There is a report that the London Office of AIG’s now notorious Financial Products Group took on notional exposure of USD 500-billion in sub-prime CDSs … not bad leverage for one office of one division, considering AIG’s total equity was $104-billion in June 07, just before the fun started.

Econbrowser‘s James Hamilton advocates having AIG default on its CDSs:

But the issue for me has always been not to exact retribution or instill market discipline, but instead the very pragmatic question of how to use available resources to minimize collateral damage. I accept the argument that a complete failure of AIG would have unacceptable consequences. The relevant question then is, what combination of parties is going to absorb the loss?

The concern I wish to raise is that any reasonable answer to that question would include Goldman Sachs, Merrill Lynch, Societe Generale, and Calyon, to pick a few names at random, as major contributors to this particular collateral-damage-minimization relief fund.

…

Then there’s the domino effect to consider. What do we do when this brings down the next player who can’t continue operations without those payments AIG (or the taxpayers) were supposedly going to deliver? I say, we implement the parallel operation there.

I can’t agree. This would have knock-on effects akin to another Lehman; the cure would be worse than the disease. The policy focus should not be on minimizing cost, but on minimizing harm.

I certainly agree that it is unfortunated that taxpayers are getting hurt and it is clear that regulation must be improved. However, pain is part of the game. Western economies in general and Amercian taxpayers in particular have been well served by the financial system.

Who wants to live in a country without a functional banking system, particularly the mortgage market? I don’t know what the system is like now, but I understand the Indian mortgage market was basically non-existent not too many years ago. So the middle class had to save all their lives to buy a place and maybe be able to look around by the time they were 55. Housing 55! There’s a good insurance slogan!

However, the drumbeat of retribution continues:

Debt investors are an attractive target because of the size of their holdings — more than $1 trillion just at the four largest U.S. banks — and because they’ve emerged almost unscathed so far. Since any reduction in debt at a bank helps boost capital ratios, members of Congress including U.S. Representative Brad Sherman, a California Democrat, say it’s time for bondholders to share the pain.

“These banks can go into receivership, shed their shareholders, shed or reduce the amount they owe to their bondholders and come back out much stronger institutions,” said Sherman, who sits on the House Financial Services Committee, in a statement to Bloomberg News. More U.S. capital might be offered as part of the package, he said.

Go for it, Sherman. Regardless of the situation a year ago, these institutions now have TARP money and bond-holders are senior to TARP money. You might find yourself on the wrong end of a cramdown.

With this kind of talk floating around, is it any wonder the US Corporate market is dysfunctional?:

I think the corporate bond market is still fractured. It is not as dysfunctional as it was in October and November but the realization that solid well established companies need to provide as much of a concession as these entities are here is a sign that there is a very long road to travel before the corporate bond market functions with a degree of normality.

Meanwhile, the GSEs are a continuing disaster:

Freddie Mac, the mortgage-finance company thrust into a leading role in President Barack Obama’s homeowner rescue plans, said it will tap $30.8 billion in federal aid as its loan holdings and other assets deteriorated.

The company, which owns or guarantees more than 20 percent of U.S. home loans, today posted a wider fourth-quarter net loss of $23.9 billion, or $7.37 a share. The results pushed the value of Freddie’s assets below its liabilities, the McLean, Virginia- based company said in a statement, and come as Chief Executive Officer David Moffett leaves after six months on the job.

…

Freddie and larger competitor Fannie Mae have been pressured to carry out policy initiatives, including offering low-cost mortgage refinancings, since the government takeover. The often conflicting demands of appeasing regulators and pursuing profit may have led Moffett to resign, [F&R Capital Markets analyst Paul] Miller said.

“They want these guys to refi mortgages without new appraisals and to keep mortgage rates very low; those are not sound business decisions,” Miller said. “They are being used as a public policy tool to save the housing market. That is just going to make it more difficult for them to be floated out as public companies down the road.”

In what is almost certainly an orchestrated move, Bernanke’s proposed Financial Stability Regulator has attracted support:

JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon said the U.S. needs a “systemic risk regulator” and should set up procedures to deal with potential failures of large financial institutions.

“Failure is fine as long as it’s orderly, controlled, leads to resolution and doesn’t cause systemic failure,” Dimon, 52, said at a conference hosted by the U.S. Chamber of Commerce in Washington.

Dimon said at a Feb. 3 conference that he believed the Federal Reserve should have the authority to regulate all companies within the banking system.

CDS junkies, by the way, may wish to read the Observations on Management of Recent Credit Default Swap Credit Events.

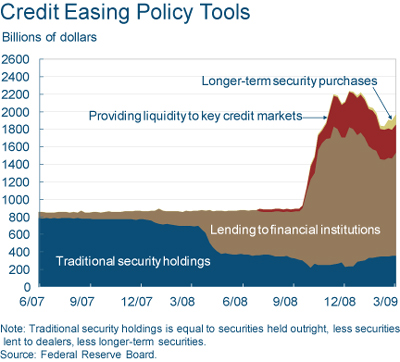

The Cleveland Fed has released its March Econotrends, with an interesting chart-pack on the impact of credit easing so far. The Fed’s balance sheet has begun to bloat again:

Annoyed at having been called insane, PerpetualDiscounts rose 90bp to yield 7.52%, equivalent to 10.53% interest at the standard equivalency factor of 1.4x. Long Corporates now yield 7.6%, so the pre-tax interest-equivalent spread is now about 290bp … certainly at the high end of its range, although nowhere near the November end-of-the-world levels.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

1.3141 % |

783.1 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

1.3141 % |

1,266.5 |

| Floater |

5.05 % |

5.96 % |

62,739 |

14.00 |

3 |

1.3141 % |

978.4 |

| OpRet |

5.34 % |

5.12 % |

138,130 |

3.91 |

15 |

0.1546 % |

2,028.8 |

| SplitShare |

7.11 % |

10.48 % |

54,848 |

4.79 |

6 |

0.3421 % |

1,560.5 |

| Interest-Bearing |

6.28 % |

13.25 % |

37,376 |

0.76 |

1 |

-1.0352 % |

1,870.9 |

| Perpetual-Premium |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.9033 % |

1,434.2 |

| Perpetual-Discount |

7.53 % |

7.52 % |

164,704 |

11.92 |

71 |

0.9033 % |

1,320.8 |

| FixedReset |

6.27 % |

5.90 % |

683,625 |

13.67 |

31 |

-0.0028 % |

1,764.3 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| NA.PR.N |

FixedReset |

-2.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 22.06

Evaluated at bid price : 22.12

Bid-YTW : 4.70 % |

| BAM.PR.O |

OpRet |

-2.11 % |

YTW SCENARIO

Maturity Type : Option Certainty

Maturity Date : 2013-06-30

Maturity Price : 25.00

Evaluated at bid price : 20.00

Bid-YTW : 10.93 % |

| RY.PR.E |

Perpetual-Discount |

-1.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 15.82

Evaluated at bid price : 15.82

Bid-YTW : 7.20 % |

| CIU.PR.A |

Perpetual-Discount |

-1.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 16.26

Evaluated at bid price : 16.26

Bid-YTW : 7.15 % |

| BMO.PR.L |

Perpetual-Discount |

-1.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 19.32

Evaluated at bid price : 19.32

Bid-YTW : 7.60 % |

| DFN.PR.A |

SplitShare |

-1.38 % |

Asset coverage of 1.5-:1 as of February 27 according to the company.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2014-12-01

Maturity Price : 10.00

Evaluated at bid price : 7.84

Bid-YTW : 10.48 % |

| ACO.PR.A |

OpRet |

-1.35 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2011-11-30

Maturity Price : 25.00

Evaluated at bid price : 25.60

Bid-YTW : 4.89 % |

| CM.PR.M |

FixedReset |

-1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 22.94

Evaluated at bid price : 24.45

Bid-YTW : 6.29 % |

| PWF.PR.F |

Perpetual-Discount |

-1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 16.10

Evaluated at bid price : 16.10

Bid-YTW : 8.32 % |

| BNS.PR.K |

Perpetual-Discount |

-1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 17.30

Evaluated at bid price : 17.30

Bid-YTW : 7.06 % |

| SBN.PR.A |

SplitShare |

-1.06 % |

Asset coverage of 1.5-:1 as of March 5 according to Mulvihill.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2014-12-01

Maturity Price : 10.00

Evaluated at bid price : 8.42

Bid-YTW : 8.97 % |

| STW.PR.A |

Interest-Bearing |

-1.04 % |

Asset coverage of 1.4+:1 as of March 5, based on Capital Unit NAV of 2.02. and 1.99 Capital Units per Preferred.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2009-12-31

Maturity Price : 10.00

Evaluated at bid price : 9.56

Bid-YTW : 13.25 % |

| CM.PR.E |

Perpetual-Discount |

1.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 17.76

Evaluated at bid price : 17.76

Bid-YTW : 8.04 % |

| GWO.PR.E |

OpRet |

1.03 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2014-03-30

Maturity Price : 25.00

Evaluated at bid price : 24.50

Bid-YTW : 5.12 % |

| IGM.PR.A |

OpRet |

1.03 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2013-06-29

Maturity Price : 25.00

Evaluated at bid price : 25.41

Bid-YTW : 5.27 % |

| TD.PR.C |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 23.26

Evaluated at bid price : 23.30

Bid-YTW : 5.16 % |

| PWF.PR.G |

Perpetual-Discount |

1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.20

Evaluated at bid price : 18.20

Bid-YTW : 8.27 % |

| POW.PR.A |

Perpetual-Discount |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 17.75

Evaluated at bid price : 17.75

Bid-YTW : 8.07 % |

| TD.PR.R |

Perpetual-Discount |

1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 19.99

Evaluated at bid price : 19.99

Bid-YTW : 7.13 % |

| BNS.PR.M |

Perpetual-Discount |

1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 16.10

Evaluated at bid price : 16.10

Bid-YTW : 7.11 % |

| BNS.PR.O |

Perpetual-Discount |

1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 20.05

Evaluated at bid price : 20.05

Bid-YTW : 7.11 % |

| CM.PR.I |

Perpetual-Discount |

1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 15.00

Evaluated at bid price : 15.00

Bid-YTW : 7.99 % |

| BNS.PR.N |

Perpetual-Discount |

1.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.51

Evaluated at bid price : 18.51

Bid-YTW : 7.22 % |

| MFC.PR.B |

Perpetual-Discount |

1.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 14.50

Evaluated at bid price : 14.50

Bid-YTW : 8.08 % |

| RY.PR.H |

Perpetual-Discount |

1.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 20.80

Evaluated at bid price : 20.80

Bid-YTW : 6.88 % |

| SLF.PR.A |

Perpetual-Discount |

1.44 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 13.39

Evaluated at bid price : 13.39

Bid-YTW : 8.92 % |

| RY.PR.L |

FixedReset |

1.44 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 23.20

Evaluated at bid price : 23.24

Bid-YTW : 5.09 % |

| CM.PR.J |

Perpetual-Discount |

1.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 14.57

Evaluated at bid price : 14.57

Bid-YTW : 7.88 % |

| PWF.PR.E |

Perpetual-Discount |

1.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 17.00

Evaluated at bid price : 17.00

Bid-YTW : 8.25 % |

| CM.PR.D |

Perpetual-Discount |

1.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.47

Evaluated at bid price : 18.47

Bid-YTW : 7.94 % |

| SLF.PR.D |

Perpetual-Discount |

1.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 12.85

Evaluated at bid price : 12.85

Bid-YTW : 8.70 % |

| TD.PR.P |

Perpetual-Discount |

1.60 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.46

Evaluated at bid price : 18.46

Bid-YTW : 7.24 % |

| CM.PR.K |

FixedReset |

1.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 21.52

Evaluated at bid price : 21.85

Bid-YTW : 4.99 % |

| CU.PR.A |

Perpetual-Discount |

1.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 21.35

Evaluated at bid price : 21.35

Bid-YTW : 6.86 % |

| BNS.PR.L |

Perpetual-Discount |

1.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 16.41

Evaluated at bid price : 16.41

Bid-YTW : 6.98 % |

| CM.PR.P |

Perpetual-Discount |

1.73 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 17.61

Evaluated at bid price : 17.61

Bid-YTW : 7.97 % |

| BAM.PR.M |

Perpetual-Discount |

1.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 12.20

Evaluated at bid price : 12.20

Bid-YTW : 9.79 % |

| BAM.PR.N |

Perpetual-Discount |

1.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 12.18

Evaluated at bid price : 12.18

Bid-YTW : 9.81 % |

| ENB.PR.A |

Perpetual-Discount |

1.77 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 22.71

Evaluated at bid price : 23.00

Bid-YTW : 6.02 % |

| CM.PR.H |

Perpetual-Discount |

1.87 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 15.28

Evaluated at bid price : 15.28

Bid-YTW : 8.01 % |

| BAM.PR.J |

OpRet |

1.87 % |

YTW SCENARIO

Maturity Type : Soft Maturity

Maturity Date : 2018-03-30

Maturity Price : 25.00

Evaluated at bid price : 17.51

Bid-YTW : 10.66 % |

| ELF.PR.G |

Perpetual-Discount |

1.92 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 13.30

Evaluated at bid price : 13.30

Bid-YTW : 9.16 % |

| SLF.PR.E |

Perpetual-Discount |

2.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 13.16

Evaluated at bid price : 13.16

Bid-YTW : 8.59 % |

| GWO.PR.G |

Perpetual-Discount |

2.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 15.40

Evaluated at bid price : 15.40

Bid-YTW : 8.49 % |

| PWF.PR.A |

Floater |

2.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 11.45

Evaluated at bid price : 11.45

Bid-YTW : 3.85 % |

| HSB.PR.D |

Perpetual-Discount |

2.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 16.80

Evaluated at bid price : 16.80

Bid-YTW : 7.47 % |

| NA.PR.K |

Perpetual-Discount |

2.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 20.15

Evaluated at bid price : 20.15

Bid-YTW : 7.37 % |

| POW.PR.D |

Perpetual-Discount |

2.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 15.62

Evaluated at bid price : 15.62

Bid-YTW : 8.19 % |

| TD.PR.Q |

Perpetual-Discount |

2.38 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 20.20

Evaluated at bid price : 20.20

Bid-YTW : 7.05 % |

| GWO.PR.I |

Perpetual-Discount |

2.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 14.10

Evaluated at bid price : 14.10

Bid-YTW : 8.02 % |

| PWF.PR.K |

Perpetual-Discount |

2.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 14.90

Evaluated at bid price : 14.90

Bid-YTW : 8.48 % |

| BMO.PR.H |

Perpetual-Discount |

3.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 19.06

Evaluated at bid price : 19.06

Bid-YTW : 7.04 % |

| POW.PR.C |

Perpetual-Discount |

3.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.73

Evaluated at bid price : 18.73

Bid-YTW : 7.92 % |

| PWF.PR.L |

Perpetual-Discount |

3.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 15.31

Evaluated at bid price : 15.31

Bid-YTW : 8.50 % |

| BNS.PR.S |

FixedReset |

4.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 23.46

Evaluated at bid price : 26.00

Bid-YTW : 5.50 % |

| PWF.PR.H |

Perpetual-Discount |

4.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.15

Evaluated at bid price : 18.15

Bid-YTW : 8.08 % |

| BNA.PR.B |

SplitShare |

4.53 % |

Asset coverage of 1.7-:1 as of February 28 according to the company.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2016-03-25

Maturity Price : 25.00

Evaluated at bid price : 21.01

Bid-YTW : 8.02 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| TD.PR.P |

Perpetual-Discount |

124,400 |

Scotia crossed 21,300 at 18.50, then another 95,000 at the same price.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 18.46

Evaluated at bid price : 18.46

Bid-YTW : 7.24 % |

| RY.PR.T |

FixedReset |

83,101 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 23.07

Evaluated at bid price : 24.83

Bid-YTW : 5.90 % |

| TD.PR.I |

FixedReset |

80,955 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 23.09

Evaluated at bid price : 24.88

Bid-YTW : 5.96 % |

| CM.PR.L |

FixedReset |

55,289 |

National bought 13,800 from TD at 25.00.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 24.78

Evaluated at bid price : 24.83

Bid-YTW : 6.40 % |

| BNS.PR.X |

FixedReset |

48,297 |

Scotia bought 25,000 from HSBC at 25.15.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 25.16

Evaluated at bid price : 25.21

Bid-YTW : 6.22 % |

| CM.PR.M |

FixedReset |

44,785 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-03-11

Maturity Price : 22.94

Evaluated at bid price : 24.45

Bid-YTW : 6.29 % |

| There were 28 other index-included issues trading in excess of 10,000 shares. |