Brookfield Renewable Partners L.P. has announced (on April 1, they say, but I swear I looked on their site and on Globe Newswire that night and didn’t find anything):

Brookfield Renewable Power Preferred Equity Inc. (“BRP Equity”) has determined the fixed dividend rate on its Class A Preference Shares, Series 1 (“Series 1 Shares”) (TSX:BRF.PR.A) for the five years commencing May 1, 2020 and ending April 30, 2025. If declared, the fixed quarterly dividends on the Series 1 Shares during that period will be paid at an annual rate of 3.137% ($0.196063 per share per quarter).

Holders of Series 1 Shares have the right, at their option, exercisable not later than 5:00 p.m. (Toronto time) on April 15, 2020, to convert all or part of their Series 1 Shares, on a one-for-one basis, into Class A Preference Shares, Series 2 (“Series 2 Shares”) (TSX:BRF.PR.B), effective April 30, 2020. Holders of Series 1 Shares are not required to elect to convert all or any part of their Series 1 Shares into Series 2 Shares.

The quarterly floating rate dividends on the Series 2 Shares will be paid at an annual rate, calculated for each quarter, of 2.62% over the annual yield on three-month Government of Canada treasury bills. The actual quarterly dividend rate in respect of the May 1, 2020 to July 31, 2020 dividend period for the Series 2 Shares will be 0.71911% (2.853% on an annualized basis) and the dividend, if declared, for such dividend period will be $0.179778 per share, payable on July 31, 2020.

Holders of Series 2 Shares have the right, at their option, exercisable not later than 5:00 p.m. (Toronto time) on April 15, 2020, to convert all or part of their Series 2 Shares, on a one-for-one basis, into Series 1 Shares, effective April 30, 2020. Holders of Series 2 Shares are not required to elect to convert all or any part of their Series 2 Shares into Series 1 Shares.

As provided in the share conditions of the Series 1 Shares, (i) if BRP Equity determines that there would be fewer than 1,000,000 Series 1 Shares outstanding after April 30, 2020, all remaining Series 1 Shares will be automatically converted into Series 2 Shares on a one-for-one basis effective April 30, 2020; and (ii) if BRP Equity determines that there would be fewer than 1,000,000 Series 2 Shares outstanding after April 30, 2020, no Series 1 Shares will be permitted to be converted into Series 2 Shares. There are currently 5,449,675 Series 1 Shares outstanding.

As provided in the share conditions of the Series 2 Shares, (i) if BRP Equity determines that there would be fewer than 1,000,000 Series 2 Shares outstanding after April 30, 2020, all remaining Series 2 Shares will be automatically converted into Series 1 Shares on a one-for-one basis effective April 30, 2020; and (ii) if BRP Equity determines that there would be fewer than 1,000,000 Series 1 Shares outstanding after April 30, 2020, no Series 2 Shares will be permitted to be converted into Series 1 Shares. There are currently 4,510,389 Series 2 Shares outstanding.

BRF.PR.A was issued as a FixedReset, 5.25%+262, that commenced trading 2010-3-10 after being announced 2010-2-18. It reset to 3.355% in 2015 and I recommended against conversion. Nevertheless, there was a 45% conversion to the FloatingReset.

BRF.PR.B is a FloatingReset, Float+262, that resulted from a 45% conversion from BRF.PR.A in 2015.

The most logical way to analyze the question of whether or not to convert is through the theory of Preferred Pairs, for which a calculator is available. Briefly, a Strong Pair is defined as a pair of securities that can be interconverted in the future (e.g., FFH.PR.M and the FloatingReset that will exist if enough holders convert). Since they will be interconvertible on this future date, it may be assumed that they will be priced identically on this date (if they aren’t then holders will simply convert en masse to the higher-priced issue). And since they will be priced identically on a given date in the future, any current difference in price must be offset by expectations of an equal and opposite value of dividends to be received in the interim. And since the dividend rate on one element of the pair is both fixed and known, the implied average rate of the other, floating rate, instrument can be determined. Finally, we say, we may compare these average rates and take a view regarding the actual future course of that rate relative to the implied rate, which will provide us with guidance on which element of the pair is likely to outperform the other until the next interconversion date, at which time the process will be repeated.

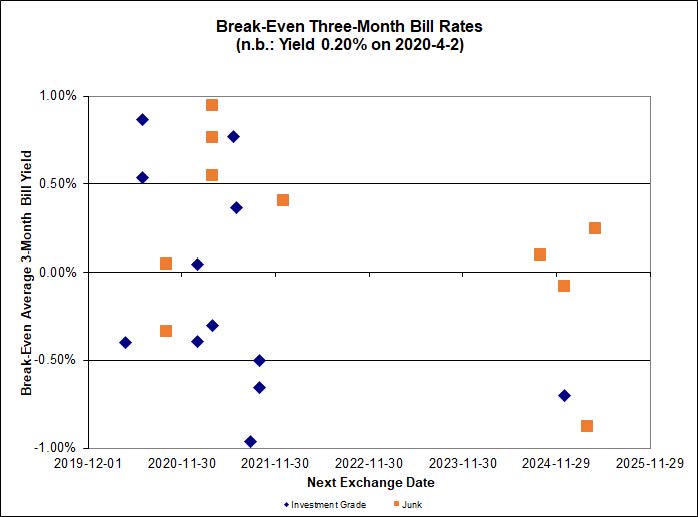

We can show the break-even rates for each FixedReset / FloatingReset Strong Pair graphically by plotting the implied average 3-month bill rate against the next Exchange Date (which is the date to which the average will be calculated). Inspection of the graph and the overall average break-even rates for extant pairs will provide a guide for estimating the break-even rate for the pair now under consideration assuming, of course, that enough conversions occur so that the pair is in fact created.

Ludicrous quotes supplied at great expense by the Toronto Stock Exchange are not up task of providing a particularly view of market pricing although an overall tendency is clear. I have not checked whether the lamentable state of the quote is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

Click for Big

Click for BigThe market shows wide dispersion in its quoted enthusiasm for floating rate product; the implied rates until the next interconversion are generally well below the current 3-month bill rate as the averages for investment-grade and junk issues are at -0.51% (ignoring the outlier FTS.PR.H / FTS.PR.I) and -0.11%, respectively. Whatever might be the result of the next few Bank of Canada overnight rate decisions, I suggest that it is unlikely that the average rate over the next five years will be lower than current – but if you disagree, of course, you may interpret the data any way you like.

The breakeven rate for the junk pairs has been relatively high recently; I confess I’m not quite sure what to make of it.

Since credit quality of each element of the pair is equal to the other element, it should not make any difference whether the pair examined is investment-grade or junk, although we might expect greater variation of implied rates between junk issues on grounds of lower liquidity, and this is just what we see.

If we plug in the current bid price of the BRF.PR.A FixedReset, we may construct the following table showing consistent prices for its soon-may-be-issued FloatingReset counterpart given a variety of Implied Breakeven yields consistent with issues currently trading:

| Estimate of FloatingReset BRF.PR.B (received in exchange for BRF.PR.A) Trading Price In Current Conditions |

| |

Assumed FloatingReset

Price if Implied Bill

is equal to |

| FixedReset |

Bid Price |

Spread |

0.50% |

0.00% |

-0.50% |

| BRF.PR.A |

10.75 |

262bp |

10.73 |

10.27 |

9.81 |

Before I get eviscerated in the comments, please note that I am well aware that BRF.PR.B is trading and is quoted with a bid of 10.50. Who cares? At the moment, the issues are interconvertible effective May 1 and are therefore exactly same thing (except for a minor difference in final dividend) from an investment perspective. We are interested in predicting what might happen after the potential for conversion has passed.

Based on current market conditions, I suggest that the FloatingResets, BRF.PR.B, that will result from conversion are likely to trade at a lower price than their FixedReset counterparts, BRF.PR.A. Therefore, it seems likely that I will recommend that holders of BRF.PR.A retain their shares, while holders of BRF.PR.B convert to BRF.PR.A, but I will wait until it’s closer to the April 15 notification deadline before making a final pronouncement. I will note that once the conversion period has passed it may be a good trade to swap one issue for the other in the market once both elements of each pair are trading and you can – hopefully – do it with a reasonably good take-out in price, rather than doing it through the company on a 1:1 basis. But that, of course, will depend on the prices at that time and your forecast for the path of policy rates over the next five years. There are no guarantees – my recommendation is based on the assumption that current market conditions with respect to the pairs will continue until the FloatingResets commence trading and that the relative pricing of the two new pairs will reflect these conditions.