Treasuries and swap spreads declined today:

The 10-year swap spread ended little changed after falling to negative 17.6 basis points Thursday, the lowest in Bloomberg data beginning in 1988. A basis point is 0.01 percentage point. The gap turned negative for the first time in three years in September. The spread reached record negative levels in other maturities as well, including the five- and seven-year.

Slumping Treasuries contributed to the narrowing of the spread. Yields on 10-year U.S. notes reached 2.26 percent Thursday, the highest since mid-September, as bets mounted that the Federal Reserve will raise interest rates as soon as next month. Investment-grade corporate issuance may tally about $30 billion this week, putting further pressure on Treasuries. On top of all that, regulations enacted after the financial crisis have curtailed the amount of risk banks can take, leading them to scale back trading and lending.

“This is more of a Treasury-led move as all the on-balance sheet products are becoming more costly to dealers,” said Priya Misra, head of global interest-rate strategy in New York at TD Securities, one of the 22 primary dealers that trade with the Fed. “Treasuries are an on-balance sheet product so they are getting more costly relative to swaps.”

Click for Big

Click for BigFor those unfamiliar with swap spreads:

In finance, swap spread is a popular way to indicate the credit spreads in a market. It is defined as the spread paid by the fixed-rate payer of an interest rate swap over the rate of the on the run treasury with the same maturity as the swap. For example, if the fixed-rate of a 5-year fixed-for-float LIBOR swap is 7.26% and the 5-year Treasury is yielding at 6.43%, the swap spread is 7.26% – 6.43% = 83 bps.

The endlessly entertaining Sprott / Silver Bullion battle is entering yet another new chapter (emphasis from original):

Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (C$) (TSX:SBT.U) (US$) confirmed today that the unsolicited offer by Sprott Asset Management LP and Sprott Physical Silver Trust (“Sprott PSLV”; and collectively, “Sprott”) for all of the outstanding Units of SBT has once again failed to achieve sufficient acceptance to satisfy the required minimum tender condition. As of October 30, 2015, only 39.64% of SBT Units were tendered, falling far short of the 66 2/3% minimum tender condition. As a result, Sprott has yet again, for the 6th time, extended the expiry date of the offer, which is now set to expire on November 20, 2015.

…

- •The Trustees will continue to act in the best interests of ALL Unitholders and cannot endorse a deficient offer that does not benefit ALL Unitholders. Principally because we don’t agree with them, Sprott has waged a smear campaign claiming poor governance and entrenchment of the Trustees. Their numerous unfounded allegations are intended to distract Unitholders from the deficiencies of their inadequate offer: no material premium, higher management fees, lower bullion security and safeguards, significantly reduced governance rights and higher potential tax liability for certain U.S. Unitholders.

- •Sprott’s claims that SBT Units have “traded for most of their existence at double-digit discounts” [footnote] are completely false. In fact, SBT Units have, on average, traded in-line to net asset value (“NAV”) since SBT was established in 2009

…

Footnote reads: Rick Rule stated on October 1, 2015 during the Sprott webcast relating to the Sprott offer: “It must be stressed that neither [GoldTrust] nor [Silver Bullion Trust] have ever or very seldom traded close to or above par, they have in fact traded at a persistent discount and they’ve traded at a persistent discount for over a decade.”

There was an interesting paper today from the Boston Fed by Joe Peek & Eric Rosengren, titled Credit Supply Disruptions: From Credit Crunches to Financial Crisis:

It is useful to reflect on how the financial environment changed in the interim between the bank credit crunch episode in the early 1990s and the recent financial crisis. What did we learn from the earlier crisis and how did the credit crunch literature help guide policy in the more recent crisis? Among the important changes were the consolidation of the banking sector and the dramatic growth in nonbank financial intermediaries, which are much more susceptible than banks to liquidity risks due to a lack of deposit insurance. This paper highlights the fact that while broker-dealers, money market mutual funds, and issuers of asset-backed securities were not particularly important in the early 1990s when the bank credit crunch occurred, they had grown dramatically over the subsequent two decades to become both a major source of financing and a key element in exacerbating the problems experienced during the recent financial crisis.

The key findings are:

- •The earlier literature on credit crunches contributed importantly to economists’ understanding of how financial shocks can impact the real economy. The real estate shock that caused capital-constrained banks to reduce credit availability to households and firms provided an important lesson learned from the 1990 recession and the academic work that followed. That literature provided a helpful guide as to how to respond to adverse credit shocks.

- •However, many of the financial innovations that occurred after the 1990 recession moved much of the issuance of credit to non-depository financial intermediaries. These intermediaries included money market mutual funds, broker-dealers, and issuers of asset-backed securities.

- •While the main problem facing banks was how to satisfy capital constraints when experiencing large declines in capital, these nonbank intermediaries were much more susceptible than banks to liquidity shocks, runs on liabilities, and fire sales of assets. Although the earlier literature provided important context, the nature of the problems was quite different for non-depository entities. Because these potential problems of nonbank intermediaries had not arisen in the earlier credit crunch, they were largely ignored in the subsequent credit crunch literature.

It seems to me that the moral of the story so far is that during boom times, money is going to flow from willing lenders to willing borrowers, come what may. If it can’t do it through regulated channels, it will do so via unregulated channels. So the authorities, in their wisdom, are attempting to micro-manage the economy, through, for instance, changes in the qualifying rules for mortgages in Canada (which has led directly to mortgage fraud, as discussed on October 30) and changes in tax-deductability of mortgage interest in the UK, as discussed on October 19 and October 1. Which, no doubt, creates a lot of very nicely paid work for the bureaucrats and lets everybody know that Your Government Is Doing Something, but when it comes to human nature vs. political platitudes, you know how I’m placing my bets. If it’s not houses, it will be something else. Bre-X, Nortel, internet stocks … there will be a special prize for those who can guess what the Next Big Thing is going to be!

But fear not! The SEC is working diligently to ensure that people who make instant investment decisions based on randomly selected Twitter posts will be protected:

According to the SEC’s complaint filed in federal court in the Northern District of California, James Alan Craig of Dunragit, Scotland, tweeted multiple false statements about the two companies on Twitter accounts that he deceptively created to look like the real Twitter accounts of well-known securities research firms.

The U.S. Attorney’s Office for the Northern District of California today filed criminal charges against Craig.

The SEC’s complaint alleges that Craig’s first false tweets caused one company’s share price to fall 28 percent before Nasdaq temporarily halted trading. The next day, Craig’s false tweets about a different company caused a 16 percent decline in that company’s share price. On each occasion, Craig bought and sold shares of the target companies in a largely unsuccessful effort to profit from the sharp price swings.

…

The SEC’s complaint charges that Craig committed securities fraud in violation of Section 10(b) of the Securities Exchange Act of 1934 and Rule 10b-5. The complaint seeks a permanent injunction against future violations, disgorgement, and a monetary penalty from Craig.

The SEC has issued an Investor Alert titled Social Media and Investing – Stock Rumors prepared by the Office of Investor Education and Advocacy. The alert aims to warn investors about fraudsters who may attempt to manipulate share prices by using social media to spread false or misleading information about stocks, and provides tips for checking for red flags of investment fraud.

Some may be interested in another Boston Fed paper by Daniel Cooper & Maria José Luengo-Prado titled Household Formation Over Time: Evidence from Two Cohorts of Young Adults:

Residential investment accounts for an important component of U.S. gross domestic product, and traditionally plays a strong role in business cycle expansions. U.S. residential investment has improved slowly during the recovery from the Great Recession, despite a relatively strong national rebound in house prices and record low interest rates. An important determinant of residential investment is the household formation rate, which is largely driven by young adults moving out of their parents’ homes after completing high school or college. New household formation can be offset when existing households combine, typically through marriage or by moving in with parents or other relatives for economic reasons. This paper uses National Longitudinal Survey of Youth (NLSY) data from the 1979 and the 1997 cohorts to examine how various demographic, economic, and geographic factors influence the rate of household formation among young adults, both within cohorts and over time across cohorts.

… with the key findings:

- •Comparing parental co-residence rates for young adults between the ages of 23 and 31 years shows that the share of individuals living with parents declines with age, but that the share of those living with parents is higher at nearly every age for the 1997 cohort compared to the 1979 cohort.

- •There is important variation in household formation by race both within a given cohort and over time. The share of black youth living with parents is substantially lower at young ages in both cohorts, but after the late teenage years, blacks and Hispanics are more likely to be living with parents than non-black/non-Hispanic youths. In the 1997 cohort, non-black/non-Hispanic and Hispanic youths, regardless of age, are more likely to be living with parents relative to their 1979 counterparts, while the rate of living with parents for blacks is unchanged.

- •Overall, housing costs have a meaningful effect on the decision of young adults to live with parents. The share of the 1979 cohort living with parents rose with the cost of housing. Among the 1997 cohort, 23 year-olds living in regions with high housing costs were about 15 percent more likely to be residing with parents than same-age members of the 1979 cohort who were living in areas with low housing costs.

But Holy Smokarisms! Today FixedResets were …

Click for Big

Click for Big… ON WHEELS!

It was a very strong, very uneven day for the Canadian preferred share market, with PerpetualDiscounts flat, FixedResets up 164bp and DeemedRetractibles gaining 25bp. The only losers on the ridiculously long Performance Highlights tables are BAM PerpetualDiscounts, which got whacked. Volume was very heavy.

Basically, FixedResets were strong all day:

Click for Big

Click for BigI don’t think we can ascribe the move to ETF action – only one block of ZPR changed hands today, Scotia buying 16,000 from Nesbitt at 10.79. CPD was similarly boring, with CIBC buying 10,000 from RBC at 13.20 and TD crossing 13,600 at 13.36.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

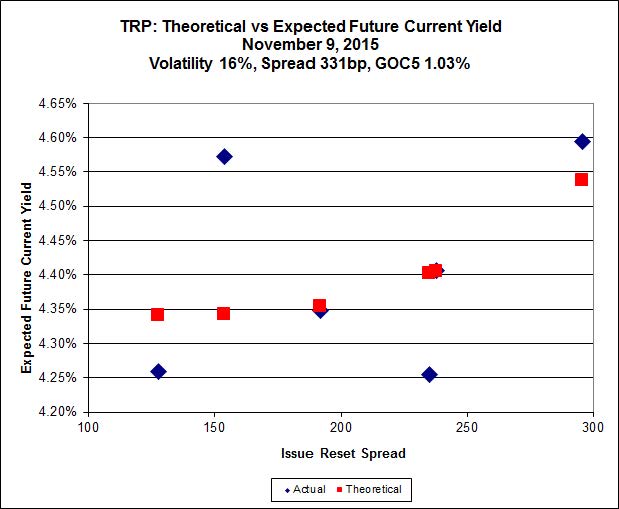

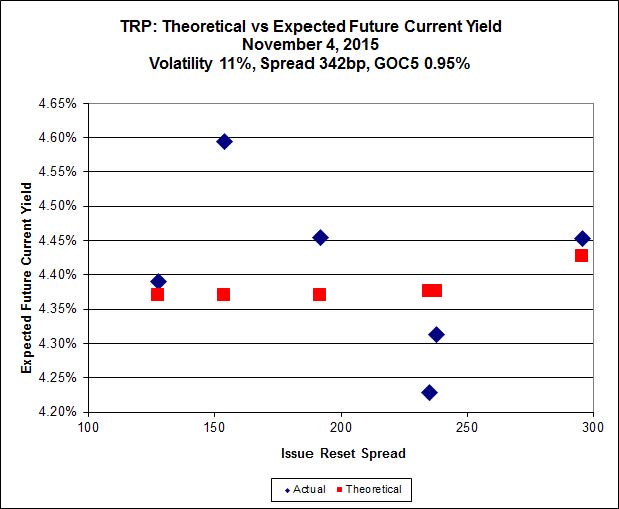

Here’s TRP:

Click for Big

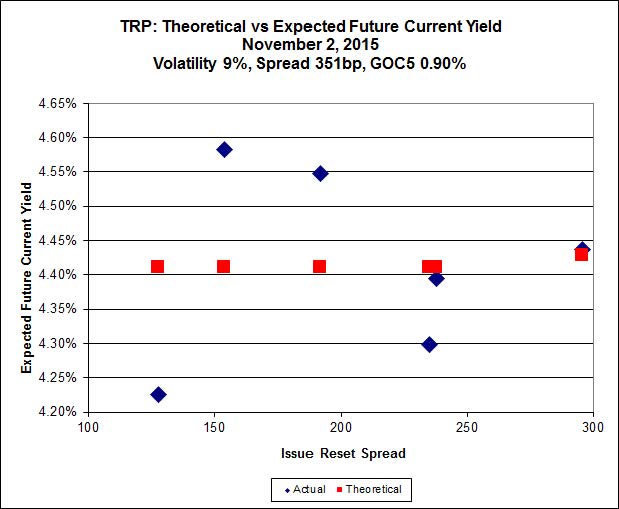

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.75 to be $0.61 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.60 cheap at its bid price of 13.90.

Click for Big

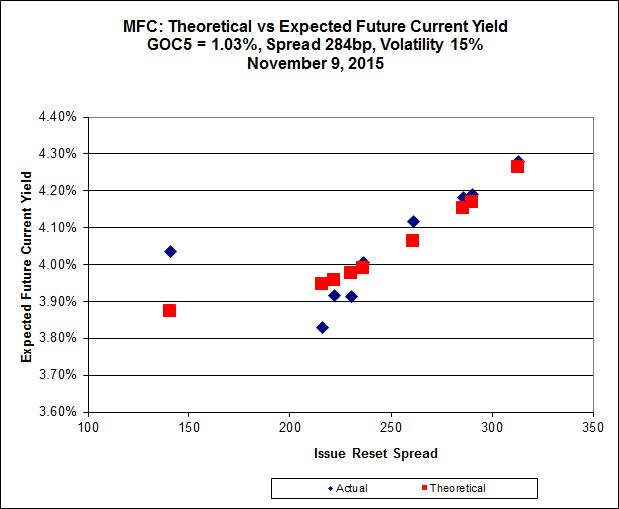

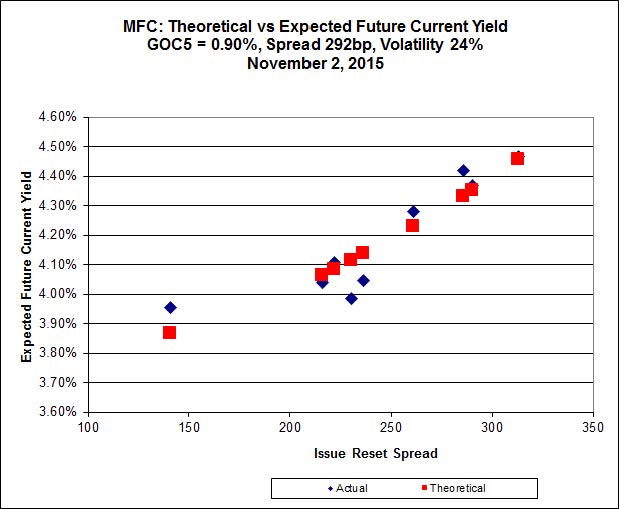

Click for BigMost expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 20.81 to be 0.61 rich, while MFC.PR.I resetting at +286bp on 2017-9-19, is bid at 21.92 to be 0.58 cheap.

Click for Big

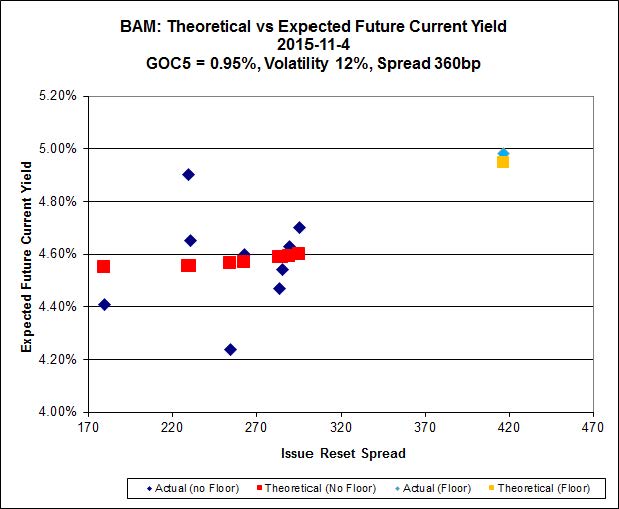

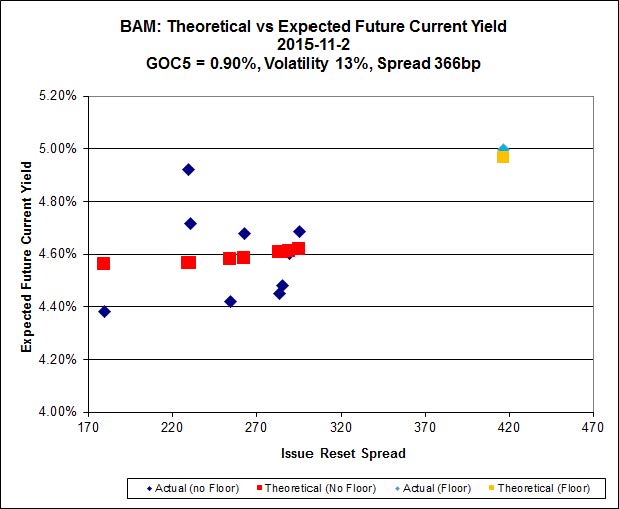

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 17.00 to be $1.13 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 20.69 and appears to be $1.22 rich.

Click for Big

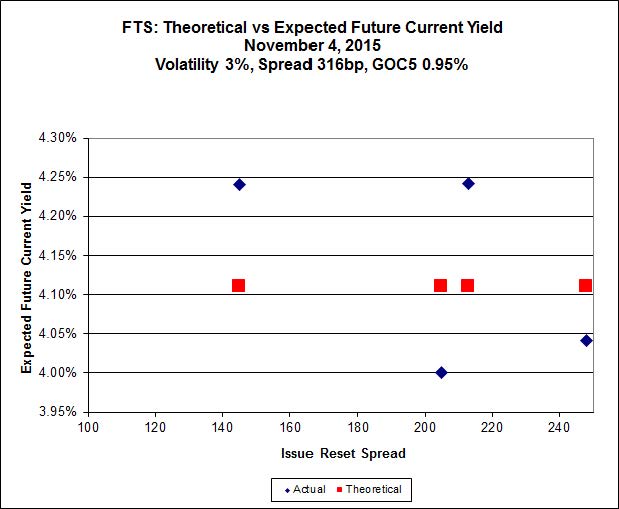

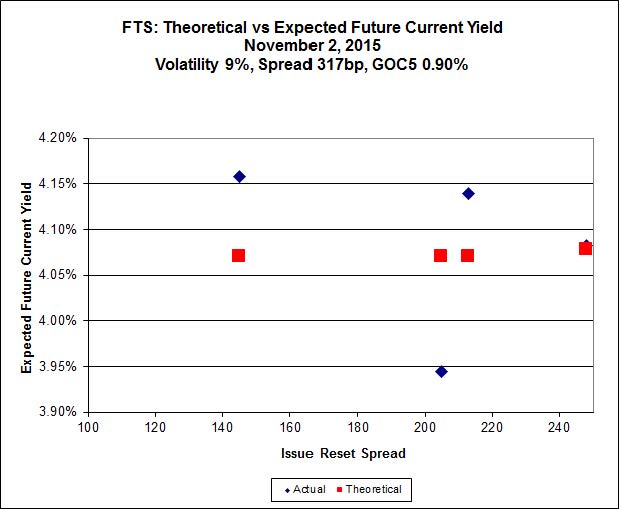

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 19.55, looks $0.89 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 18.69 and is $0.47 cheap.

Click for Big

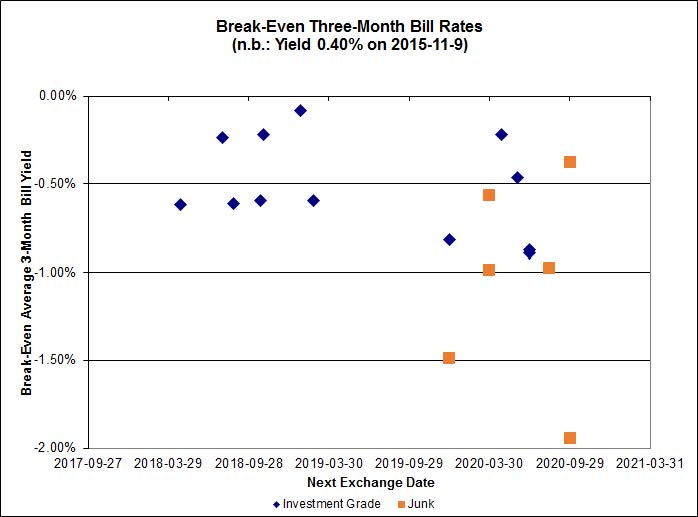

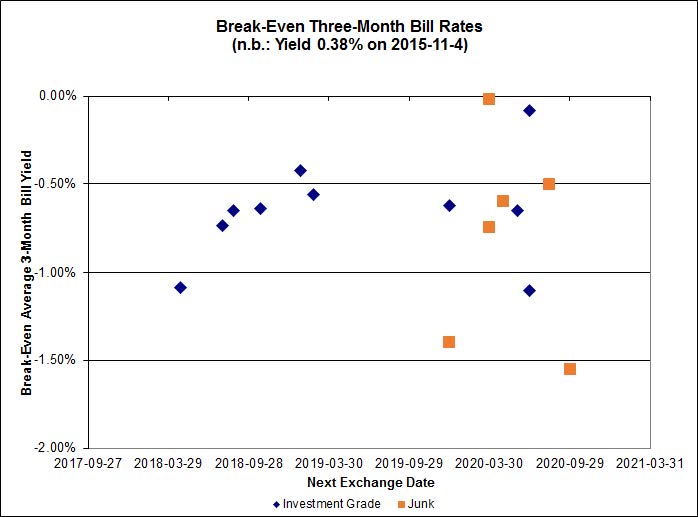

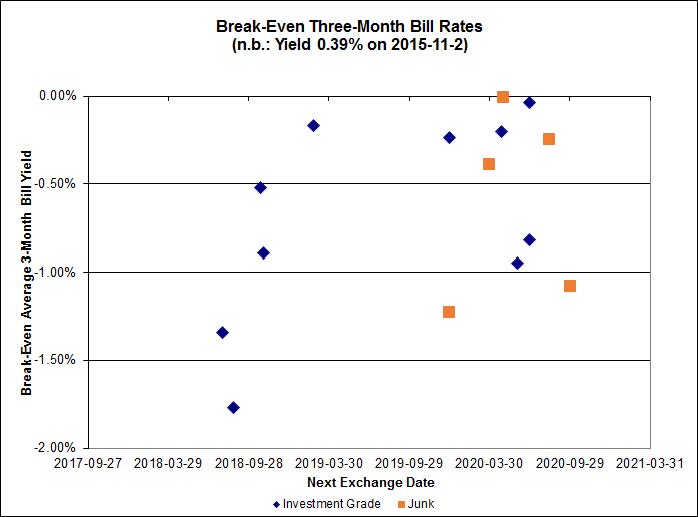

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.53%, with no outliers. There are four junk outliers above 0.00% and two below -2.00%.

Click for Big

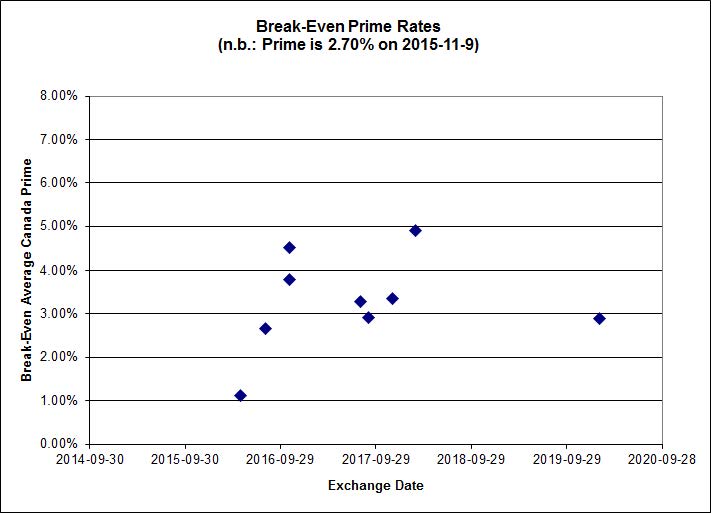

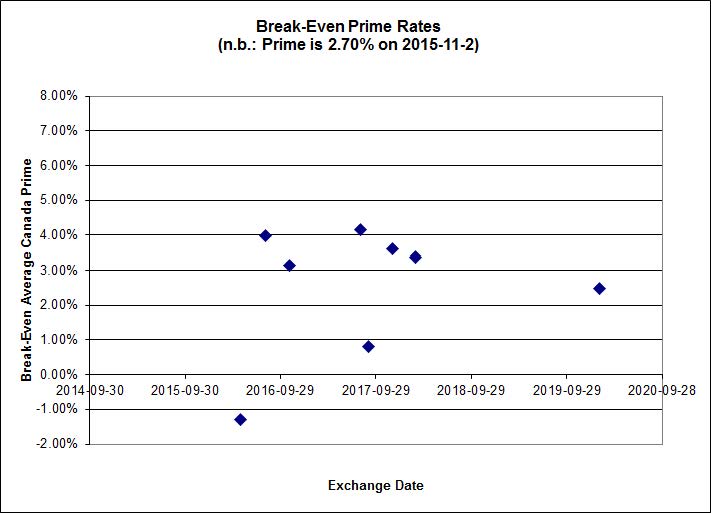

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

4.27 % |

5.12 % |

30,113 |

17.69 |

1 |

2.8939 % |

1,819.2 |

| FixedFloater |

6.11 % |

5.35 % |

31,607 |

17.12 |

1 |

0.0643 % |

3,196.4 |

| Floater |

4.10 % |

4.15 % |

63,890 |

17.09 |

3 |

1.6451 % |

1,927.5 |

| OpRet |

4.84 % |

4.36 % |

33,436 |

0.79 |

1 |

-0.1183 % |

2,719.7 |

| SplitShare |

4.76 % |

5.69 % |

155,319 |

4.39 |

5 |

0.0963 % |

3,194.0 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0963 % |

2,492.1 |

| Perpetual-Premium |

5.81 % |

2.01 % |

88,100 |

0.08 |

6 |

0.2253 % |

2,501.2 |

| Perpetual-Discount |

5.53 % |

5.63 % |

82,422 |

14.45 |

33 |

-0.0040 % |

2,586.7 |

| FixedReset |

4.85 % |

4.34 % |

214,334 |

15.70 |

76 |

1.6439 % |

2,108.2 |

| Deemed-Retractible |

5.17 % |

5.21 % |

111,540 |

5.43 |

34 |

0.2519 % |

2,585.0 |

| FloatingReset |

2.56 % |

3.75 % |

57,419 |

5.81 |

10 |

0.0562 % |

2,186.0 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| BAM.PR.N |

Perpetual-Discount |

-2.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.51

Evaluated at bid price : 20.51

Bid-YTW : 5.87 % |

| BAM.PR.M |

Perpetual-Discount |

-1.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.65

Evaluated at bid price : 20.65

Bid-YTW : 5.83 % |

| BAM.PF.C |

Perpetual-Discount |

-1.88 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.90

Evaluated at bid price : 20.90

Bid-YTW : 5.88 % |

| BAM.PF.D |

Perpetual-Discount |

-1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.23

Evaluated at bid price : 21.23

Bid-YTW : 5.85 % |

| GWO.PR.I |

Deemed-Retractible |

1.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.56

Bid-YTW : 6.62 % |

| BAM.PF.H |

FixedReset |

1.05 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.97

Bid-YTW : 4.28 % |

| BIP.PR.A |

FixedReset |

1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.51

Evaluated at bid price : 21.80

Bid-YTW : 5.17 % |

| GWO.PR.N |

FixedReset |

1.08 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.10

Bid-YTW : 9.53 % |

| FTS.PR.J |

Perpetual-Discount |

1.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 22.01

Evaluated at bid price : 22.30

Bid-YTW : 5.41 % |

| SLF.PR.I |

FixedReset |

1.20 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.05

Bid-YTW : 6.08 % |

| BAM.PF.A |

FixedReset |

1.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.04

Evaluated at bid price : 21.04

Bid-YTW : 4.70 % |

| NA.PR.S |

FixedReset |

1.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.06

Evaluated at bid price : 20.06

Bid-YTW : 4.31 % |

| TRP.PR.E |

FixedReset |

1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.75

Evaluated at bid price : 19.75

Bid-YTW : 4.40 % |

| RY.PR.M |

FixedReset |

1.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.04

Evaluated at bid price : 21.04

Bid-YTW : 4.22 % |

| PWF.PR.S |

Perpetual-Discount |

1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.99

Evaluated at bid price : 22.30

Bid-YTW : 5.40 % |

| SLF.PR.G |

FixedReset |

1.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.47

Bid-YTW : 8.35 % |

| TRP.PR.D |

FixedReset |

1.55 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.60

Evaluated at bid price : 19.60

Bid-YTW : 4.38 % |

| BAM.PR.K |

Floater |

1.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 11.50

Evaluated at bid price : 11.50

Bid-YTW : 4.15 % |

| BAM.PR.C |

Floater |

1.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 11.50

Evaluated at bid price : 11.50

Bid-YTW : 4.15 % |

| NA.PR.W |

FixedReset |

1.60 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.66

Evaluated at bid price : 19.66

Bid-YTW : 4.23 % |

| IAG.PR.G |

FixedReset |

1.61 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.10

Bid-YTW : 5.56 % |

| MFC.PR.N |

FixedReset |

1.61 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.81

Bid-YTW : 6.00 % |

| BAM.PF.G |

FixedReset |

1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.55

Evaluated at bid price : 21.55

Bid-YTW : 4.61 % |

| BAM.PF.B |

FixedReset |

1.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.80

Evaluated at bid price : 19.80

Bid-YTW : 4.68 % |

| BAM.PR.B |

Floater |

1.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 11.60

Evaluated at bid price : 11.60

Bid-YTW : 4.11 % |

| TD.PF.C |

FixedReset |

1.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.61

Evaluated at bid price : 19.61

Bid-YTW : 4.21 % |

| CM.PR.O |

FixedReset |

1.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.95

Evaluated at bid price : 19.95

Bid-YTW : 4.23 % |

| SLF.PR.J |

FloatingReset |

1.80 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.55

Bid-YTW : 9.35 % |

| TRP.PR.B |

FixedReset |

1.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 12.93

Evaluated at bid price : 12.93

Bid-YTW : 4.25 % |

| MFC.PR.C |

Deemed-Retractible |

1.82 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.30

Bid-YTW : 6.81 % |

| SLF.PR.H |

FixedReset |

1.92 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.09

Bid-YTW : 7.43 % |

| MFC.PR.G |

FixedReset |

1.92 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.29

Bid-YTW : 5.49 % |

| HSE.PR.A |

FixedReset |

1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 14.21

Evaluated at bid price : 14.21

Bid-YTW : 4.79 % |

| RY.PR.Z |

FixedReset |

1.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.98

Evaluated at bid price : 19.98

Bid-YTW : 4.10 % |

| TD.PF.A |

FixedReset |

2.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.91

Evaluated at bid price : 19.91

Bid-YTW : 4.16 % |

| RY.PR.J |

FixedReset |

2.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.34

Evaluated at bid price : 21.63

Bid-YTW : 4.18 % |

| MFC.PR.M |

FixedReset |

2.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.98

Bid-YTW : 5.96 % |

| CM.PR.P |

FixedReset |

2.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.41

Evaluated at bid price : 19.41

Bid-YTW : 4.25 % |

| HSE.PR.C |

FixedReset |

2.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.68

Evaluated at bid price : 22.00

Bid-YTW : 4.74 % |

| MFC.PR.L |

FixedReset |

2.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.99

Bid-YTW : 6.44 % |

| MFC.PR.F |

FixedReset |

2.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.06

Bid-YTW : 8.97 % |

| MFC.PR.I |

FixedReset |

2.38 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.92

Bid-YTW : 5.75 % |

| FTS.PR.H |

FixedReset |

2.47 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 14.50

Evaluated at bid price : 14.50

Bid-YTW : 4.18 % |

| PWF.PR.T |

FixedReset |

2.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.39

Evaluated at bid price : 21.72

Bid-YTW : 3.93 % |

| BMO.PR.Y |

FixedReset |

2.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.92

Evaluated at bid price : 22.40

Bid-YTW : 4.05 % |

| BAM.PR.R |

FixedReset |

2.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 17.00

Evaluated at bid price : 17.00

Bid-YTW : 4.87 % |

| TRP.PR.C |

FixedReset |

2.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 13.90

Evaluated at bid price : 13.90

Bid-YTW : 4.42 % |

| RY.PR.H |

FixedReset |

2.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.91

Evaluated at bid price : 19.91

Bid-YTW : 4.16 % |

| TD.PF.B |

FixedReset |

2.88 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.02

Evaluated at bid price : 20.02

Bid-YTW : 4.13 % |

| TD.PF.D |

FixedReset |

2.88 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.98

Evaluated at bid price : 22.48

Bid-YTW : 4.06 % |

| BAM.PR.E |

Ratchet |

2.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 25.00

Evaluated at bid price : 16.00

Bid-YTW : 5.12 % |

| BAM.PR.X |

FixedReset |

2.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 16.05

Evaluated at bid price : 16.05

Bid-YTW : 4.52 % |

| FTS.PR.G |

FixedReset |

2.98 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 18.69

Evaluated at bid price : 18.69

Bid-YTW : 4.30 % |

| MFC.PR.H |

FixedReset |

2.99 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.75

Bid-YTW : 4.90 % |

| VNR.PR.A |

FixedReset |

3.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.96

Evaluated at bid price : 20.96

Bid-YTW : 4.54 % |

| PWF.PR.P |

FixedReset |

3.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 14.50

Evaluated at bid price : 14.50

Bid-YTW : 4.34 % |

| BMO.PR.T |

FixedReset |

3.13 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.41

Evaluated at bid price : 19.41

Bid-YTW : 4.24 % |

| TRP.PR.A |

FixedReset |

3.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 16.65

Evaluated at bid price : 16.65

Bid-YTW : 4.44 % |

| TD.PF.E |

FixedReset |

3.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 22.22

Evaluated at bid price : 22.90

Bid-YTW : 4.07 % |

| IFC.PR.C |

FixedReset |

3.44 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.55

Bid-YTW : 6.95 % |

| BMO.PR.W |

FixedReset |

3.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.36

Evaluated at bid price : 19.36

Bid-YTW : 4.22 % |

| CM.PR.Q |

FixedReset |

3.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.98

Evaluated at bid price : 22.49

Bid-YTW : 4.06 % |

| MFC.PR.K |

FixedReset |

3.91 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.95

Bid-YTW : 6.39 % |

| FTS.PR.K |

FixedReset |

4.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.55

Evaluated at bid price : 19.55

Bid-YTW : 4.07 % |

| BMO.PR.S |

FixedReset |

4.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.20

Evaluated at bid price : 20.20

Bid-YTW : 4.18 % |

| IFC.PR.A |

FixedReset |

5.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.97

Bid-YTW : 8.24 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| NA.PR.S |

FixedReset |

151,227 |

STD crossed blocks of 50,000 shares, 35,000 and 34,600, all at 20.00.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 20.06

Evaluated at bid price : 20.06

Bid-YTW : 4.31 % |

| PVS.PR.E |

SplitShare |

73,928 |

Recent new issue.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-10-31

Maturity Price : 25.00

Evaluated at bid price : 24.36

Bid-YTW : 6.00 % |

| BAM.PR.R |

FixedReset |

61,370 |

National bought 33,000 from Desjardins at 16.90.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 17.00

Evaluated at bid price : 17.00

Bid-YTW : 4.87 % |

| RY.PR.Z |

FixedReset |

52,126 |

Scotia crossed 25,000 at 19.63.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.98

Evaluated at bid price : 19.98

Bid-YTW : 4.10 % |

| TD.PF.A |

FixedReset |

51,942 |

RBC crossed 35,900 at 19.73.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.91

Evaluated at bid price : 19.91

Bid-YTW : 4.16 % |

| BMO.PR.T |

FixedReset |

45,210 |

TD crossed 25,000 at 18.92.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.41

Evaluated at bid price : 19.41

Bid-YTW : 4.24 % |

| There were 57 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| MFC.PR.G |

FixedReset |

Quote: 22.29 – 23.20

Spot Rate : 0.9100

Average : 0.5805

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.29

Bid-YTW : 5.49 % |

| MFC.PR.I |

FixedReset |

Quote: 21.92 – 22.50

Spot Rate : 0.5800

Average : 0.3431

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.92

Bid-YTW : 5.75 % |

| MFC.PR.J |

FixedReset |

Quote: 21.01 – 21.64

Spot Rate : 0.6300

Average : 0.4271

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.01

Bid-YTW : 6.03 % |

| TD.PF.C |

FixedReset |

Quote: 19.61 – 20.10

Spot Rate : 0.4900

Average : 0.3113

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 19.61

Evaluated at bid price : 19.61

Bid-YTW : 4.21 % |

| BAM.PR.Z |

FixedReset |

Quote: 21.00 – 21.50

Spot Rate : 0.5000

Average : 0.3317

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 21.00

Evaluated at bid price : 21.00

Bid-YTW : 4.80 % |

| PWF.PR.P |

FixedReset |

Quote: 14.50 – 14.96

Spot Rate : 0.4600

Average : 0.2918

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-05

Maturity Price : 14.50

Evaluated at bid price : 14.50

Bid-YTW : 4.34 % |