These are deflationary times in Europe:

Professional forecasters surveyed by the ECB before the QE announcement saw price growth of 0.3 percent this year and 1.1 percent in 2016. The bond-buying program is seen adding 0.4 percentage point and 0.3 percentage point respectively, according to a euro-area central bank official who has seen the ECB’s internal calculations.

In a Bloomberg News survey of 38 economists, the median forecast for January is for prices to drop 0.5 percent from a year earlier. That would follow a 0.2 percent decline in December and mark the second-biggest decrease since the creation of the euro in 1999. The record drop was in the depths of the recession, when prices fell 0.6 percent in July 2009. The data will be published at 11 a.m. in Luxembourg on Friday.

A separate report will show that unemployment in the region held at 11.5 percent in December, still near its record high of 12 percent. Persistently high joblessness, along with a backlash against austerity, was one of the key factors behind the victory of the Syriza party in elections in Greece on Sunday.

Some investors have become emboldened to justify their holdings of negative-yield debt:

Mike Amey never thought he’d buy bonds from countries like Germany and Switzerland when losses were all but guaranteed.

…

“It’s not a good feeling,” said Amey, whose firm runs the world’s biggest bond fund and is one of the largest investors in nations with negative yields. Others include BlackRock Inc., Deutsche Asset & Wealth Management and Vanguard Group, data compiled by Bloomberg show.The seemingly insatiable demand for only the safest assets underscores the challenge the European Central Bank faces in convincing bond investors it has the wherewithal to jump-start the euro region after consumer prices fell for the first time in five years. Last week, ECB President Mario Draghi pledged to pump 1.1 trillion euros ($1.2 trillion) into the region’s economies by buying public and private debt.

Although the ECB’s move may push more investors into riskier assets, JPMorgan Asset Management’s David Tan says it’s possible to profit from holding negative-yielding debt.

The central bank’s full-scale quantitative easing, which starts in March, will lift prices of even the most-expensive bonds, while the potential for deflation to persist in the euro area means investors will see their purchasing power increase.

“It still makes sense to hold the bonds” when the alternative is the ECB’s deposit rate of minus 0.2 percent, said Tan, the London-based head of global rates at JPMorgan Asset, which oversees about $1.7 trillion.

Tan purchased German five-year notes when yields plunged to zero this month. The debt has since rallied, pushing yields to an all-time low of minus 0.06 percent last week. The rate was 0.01 percent at 10 a.m. in New York.

Fans of negative yields will be please to note that, given the recent 50bp-odd decline in five-year Canada yields, five year mortgages have come down a whopping 10bp:

Royal Bank of Canada is the first major lender to lower mortgage rates after five-year bond yields fell in the wake of a surprise cut by the Bank of Canada last week, according to rate-monitoring websites.

Royal Bank, the country’s second-biggest lender by assets, offered a five-year fixed rate of 2.84 per cent on Jan. 24, down from 2.94 per cent last week, according to rate-tracking website Ratespy.com. That’s below RBC’s posted rate of 4.84 per cent. The bank also trimmed its three-, seven-, and 10-year rates, according to CanadianMortgageTrends.com, an industry news website.

S&P, which last downgraded Russia in April, cut the sovereign one step to BB+, according to a statement released on Monday, the same as countries including Bulgaria and Indonesia. The ratings firm said the outlook is “negative.” Russian stocks on U.S. exchanges tumbled with the ruble following the announcement which came after the close of equity trading in Moscow.

…

“Russia’s monetary-policy flexibility has become more limited and its economic growth prospects have weakened,” S&P said in a statement. “We also see a heightened risk that external and fiscal buffers will deteriorate due to rising external pressures and increased government support to the economy.”The ruble, the world’s second-worst performer last year after a 46 percent plunge against the dollar, plummeted after the S&P decision and closed 6.6 percent weaker at 68.7990 versus the U.S. currency on Monday. A Bloomberg index of the most-traded Russian stocks in the U.S. ended a three-day gain, tumbling 5.5 percent.

Bombardier, proud issuer of BBD.PR.B, BBD.PR.C and BBD.PR.D, has been placed on Review-Negative by Moody’s. I have updated the post that reported S&P’s downgrade of BBD earlier this month.

Brookfield Office Properties Inc., proud issuer of BPO.PR.A, BPO.PR.H, BPO.PR.J, BPO.PR.K, BPO.PR.N, BPO.PR.P, BPO.PR.R, BPO.PR.T,BPO.PR.W, BPO.PR.X and BPO.PR.Y, has been confirmed at Pfd-3 by DBRS:

DBRS Limited (DBRS) has today confirmed the Senior Unsecured Notes of Brookfield Office Properties Inc. (Brookfield or the Company) at BBB and its Cumulative Preferred Shares, Class AAA at Pfd-3, both with Stable trends. The confirmation reflects the successful re-leasing of the Bank of America/Merrill Lynch space at Brookfield Place New York. The confirmation also acknowledges that Brookfield’s coverage ratios will remain under pressure in the near term because of the re-leasing transition period of the aforementioned space. DBRS expects that coverage ratios should recover following this transition period but will remain at weak levels for the current rating category. DBRS notes that a prolonged weakness in operating performance (excluding the lease transition period of Brookfield Place New York) and/or a change in financial policy that results in further deterioration of key credit metrics could result in a Negative trend change.

The current ratings are based on Brookfield’s large, premier office portfolio, its presence in relatively stronger office markets and long-term leases to high quality tenants. DBRS expects these attributes to provide reasonable underlying support to the Company’s earnings profile. In addition, DBRS notes that Brookfield should also benefit from improving office fundamentals in the Company’s major U.S. markets, particularly downtown New York. Lower unemployment levels and a recovering economic environment in the United States should contribute to higher rental rates.

It was another violently mixed day for the Canadian preferred share market, with PerpetualDiscounts off 4bp, FixedResets down 38bp and DeemedRetractibles gaining 9bp. There is what has become the usual lengthy list of performance highlights, dominated by FixedReset losers. Volume was above average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

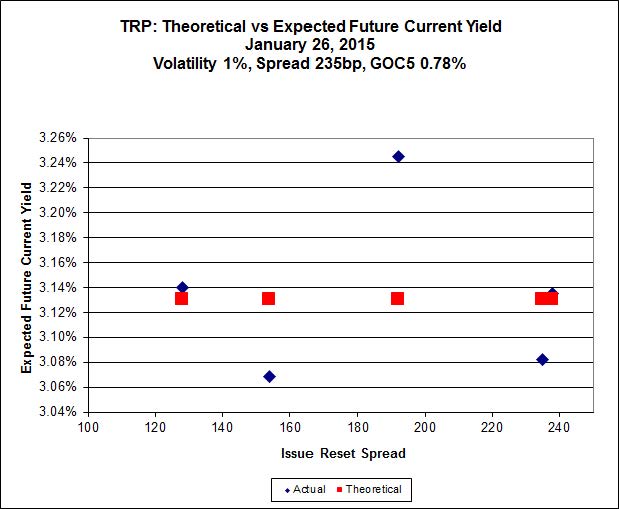

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 20.80, is $0.77 cheap, but it has already reset (at +192). TRP.PR.C, bid at 18.90 and resetting at +154bp on 2016-1-30 is $0.37 rich.

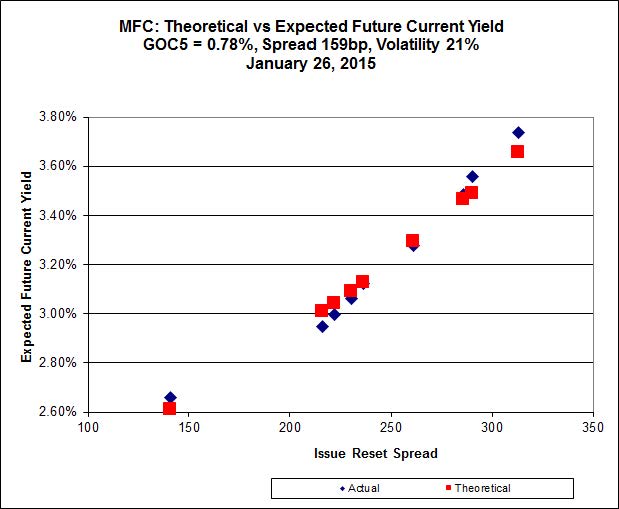

Click for Big

MFC.PR.F continues to be near the line defined by its peers.

Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

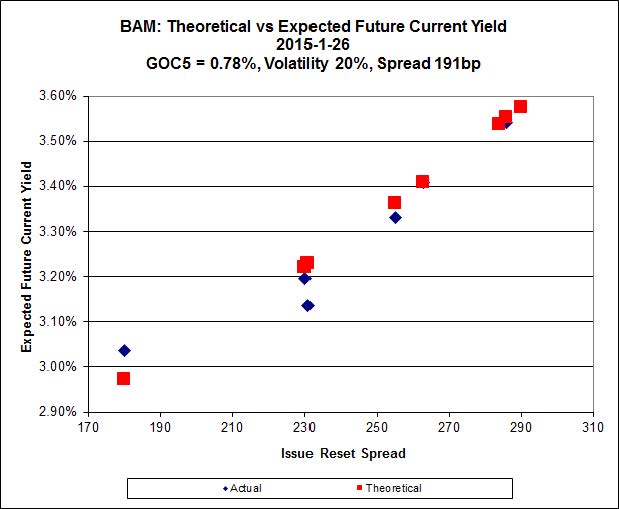

Click for Big

There continues to be cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, which is bid at 21.25 and appears to be $0.46 cheap, while BAM.PR.T, resetting at +231bp 2017-3-31 is bid at 24.63 and appears to be $0.71 rich.

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.22, looks $0.94 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 25.16, looks $1.13 expensive and resets 2019-3-1.

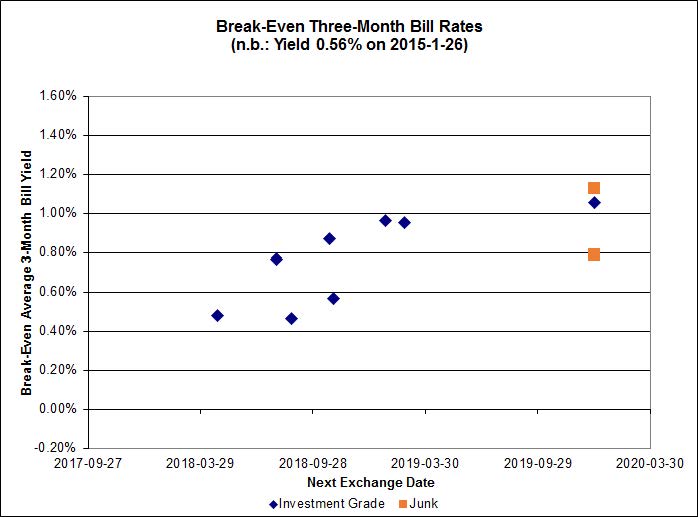

Click for Big

Pairs equivalence is looking more rational, with the investment grade pairs (which are presumably more closely watched and easier to trade) do show a rising trend with increasing time to interconversio which, qualitatively speaking, is entirely reasonable, although the increase (over five years-odd) looks pretty substantial given the scale of the chart (two years-odd). The average break-even rate is way down from recent levels again today.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.6627 % | 2,437.4 |

| FixedFloater | 4.44 % | 3.63 % | 18,518 | 18.23 | 1 | 0.1404 % | 3,981.4 |

| Floater | 3.11 % | 3.26 % | 54,506 | 19.08 | 4 | -0.6627 % | 2,591.2 |

| OpRet | 4.06 % | 2.47 % | 103,651 | 0.39 | 1 | -0.3549 % | 2,745.5 |

| SplitShare | 4.29 % | 4.08 % | 32,373 | 3.60 | 5 | -0.1059 % | 3,185.0 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.3549 % | 2,510.5 |

| Perpetual-Premium | 5.42 % | -6.99 % | 54,825 | 0.09 | 19 | -0.0945 % | 2,509.7 |

| Perpetual-Discount | 5.01 % | 4.86 % | 108,519 | 15.14 | 16 | -0.0359 % | 2,768.1 |

| FixedReset | 4.25 % | 3.21 % | 206,127 | 17.31 | 77 | -0.3797 % | 2,515.3 |

| Deemed-Retractible | 4.91 % | 0.26 % | 103,019 | 0.16 | 39 | 0.0929 % | 2,644.2 |

| FloatingReset | 2.44 % | 2.58 % | 67,041 | 6.46 | 7 | -0.5450 % | 2,400.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BNS.PR.Z | FixedReset | -3.72 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.03 Bid-YTW : 3.65 % |

| BAM.PR.Z | FixedReset | -3.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.48 Evaluated at bid price : 25.25 Bid-YTW : 3.76 % |

| TRP.PR.C | FixedReset | -2.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 3.20 % |

| SLF.PR.G | FixedReset | -2.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.10 Bid-YTW : 5.39 % |

| BAM.PR.X | FixedReset | -1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 21.25 Evaluated at bid price : 21.25 Bid-YTW : 3.34 % |

| GWO.PR.P | Deemed-Retractible | -1.58 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-03-31 Maturity Price : 25.25 Evaluated at bid price : 26.15 Bid-YTW : 4.68 % |

| FTS.PR.F | Perpetual-Discount | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 24.46 Evaluated at bid price : 24.71 Bid-YTW : 5.02 % |

| BAM.PR.B | Floater | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 16.08 Evaluated at bid price : 16.08 Bid-YTW : 3.29 % |

| TD.PR.Z | FloatingReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.31 Bid-YTW : 2.60 % |

| PWF.PR.A | Floater | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 2.75 % |

| TRP.PR.B | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 16.40 Evaluated at bid price : 16.40 Bid-YTW : 3.21 % |

| RY.PR.H | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.25 Evaluated at bid price : 25.16 Bid-YTW : 3.04 % |

| TD.PF.A | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.23 Evaluated at bid price : 25.16 Bid-YTW : 3.04 % |

| TRP.PR.F | FloatingReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 3.05 % |

| BAM.PR.T | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.40 Evaluated at bid price : 24.63 Bid-YTW : 3.21 % |

| BAM.PF.A | FixedReset | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.46 Evaluated at bid price : 25.54 Bid-YTW : 3.63 % |

| BAM.PF.G | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.31 Evaluated at bid price : 25.55 Bid-YTW : 3.64 % |

| BAM.PF.E | FixedReset | -1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.15 Evaluated at bid price : 25.00 Bid-YTW : 3.48 % |

| BMO.PR.R | FloatingReset | -1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.65 Bid-YTW : 2.44 % |

| GWO.PR.R | Deemed-Retractible | 1.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.25 Bid-YTW : 4.74 % |

| IFC.PR.C | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.04 Bid-YTW : 3.60 % |

| ENB.PF.G | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 22.81 Evaluated at bid price : 24.15 Bid-YTW : 3.80 % |

| PWF.PR.P | FixedReset | 1.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 21.01 Evaluated at bid price : 21.01 Bid-YTW : 2.94 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BMO.PR.P | FixedReset | 559,873 | Called for redemption February 25. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.30 Bid-YTW : 1.93 % |

| RY.PR.I | FixedReset | 117,341 | National sold 25,000 to Scotia and 14,500 to TD, both at 25.30. Scotia crossed 45,000 and TD crossed 15,000, both at the same price. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.31 Bid-YTW : 2.96 % |

| TD.PF.C | FixedReset | 101,135 | TD crossed 25,800 at 25.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.16 Evaluated at bid price : 25.01 Bid-YTW : 3.08 % |

| TD.PF.B | FixedReset | 82,839 | TD crossed 31,500 at 25.12. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.23 Evaluated at bid price : 25.10 Bid-YTW : 3.05 % |

| FTS.PR.M | FixedReset | 73,810 | Scotia crossed 46,400 at 25.60. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.31 Evaluated at bid price : 25.42 Bid-YTW : 3.27 % |

| CM.PR.P | FixedReset | 63,750 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-01-26 Maturity Price : 23.16 Evaluated at bid price : 25.01 Bid-YTW : 3.08 % |

| There were 39 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BNS.PR.Z | FixedReset | Quote: 23.03 – 23.80 Spot Rate : 0.7700 Average : 0.4431 YTW SCENARIO |

| FTS.PR.F | Perpetual-Discount | Quote: 24.71 – 25.15 Spot Rate : 0.4400 Average : 0.2661 YTW SCENARIO |

| TD.PR.Z | FloatingReset | Quote: 24.31 – 24.69 Spot Rate : 0.3800 Average : 0.2615 YTW SCENARIO |

| ENB.PR.P | FixedReset | Quote: 22.36 – 22.89 Spot Rate : 0.5300 Average : 0.4146 YTW SCENARIO |

| CGI.PR.D | SplitShare | Quote: 25.10 – 25.50 Spot Rate : 0.4000 Average : 0.2870 YTW SCENARIO |

| BNS.PR.P | FixedReset | Quote: 25.32 – 25.70 Spot Rate : 0.3800 Average : 0.2719 YTW SCENARIO |