So the banks are taking advantage of the anti-competitive Bank Act ownership provisions to increase their mortgage margins as well as their margins on Prime:

But now, all in mortgage-land are waiting and wondering if Canada’s major banks will actually pass along that rate cut. The Globe and Mail’s Streetwise reported Wednesday that TD Canada Trust may not reduce its prime rate. (TD sent me a statement this morning confirming that it is not changing prime rate “at this time.”)

…

We’re in a different world this time around. The average home price is 44 per cent higher than 2008, debt levels are at a record, bank revenue is pressured by multi-year lows in mortgage growth, competition has shrunk net interest margins and Ottawa had burdened banks with heaps of regulatory, capital and securitization restrictions. That makes banks and the federal government quite reluctant to see a lower prime rate.The housing policy factor cannot be underestimated, not with the Bank of Canada admitting that certain regions’ home values may be up to 30 per cent overvalued. I spoke with one capital markets executive Thursday. He said, “I wouldn’t be surprised if the Bank of Canada called all the major banks and said, ‘Don’t use this rate cut as fuel to get more debt in consumers’ hands by lowering rates.”

Yes, if there were more banks, then the bureaucrats at the BoC and the politicians would have to make more than six calls, which would be too much like work. After all, when you’re busily micro-managing the economy and it turns out you need a two-tier interest rate policy like any other proud member of the third world, you don’t have time to waste talking.

Regrettably, there still a few members of the private sector who have not yet been re-educated:

Mortgage brokers, however, say it is only a matter of time – anywhere from a few days to a few weeks – before banks start slashing their rates, with some predicting that as Government of Canada bond yields plummet below 1 per cent, five-year fixed rates could hit a new record-low 2.5 per cent, reigniting a fierce competition for new borrowers.

…

Some small non-bank lenders have already begun cutting their fixed-mortgage offerings, said Drew Donaldson, a mortgage broker and executive vice-president Safebridge Financial Group. Consumers with variable-rate mortgages and preapprovals have been calling Mr. Donaldson’s office in droves looking to find out when their rates might drop.

…

Some industry officials say that while banks will inevitably be forced to drop their fixed mortgage rates if bond yields settle at record lows, they may put off dropping their prime rate, which affects variable-rate mortgages along with a host of non-mortgage lending, such as car loans and personal lines of credit, in order to protect their non-mortgage profits and push borrowers toward longer-term fixed rate mortgage contracts.Others speculated that federal regulators may be pressuring banks not to lower their rates too drastically by warning that they could introduce tighter lending rules to avoid driving up already high levels of household debt.

…

But with the average five-year rate among the major banks now sitting around 195 basis points above five-year government bond yields, well above the historical range of between 150 and 160 basis points, most expect the banks to eventually bow to consumer pressure to slash their rates, sending potential buyers running back into the housing market.“You’ll definitely get more interest in homebuying when you see rates go below 2.5 per cent,” Mr. McLister said.

“It’s going to be a huge flood of buyers.”

It was another violently mixed day for the Canadian preferred share market, with PerpetualDiscounts up 74bp, FixedResets off 11bp and DeemedRetractibles down 20bp. Yet another lengthy Performance Highlights table is predictably dominated by FixedReset and Floating Rate losers and Straight Perpetual winners. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

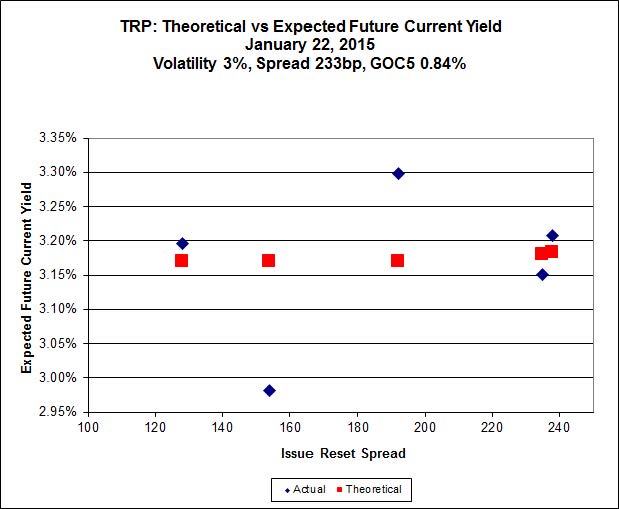

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 20.92, is $0.85 cheap, but it has already reset (at +192). TRP.PR.C, bid at 19.96 and resetting at +154bp on 2016-1-30 is $1.19 rich.

Click for Big

MFC.PR.F continues to be near the line defined by its peers despite its very poor performance today, as Implied Volatility declined dramatically from 30% yesterday to 24% today.

Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

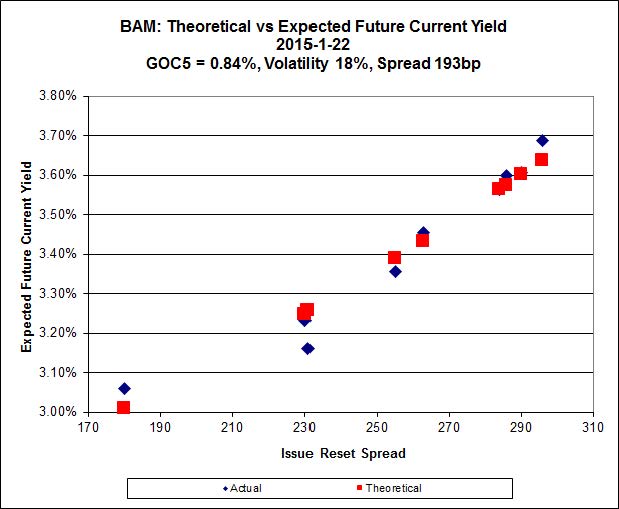

Click for Big

There continues to be cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, which is bid at 21.58 and appears to be $0.36 cheap, while BAM.PR.T, resetting at +231bp 2017-3-31 is bid at 24.92 and appears to be $0.74 rich.

Relative value changes were unusual today: the bid for BAM.PR.X gained $0.07 on the day, while BAM.PR.T’s bid is down $0.28, reinforcing yesterday’s moves. Sell on rumour, buy on news?

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.11, looks $1.04 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 25.32, looks $1.30 expensive and resets 2019-3-1

Click for Big

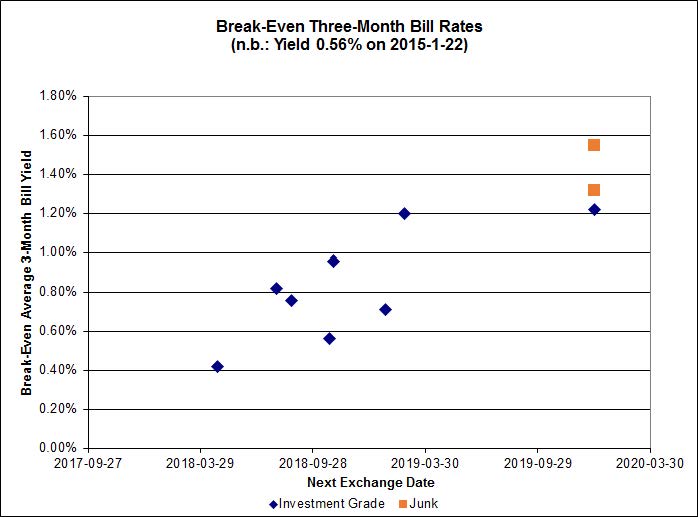

Pairs equivalence is all over the map, but the investment grade pairs (which are presumably more closely watched and easier to trade) do show a rising trend with increasing time to interconversio which, qualitatively speaking, is entirely reasonable. The average break-even rate is way down from recent levels again today, reinforcing yesterday’s move.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -1.5727 % | 2,442.5 |

| FixedFloater | 4.43 % | 3.62 % | 19,586 | 18.25 | 1 | -0.3719 % | 3,987.0 |

| Floater | 3.11 % | 3.27 % | 55,245 | 19.07 | 4 | -1.5727 % | 2,596.5 |

| OpRet | 4.04 % | 1.51 % | 95,980 | 0.40 | 1 | -0.0788 % | 2,755.3 |

| SplitShare | 4.28 % | 4.06 % | 30,290 | 3.61 | 5 | 0.1190 % | 3,194.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0788 % | 2,519.4 |

| Perpetual-Premium | 5.40 % | -9.01 % | 55,918 | 0.09 | 19 | 0.1778 % | 2,517.4 |

| Perpetual-Discount | 5.03 % | 4.91 % | 107,982 | 15.55 | 16 | 0.7393 % | 2,757.6 |

| FixedReset | 4.23 % | 3.18 % | 211,047 | 17.26 | 77 | -0.1115 % | 2,528.3 |

| Deemed-Retractible | 4.91 % | -0.46 % | 101,098 | 0.09 | 39 | -0.1969 % | 2,643.7 |

| FloatingReset | 2.47 % | 2.55 % | 67,443 | 6.46 | 7 | -0.6313 % | 2,407.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BMO.PR.Q | FixedReset | -2.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.92 Bid-YTW : 3.24 % |

| BAM.PR.C | Floater | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 16.05 Evaluated at bid price : 16.05 Bid-YTW : 3.29 % |

| TD.PR.R | Deemed-Retractible | -2.42 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-21 Maturity Price : 25.75 Evaluated at bid price : 25.86 Bid-YTW : -1.57 % |

| FTS.PR.H | FixedReset | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 18.11 Evaluated at bid price : 18.11 Bid-YTW : 3.25 % |

| BAM.PR.K | Floater | -2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 16.02 Evaluated at bid price : 16.02 Bid-YTW : 3.30 % |

| BAM.PR.B | Floater | -1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 16.17 Evaluated at bid price : 16.17 Bid-YTW : 3.27 % |

| TRP.PR.C | FixedReset | -1.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 19.96 Evaluated at bid price : 19.96 Bid-YTW : 3.11 % |

| MFC.PR.F | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.05 Bid-YTW : 4.60 % |

| TD.PR.Q | Deemed-Retractible | -1.65 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-03-02 Maturity Price : 25.50 Evaluated at bid price : 25.57 Bid-YTW : 1.51 % |

| BNS.PR.A | FloatingReset | -1.64 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.65 Bid-YTW : 2.77 % |

| BNS.PR.C | FloatingReset | -1.61 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.52 Bid-YTW : 2.69 % |

| BAM.PR.R | FixedReset | -1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.90 Evaluated at bid price : 24.29 Bid-YTW : 3.39 % |

| PWF.PR.O | Perpetual-Premium | -1.39 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-21 Maturity Price : 26.00 Evaluated at bid price : 26.21 Bid-YTW : -5.99 % |

| TD.PR.P | Deemed-Retractible | -1.31 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-21 Maturity Price : 25.50 Evaluated at bid price : 25.57 Bid-YTW : 0.09 % |

| MFC.PR.B | Deemed-Retractible | -1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.46 Bid-YTW : 5.01 % |

| ENB.PR.P | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 21.88 Evaluated at bid price : 22.29 Bid-YTW : 3.93 % |

| BNS.PR.Z | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.99 Bid-YTW : 3.06 % |

| BAM.PR.T | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.51 Evaluated at bid price : 24.92 Bid-YTW : 3.22 % |

| TRP.PR.B | FixedReset | -1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 16.58 Evaluated at bid price : 16.58 Bid-YTW : 3.28 % |

| BAM.PR.N | Perpetual-Discount | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 22.67 Evaluated at bid price : 22.94 Bid-YTW : 5.21 % |

| GWO.PR.N | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.82 Bid-YTW : 4.98 % |

| POW.PR.G | Perpetual-Premium | 1.12 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2017-04-15 Maturity Price : 26.00 Evaluated at bid price : 27.00 Bid-YTW : 3.64 % |

| SLF.PR.G | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.63 Bid-YTW : 5.14 % |

| BAM.PF.C | Perpetual-Discount | 1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.00 Evaluated at bid price : 23.32 Bid-YTW : 5.24 % |

| CU.PR.F | Perpetual-Discount | 1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.07 Evaluated at bid price : 23.39 Bid-YTW : 4.86 % |

| BAM.PF.D | Perpetual-Discount | 1.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.18 Evaluated at bid price : 23.50 Bid-YTW : 5.25 % |

| CU.PR.G | Perpetual-Discount | 2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.18 Evaluated at bid price : 23.50 Bid-YTW : 4.84 % |

| BNS.PR.R | FixedReset | 3.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.60 Bid-YTW : 3.00 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.I | FixedReset | 197,187 | Desjardins bought blocks of 12,000 shares, 15,000, two of 10,000 each, and 15,900 from RBC, all at 26.20. They also bought blocks of 11,300 shares, 30,000 and 12,900 from TD at the same price. RBC crossed 39,100 at the same price again. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-12-31 Maturity Price : 25.00 Evaluated at bid price : 26.20 Bid-YTW : 1.86 % |

| RY.PR.D | Deemed-Retractible | 101,415 | Nesbitt crossed blocks of 24,500 and 75,000 at 25.55. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-24 Maturity Price : 25.25 Evaluated at bid price : 25.56 Bid-YTW : -13.06 % |

| BNS.PR.Y | FixedReset | 89,041 | Scotia crossed 85,000 at 22.77. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.78 Bid-YTW : 3.34 % |

| RY.PR.Z | FixedReset | 84,220 | Desjardins crossed 75,000 at 25.51. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 23.38 Evaluated at bid price : 25.53 Bid-YTW : 3.00 % |

| ENB.PR.J | FixedReset | 80,120 | RBC crossed blocks of 50,000 and 25,000, both at 23.95. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-22 Maturity Price : 22.78 Evaluated at bid price : 23.85 Bid-YTW : 3.76 % |

| GWO.PR.R | Deemed-Retractible | 61,806 | RBC bought 13,900 from anonymous at 25.00, then crossed 10,000 at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 4.81 % |

| There were 30 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.N | Perpetual-Discount | Quote: 22.94 – 23.95 Spot Rate : 1.0100 Average : 0.6503 YTW SCENARIO |

| GWO.PR.P | Deemed-Retractible | Quote: 25.96 – 26.68 Spot Rate : 0.7200 Average : 0.4961 YTW SCENARIO |

| POW.PR.G | Perpetual-Premium | Quote: 27.00 – 27.68 Spot Rate : 0.6800 Average : 0.4990 YTW SCENARIO |

| CU.PR.F | Perpetual-Discount | Quote: 23.39 – 23.78 Spot Rate : 0.3900 Average : 0.2679 YTW SCENARIO |

| TD.PR.T | FloatingReset | Quote: 24.50 – 25.00 Spot Rate : 0.5000 Average : 0.3879 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 18.11 – 18.49 Spot Rate : 0.3800 Average : 0.2756 YTW SCENARIO |

Nice of TD to advise you they are not dropping their loan rates. They did however react swiftly and cut 25 bps off their “high” interest Investment Savings Accounts such as TDB8150. See https://www.tdassetmanagement.com/solutions/additional-solutions/td-investment-savings-account/index.jsp

GIC rates also went down, surprise, surprise.