Matt Levine of Bloomberg ran a thoughtful – if disjointed – piece on bond market structure philosophy titled SEC Wants to Give Everyone a Chance to Be a Bond Trader:

There are more fundamental structural worries about declining liquidity in the bond markets: What will happen if investors want to sell and there are no dealers to buy?7 How risky is it to have so many bonds held by ETFs? Should big bond managers such as BlackRock and Pimco be regulated as too-big-to-fail risks to financial stability?

These are tough questions, but one plausible way of addressing them might be to open up trading of bonds somewhat. The current model of investors calling dealers for quotes makes sense if dealers provide a lot of liquidity; but if the dealers are just working as well-paid, information-hoarding middlemen between investors, then maybe there are more efficient ways for investors to interact. And in fact there have been efforts to develop electronic, inter-institution trading platforms that would make the bond markets a bit more like the stock markets, by allowing investors and dealers to post quotes in the same place, and trade directly with each other.

…

But what’s gotten attention was [chairman of the Securities and Exchange Commission Mary Jo] White’s call for more transparency in bond markets. In particular, White wants more technology-supported pre-trade transparency: That is, she wants more publicly available, electronically distributed, quotes for bonds, so you can know before you trade what prices are being offered in the market for the bond you want to buy. This would be a move toward making the bond market more like the equity market, with publicly posted quotes and potentially electronic (and high-frequency! maybe) trading.

…

The SEC’s job is to regulate the financial markets. One way to approach that job would be to put a priority on optimizing market efficiency and stability. Another way to approach it would be to put a priority on protecting retail investors and preventing two-bit frauds. Obviously both are good but one is more important. If you think about bond market structure in terms of protecting the little guy, you will make one set of choices; if you think about it in terms of providing a stable liquid platform for massive flows of capital, you will make a second, probably somewhat different, set of choices.14 The second set of choices is probably right.

Quite right, and this is something I have reiterated in PrefBlog to the point of boredom. Increased price transparency will result in shallower, more brittle bond markets; there’s tons of evidence supporting this thesis. But the SEC is leaning in the other direction:

The main U.S. securities regulator is ramping up calls to democratize a $40 trillion bond market, proposing that smaller investors receive more price information to avoid getting fleeced when buying less-traded debt.

The Securities and Exchange Commission wants retail investors to have the same access to privately negotiated bond prices as big institutions, allowing them to make better decisions about how much to pay for the securities, Chair Mary Jo White said yesterday. Releasing such information on corporate and municipal transactions would promote competition and better execution, she said.

…

Finra is expanding its bond-price reporting into the $1.5 trillion market for private company debt, which is only sold to institutional buyers.

Another effect will be the continued acceleration of the current trend towards private placements. So retail will be able to get lots of pricing information on every publicly traded bond there is, but there won’t be too many. So we’ll see even more retail portfolios highly concentrated with big household names – the GMACs and GMs of this world, as worked out so well during the Credit Crunch. Another possibility, that I would like to see more of, would be institutional accounts trading directly with each other, bypassing the dealers completely. Naturally, you’ll get a few institutional houses running hedge-fund-like actively managed bond portfolios dominating the market – I see nothing wrong with that.

There are few inflation worries in the Treasury market:

In the past 13 months, the gap between yields of two- and five-year Treasuries has doubled to 1.22 percentage points, according to data compiled by Bloomberg. At the same time, the difference between those of five- and 30-year securities has narrowed to the least since 2009 as the long bond rallied.

Because yields on longer-dated debt usually rise more than shorter-term notes when investors see faster inflation spurring rate increases, the moves suggest a more sanguine outlook, according to Priya Misra, the New York-based head of U.S. rates strategy at Bank of America Corp., one of 22 primary dealers obligated to bid at U.S. debt auctions.

Taken together, the relationship now implies that while investors anticipate the Fed will eventually lift its benchmark rate after holding it close to zero for six years, they don’t foresee the central bank’s stimulus measures creating the kind of inflationary pressures that would force its hand, she said.

“The bond vigilantes have all been quieted,” Misra said by telephone on June 19. “The idea that just the act of printing money gets you inflation has been debunked.”

That view also indicates there’s little concern over a repeat of 1994, one of the worst years for bonds when Treasuries lost more than 4 percent in the first six months as the Fed began to double its benchmark rate to 6 percent, according to the Bank of America Merrill Lynch U.S. Treasury Index. In part because of the Fed’s success as an inflation fighter, Treasuries generated returns in 2004, 2005 and 2006 even though the bank boosted rates to 5.25 percent from 1 percent.

This year, Treasuries have advanced 2.58 percent in the biggest year-to-date gain since 2011, even as the Fed began to pare back its $85 billion-a-month bond buying program.

I’ll believe it’s not 1994 all over again when the Fed actually hikes its policy rate! But we’ll see.

There is some concern about the bond market’s vulnerability to mass ETF redemptions – particularly in odd sectors:

It’s never been easier for individuals to enter some of the most esoteric debt markets. Wall Street’s biggest firms are worried that it’ll be just as simple for them to leave.

Investors have piled more than $900 billion into taxable bond funds since the 2008 financial crisis, buying stock-like shares of mutual and exchange-traded funds to gain access to infrequently-traded markets. This flood of cash has helped cause prices to surge and yields to plunge.

Now, as the Federal Reserve discusses ending its easy-money policies, concern is mounting that the withdrawal of stimulus will lead to an exodus that’ll cause credit markets to freeze up. While new regulations have forced banks to reduce their balance-sheet risk, analysts at JPMorgan Chase & Co. (JPM) are focusing on the problems that individual investors could cause by yanking money from funds.

…

That concern is also revealed in BlackRock Inc.’s pitch in a paper published last month that regulators should consider redemption restrictions for some bond mutual funds, including extra fees for large redeemers.A year ago, bond funds suffered record withdrawals amid hysteria about a sudden increase in benchmark yields. A 0.8 percentage point rise in the 10-year Treasury yield in May and June last year spurred a sell-off that caused $248 billion of market value losses on the Bank of America Merrill Lynch U.S. Corporate and High Yield Index.

Of course, yields on 10-year Treasuries (USGG10YR) have since fallen to 2.6 percent from 3 percent at the end of December and company bonds have resumed their rally. Analysts are worrying about what happens when the gift of easy money goes away for good.

US municipalities are a little gun-shy when it comes to infrastructure:

Across the U.S., localities are refraining from raising new funds in the $3.7 trillion municipal-bond market after the worst financial crisis since the Great Depression left them with unprecedented deficits. Rather than take advantage of Federal Reserve (FDTR) policy that’s held benchmark interest rates at historic lows since December 2008, they’re repaying obligations by the most on record.

…

Issuance this year has tumbled to $123 billion nationwide through June 13, down 20 percent from the 2013 pace, according to data compiled by Bloomberg. It’s also 30 percent below levels seen in 2010, the final year of the federally subsidized Build America Bonds program, which was designed to spur infrastructure investment.Since 2010, states and localities have lowered their bond load by $111 billion, the most since the Fed began keeping records in 1945. They’ve paid down the liabilities even as yields on 20-year general obligations have averaged 4.25 percent in the five years since the recession, the lowest since 1969, according to Bond Buyer data.

…

America’s governments would need to spend about $3.6 trillion through 2020 to put everything from roads and water to sewers and electricity networks into adequate shape, according to the American Society of Civil Engineers, based in Reston, Virginia. That’s about $1.6 trillion more than governments are expected to dispense.

Meanwhile, the Minister of Asset Allocation has market-timing advice:

Canada’s Finance Minister Joe Oliver warned on Monday that investors could be mispricing risk as they hunt for better investment returns, and said policymakers should keep the issue under close review.

Oliver is in London to promote trade and investment, and told Reuters in an interview that the global economy remained vulnerable to financial shocks.

“We’ve said again and again … that international financial markets are still fragile. Part of that is macroeconomic and monetary issues, but there is a geopolitical issue,” he said at the London residence of Canada’s envoy to London.

James Langton of Investment Executive highlights some interesting research in his piece Video better than text in boosting financial literacy:

New research finds that online video may be a particularly effective way of bolstering financial literacy.

According to a new paper (Visual Tools and Narratives: New Ways to Improve Financial Literacy) published by the U.S. National Bureau of Economic Research (NBER), video appears to be better at improving basic financial literacy than text-based approaches. The conclusion is based on an experiment financed by a grant from the U.S. Social Security Administration (SSA), and funded as part of the Financial Literacy Research Consortium.

Researchers developed four different online approaches to explaining the concept of risk diversification — a brochure, an interactive visual tool, a written narrative, and a video — and then tested them with a sample of 900 people. Overall, they found that video performed the best at both improving financial literacy scores and increasing people’s levels of confidence in their financial knowledge.

The actual paper is titled Visual Tools and Narratives: New Ways to Improve Financial Literacy:

We developed and experimentally evaluated four novel educational programs delivered online: an informational brochure, a visual interactive tool, a written narrative, and a video narrative. The programs were designed to inform people about risk diversification, an essential concept for financial decision- making. The effectiveness of these programs was evaluated using the RAND American Life Panel. Participants were exposed to one of the programs, and then asked to answer questions measuring financial literacy and self-efficacy. All of the programs were found to be effective at increasing self-efficacy, and several improved financial literacy, providing new evidence for the value of programs designed to help individuals make financial decisions. The video was more effective at improving financial literacy scores than the written narrative, highlighting the power of online media in financial education.

Institutional subscribers to the NBER working paper series, and residents of developing countries may download this paper without additional charge at www.nber.org.

Well, I’m not paying for it.

Anyway, I had been hoping to read it to check what their actual conclusion regarding videos is. I suspect – although without reading the paper this is mere speculation, of course – that what they have measured is people’s ease of learning via different media, rather than anything specific to financial literacy. I hate videos and lectures. If I’m going to learn anything, I’ve got to read it. It’s entirely possible that all that has been discovered is that I am in the minority, which I knew already.

Nice to see such work being done, though. Here in Canada, potential funding for such research is instead splashed out to cronies with zero public benefit.

It was a modestly good day for the Canadian preferred share market, with PerpetualDiscounts gaining 7bp, FixedResets winning 9bp and DeemedRetractibles up 8bp. Volatility was average, skewed to winners. Volume was below average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4787 % | 2,491.4 |

| FixedFloater | 4.43 % | 3.69 % | 28,816 | 17.95 | 1 | -0.0932 % | 3,873.3 |

| Floater | 2.94 % | 3.06 % | 44,199 | 19.58 | 4 | 0.4787 % | 2,690.0 |

| OpRet | 4.38 % | -9.03 % | 23,129 | 0.08 | 2 | 0.0195 % | 2,711.6 |

| SplitShare | 4.83 % | 4.41 % | 58,130 | 4.09 | 5 | -0.0399 % | 3,106.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0195 % | 2,479.5 |

| Perpetual-Premium | 5.52 % | -0.94 % | 80,996 | 0.09 | 17 | 0.0739 % | 2,406.6 |

| Perpetual-Discount | 5.26 % | 5.26 % | 112,725 | 14.97 | 20 | 0.0664 % | 2,556.1 |

| FixedReset | 4.46 % | 3.69 % | 206,436 | 6.66 | 78 | 0.0855 % | 2,543.8 |

| Deemed-Retractible | 4.99 % | 1.30 % | 132,472 | 0.17 | 43 | 0.0751 % | 2,538.6 |

| FloatingReset | 2.67 % | 2.39 % | 123,281 | 3.94 | 6 | -0.1579 % | 2,495.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.A | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 22.29 Evaluated at bid price : 23.06 Bid-YTW : 3.83 % |

| BAM.PR.B | Floater | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 17.05 Evaluated at bid price : 17.05 Bid-YTW : 3.07 % |

| FTS.PR.J | Perpetual-Discount | 1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 23.40 Evaluated at bid price : 23.75 Bid-YTW : 5.03 % |

| GWO.PR.N | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.76 Bid-YTW : 4.62 % |

| W.PR.H | Perpetual-Premium | 1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 24.84 Evaluated at bid price : 25.07 Bid-YTW : 5.58 % |

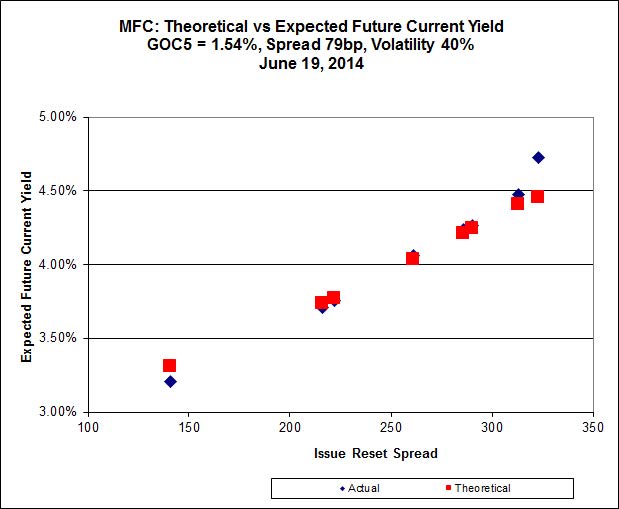

| MFC.PR.B | Deemed-Retractible | 2.14 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.40 Bid-YTW : 5.49 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.H | FixedReset | 292,590 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 23.21 Evaluated at bid price : 25.19 Bid-YTW : 3.74 % |

| ENB.PF.C | FixedReset | 215,075 | Nesbitt crossed blocks of 45,000 and 100,000, both at 25.14. Scotia crossed 50,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 23.16 Evaluated at bid price : 25.13 Bid-YTW : 4.19 % |

| RY.PR.L | FixedReset | 108,216 | Nesbitt crossed 100,000 at 26.30. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-02-24 Maturity Price : 25.00 Evaluated at bid price : 26.35 Bid-YTW : 3.10 % |

| TD.PF.A | FixedReset | 101,430 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 23.21 Evaluated at bid price : 25.22 Bid-YTW : 3.72 % |

| CM.PR.O | FixedReset | 99,425 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-23 Maturity Price : 23.22 Evaluated at bid price : 25.19 Bid-YTW : 3.78 % |

| GWO.PR.I | Deemed-Retractible | 75,201 | TD crossed 70,000 at 22.80. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.51 Bid-YTW : 5.79 % |

| There were 24 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.F | FixedReset | Quote: 23.06 – 23.85 Spot Rate : 0.7900 Average : 0.6585 YTW SCENARIO |

| BAM.PR.X | FixedReset | Quote: 22.12 – 22.44 Spot Rate : 0.3200 Average : 0.2372 YTW SCENARIO |

| BNA.PR.C | SplitShare | Quote: 24.79 – 25.00 Spot Rate : 0.2100 Average : 0.1341 YTW SCENARIO |

| CU.PR.G | Perpetual-Discount | Quote: 22.29 – 22.53 Spot Rate : 0.2400 Average : 0.1642 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 20.87 – 21.25 Spot Rate : 0.3800 Average : 0.3183 YTW SCENARIO |

| GWO.PR.I | Deemed-Retractible | Quote: 22.51 – 22.80 Spot Rate : 0.2900 Average : 0.2286 YTW SCENARIO |