“Markets, schmarkets!” says the US consumer, “Where can I spend what I just saved on gas?“:

Retail sales in the U.S. climbed for a second straight month, a sign consumers may be looking past recent volatility in financial markets.

The 0.2 percent increase in August followed a 0.7 percent gain in July that was larger than previously reported, Commerce Department figures showed Tuesday in Washington. The median forecast of 84 economists surveyed by Bloomberg called for a 0.3 percent advance.

Although confidence has taken a hit from stock-market turmoil and global-growth concerns, the data show households are still putting their savings from cheap energy to work. More jobs and higher pay would go a long way in supporting household spending, which Federal Reserve policy makers are watching as they consider raising interest rates as soon as this week.

Treasuries tumbled, lifting the two-year note yield to the highest since April 2011, as gains in U.S. retail sales prompted investors to retreat from the securities that would be most affected if the Federal Reserve raises interest rates.

Sell orders in two- and five-year Treasury futures helped accelerate the move higher in yields amid investors’ concern that the Fed may raise rates as soon as Thursday for the first time since 2006. Yields rose the most in almost three weeks after data showed retail sales increased 0.2 percent in August while July’s gain was larger than previously reported. The figures signal consumers may be looking past recent financial-market volatility.

…

Treasury two-year note yields rose eight basis points, or 0.08 percentage point, to 0.80 percent as of 5 p.m. in New York, based on Bloomberg Bond Trader data. The price of the 0.625 percent security due in August 2017 fell 5/32, or $1.56 per $1,000 face amount, to 99 21/32.Benchmark 10-year note yields rose 10 basis points to 2.29 percent.

Futures contracts show a 28 percent probability that the Fed will boost rates when it meets Sept. 16-17, according to data compiled by Bloomberg.The calculation is based on the assumption that the effective fed funds rate will average 0.375 percent after the first increase, versus the current target of zero to 0.25 percent.

It was a mostly lousy day for the Canadian preferred share market, with PerpetualDiscounts gaining 1bp, FixedResets down 58bp and DeemedRetractibles off 14bp. The Performance Highlights table is comprised almost entirely of losers. Volume was below average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

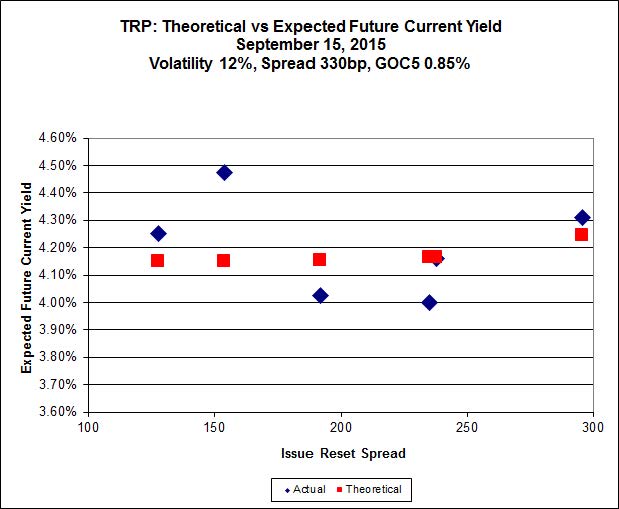

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 20.00 to be $0.79 rich, while TRP.PR.C, resetting 2016-1-30 at +164, is $1.05 cheap at its bid price of 13.35.

Click for Big

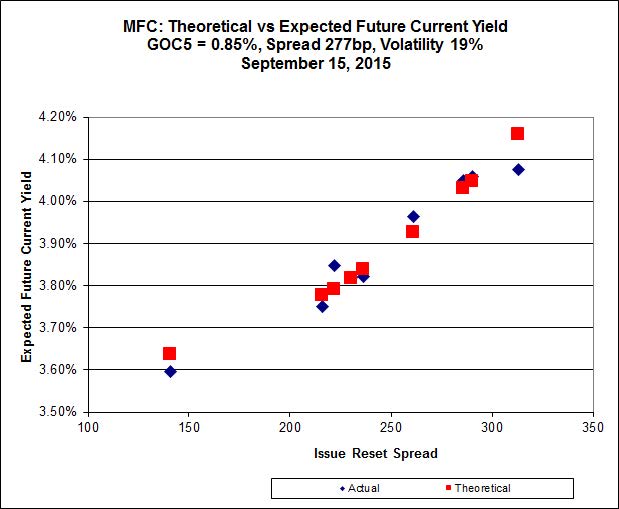

Another good fit today for MFC, with Implied Volatility falling a bit today.

Most expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 24.41 to be 0.48 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 19.95 to be 0.29 cheap.

Click for Big

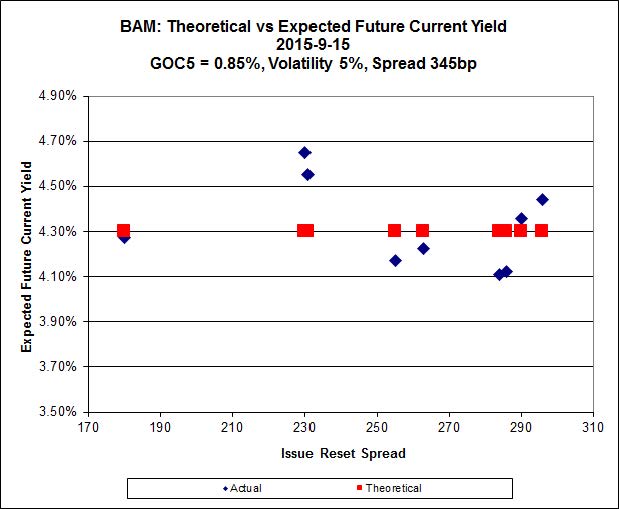

The fit on the BAM issues continues to be horrible.

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.90 to be $1.37 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 22.44 and appears to be $0.99 rich.

Click for Big

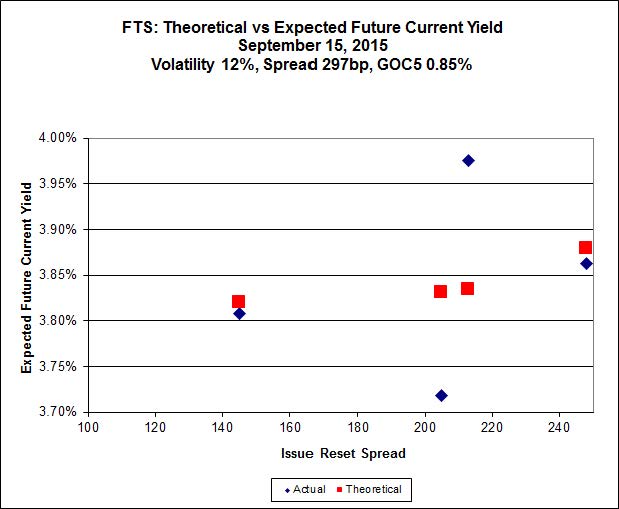

FTS.PR.K, with a spread of +205bp, and bid at 19.50, looks $0.57 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.74 and is $0.69 cheap.

Click for Big

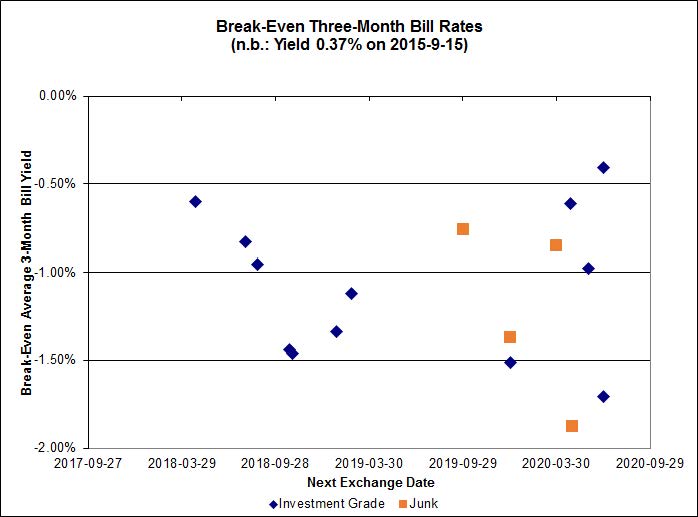

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -1.08%, with no outliers. The distribution is no longer bimodal. There are no junk outliers below -2.00%, but two above 0.00%.

Click for Big

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0315 % | 1,663.3 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0315 % | 2,908.2 |

| Floater | 4.47 % | 4.46 % | 56,225 | 16.53 | 3 | 0.0315 % | 1,768.2 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2572 % | 2,782.8 |

| SplitShare | 4.62 % | 5.03 % | 63,003 | 3.07 | 3 | 0.2572 % | 3,261.3 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2572 % | 2,544.6 |

| Perpetual-Premium | 5.72 % | 3.85 % | 54,940 | 0.08 | 8 | 0.0198 % | 2,492.7 |

| Perpetual-Discount | 5.45 % | 5.55 % | 69,845 | 14.55 | 30 | 0.0130 % | 2,600.8 |

| FixedReset | 4.72 % | 4.14 % | 176,254 | 16.16 | 74 | -0.5779 % | 2,159.0 |

| Deemed-Retractible | 5.13 % | 5.08 % | 94,906 | 5.50 | 33 | -0.1431 % | 2,589.3 |

| FloatingReset | 2.47 % | 3.89 % | 50,759 | 5.91 | 9 | -0.5791 % | 2,161.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.G | FixedReset | -2.86 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.70 Evaluated at bid price : 22.10 Bid-YTW : 4.23 % |

| MFC.PR.N | FixedReset | -2.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.62 Bid-YTW : 5.94 % |

| TD.PR.S | FixedReset | -2.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.21 Bid-YTW : 3.48 % |

| NA.PR.S | FixedReset | -2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.42 Evaluated at bid price : 21.75 Bid-YTW : 3.84 % |

| SLF.PR.C | Deemed-Retractible | -2.00 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.07 Bid-YTW : 6.75 % |

| BNS.PR.P | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 3.63 % |

| FTS.PR.H | FixedReset | -1.95 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 15.10 Evaluated at bid price : 15.10 Bid-YTW : 3.80 % |

| IAG.PR.G | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 4.65 % |

| MFC.PR.F | FixedReset | -1.94 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.71 Bid-YTW : 8.09 % |

| HSE.PR.G | FixedReset | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.95 Evaluated at bid price : 22.45 Bid-YTW : 4.84 % |

| MFC.PR.M | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.00 Bid-YTW : 5.76 % |

| TRP.PR.F | FloatingReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 14.65 Evaluated at bid price : 14.65 Bid-YTW : 3.89 % |

| HSE.PR.C | FixedReset | -1.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 4.96 % |

| SLF.PR.D | Deemed-Retractible | -1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.10 Bid-YTW : 6.73 % |

| BAM.PR.T | FixedReset | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 17.36 Evaluated at bid price : 17.36 Bid-YTW : 4.63 % |

| MFC.PR.G | FixedReset | -1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.10 Bid-YTW : 4.80 % |

| NA.PR.W | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.37 Evaluated at bid price : 21.37 Bid-YTW : 3.78 % |

| SLF.PR.H | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.02 Bid-YTW : 7.19 % |

| BMO.PR.M | FixedReset | -1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.30 Bid-YTW : 3.41 % |

| BNS.PR.D | FloatingReset | -1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.21 Bid-YTW : 4.88 % |

| PWF.PR.F | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 23.67 Evaluated at bid price : 23.94 Bid-YTW : 5.55 % |

| TRP.PR.C | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 13.35 Evaluated at bid price : 13.35 Bid-YTW : 4.43 % |

| BMO.PR.S | FixedReset | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.39 Evaluated at bid price : 21.71 Bid-YTW : 3.75 % |

| BNS.PR.A | FloatingReset | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.16 Bid-YTW : 3.69 % |

| GWO.PR.N | FixedReset | 1.21 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.10 Bid-YTW : 8.30 % |

| BAM.PF.D | Perpetual-Discount | 1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.43 Evaluated at bid price : 21.77 Bid-YTW : 5.63 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| NA.PR.M | Deemed-Retractible | 95,150 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2015-10-15 Maturity Price : 25.50 Evaluated at bid price : 25.79 Bid-YTW : -1.86 % |

| FTS.PR.G | FixedReset | 86,685 | Scotia crossed 25,000 at 18.90. Nesbitt crossed 25,000 at the same price.; RBC crossed 29,000 at the same price again. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 18.74 Evaluated at bid price : 18.74 Bid-YTW : 4.08 % |

| BMO.PR.T | FixedReset | 71,390 | Scotia crossed 60,000 at 21.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 21.32 Evaluated at bid price : 21.32 Bid-YTW : 3.75 % |

| BMO.PR.Q | FixedReset | 51,048 | RBC crossed 45,000 at 21.50. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.30 Bid-YTW : 5.00 % |

| BNS.PR.O | Deemed-Retractible | 50,768 | Nesbitt crossed 50,000 at 25.65. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-04-27 Maturity Price : 25.25 Evaluated at bid price : 25.65 Bid-YTW : 4.04 % |

| BAM.PR.R | FixedReset | 39,990 | RBC crossed 30,800 at 16.99. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-09-15 Maturity Price : 16.94 Evaluated at bid price : 16.94 Bid-YTW : 4.65 % |

| There were 27 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| VNR.PR.A | FixedReset | Quote: 19.89 – 20.95 Spot Rate : 1.0600 Average : 0.6101 YTW SCENARIO |

| MFC.PR.M | FixedReset | Quote: 21.00 – 21.90 Spot Rate : 0.9000 Average : 0.6707 YTW SCENARIO |

| SLF.PR.H | FixedReset | Quote: 18.02 – 18.55 Spot Rate : 0.5300 Average : 0.3767 YTW SCENARIO |

| TD.PR.S | FixedReset | Quote: 24.21 – 24.64 Spot Rate : 0.4300 Average : 0.2794 YTW SCENARIO |

| BNS.PR.D | FloatingReset | Quote: 20.21 – 20.65 Spot Rate : 0.4400 Average : 0.2898 YTW SCENARIO |

| BAM.PF.G | FixedReset | Quote: 22.44 – 22.81 Spot Rate : 0.3700 Average : 0.2284 YTW SCENARIO |

OK James, figure out the YTW on this puppy

http://www.bloomberg.com/news/articles/2015-09-16/yale-to-be-paid-interest-on-dutch-water-authority-bond-from-1648

Hah! Discussed on September 16.