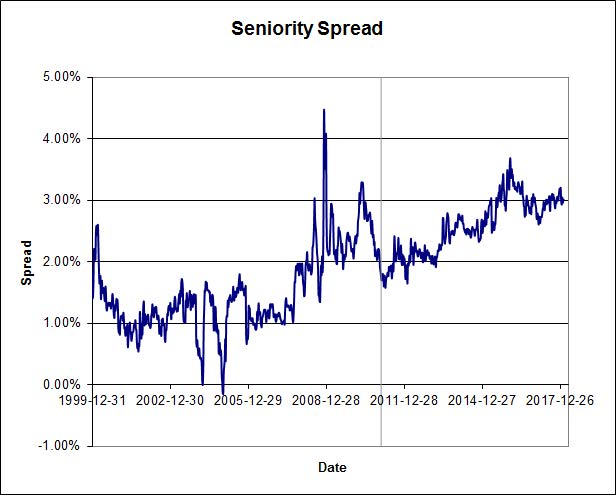

PerpetualDiscounts now yield 5.42%, equivalent to 7.05% interest at the standard equivalency factor of 1.3x. Long corporates now yield about 3.90%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 315bp, a slight (and perhaps spurious) narrowing from the 320bp reported March 7.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1944 % | 3,089.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.1944 % | 5,668.7 |

| Floater | 3.23 % | 3.40 % | 111,341 | 18.77 | 4 | -0.1944 % | 3,266.9 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0549 % | 3,163.6 |

| SplitShare | 4.69 % | 4.18 % | 61,594 | 3.28 | 5 | -0.0549 % | 3,778.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0549 % | 2,947.8 |

| Perpetual-Premium | 5.60 % | -1.11 % | 77,835 | 0.08 | 11 | 0.1719 % | 2,842.3 |

| Perpetual-Discount | 5.32 % | 5.42 % | 87,936 | 14.72 | 23 | 0.1024 % | 2,950.7 |

| FixedReset | 4.26 % | 4.57 % | 175,822 | 5.82 | 104 | 0.0277 % | 2,524.7 |

| Deemed-Retractible | 5.15 % | 5.69 % | 93,190 | 5.75 | 28 | 0.0582 % | 2,930.3 |

| FloatingReset | 3.01 % | 3.13 % | 36,175 | 3.66 | 10 | -0.1809 % | 2,761.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| IAG.PR.A | Deemed-Retractible | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.00 Bid-YTW : 6.81 % |

| BIP.PR.B | FixedReset | 1.13 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 26.00 Bid-YTW : 3.90 % |

| IFC.PR.E | Deemed-Retractible | 1.49 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.59 Bid-YTW : 5.48 % |

| IFC.PR.F | Deemed-Retractible | 1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 5.29 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.J | FixedReset | 605,636 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-14 Maturity Price : 23.15 Evaluated at bid price : 24.98 Bid-YTW : 4.65 % |

| W.PR.J | Perpetual-Discount | 308,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-14 Maturity Price : 24.49 Evaluated at bid price : 24.72 Bid-YTW : 5.76 % |

| BMO.PR.B | FixedReset | 185,072 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.91 Bid-YTW : 3.94 % |

| W.PR.M | FixedReset | 184,131 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-10-15 Maturity Price : 25.00 Evaluated at bid price : 26.04 Bid-YTW : 4.22 % |

| POW.PR.D | Perpetual-Discount | 181,803 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-14 Maturity Price : 23.32 Evaluated at bid price : 23.60 Bid-YTW : 5.37 % |

| BAM.PF.J | FixedReset | 180,850 | YTW SCENARIO Maturity Type : Call Maturity Date : 2022-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.11 Bid-YTW : 4.62 % |

| BAM.PF.A | FixedReset | 167,506 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-14 Maturity Price : 23.85 Evaluated at bid price : 24.51 Bid-YTW : 5.02 % |

| IFC.PR.C | FixedReset | 153,573 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.37 Bid-YTW : 5.11 % |

| CM.PR.O | FixedReset | 131,067 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2048-03-14 Maturity Price : 23.44 Evaluated at bid price : 23.89 Bid-YTW : 4.56 % |

| NA.PR.A | FixedReset | 105,875 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-15 Maturity Price : 25.00 Evaluated at bid price : 26.22 Bid-YTW : 4.02 % |

| There were 45 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.C | Perpetual-Discount | Quote: 21.84 – 22.09 Spot Rate : 0.2500 Average : 0.1516 YTW SCENARIO |

| BAM.PF.H | FixedReset | Quote: 25.69 – 25.94 Spot Rate : 0.2500 Average : 0.1561 YTW SCENARIO |

| IFC.PR.C | FixedReset | Quote: 23.37 – 23.58 Spot Rate : 0.2100 Average : 0.1289 YTW SCENARIO |

| RY.PR.R | FixedReset | Quote: 26.51 – 26.72 Spot Rate : 0.2100 Average : 0.1359 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 24.63 – 24.99 Spot Rate : 0.3600 Average : 0.2890 YTW SCENARIO |

| RY.PR.W | Perpetual-Discount | Quote: 24.80 – 24.99 Spot Rate : 0.1900 Average : 0.1201 YTW SCENARIO |