TransAlta Corporation has announced:

entered into an investment agreement with TransAlta Renewables Inc. (“TransAlta Renewables”) (TSX: RNW) pursuant to which TransAlta Renewables has agreed to invest in TransAlta’s Australian power generation and gas pipeline portfolio (the “Portfolio”) and fund the remaining project costs for the South Hedland gas-fired project for a combined value of approximately $1.78 billion (the “Transaction”). The Portfolio consists of 575 MW of power generation from six operating assets and the South Hedland project currently under construction, as well as the recently commissioned 270 km gas pipeline. TransAlta Renewables’ investment will consist of the acquisition of securities which track the cash flows of the Portfolio.

“TransAlta created TransAlta Renewables in 2013 to unlock the underlying value in our contracted assets and to fund our growth” said Dawn Farrell, President and CEO. “This transaction highlights the value of our Australian investment strategy, finances the South Hedland plant, generates cash to strengthen our balance sheet and provides greater financial flexibility. The transaction significantly benefits both companies as TransAlta remains the majority shareholder and sponsor of TransAlta Renewables.”

Initially, the Transaction is expected to have a minimal impact on the credit quality of TAC as the Transaction is to be funded with all equity at OpCo. In the medium term, the ratings of TAC will likely be influenced by OpCo’s funding strategy related to the South Hedland gas-fired project under construction which requires a substantial investment of approximately $570 million (approximately $70 million spent in 2014). OpCo is contemplating funding alternatives associated with the South Hedland project. In the interim, the intercompany credit facility increase from TAC gives OpCo time to assess alternatives. DBRS will treat the funding alternative review as an event and assess OpCo’s actions and the resulting impact on TAC’s ratings when the funding plan is finalized.

…

DBRS acknowledges that the new OpCo structure creates another source of equity and could serve as a lower cost of capital for future growth opportunities; however, as TAC’s ownership in OpCo decreases and OpCo’s asset portfolio grows, the integration between TAC and OpCo could weaken. In this case, DBRS will increasingly weigh in on deconsolidated analysis for both TAC and CHD, which could ultimately result in a rating differential between TAC and CHD. TAC’s rating could be pressured if it significantly increases its exposure to construction and development risk as well as merchant risk of greenfield projects, and funds new projects with debt. This may not have a material impact on CHD if OpCo continues to fully hedge power production through PPAs with investment-grade counterparties and maintains reasonable financial metrics. Construction cost overrun risk associated with the South Hedland project is manageable given that the majority of the budgeted investment is either under fixed- price engineering, procurement and construction contracts or fixed fee to the off-taker, Horizon Power, a state government-owned corporation for existing assets.Finally, since the lower-risk assets of TAC have been transferred to OpCo and this trend is expected to continue, holders of TAC’s direct external debt are facing structural subordination risk should OpCo raise a material amount of third-party debt in the future. OpCo has not raised any new external recourse debt since its inception in 2013 as TAC has provided virtually all necessary funding requirements to date. As such, TAC’s rating has not taken meaningful structural subordination effects into account, except outstanding debt related to CHD (which was grandfathered to OpCo at its inception in 2013). TAC’s ratings will likely be affected negatively should OpCo issue a material amount of third-party debt in the future as this will create structural subordination challenges for TAC’s bondholders.

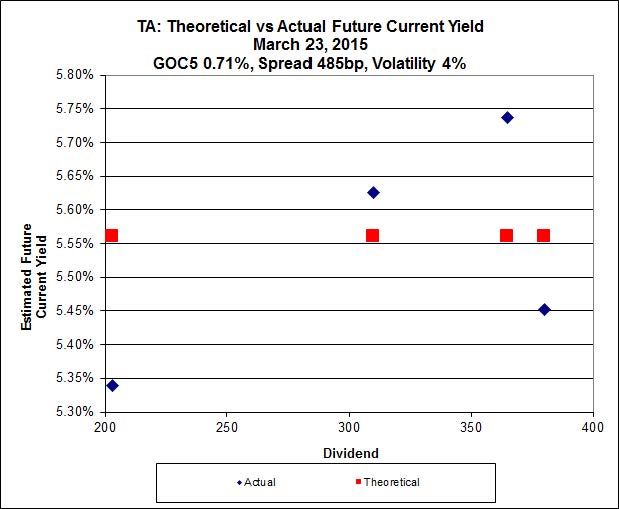

TransAlta has four series of preferreds outstanding, all FixedResets: TA.PR.D, TA.PR.F, TA.PR.H and TA.PR.J.

Implied Volatility gives a murky picture. The Implied Volatility (which is of the Market Reset Spread, remember) is extremely low, but it could be simply that the highest spread issue, TA.PR.J, resetting at +380bp on 2019-9-30, is simply ridiculously expensive and is throwing everything off.

Click for Big