DBRS has announced that it:

has today placed the preferred shares and Tier 1 innovative instruments ratings of all the Canadian banks it rates Under Review with Negative Implications following changes made to the DBRS global banking methodology, which will be made public shortly, and the updated Enhanced Methodology for Bank Ratings – Intrinsic and Support Assessment. The changes in methodologies reflect the revision of our views on external support as it relates to preferred shares and the elevated risk of non-payment of preferred dividends relative to the risk of default indicated by senior debt ratings based on the more severe business environment being faced by global banks. They do not reflect any specific credit event at any of the listed institutions or related entities. Today’s actions apply only to the preferred shares and Tier 1 innovative instruments of the Canadian banks that DBRS rates; all other ratings are unaffected.

Under the previous Enhanced Methodology for Bank Ratings – Intrinsic and Support Assessment (for more details, refer to the press release dated October 6, 2006), many of the preferred shares and Tier 1 innovative instruments ratings of both the listed institutions and their related entities benefited from a one-notch uplift in October 2006. The primary factor that has led DBRS to rethink our support assessment methodology as it applies to preferred shares and Tier 1 innovative instruments is recent actions taken in other jurisdictions that demonstrate no systemic external support for preferred shares.

Historically, DBRS’s Rating Banks in Canada methodology resulted in a generally fixed relationship between the different securities of the same banking entity, with preferred shares ratings being notched down from the senior unsecured debt rating level. The changes in the methodologies have increased the base notching at even the strongest rating categories and the base notching also now expands as the credit quality of the bank migrates downward. Within this approach, there exists greater flexibility to adjust the notching for factors that reflect the position of individual banks. Canadian Tier 1 innovative instruments, as they are typically convertible into preferred shares, will continue to be rated in line with preferred shares.

Our review will consider the revised global banking methodology in light of the fact that neither the Canadian financial system nor Canadian banks have exhibited the types of stress that have been witnessed with many other banks. Should rating downgrades be the result of our review for Canadian banks, DBRS does not expect the downgrades to be as severe as the actions DBRS has recently taken with ratings in the U.S. banking sector. For more information on the U.S. banking downgrades, please see the related press releases at www.dbrs.com.

The applicable methodologies are Rating Banks in Canada and Enhanced Methodology for Bank Ratings – Intrinsic and Support Assessment, which can be found on the DBRS website under Methodologies.

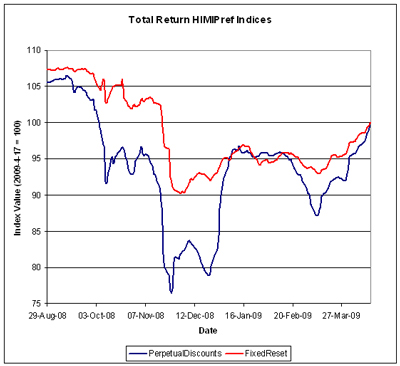

They provide a link to the methodology. The mass-upgrade of October 2006 and its effect on the yield curve were discussed on PrefBlog.

Well! Here’s some excitement in PrefLand! They did a mass downgrade of US financial preferreds today as well:

- Morgan Stanley

- CIT Group Inc.

- Goldman Sachs Group, Inc., The

- Bank of America Corporation

- KeyCorp

- Zions Bancorporation

- U.S. Bancorp

- Fifth Third Bancorp

- SunTrust Banks, Inc.

- Huntington Bancshares Inc.

- Webster Financial Corporation

- New York Community Bank

- CBG Florida REIT Corp.

Update, 2009-4-21: DBRS inadverdently left the HSBC HaTS off the Review-Negative list; they have now been added.

In a Mass Downgrade of European Hybrids they note:

banks and their regulators in Europe and elsewhere have become much more focused on conserving capital, particularly common equity, which may be achieved in part by the suspension of preferred dividends. Today’s action also reflects the increasing importance being placed on common equity in the capital structure by regulators and the financial markets that could lead to adverse action on preferreds. One consequence is that the starting point in rating preferred shares and hybrids becomes the intrinsic assessment, rather than the final rating, which benefits from implicit systemic support by typically a notch for SA2 banks. Preferred shares and hybrids are very unlikely to benefit from systemic support and do not benefit from any implied support. The application of DBRS’s methodology has resulted in a generally fixed relationship across rating categories between preferreds and senior issuer ratings, with some flexibility. Today’s actions reflect a revision to DBRS’s methodology whereby the notching has been increased at even the strongest rating categories and expanded as the credit quality of a bank migrates downwards. Within this approach, there remains the flexibility to adjust the notching for factors that reflect the position of individual banks.