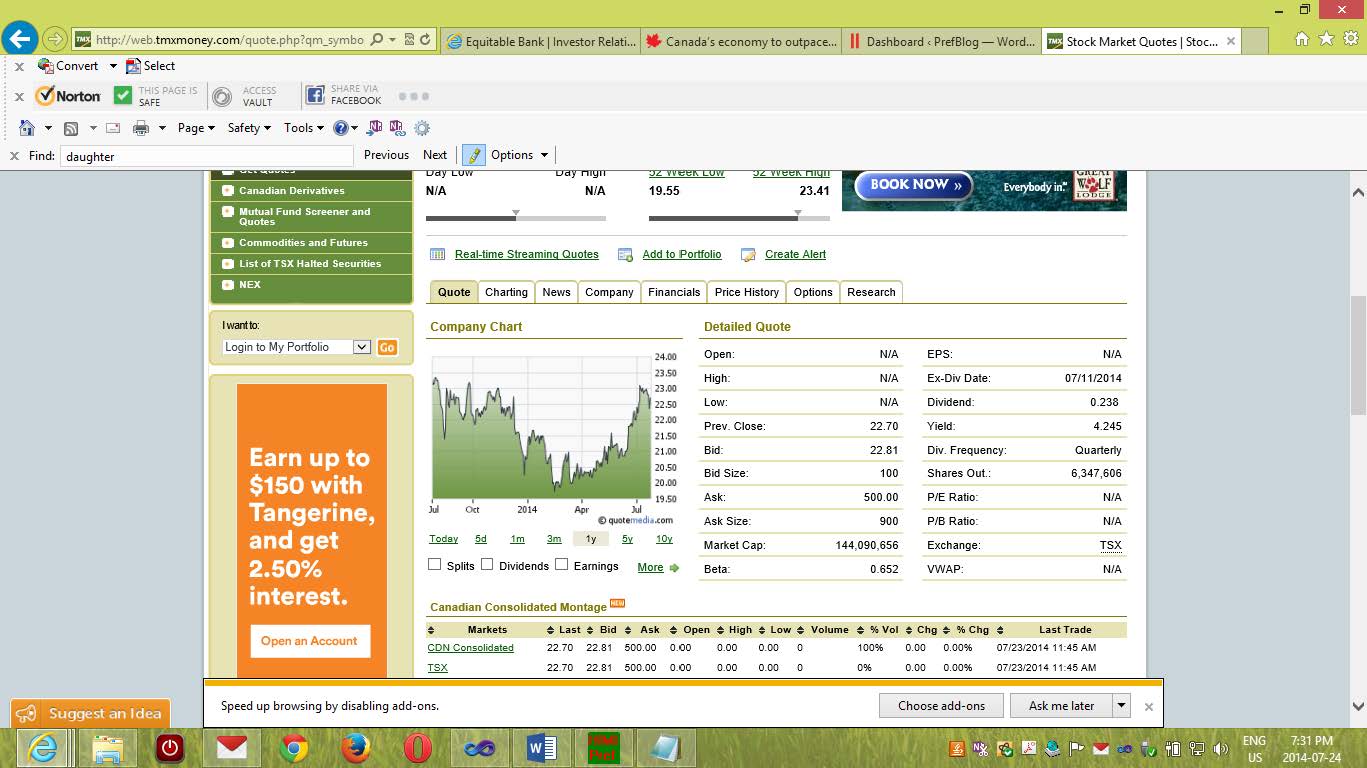

Well, it looks like we have a winner for Quote of the Day!

Click for Big

Yes, that’s right, BAM.PR.G is quoted at 22.81-500.00, 1×9. Timestamped details are not yet available from the Toronto Stock Exchange, so it’s not clear whether this is due to a moronic market-maker, or to the TMX’s moronic practice of reporting the ‘last’ quote rather than the closing quote. I have followed my usual practice in such cases and reset the ask price used by HIMIPref™ to $1 above the bid.

Update: I’ve checked it out, buying all ‘Trades and Quotes’ between 3:55pm and 4:00pm. The only entry in the file is a quote timestamped 15:59:45, 22.81-500.00, 1×1. So what we have here, people, is a lackadaisical market-maker

It was a modestly negative day for the Canadian preferred share market, with PerpetualDiscounts flat, FixedResets down 8bp and DeemedRetractibles off 3bp. Volatility was negligible. Volume was average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 3.09 % | 3.07 % | 19,802 | 19.49 | 1 | -0.4098 % | 2,574.3 |

| FixedFloater | 4.16 % | 3.40 % | 29,083 | 18.65 | 1 | 0.4846 % | 4,165.7 |

| Floater | 2.86 % | 2.95 % | 46,302 | 19.85 | 4 | -0.3118 % | 2,776.8 |

| OpRet | 4.02 % | -2.74 % | 79,535 | 0.08 | 1 | -0.5462 % | 2,719.0 |

| SplitShare | 4.25 % | 3.86 % | 52,079 | 4.01 | 6 | 0.0398 % | 3,121.7 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5462 % | 2,486.2 |

| Perpetual-Premium | 5.52 % | -5.27 % | 82,840 | 0.09 | 17 | 0.0878 % | 2,432.0 |

| Perpetual-Discount | 5.23 % | 5.09 % | 109,492 | 15.24 | 20 | 0.0000 % | 2,584.9 |

| FixedReset | 4.40 % | 3.59 % | 199,507 | 8.60 | 77 | -0.0843 % | 2,557.4 |

| Deemed-Retractible | 4.98 % | 0.08 % | 122,672 | 0.09 | 43 | -0.0333 % | 2,553.4 |

| FloatingReset | 2.66 % | 2.13 % | 94,093 | 3.82 | 6 | -0.0787 % | 2,518.8 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BAM.PF.A | FixedReset | -1.08 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2018-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.53 Bid-YTW : 4.04 % |

| BMO.PR.S | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-07-24 Maturity Price : 23.30 Evaluated at bid price : 25.41 Bid-YTW : 3.70 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| GWO.PR.Q | Deemed-Retractible | 303,100 | Scotia crossed 298,800 at 24.95. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 5.25 % |

| RY.PR.H | FixedReset | 268,050 | Nesbitt crossed 153,100 and two blocks of 50,000 each, all at 25.26. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-07-24 Maturity Price : 23.22 Evaluated at bid price : 25.20 Bid-YTW : 3.59 % |

| ELF.PR.H | Perpetual-Discount | 202,900 | Nesbitt crossed 200,000 at 24.85. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-07-24 Maturity Price : 24.38 Evaluated at bid price : 24.81 Bid-YTW : 5.56 % |

| GWO.PR.P | Deemed-Retractible | 199,660 | TD crossed blocks of 75,000 shares, 35,000 and 85,000, all at 25.80. YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-31 Maturity Price : 25.25 Evaluated at bid price : 25.80 Bid-YTW : 5.01 % |

| BAM.PF.F | FixedReset | 136,300 | Nesbitt crossed 125,000 at 25.45. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-07-24 Maturity Price : 23.29 Evaluated at bid price : 25.45 Bid-YTW : 4.21 % |

| GWO.PR.S | Deemed-Retractible | 90,600 | RBC crossed 84,700 at 25.60. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.56 Bid-YTW : 5.12 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.C | Deemed-Retractible | Quote: 22.89 – 23.30 Spot Rate : 0.4100 Average : 0.2493 YTW SCENARIO |

| BAM.PR.G | FixedFloater | Quote: 22.81 – 23.81 Spot Rate : 1.0000 Average : 0.8542 YTW SCENARIO |

| IAG.PR.A | Deemed-Retractible | Quote: 23.20 – 23.68 Spot Rate : 0.4800 Average : 0.3518 YTW SCENARIO |

| BNS.PR.B | FloatingReset | Quote: 25.37 – 25.62 Spot Rate : 0.2500 Average : 0.1463 YTW SCENARIO |

| VNR.PR.A | FixedReset | Quote: 25.33 – 25.68 Spot Rate : 0.3500 Average : 0.2571 YTW SCENARIO |

| MFC.PR.B | Deemed-Retractible | Quote: 23.40 – 23.70 Spot Rate : 0.3000 Average : 0.2073 YTW SCENARIO |