Manulife Financial Corporation has announced:

that it has completed its offering of 16 million Non-cumulative Rate Reset Class 1 Shares Series 21 (the “Series 21 Preferred Shares”) at a price of $25 per share to raise gross proceeds of $400 million.

The offering was underwritten by a syndicate of investment dealers co-led by RBC Capital Markets, Scotia Capital Inc. and TD Securities Inc. The Series 21 Preferred Shares commence trading on the Toronto Stock Exchange today under the ticker symbol MFC.PR.O.

Manulife has granted the underwriters’ an option, exercisable in whole or in part, to purchase up to an additional 1 million Series 21 Preferred shares at the same offering price. The underwriters have 30 days from the closing of the preferred share offering to exercise the option.

The Series 21 Preferred Shares were issued under a prospectus supplement dated February 18, 2016 to Manulife’s short form base shelf prospectus dated December 17, 2015.

MFC.PR.O is a FixedReset, 5.60%+497, announced 2016-2-16. The issue will be tracked by HIMIPref™ and assigned to the FixedReset subindex.

As this issue is from an insurer and there is no provision for conversion into common shares at the option of the issuer, I consider this to be subject to my Deemed Retraction policy; accordingly I have placed a maturity entry dated 2025-1-31 at par in the call schedule of this instrument for analytical purposes. Note that this approach is due to analysis and there is no contractual provision in the terms of issue for any such maturity.

The issue traded 753,902 shares today (consolidated exchanges) in a range of 24.80-92 before closing at 24.86-89, 82×36. Since announcement date, the TXPL total return index has increased by 43bp since the announcement date, so ‘a little soft’ is an appropriate appraisal of its performance.

Vital statistics are:

| MFC.PR.O | FixedReset | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.86 Bid-YTW : 5.71 % |

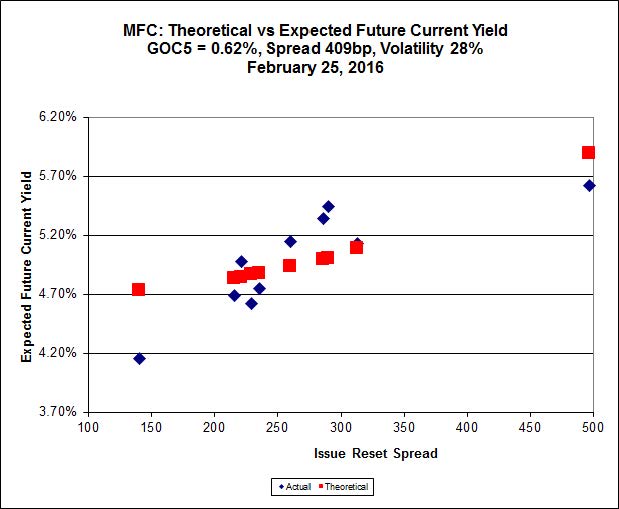

Implied volatility analysis indicates the issue is expensive at its current level:

Click for Big

According to this, the fair value for MFC.PR.O is 23.74 – and even at that, the slope of the theoretical line is clearly flattened by the influence of this issue. The issue is clearly well off the line defined by the lower-spread MFC issues.

I’m hoping that someone can help me understand this analysis for the price of MFC.pr.O. I’ve read everything that I can about implied volatility theory on the blog and in the newsletter but I’m afraid that I don’t fully understand it. I’m really curious to know if you actually think that MFC.pr.O should trade at $23.74 or if you just think that this is a spurious result from an inaccurate pricing model?

This new MFC issue pays a 5.6% dividend which is very much in line with recent bank fixed resets paying about 5.5% (and I believe the credit rating on this MFC is also the same as the bank issues). This would indicate to me (and the market seems to agree) that a price near $25 is quite reasonable for MFC.pr.O.

The above implied volatility analysis for MFC issues indicates that this new MFC issue should theoretically be yielding somewhere around 5.9% which is out of touch with market realities. I understand that implied volatility theory is based on a number of assumptions and approximations and thus cannot be relied upon for perfect results but in a case such as this where (to my simple way of thinking) the result is wrong, wouldn’t it make sense to adjust the theoretical implied volatility to fit the facts? ie. couldn’t you just “anchor” the theoretical implied volatility curve on the right at a yield of 5.6% for MFC.pr.O and then try and fit the curve to the other data points from there. This would presumably result in a lower volatility. Perhaps this tweaking of implied volatility curves is simply taboo and I’m missing the whole point of implied volatility analysis? Any help would be appreciated as I would really like to understand this.

thanks,

Brian

wouldn’t it make sense to adjust the theoretical implied volatility to fit the facts? ie. couldn’t you just “anchor” the theoretical implied volatility curve on the right at a yield of 5.6% for MFC.pr.O and then try and fit the curve to the other data points from there. This would presumably result in a lower volatility

The analysis finds the global minimum fitting error for the entire series; thus, any ‘anchoring’ of the curve will result in a worse fit than the one that has been found.

Mind you, the fitting error is defined as the sum of squares of pricing differences for each issue in the series. Define the fitting error in a different manner, you’ll get a different fit.

Additionally, the Implied Volatility is assumed to be the same for each issue; this ignores a few things, such as the fact that different issues will have different terms to their next reset and such intricacies as the “Volatility Smile”. You’ll have to research that one for yourself!

My calculations of implied volatility for preferred shares are just one piece of the puzzle. I take the view that the calculated richness of the high-spread new issues is qualitatively justified because

i) A lot of investors really love the high spread

ii) A lot of investors really love the idea that these are more likely to be called in five years than other issues (even though this will be a Bad Thing for their total returns)

iii) A few investors, with lots and lots of money, will buy large portions of the new issues as a way of gaining exposure to preferred shares in general, because they can do this with one ‘phone call and their time is too valuable to be wasted on doing their ostensible job.