A day like today needs a little light relief; it seems that the Big Banks’ darling Visa is shocked, shocked, that:

I’ll tell you guys one thing … once some fintech company comes up with a payment mechanism that is reasonably widespread and cheap, I’ll start taking it for PrefLetter. The day can’t come soon enough!

There’s been a lot of noise lately about housing prices in Vancouver and Toronto; foreign money has come in for a great deal of opprobrium; low mortgage rates and easy credit also take a lot of blame. I contend that another culprit is the lousy returns and extreme volatility experienced in the markets since the turn of the century – why invest in the stock market when you can buy a house? We won’t get rid of that attitude until we see a lot more underwater mortgages … which, unlike American mortgages, have recourse to the borrower.

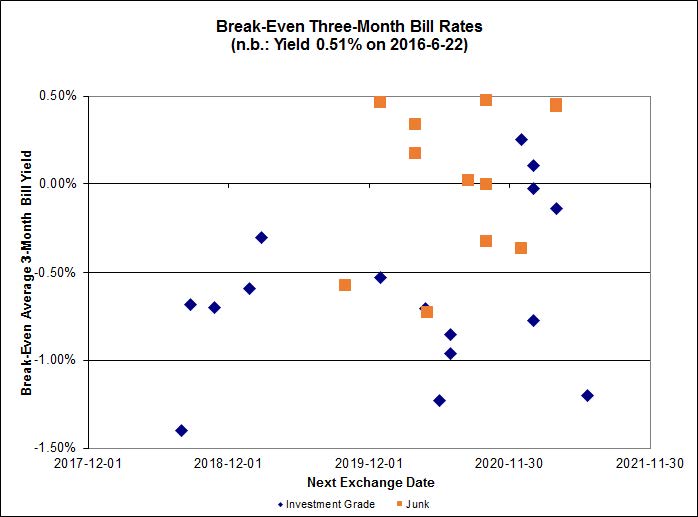

The GOC-5 closed at 0.57% and who knows? Maybe we’re back to the days when all changes in GOC-5 would be reflected in FixedReset prices (with a high negative duration!) as the market attempts to keep yields constant … which makes no sense, but since when is the preferred share market supposed to make sense?

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| PWF.PR.Q |

FloatingReset |

-8.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 11.50

Evaluated at bid price : 11.50

Bid-YTW : 4.69 % |

| IAG.PR.G |

FixedReset |

-5.76 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.50

Bid-YTW : 7.75 % |

| HSE.PR.C |

FixedReset |

-4.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.59

Evaluated at bid price : 17.59

Bid-YTW : 5.55 % |

| PWF.PR.T |

FixedReset |

-3.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 20.20

Evaluated at bid price : 20.20

Bid-YTW : 3.94 % |

| TD.PF.A |

FixedReset |

-3.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.96

Evaluated at bid price : 17.96

Bid-YTW : 4.28 % |

| IFC.PR.C |

FixedReset |

-3.70 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.66

Bid-YTW : 8.89 % |

| BMO.PR.T |

FixedReset |

-3.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.69

Evaluated at bid price : 17.69

Bid-YTW : 4.29 % |

| CM.PR.Q |

FixedReset |

-3.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 19.05

Evaluated at bid price : 19.05

Bid-YTW : 4.57 % |

| CM.PR.P |

FixedReset |

-3.60 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.65

Evaluated at bid price : 17.65

Bid-YTW : 4.34 % |

| BMO.PR.S |

FixedReset |

-3.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.03

Evaluated at bid price : 18.03

Bid-YTW : 4.32 % |

| CM.PR.O |

FixedReset |

-3.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.05

Evaluated at bid price : 18.05

Bid-YTW : 4.34 % |

| MFC.PR.M |

FixedReset |

-3.58 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.32

Bid-YTW : 7.72 % |

| SLF.PR.I |

FixedReset |

-3.58 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.80

Bid-YTW : 8.12 % |

| BMO.PR.W |

FixedReset |

-3.56 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.60

Evaluated at bid price : 17.60

Bid-YTW : 4.28 % |

| SLF.PR.G |

FixedReset |

-3.48 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.85

Bid-YTW : 10.00 % |

| TD.PF.B |

FixedReset |

-3.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.80

Evaluated at bid price : 17.80

Bid-YTW : 4.31 % |

| MFC.PR.L |

FixedReset |

-3.41 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.58

Bid-YTW : 8.09 % |

| TD.PF.C |

FixedReset |

-3.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.68

Evaluated at bid price : 17.68

Bid-YTW : 4.34 % |

| NA.PR.W |

FixedReset |

-3.35 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.00

Evaluated at bid price : 17.00

Bid-YTW : 4.53 % |

| HSE.PR.A |

FixedReset |

-3.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 11.44

Evaluated at bid price : 11.44

Bid-YTW : 5.14 % |

| TD.PF.D |

FixedReset |

-3.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 19.30

Evaluated at bid price : 19.30

Bid-YTW : 4.51 % |

| BAM.PR.R |

FixedReset |

-3.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 14.06

Evaluated at bid price : 14.06

Bid-YTW : 5.17 % |

| BAM.PR.T |

FixedReset |

-3.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 14.38

Evaluated at bid price : 14.38

Bid-YTW : 5.20 % |

| TD.PF.E |

FixedReset |

-3.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 20.02

Evaluated at bid price : 20.02

Bid-YTW : 4.45 % |

| FTS.PR.H |

FixedReset |

-3.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 13.40

Evaluated at bid price : 13.40

Bid-YTW : 4.01 % |

| MFC.PR.N |

FixedReset |

-3.02 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.29

Bid-YTW : 7.68 % |

| HSE.PR.G |

FixedReset |

-2.99 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 19.50

Evaluated at bid price : 19.50

Bid-YTW : 5.44 % |

| MFC.PR.K |

FixedReset |

-2.92 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.96

Bid-YTW : 8.47 % |

| FTS.PR.M |

FixedReset |

-2.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.50

Evaluated at bid price : 18.50

Bid-YTW : 4.44 % |

| MFC.PR.J |

FixedReset |

-2.88 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.56

Bid-YTW : 7.53 % |

| BMO.PR.Y |

FixedReset |

-2.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 19.60

Evaluated at bid price : 19.60

Bid-YTW : 4.39 % |

| BNS.PR.Z |

FixedReset |

-2.83 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.60

Bid-YTW : 6.81 % |

| RY.PR.H |

FixedReset |

-2.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.91

Evaluated at bid price : 17.91

Bid-YTW : 4.26 % |

| BAM.PF.G |

FixedReset |

-2.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 19.13

Evaluated at bid price : 19.13

Bid-YTW : 4.80 % |

| BAM.PF.F |

FixedReset |

-2.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.86

Evaluated at bid price : 18.86

Bid-YTW : 4.84 % |

| TRP.PR.A |

FixedReset |

-2.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 14.41

Evaluated at bid price : 14.41

Bid-YTW : 4.63 % |

| MFC.PR.F |

FixedReset |

-2.56 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.96

Bid-YTW : 10.74 % |

| TRP.PR.F |

FloatingReset |

-2.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 13.50

Evaluated at bid price : 13.50

Bid-YTW : 4.54 % |

| BNS.PR.Y |

FixedReset |

-2.49 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.60

Bid-YTW : 6.45 % |

| SLF.PR.J |

FloatingReset |

-2.47 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.25

Bid-YTW : 11.37 % |

| RY.PR.Z |

FixedReset |

-2.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.86

Evaluated at bid price : 17.86

Bid-YTW : 4.21 % |

| MFC.PR.G |

FixedReset |

-2.42 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.57

Bid-YTW : 7.70 % |

| MFC.PR.I |

FixedReset |

-2.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.52

Bid-YTW : 7.06 % |

| BAM.PF.B |

FixedReset |

-2.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 16.93

Evaluated at bid price : 16.93

Bid-YTW : 5.02 % |

| TRP.PR.D |

FixedReset |

-2.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.11

Evaluated at bid price : 17.11

Bid-YTW : 4.64 % |

| BAM.PF.E |

FixedReset |

-2.21 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.69

Evaluated at bid price : 17.69

Bid-YTW : 4.84 % |

| BAM.PF.A |

FixedReset |

-2.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.27

Evaluated at bid price : 18.27

Bid-YTW : 4.97 % |

| RY.PR.I |

FixedReset |

-2.18 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.84

Bid-YTW : 4.85 % |

| TRP.PR.H |

FloatingReset |

-2.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 9.88

Evaluated at bid price : 9.88

Bid-YTW : 4.58 % |

| GWO.PR.N |

FixedReset |

-2.14 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.70

Bid-YTW : 10.04 % |

| RY.PR.J |

FixedReset |

-2.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.65

Evaluated at bid price : 18.65

Bid-YTW : 4.58 % |

| NA.PR.S |

FixedReset |

-2.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.74

Evaluated at bid price : 17.74

Bid-YTW : 4.51 % |

| NA.PR.Q |

FixedReset |

-2.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.21

Bid-YTW : 4.78 % |

| IFC.PR.A |

FixedReset |

-2.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.12

Bid-YTW : 10.63 % |

| PWF.PR.P |

FixedReset |

-1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 12.51

Evaluated at bid price : 12.51

Bid-YTW : 4.50 % |

| BAM.PR.M |

Perpetual-Discount |

-1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 20.55

Evaluated at bid price : 20.55

Bid-YTW : 5.80 % |

| TRP.PR.C |

FixedReset |

-1.91 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 11.80

Evaluated at bid price : 11.80

Bid-YTW : 4.65 % |

| BAM.PR.N |

Perpetual-Discount |

-1.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 20.55

Evaluated at bid price : 20.55

Bid-YTW : 5.80 % |

| RY.PR.M |

FixedReset |

-1.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.51

Evaluated at bid price : 18.51

Bid-YTW : 4.50 % |

| TRP.PR.G |

FixedReset |

-1.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.68

Evaluated at bid price : 18.68

Bid-YTW : 4.87 % |

| HSE.PR.E |

FixedReset |

-1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 19.35

Evaluated at bid price : 19.35

Bid-YTW : 5.50 % |

| FTS.PR.K |

FixedReset |

-1.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 16.90

Evaluated at bid price : 16.90

Bid-YTW : 4.22 % |

| TRP.PR.I |

FloatingReset |

-1.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 11.70

Evaluated at bid price : 11.70

Bid-YTW : 4.47 % |

| SLF.PR.H |

FixedReset |

-1.66 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.40

Bid-YTW : 9.37 % |

| TD.PR.S |

FixedReset |

-1.65 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.72

Bid-YTW : 4.64 % |

| BAM.PF.D |

Perpetual-Discount |

-1.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 21.22

Evaluated at bid price : 21.22

Bid-YTW : 5.80 % |

| BAM.PF.C |

Perpetual-Discount |

-1.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 21.02

Evaluated at bid price : 21.02

Bid-YTW : 5.79 % |

| GWO.PR.O |

FloatingReset |

-1.54 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.80

Bid-YTW : 10.60 % |

| BNS.PR.R |

FixedReset |

-1.50 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.94

Bid-YTW : 4.90 % |

| FTS.PR.I |

FloatingReset |

-1.43 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 11.68

Evaluated at bid price : 11.68

Bid-YTW : 4.27 % |

| BMO.PR.M |

FixedReset |

-1.39 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.73

Bid-YTW : 4.61 % |

| CU.PR.I |

FixedReset |

-1.36 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-01

Maturity Price : 25.00

Evaluated at bid price : 25.45

Bid-YTW : 4.12 % |

| TRP.PR.B |

FixedReset |

-1.31 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 11.28

Evaluated at bid price : 11.28

Bid-YTW : 4.29 % |

| BAM.PR.K |

Floater |

-1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 10.03

Evaluated at bid price : 10.03

Bid-YTW : 4.71 % |

| BAM.PR.Z |

FixedReset |

-1.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 18.17

Evaluated at bid price : 18.17

Bid-YTW : 5.07 % |

| TRP.PR.E |

FixedReset |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 17.82

Evaluated at bid price : 17.82

Bid-YTW : 4.52 % |

| FTS.PR.G |

FixedReset |

-1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 16.50

Evaluated at bid price : 16.50

Bid-YTW : 4.36 % |

| BNS.PR.Q |

FixedReset |

-1.05 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.70

Bid-YTW : 4.83 % |

| TD.PR.T |

FloatingReset |

-1.02 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.39

Bid-YTW : 5.19 % |

| BIP.PR.B |

FixedReset |

1.00 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.20

Bid-YTW : 5.28 % |

| CU.PR.C |

FixedReset |

1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-06-16

Maturity Price : 16.74

Evaluated at bid price : 16.74

Bid-YTW : 4.57 % |

| BNS.PR.F |

FloatingReset |

2.78 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.51

Bid-YTW : 7.71 % |