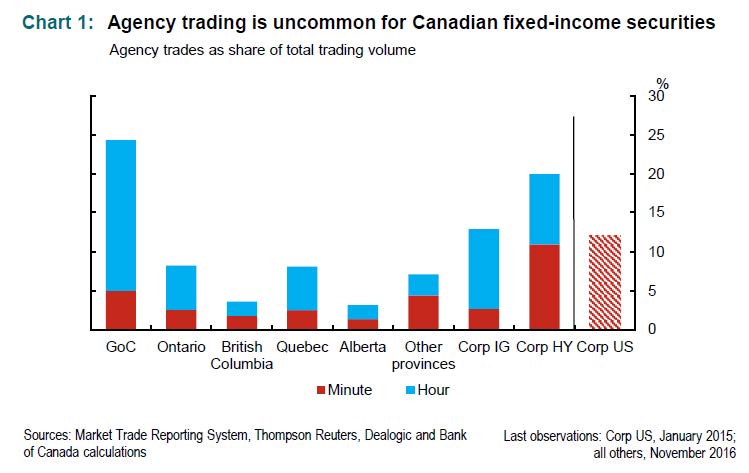

The BoC has had a look at Canadian bond trading:

Technology, risk tolerance and regulation may influence dealers to reduce their trading as principals (using their own balance sheets for sales and purchases of securities) in favour of agency trading (matching client trades). A move toward agency trading would represent a change in the structure of Canadian bond markets and, in theory, could worsen some aspects of market liquidity. To assess the prevalence of agency trading in Canada, we use data from the Market Trade Reporting System to construct the first estimate of agency-based trading in Canadian bond markets. We find that agency trading is relatively uncommon across major segments of Canadian fixed-income market and that large bank broker-dealers are less likely than their smaller counterparts to trade as an agent.

Click for Big

One economist has been brave enough to criticize the BoC’s communications:

The Bank of Canada didn’t give a speech or make other public comments about the strength of an economic recovery in the days before its Sept. 6 increase, a decision that Bank of Montreal Chief Economist Doug Porter called “an epic fail” in a report on Friday. The quarter-point increase to 1 percent was anticipated by six of 29 economists surveyed by Bloomberg.

Jeremy Harrison, the central bank’s chief spokesman, said in emailed comments that policy makers indicated at the last decision in July that monetary policy would be forward-looking and depend on economic data. Trading in overnight index swaps had also priced in 50-50 odds of a move this month after a strong report on second-quarter gross domestic product, which was published during a traditional blackout period in the days just before a rate meeting, Harrison said. Harrison had initially provided these comments to the Globe and Mail newspaper.

Seems to me like Porter wants his policy forecasts to be served to him on a plate, as was the case with the July increase. The major problem with the BoC’s communications is that committee votes and reasons for dissents – a normal component of the communication of a professionally run central bank – are not specified in the bank’s press releases and that the bank’s outreach is very close to being all Poloz, all the time!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1854 % | 2,407.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1854 % | 4,417.3 |

| Floater | 3.90 % | 3.95 % | 109,308 | 17.44 | 3 | -0.1854 % | 2,545.7 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0950 % | 3,064.1 |

| SplitShare | 4.75 % | 4.53 % | 65,251 | 3.70 | 5 | -0.0950 % | 3,659.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0950 % | 2,855.1 |

| Perpetual-Premium | 5.43 % | 4.92 % | 62,749 | 6.13 | 16 | -0.1999 % | 2,770.8 |

| Perpetual-Discount | 5.37 % | 5.43 % | 66,841 | 14.70 | 19 | -0.5296 % | 2,880.0 |

| FixedReset | 4.36 % | 4.53 % | 145,685 | 6.26 | 98 | -0.0149 % | 2,396.5 |

| Deemed-Retractible | 5.16 % | 5.74 % | 96,928 | 6.07 | 31 | -0.0761 % | 2,840.5 |

| FloatingReset | 2.84 % | 3.11 % | 43,417 | 4.12 | 8 | 0.2209 % | 2,627.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| CU.PR.H | Perpetual-Discount | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-09-11 Maturity Price : 24.09 Evaluated at bid price : 24.50 Bid-YTW : 5.38 % |

| SLF.PR.H | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.55 Bid-YTW : 6.33 % |

| HSE.PR.A | FixedReset | -1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-09-11 Maturity Price : 16.63 Evaluated at bid price : 16.63 Bid-YTW : 4.86 % |

| POW.PR.D | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-09-11 Maturity Price : 23.41 Evaluated at bid price : 23.70 Bid-YTW : 5.35 % |

| MFC.PR.B | Deemed-Retractible | -1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.71 Bid-YTW : 6.98 % |

| BAM.PF.D | Perpetual-Discount | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-09-11 Maturity Price : 21.90 Evaluated at bid price : 22.22 Bid-YTW : 5.61 % |

| IFC.PR.A | FixedReset | 1.12 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.92 Bid-YTW : 7.26 % |

| VNR.PR.A | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-09-11 Maturity Price : 21.94 Evaluated at bid price : 22.45 Bid-YTW : 5.08 % |

| SLF.PR.J | FloatingReset | 1.51 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.86 Bid-YTW : 8.33 % |

| IFC.PR.E | Deemed-Retractible | 2.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.35 Bid-YTW : 5.94 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.H | FixedReset | 118,225 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-31 Maturity Price : 25.00 Evaluated at bid price : 26.16 Bid-YTW : 3.79 % |

| CM.PR.R | FixedReset | 113,338 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.21 Bid-YTW : 4.52 % |

| BAM.PF.B | FixedReset | 98,418 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2047-09-11 Maturity Price : 22.42 Evaluated at bid price : 22.80 Bid-YTW : 4.80 % |

| W.PR.K | FixedReset | 91,200 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-01-15 Maturity Price : 25.00 Evaluated at bid price : 26.13 Bid-YTW : 4.08 % |

| BMO.PR.B | FixedReset | 90,992 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 26.16 Bid-YTW : 3.78 % |

| NA.PR.C | FixedReset | 83,425 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-11-15 Maturity Price : 25.00 Evaluated at bid price : 25.20 Bid-YTW : 4.54 % |

| There were 35 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.G | FixedReset | Quote: 24.00 – 25.05 Spot Rate : 1.0500 Average : 0.6057 YTW SCENARIO |

| TRP.PR.A | FixedReset | Quote: 19.02 – 19.56 Spot Rate : 0.5400 Average : 0.3492 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 23.13 – 23.53 Spot Rate : 0.4000 Average : 0.2890 YTW SCENARIO |

| W.PR.K | FixedReset | Quote: 26.13 – 26.47 Spot Rate : 0.3400 Average : 0.2321 YTW SCENARIO |

| ELF.PR.G | Perpetual-Discount | Quote: 22.00 – 22.36 Spot Rate : 0.3600 Average : 0.2595 YTW SCENARIO |

| SLF.PR.E | Deemed-Retractible | Quote: 20.93 – 21.17 Spot Rate : 0.2400 Average : 0.1526 YTW SCENARIO |