The decimated energy sector has rallied hard off of 20-year lows, pushing Canadian stocks to a decent gain on a day that saw the U.S. market slip.

For the first time since the COVID-19 pandemic consumed global financial markets starting in early March, the S&P/TSX Composite Index meaningfully diverged from U.S. equity benchmarks, with a gain of 2.6 per cent on Tuesday. The S&P 500 index dropped by 1.6 per cent.

Canada’s biggest oil sands players led the advance, adding to a rebound that started on Monday. Over just two trading days, Canadian Natural Resources Ltd. shares have surged by 45 per cent, and Suncor Energy Inc. by 37 per cent.

Potential catalysts for the sudden reversal include expanded federal wage subsidies that would apply to energy sector employees, as well as Tuesday’s announcement that the long-delayed Keystone XL pipeline would go ahead with support from the province of Alberta.

…

For energy companies facing a liquidity crunch, there is hope that lenders will be flexible. “We’re seeing the banks be somewhat understanding,” Mr. Stelmach said. In some cases, lenders are offering extensions and renewals rather than calling in loans.Loan guarantees are also expected to be included in a multibillion-dollar aid package for the oil patch, which Finance Minister Bill Morneau said last week was coming soon. These incremental developments are insufficient to explain the magnitude of the move in Canadian energy stocks so far this week, with the S&P/TSX Capped Energy Index rising by 30 per cent.

There was some talk in trading circles that a big U.S. investor has accumulated shares of Suncor and Canadian Natural Resources over the last couple of days.

…

Wall Street’s three major indexes tumbled on Tuesday, with the Dow registering its biggest quarterly decline since 1987 and the S&P 500 suffering its deepest quarterly drop since the financial crisis on growing evidence of massive economic damage from the coronavirus pandemic.In one of the fastest turns into a bear market, the S&P 500 and the Dow both ended the first quarter more than 20% below the end of 2019, as the health crisis worsened in the United States and brought business activity to a standstill.

It was also the S&P’s biggest first-quarter decline on record as consumers were advised to stay at home, leading businesses to announce temporary closures and massive staff furloughs.

…

The Dow Jones Industrial Average fell 410.32 points, or 1.84%, to 21,917.16, the S&P 500 lost 42.06 points, or 1.60%, to 2,584.59 and the Nasdaq Composite dropped 74.05 points, or 0.95%, to 7,700.10.

Amid draconian efforts to contain the spread of the novel coronavirus, the avalanche of pink slips stemming from the COVID-19 pandemic has only begun. Some economists predict job losses will be nearly three times greater than they were during the Great Recession of 2008-09, and Canada’s unemployment rate could reach 9 per cent by summer.

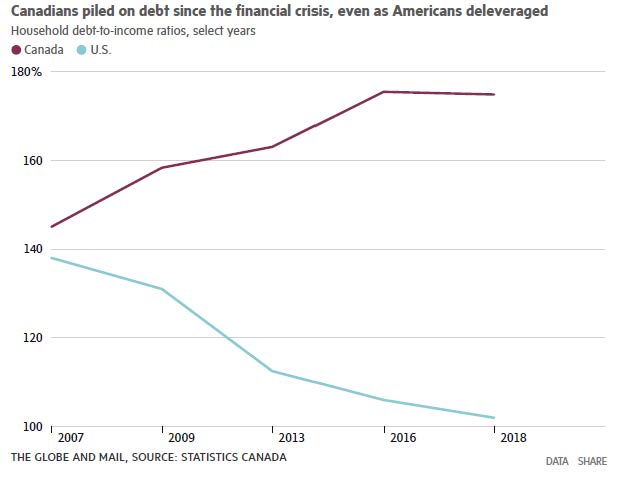

The jarring disruptions caused by COVID-19 threaten to send many Canadian households into financial tailspins. In that scenario, a crisis many policymakers hoped would cause just a sharp but brief economic interruption could morph into a more painful, long-lasting collapse in aggregate demand, reverberating long after pandemic control measures have ended.

Click for Big

And quantitative easing is on the way:

The Bank of Canada is likely to buy about $200 billion of government debt after announcing its first quantitative easing program, which would nearly triple the amount of assets on the central bank’s balance sheet, bond strategists estimate.

Just a few weeks ago, Canada’s central bank was defying the global trend of monetary policy easing. But in a series of emergency interest rate cuts this month it has slashed its key interest rate to 0.25 per cent, the level it regards as the floor.

Quantitative easing, or large-scale buying of assets, is now the policy measure favored by the BoC to ease the economic impact of the coronavirus pandemic.

The bank plans to buy at least $5 billion a week of Government of Canada securities, starting on April 1, with the purchases continuing “until the economic recovery is well underway.”

Regrettably, easing is targetted on liquidity. It does not directly address solvency.

But there’s at least one group with no worries:

A tentative deal between Ontario’s public elementary school teachers and the government comes with an annual wage increase of just 1 per cent but allows boards to hire 434 more educators across the province to support students with special learning needs.

The Elementary Teachers’ Federation of Ontario (ETFO) shared details Monday evening of its recently negotiated deal, which includes a 4-per-cent bump in benefits in each year of the three-year offer – higher than the government originally wanted.

Now, if that’s not the classic contract in the education monopoly, I don’t know what is. A nice tough headline number for the politicians to brag about; a boatload of money slipped in through the back-door for the union to snicker about.

TXPR closed at 468.69, up 2.17% on the day. Volume today was 2.40-million, second-lowest of the past thirty days, ahead of only March 5.

CPD closed at 9.37, up 2.18% on the day. Volume was 161,128, below the average of the past 30 trading days.

ZPR closed at 7.29, up 1.96% on the day. Volume of 674,913 was low in the context of the past 30 trading days.

Five-year Canada yields were down 4bp at 0.59% today.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 3.4739 % | 1,375.7 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 3.4739 % | 2,524.3 |

| Floater | 5.59 % | 5.65 % | 50,804 | 14.42 | 4 | 3.4739 % | 1,454.8 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.6423 % | 3,141.8 |

| SplitShare | 5.28 % | 7.30 % | 79,171 | 3.96 | 7 | 1.6423 % | 3,752.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.6423 % | 2,927.5 |

| Perpetual-Premium | 6.67 % | 6.87 % | 105,336 | 12.68 | 12 | 2.6629 % | 2,568.1 |

| Perpetual-Discount | 6.37 % | 6.58 % | 88,016 | 13.15 | 24 | 2.6737 % | 2,754.6 |

| FixedReset Disc | 7.62 % | 6.32 % | 215,083 | 13.00 | 64 | 3.8063 % | 1,576.6 |

| Deemed-Retractible | 6.14 % | 6.69 % | 103,246 | 12.98 | 27 | 3.0158 % | 2,752.5 |

| FloatingReset | 5.16 % | 5.10 % | 60,812 | 15.25 | 3 | 6.0236 % | 1,687.2 |

| FixedReset Prem | 6.23 % | 6.18 % | 208,665 | 13.56 | 22 | 2.8830 % | 2,180.4 |

| FixedReset Bank Non | 2.01 % | 5.09 % | 130,409 | 1.78 | 3 | -0.9671 % | 2,638.9 |

| FixedReset Ins Non | 7.57 % | 6.48 % | 110,196 | 12.69 | 22 | 5.3041 % | 1,555.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| EMA.PR.F | FixedReset Disc | -11.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 11.75 Evaluated at bid price : 11.75 Bid-YTW : 7.67 % |

| BMO.PR.Q | FixedReset Bank Non | -3.08 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 9.15 % |

| HSE.PR.G | FixedReset Disc | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.00 Evaluated at bid price : 9.00 Bid-YTW : 11.52 % |

| TD.PF.D | FixedReset Disc | -2.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.41 Evaluated at bid price : 12.41 Bid-YTW : 6.93 % |

| TRP.PR.D | FixedReset Disc | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.01 Evaluated at bid price : 12.01 Bid-YTW : 6.66 % |

| BAM.PF.C | Perpetual-Discount | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.79 % |

| PWF.PR.A | Floater | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 7.95 Evaluated at bid price : 7.95 Bid-YTW : 5.47 % |

| RY.PR.A | Deemed-Retractible | 1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.79 Bid-YTW : 7.63 % |

| RY.PR.F | Deemed-Retractible | 1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.85 Bid-YTW : 7.48 % |

| PVS.PR.F | SplitShare | 1.11 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2024-09-30 Maturity Price : 25.00 Evaluated at bid price : 22.75 Bid-YTW : 7.30 % |

| BAM.PF.I | FixedReset Prem | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 6.04 % |

| CM.PR.T | FixedReset Disc | 1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 16.80 Evaluated at bid price : 16.80 Bid-YTW : 6.27 % |

| RY.PR.G | Deemed-Retractible | 1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.64 Bid-YTW : 8.06 % |

| TRP.PR.K | FixedReset Prem | 1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 6.18 % |

| BAM.PR.N | Perpetual-Discount | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 6.76 % |

| CCS.PR.C | Deemed-Retractible | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 6.63 % |

| EMA.PR.C | FixedReset Disc | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.84 Evaluated at bid price : 13.84 Bid-YTW : 6.53 % |

| BAM.PF.J | FixedReset Prem | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.39 Evaluated at bid price : 19.39 Bid-YTW : 6.17 % |

| RY.PR.P | Perpetual-Premium | 1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 22.49 Evaluated at bid price : 22.82 Bid-YTW : 5.82 % |

| RY.PR.W | Perpetual-Discount | 1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 5.92 % |

| RY.PR.Q | FixedReset Prem | 1.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.43 Evaluated at bid price : 21.75 Bid-YTW : 5.96 % |

| BAM.PF.D | Perpetual-Discount | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 6.76 % |

| GWO.PR.N | FixedReset Ins Non | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 8.93 Evaluated at bid price : 8.93 Bid-YTW : 5.30 % |

| GWO.PR.M | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 6.85 % |

| SLF.PR.C | Deemed-Retractible | 1.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.07 Evaluated at bid price : 17.07 Bid-YTW : 6.57 % |

| ELF.PR.H | Perpetual-Premium | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 6.98 % |

| BMO.PR.E | FixedReset Disc | 1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.27 Evaluated at bid price : 15.27 Bid-YTW : 6.00 % |

| PWF.PR.G | Perpetual-Premium | 1.94 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.78 Evaluated at bid price : 22.02 Bid-YTW : 6.83 % |

| EIT.PR.B | SplitShare | 1.95 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2025-03-14 Maturity Price : 25.00 Evaluated at bid price : 22.50 Bid-YTW : 7.34 % |

| RY.PR.O | Perpetual-Discount | 1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 5.95 % |

| PWF.PR.S | Perpetual-Discount | 1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.00 Evaluated at bid price : 18.00 Bid-YTW : 6.81 % |

| PVS.PR.H | SplitShare | 2.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2027-02-28 Maturity Price : 25.00 Evaluated at bid price : 22.95 Bid-YTW : 6.27 % |

| EIT.PR.A | SplitShare | 2.09 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2024-03-14 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 7.27 % |

| TRP.PR.C | FixedReset Disc | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 8.50 Evaluated at bid price : 8.50 Bid-YTW : 6.23 % |

| CU.PR.I | FixedReset Prem | 2.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.95 Evaluated at bid price : 20.95 Bid-YTW : 5.44 % |

| BAM.PF.H | FixedReset Prem | 2.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 6.05 % |

| PWF.PR.I | Perpetual-Premium | 2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 22.33 Evaluated at bid price : 22.60 Bid-YTW : 6.77 % |

| PWF.PR.R | Perpetual-Premium | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 6.95 % |

| PWF.PR.F | Perpetual-Discount | 2.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 6.95 % |

| IAF.PR.B | Deemed-Retractible | 2.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.60 Evaluated at bid price : 17.60 Bid-YTW : 6.59 % |

| IFC.PR.G | FixedReset Ins Non | 2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.56 Evaluated at bid price : 13.56 Bid-YTW : 6.48 % |

| BIP.PR.F | FixedReset Disc | 2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 7.39 % |

| PWF.PR.Z | Perpetual-Discount | 2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.05 Evaluated at bid price : 19.05 Bid-YTW : 6.90 % |

| CU.PR.H | Perpetual-Discount | 2.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.61 Evaluated at bid price : 20.61 Bid-YTW : 6.46 % |

| BAM.PF.F | FixedReset Disc | 2.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 6.48 % |

| TRP.PR.J | FixedReset Prem | 2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.74 Evaluated at bid price : 22.20 Bid-YTW : 6.26 % |

| EMA.PR.E | Perpetual-Discount | 2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.46 Evaluated at bid price : 18.46 Bid-YTW : 6.19 % |

| IFC.PR.F | Deemed-Retractible | 2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.40 Evaluated at bid price : 21.40 Bid-YTW : 6.24 % |

| TD.PF.I | FixedReset Disc | 2.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.25 Evaluated at bid price : 15.25 Bid-YTW : 6.25 % |

| SLF.PR.E | Deemed-Retractible | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.46 Evaluated at bid price : 17.46 Bid-YTW : 6.49 % |

| CU.PR.D | Perpetual-Discount | 2.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.72 Evaluated at bid price : 19.72 Bid-YTW : 6.30 % |

| IFC.PR.E | Deemed-Retractible | 2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.59 Evaluated at bid price : 20.59 Bid-YTW : 6.36 % |

| BIP.PR.D | FixedReset Disc | 2.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 6.85 % |

| PWF.PR.O | Perpetual-Premium | 2.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.28 Evaluated at bid price : 21.28 Bid-YTW : 6.96 % |

| BMO.PR.F | FixedReset Disc | 2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.85 Evaluated at bid price : 17.85 Bid-YTW : 6.17 % |

| TD.PF.H | FixedReset Prem | 2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 6.32 % |

| BMO.PR.C | FixedReset Disc | 2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 6.40 % |

| CU.PR.F | Perpetual-Discount | 2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.45 Evaluated at bid price : 18.45 Bid-YTW : 6.18 % |

| PWF.PR.K | Perpetual-Discount | 2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.43 Evaluated at bid price : 18.43 Bid-YTW : 6.86 % |

| MFC.PR.O | FixedReset Ins Non | 2.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 6.85 % |

| TD.PF.L | FixedReset Disc | 2.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.30 Evaluated at bid price : 17.30 Bid-YTW : 6.18 % |

| BNS.PR.I | FixedReset Disc | 3.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.72 Evaluated at bid price : 15.72 Bid-YTW : 5.56 % |

| SLF.PR.J | FloatingReset | 3.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 8.25 Evaluated at bid price : 8.25 Bid-YTW : 4.92 % |

| SLF.PR.A | Deemed-Retractible | 3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 6.47 % |

| RY.PR.S | FixedReset Disc | 3.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 5.41 % |

| BAM.PR.K | Floater | 3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 7.54 Evaluated at bid price : 7.54 Bid-YTW : 5.71 % |

| BMO.PR.D | FixedReset Disc | 3.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.50 Evaluated at bid price : 15.50 Bid-YTW : 6.29 % |

| BNS.PR.E | FixedReset Prem | 3.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 6.06 % |

| TD.PF.F | Perpetual-Discount | 3.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 5.87 % |

| POW.PR.C | Perpetual-Premium | 3.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 6.91 % |

| BAM.PF.G | FixedReset Disc | 3.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.16 Evaluated at bid price : 13.16 Bid-YTW : 6.53 % |

| TD.PF.G | FixedReset Prem | 3.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.43 Evaluated at bid price : 21.75 Bid-YTW : 6.13 % |

| PVS.PR.G | SplitShare | 3.60 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2026-02-28 Maturity Price : 25.00 Evaluated at bid price : 23.00 Bid-YTW : 6.66 % |

| W.PR.K | FixedReset Prem | 3.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 6.47 % |

| PWF.PR.L | Perpetual-Discount | 3.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.96 Evaluated at bid price : 18.96 Bid-YTW : 6.87 % |

| BMO.PR.Z | Perpetual-Discount | 3.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.52 Evaluated at bid price : 21.52 Bid-YTW : 5.89 % |

| BMO.PR.W | FixedReset Disc | 3.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 6.16 % |

| TD.PF.J | FixedReset Disc | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.11 Evaluated at bid price : 15.11 Bid-YTW : 5.99 % |

| TRP.PR.A | FixedReset Disc | 3.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 11.26 Evaluated at bid price : 11.26 Bid-YTW : 6.21 % |

| GWO.PR.L | Deemed-Retractible | 3.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.76 Evaluated at bid price : 20.76 Bid-YTW : 6.86 % |

| BAM.PR.X | FixedReset Disc | 3.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.83 Evaluated at bid price : 9.83 Bid-YTW : 6.20 % |

| SLF.PR.B | Deemed-Retractible | 3.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 6.36 % |

| IFC.PR.C | FixedReset Ins Non | 3.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 6.40 % |

| BAM.PR.B | Floater | 3.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 7.58 Evaluated at bid price : 7.58 Bid-YTW : 5.68 % |

| TRP.PR.G | FixedReset Disc | 3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 6.67 % |

| BIP.PR.E | FixedReset Disc | 3.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.40 Evaluated at bid price : 17.40 Bid-YTW : 7.25 % |

| MFC.PR.Q | FixedReset Ins Non | 3.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.65 Evaluated at bid price : 13.65 Bid-YTW : 6.36 % |

| POW.PR.G | Perpetual-Premium | 3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 6.95 % |

| SLF.PR.D | Deemed-Retractible | 3.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 6.41 % |

| TRP.PR.B | FixedReset Disc | 3.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 7.95 Evaluated at bid price : 7.95 Bid-YTW : 5.86 % |

| CIU.PR.A | Perpetual-Discount | 3.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 6.61 % |

| POW.PR.A | Perpetual-Premium | 3.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 6.87 % |

| GWO.PR.I | Deemed-Retractible | 4.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 16.85 Evaluated at bid price : 16.85 Bid-YTW : 6.73 % |

| GWO.PR.G | Deemed-Retractible | 4.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 6.72 % |

| BMO.PR.B | FixedReset Prem | 4.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.20 Evaluated at bid price : 19.20 Bid-YTW : 6.15 % |

| SLF.PR.G | FixedReset Ins Non | 4.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 8.43 Evaluated at bid price : 8.43 Bid-YTW : 5.92 % |

| PWF.PR.E | Perpetual-Premium | 4.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.56 Evaluated at bid price : 20.56 Bid-YTW : 6.83 % |

| RY.PR.J | FixedReset Disc | 4.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 14.40 Evaluated at bid price : 14.40 Bid-YTW : 5.83 % |

| RY.PR.N | Perpetual-Discount | 4.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 5.82 % |

| BMO.PR.T | FixedReset Disc | 4.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 6.15 % |

| W.PR.M | FixedReset Prem | 4.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.70 Evaluated at bid price : 20.70 Bid-YTW : 6.31 % |

| GWO.PR.H | Deemed-Retractible | 4.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.59 Evaluated at bid price : 18.59 Bid-YTW : 6.57 % |

| MFC.PR.C | Deemed-Retractible | 4.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.31 Evaluated at bid price : 17.31 Bid-YTW : 6.57 % |

| GWO.PR.F | Deemed-Retractible | 4.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 22.07 Evaluated at bid price : 22.30 Bid-YTW : 6.66 % |

| CM.PR.Q | FixedReset Disc | 4.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.29 Evaluated at bid price : 12.29 Bid-YTW : 6.86 % |

| BAM.PR.T | FixedReset Disc | 4.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 11.48 Evaluated at bid price : 11.48 Bid-YTW : 6.49 % |

| RY.PR.R | FixedReset Prem | 4.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 22.93 Evaluated at bid price : 23.38 Bid-YTW : 5.81 % |

| MFC.PR.B | Deemed-Retractible | 4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.50 Evaluated at bid price : 18.50 Bid-YTW : 6.35 % |

| PWF.PR.T | FixedReset Disc | 4.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.53 Evaluated at bid price : 12.53 Bid-YTW : 6.65 % |

| PWF.PR.H | Perpetual-Premium | 4.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 6.94 % |

| NA.PR.S | FixedReset Disc | 4.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.40 Evaluated at bid price : 12.40 Bid-YTW : 6.68 % |

| POW.PR.D | Perpetual-Discount | 4.49 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.09 Evaluated at bid price : 19.09 Bid-YTW : 6.58 % |

| GWO.PR.R | Deemed-Retractible | 4.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.34 Evaluated at bid price : 18.34 Bid-YTW : 6.60 % |

| CM.PR.R | FixedReset Disc | 4.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 14.75 Evaluated at bid price : 14.75 Bid-YTW : 6.83 % |

| CM.PR.Y | FixedReset Disc | 4.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.67 Evaluated at bid price : 17.67 Bid-YTW : 6.32 % |

| TD.PF.K | FixedReset Disc | 4.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.07 Evaluated at bid price : 15.07 Bid-YTW : 5.95 % |

| GWO.PR.Q | Deemed-Retractible | 4.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 6.69 % |

| GWO.PR.S | Deemed-Retractible | 4.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 6.82 % |

| MFC.PR.K | FixedReset Ins Non | 4.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.41 Evaluated at bid price : 12.41 Bid-YTW : 6.40 % |

| SLF.PR.I | FixedReset Ins Non | 4.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.51 Evaluated at bid price : 13.51 Bid-YTW : 6.25 % |

| CM.PR.S | FixedReset Disc | 4.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.20 Evaluated at bid price : 13.20 Bid-YTW : 6.25 % |

| BAM.PR.R | FixedReset Disc | 4.79 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 11.37 Evaluated at bid price : 11.37 Bid-YTW : 6.38 % |

| BAM.PF.B | FixedReset Disc | 4.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.70 Evaluated at bid price : 13.70 Bid-YTW : 6.46 % |

| CM.PR.O | FixedReset Disc | 4.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.11 Evaluated at bid price : 12.11 Bid-YTW : 6.45 % |

| HSE.PR.C | FixedReset Disc | 4.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.70 Evaluated at bid price : 9.70 Bid-YTW : 10.67 % |

| GWO.PR.P | Deemed-Retractible | 4.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 6.79 % |

| MFC.PR.H | FixedReset Ins Non | 4.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.70 Evaluated at bid price : 13.70 Bid-YTW : 6.97 % |

| NA.PR.E | FixedReset Disc | 4.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.70 Evaluated at bid price : 13.70 Bid-YTW : 6.40 % |

| POW.PR.B | Perpetual-Discount | 5.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 6.77 % |

| TD.PF.M | FixedReset Disc | 5.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 6.13 % |

| IAF.PR.I | FixedReset Ins Non | 5.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.40 Evaluated at bid price : 13.40 Bid-YTW : 6.79 % |

| NA.PR.C | FixedReset Disc | 5.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.40 Evaluated at bid price : 15.40 Bid-YTW : 6.74 % |

| GWO.PR.T | Deemed-Retractible | 5.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 6.73 % |

| MFC.PR.I | FixedReset Ins Non | 5.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 6.70 % |

| CM.PR.P | FixedReset Disc | 5.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.40 Evaluated at bid price : 12.40 Bid-YTW : 6.35 % |

| RY.PR.H | FixedReset Disc | 5.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.60 Evaluated at bid price : 13.60 Bid-YTW : 5.67 % |

| MFC.PR.L | FixedReset Ins Non | 5.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 6.44 % |

| BMO.PR.S | FixedReset Disc | 5.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.85 Evaluated at bid price : 12.85 Bid-YTW : 6.21 % |

| MFC.PR.J | FixedReset Ins Non | 5.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.30 Evaluated at bid price : 13.30 Bid-YTW : 6.60 % |

| NA.PR.A | FixedReset Prem | 5.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.90 Evaluated at bid price : 20.90 Bid-YTW : 6.38 % |

| BIK.PR.A | FixedReset Prem | 5.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.86 Evaluated at bid price : 22.24 Bid-YTW : 6.61 % |

| TD.PF.A | FixedReset Disc | 5.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.18 Evaluated at bid price : 13.18 Bid-YTW : 5.89 % |

| TD.PF.C | FixedReset Disc | 5.47 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.31 Evaluated at bid price : 13.31 Bid-YTW : 6.03 % |

| MFC.PR.N | FixedReset Ins Non | 5.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.13 Evaluated at bid price : 12.13 Bid-YTW : 5.97 % |

| BIP.PR.A | FixedReset Disc | 5.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.00 Evaluated at bid price : 13.00 Bid-YTW : 8.02 % |

| CU.PR.E | Perpetual-Discount | 5.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.86 Evaluated at bid price : 19.86 Bid-YTW : 6.25 % |

| NA.PR.G | FixedReset Disc | 5.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 14.50 Evaluated at bid price : 14.50 Bid-YTW : 6.53 % |

| CU.PR.C | FixedReset Disc | 5.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 14.25 Evaluated at bid price : 14.25 Bid-YTW : 5.37 % |

| BAM.PR.C | Floater | 5.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 7.61 Evaluated at bid price : 7.61 Bid-YTW : 5.65 % |

| TRP.PR.F | FloatingReset | 6.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.68 Evaluated at bid price : 9.68 Bid-YTW : 5.52 % |

| MFC.PR.R | FixedReset Ins Non | 6.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 16.55 Evaluated at bid price : 16.55 Bid-YTW : 6.81 % |

| MFC.PR.G | FixedReset Ins Non | 6.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.05 Evaluated at bid price : 13.05 Bid-YTW : 6.81 % |

| TD.PF.B | FixedReset Disc | 6.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.30 Evaluated at bid price : 13.30 Bid-YTW : 5.87 % |

| RY.PR.Z | FixedReset Disc | 6.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.40 Evaluated at bid price : 13.40 Bid-YTW : 5.69 % |

| NA.PR.X | FixedReset Prem | 6.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 21.47 Evaluated at bid price : 21.81 Bid-YTW : 6.37 % |

| MFC.PR.F | FixedReset Ins Non | 6.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 8.40 Evaluated at bid price : 8.40 Bid-YTW : 5.99 % |

| EML.PR.A | FixedReset Ins Non | 6.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 7.07 % |

| RY.PR.M | FixedReset Disc | 6.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.99 Evaluated at bid price : 13.99 Bid-YTW : 5.81 % |

| IFC.PR.A | FixedReset Ins Non | 6.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.90 Evaluated at bid price : 9.90 Bid-YTW : 6.31 % |

| NA.PR.W | FixedReset Disc | 6.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.62 Evaluated at bid price : 12.62 Bid-YTW : 6.31 % |

| IAF.PR.G | FixedReset Ins Non | 7.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.70 Evaluated at bid price : 12.70 Bid-YTW : 6.89 % |

| TD.PF.E | FixedReset Disc | 7.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 6.28 % |

| HSE.PR.A | FixedReset Disc | 7.88 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 5.61 Evaluated at bid price : 5.61 Bid-YTW : 10.42 % |

| BNS.PR.H | FixedReset Prem | 8.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 19.52 Evaluated at bid price : 19.52 Bid-YTW : 6.24 % |

| PWF.PR.Q | FloatingReset | 8.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.00 Evaluated at bid price : 9.00 Bid-YTW : 5.10 % |

| BMO.PR.Y | FixedReset Disc | 9.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.45 Evaluated at bid price : 13.45 Bid-YTW : 6.21 % |

| MFC.PR.M | FixedReset Ins Non | 9.54 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 12.63 Evaluated at bid price : 12.63 Bid-YTW : 6.36 % |

| PWF.PR.P | FixedReset Disc | 10.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 9.43 Evaluated at bid price : 9.43 Bid-YTW : 5.88 % |

| SLF.PR.H | FixedReset Ins Non | 10.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 11.14 Evaluated at bid price : 11.14 Bid-YTW : 6.22 % |

| BAM.PF.A | FixedReset Disc | 18.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.10 Evaluated at bid price : 15.10 Bid-YTW : 6.37 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| PWF.PR.E | Perpetual-Premium | 117,745 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 20.56 Evaluated at bid price : 20.56 Bid-YTW : 6.83 % |

| BMO.PR.F | FixedReset Disc | 70,279 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 17.85 Evaluated at bid price : 17.85 Bid-YTW : 6.17 % |

| RY.PR.S | FixedReset Disc | 55,343 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 15.80 Evaluated at bid price : 15.80 Bid-YTW : 5.41 % |

| RY.PR.Z | FixedReset Disc | 54,209 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.40 Evaluated at bid price : 13.40 Bid-YTW : 5.69 % |

| TD.PF.B | FixedReset Disc | 52,330 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 13.30 Evaluated at bid price : 13.30 Bid-YTW : 5.87 % |

| TD.PF.M | FixedReset Disc | 40,191 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-31 Maturity Price : 18.28 Evaluated at bid price : 18.28 Bid-YTW : 6.13 % |

| There were 57 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.K | FixedReset Ins Non | Quote: 12.41 – 18.10 Spot Rate : 5.6900 Average : 4.6726 YTW SCENARIO |

| MFC.PR.R | FixedReset Ins Non | Quote: 16.55 – 18.86 Spot Rate : 2.3100 Average : 1.3783 YTW SCENARIO |

| EMA.PR.F | FixedReset Disc | Quote: 11.75 – 14.40 Spot Rate : 2.6500 Average : 1.8561 YTW SCENARIO |

| MFC.PR.G | FixedReset Ins Non | Quote: 13.05 – 19.17 Spot Rate : 6.1200 Average : 5.3345 YTW SCENARIO |

| TD.PF.D | FixedReset Disc | Quote: 12.41 – 14.58 Spot Rate : 2.1700 Average : 1.5280 YTW SCENARIO |

| BNS.PR.G | FixedReset Prem | Quote: 21.65 – 23.24 Spot Rate : 1.5900 Average : 1.0552 YTW SCENARIO |

“There was some talk in trading circles that a big U.S. investor has accumulated shares of Suncor and Canadian Natural Resources over the last couple of days.”

Once we get through the worst of COVID-19 and the oil price crisis (for producers), I suspect that the big untold story will be the massive and possibly historic transfer of wealth underway these past weeks.