Negative yields bring reaching for yield:

Norway’s $870 billion sovereign wealth fund said this month that it added Nigeria and lifted its share of lower-rated company debt to the highest since at least 2006. Allianz SE, Europe’s biggest insurer, is shifting from German bunds to bulk up on mortgages. JPMorgan Asset Management is buying speculative-grade corporate debt to boost returns.

…

Norges Bank Investment Management, the world’s largest sovereign wealth fund, increased corporate bonds rated BBB or lower to 8.3 percent of its debt assets at the end of last year from 7.5 percent in the prior quarter, the fund said March 13.Among those assets are about $200 million of bonds issued by Petroleo Brasiliero SA. Brazil’s state-controlled oil company, the biggest corporate debt issuer in emerging markets, has seen its benchmark 2024 bonds tumble almost 10 percent since allegations of kickbacks and bribes emerged in November.

The fund also added developing countries such as Ghana and Mauritius and invested in Nigeria’s currency for the first time. It has just 0.1 percent in top-rated corporate bonds.

Scotia has announced a sub-debt offering with a coupon of 2.58% to its pretend-maturity of 2022-3-30:

The Bank of Nova Scotia (“Scotiabank”) (TSX: BNS) (NYSE: BNS) today announced an inaugural Basel III-compliant offering of $1.25 billion of 2.58% Subordinated Debentures due 2027 (the “Debentures”) pursuant to its June 27, 2014 base shelf prospectus.

The Debentures, to be sold through an agency syndicate led by Scotiabank Global Banking & Markets, are expected to be issued on March 30, 2015. Interest will be payable semi-annually from the date of issue until March 30, 2022 at a rate of 2.58% per annum. From March 30, 2022 to maturity on March 30, 2027, the Debentures will pay a quarterly coupon at a rate equal to the 90 day bankers’ acceptance plus 1.19%, beginning June 30, 2022.

On or after March 30, 2022, Scotiabank may, at its option, with the prior approval of the Superintendent of Financial Institutions (Canada), in whole at any time or in part from time to time at a redemption price which is equal to par, plus accrued and unpaid interest, redeem the Debentures, on not less than 30 nor more than 60 days’ notice to registered holders.

Net proceeds from this transaction will be used for general banking purposes.

Scotiabank intends to file, in Canada, a pricing supplement to its June 27, 2014 base shelf prospectus. A copy of this document as well as the base shelf prospectus can be obtained at www.sedar.com.

This issue is rated A(low) by DBRS (emphasis added):

DBRS assigned the NVCC Sub Debt a rating equal to the Bank’s intrinsic assessment of AA (low) less three rating notches because the NVCC Sub Debt has the Office of the Superintendent of Financial Institutions (OSFI)-required non-viability contingent capital (NVCC) triggers and no additional triggers. Furthermore, DBRS has assumed that Scotiabank will follow the market precedent if issuing NVCC preferred shares in the future. Under this assumption, in the event of a conversion to common shares, the NVCC Sub Debt would have a potential for recovery that is sufficiently better than the NVCC Preferred Shares to allow for a differentiation in the NVCC Sub Debt rating relative to the NVCC Preferred Shares rating. Please see the DBRS press release entitled “DBRS Provides Guidance on Canadian Bank Non-Viability Contingent Capital Ratings” dated January 10, 2014, for more details.

I was hoping to learn today about the extent of the exercise of the hypothetical Unit Special Retraction Right of BSD / BSD.PR.A (discussed in the post BSD.PR.A Hypothetical Preferred Special Retraction Right: 44% Tender) but sadly there is nothing as yet.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts down 36bp, FixedResets off 4bp and DeemedRetractibles gaining 4bp. Volatility was much lower than what has become normal over the last four months. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

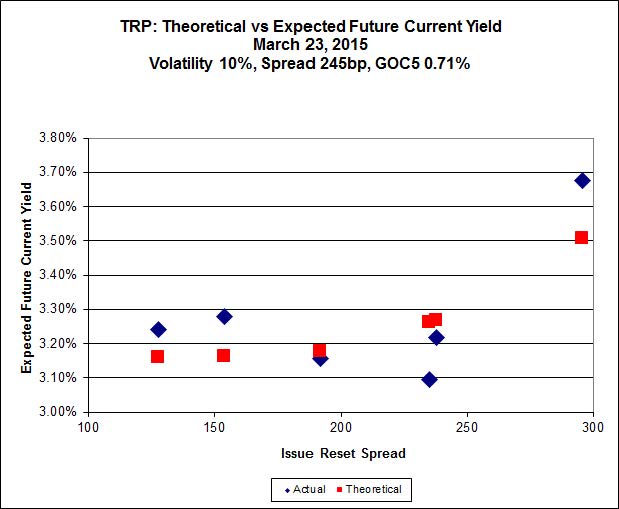

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 24.72 to be $1.25 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $1.21 cheap at its bid price of 24.95.

Click for Big

Another excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum, although it declined substantially today. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.L, resetting at +216 on 2019-6-19, bid at 24.30 to be $0.62 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 25.57 to be $0.61 cheap.

Click for Big

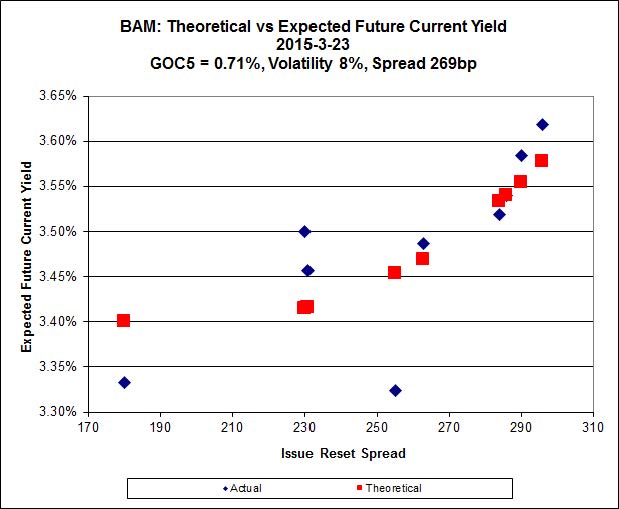

The fit on this series is actually quite reasonable – it’s the scale that makes it look so weird.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 21.50 to be $0.54 cheap. BAM.PF.E, resetting at +255bp 2020-3-31 is bid at 24.52 and appears to be $0.92 rich.

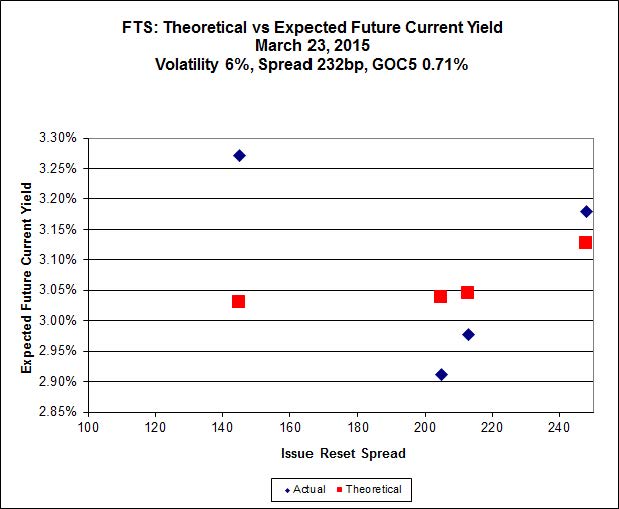

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 16.51, looks $1.31 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp and resetting 2019-3-1, is bid at 23.70 and is $0.99 rich.

Click for Big

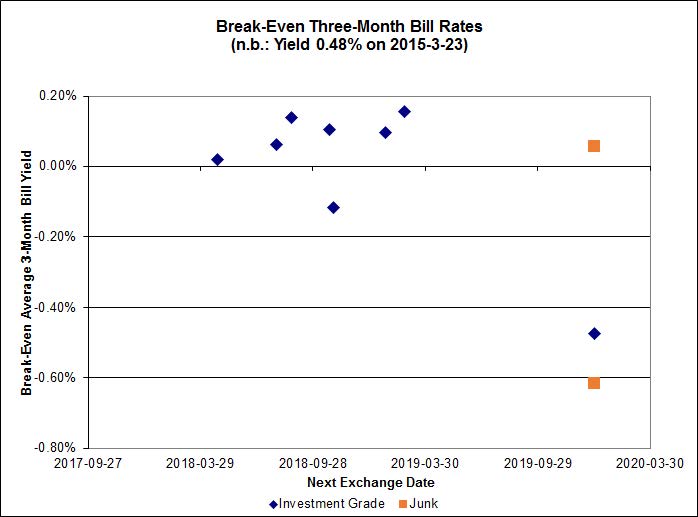

Investment-grade pairs predict an average over the next five years of a little under 0.10% – except for one outlier, TRP.PR.A / TRP.PR.F, which has a break-even of -0.47%. The DC.PR.B / DC.PR.D pair has gone from the extreme to the ludicrous and now predicts an average bill rate over the next 4 3/4 years of -2.30%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.5089 % | 2,340.1 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 2.5089 % | 4,091.7 |

| Floater | 3.24 % | 3.24 % | 62,102 | 19.15 | 3 | 2.5089 % | 2,487.7 |

| OpRet | 4.07 % | 0.96 % | 103,794 | 0.24 | 1 | 0.0000 % | 2,765.8 |

| SplitShare | 4.37 % | 4.42 % | 32,120 | 3.48 | 4 | -0.4988 % | 3,200.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,529.1 |

| Perpetual-Premium | 5.30 % | 0.81 % | 58,024 | 0.09 | 25 | 0.1094 % | 2,525.1 |

| Perpetual-Discount | 4.97 % | 5.02 % | 170,899 | 15.21 | 9 | -0.3621 % | 2,812.7 |

| FixedReset | 4.38 % | 3.44 % | 237,616 | 16.82 | 85 | -0.0421 % | 2,431.4 |

| Deemed-Retractible | 4.90 % | -1.46 % | 109,935 | 0.15 | 37 | 0.0352 % | 2,660.4 |

| FloatingReset | 2.43 % | 2.89 % | 83,375 | 6.31 | 8 | 0.3048 % | 2,340.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.D | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 22.85 Evaluated at bid price : 24.00 Bid-YTW : 3.36 % |

| ENB.PR.J | FixedReset | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 4.15 % |

| PVS.PR.C | SplitShare | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2017-12-10 Maturity Price : 25.00 Evaluated at bid price : 25.13 Bid-YTW : 4.75 % |

| BNS.PR.Z | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.31 Bid-YTW : 3.49 % |

| PWF.PR.T | FixedReset | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 23.41 Evaluated at bid price : 25.45 Bid-YTW : 3.11 % |

| TRP.PR.F | FloatingReset | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 3.15 % |

| HSE.PR.A | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 3.75 % |

| TRP.PR.C | FixedReset | 2.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 17.16 Evaluated at bid price : 17.16 Bid-YTW : 3.47 % |

| BAM.PR.K | Floater | 8.48 % | Not significant – just a reversal of Friday‘s nonsense. Thank you, Toronto Stock Exchange! YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 15.22 Evaluated at bid price : 15.22 Bid-YTW : 3.27 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.M | FixedReset | 300,440 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 22.98 Evaluated at bid price : 24.60 Bid-YTW : 3.35 % |

| RY.PR.Z | FixedReset | 202,531 | Nesbitt crossed blocks of 111,000 and 75,000, both at 25.15. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 23.23 Evaluated at bid price : 25.01 Bid-YTW : 3.01 % |

| RY.PR.J | FixedReset | 155,144 | Scotia crossed 150,000 at 25.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 23.15 Evaluated at bid price : 25.00 Bid-YTW : 3.39 % |

| TD.PF.D | FixedReset | 96,490 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 23.14 Evaluated at bid price : 24.99 Bid-YTW : 3.41 % |

| MFC.PR.L | FixedReset | 87,807 | Nesbitt crossed 84,000 at 24.43. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 3.71 % |

| BMO.PR.S | FixedReset | 77,489 | RBC crossed 75,000 at 25.12. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-03-23 Maturity Price : 23.23 Evaluated at bid price : 25.01 Bid-YTW : 3.11 % |

| There were 25 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TD.PR.T | FloatingReset | Quote: 24.03 – 24.70 Spot Rate : 0.6700 Average : 0.3918 YTW SCENARIO |

| GWO.PR.N | FixedReset | Quote: 18.37 – 18.87 Spot Rate : 0.5000 Average : 0.2989 YTW SCENARIO |

| ENB.PR.J | FixedReset | Quote: 21.35 – 21.80 Spot Rate : 0.4500 Average : 0.2841 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 18.72 – 19.14 Spot Rate : 0.4200 Average : 0.2841 YTW SCENARIO |

| BNS.PR.Z | FixedReset | Quote: 23.31 – 23.65 Spot Rate : 0.3400 Average : 0.2117 YTW SCENARIO |

| TRP.PR.D | FixedReset | Quote: 24.00 – 24.30 Spot Rate : 0.3000 Average : 0.1997 YTW SCENARIO |