My off-site server host experienced a power outage on the afternoon of August 4; their automatic fail-over to generator power failed; and my websites were down for about eight and a half hours as a result.

My apologies for the inconvenience.

My off-site server host experienced a power outage on the afternoon of August 4; their automatic fail-over to generator power failed; and my websites were down for about eight and a half hours as a result.

My apologies for the inconvenience.

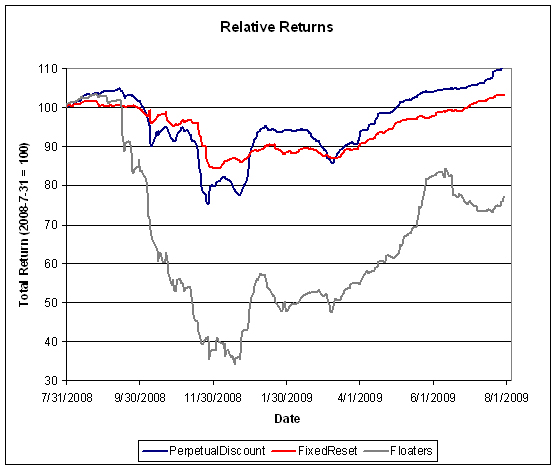

The fund performed well as the preferred share recovery now looks pretty solid. As noted in the report of Index Performance, July 2009, both the FixedReset and PerpetualDiscount posted strong gains, particularly in the latter half of the month following the TXPR Revision.

The fund’s performance was helped by its overweighting in PerpetualDiscount issues, as discussed in the post MAPF Portfolio Composition, but managed to outperform even the pure measure of PerpetualDiscount total return due to security selection and frequent trading. This has been accomplished while remaining fully invested in a portfolio with an overall composition that did not change much through the month – which is exactly what I seek to accomplish in managing the fund.

The fund’s Net Asset Value per Unit as of the close July 31 was $11.8181.

| Returns to July 31, 2009 | |||

| Period | MAPF | Index | CPD according to Claymore |

| One Month | +7.59% | +4.46% | +3.35% |

| Three Months | +21.95% | +11.49% | +8.96% |

| One Year | +56.59% | +6.50% | +5.24% |

| Two Years (annualized) | +20.61% | -0.79% | |

| Three Years (annualized) | +15.38% | -0.30% | |

| Four Years (annualized) | +12.58% | +0.54% | |

| Five Years (annualized) | +11.51% | ++1.43% | |

| Six Years (annualized) | +12.76% | +2.16% | |

| Seven Years (annualized) | +12.85% | +2.75% | |

| Eight Years (annualized) | +12.65% | +2.91% | |

| The Index is the BMO-CM “50” | |||

| MAPF returns assume reinvestment of dividends, and are shown after expenses but before fees. | |||

| CPD Returns are for the NAV and are after all fees and expenses. | |||

| Figures for Omega Preferred Equity (which are after all fees and expenses) for 1-, 3- and 12-months are +4.2%, +10.5% and +4.9%, respectively, according to Morningstar after all fees & expenses | |||

| Figures for Jov Leon Frazer Preferred Equity Fund (which are after all fees and expenses) for 1-, 3- and 12-months are N/A, N/A & N/A, respectively, according to Morningstar and the Globe and Mail | |||

| Figures for AIC Preferred Income Fund (which are after all fees and expenses) for 1-, 3- and 12-months are +2.5%, +4.1% & N/A, respectively | |||

MAPF returns assume reinvestment of dividends, and are shown after expenses but before fees. Past performance is not a guarantee of future performance. You can lose money investing in Malachite Aggressive Preferred Fund or any other fund. For more information, see the fund’s main page.

I am very pleased with the returns, but implore Assiduous Readers not to project this level of outperformance for the indefinite future. The past year in the preferred share market has been filled with episodes of panic and euphoria, together with many new entrants who do not appear to know what they are doing; perfect conditions for a disciplined quantitative approach.

All I can say about the fund’s relative returns in the past year is … sometimes everything works. The fund seeks to earn incremental return by selling liquidity (that is, taking the other side of trades that other market participants are strongly motivated to execute), which can also be referred to as ‘trading noise’. There have been a lot of strongly motivated market participants in the past year, generating a lot of noise! Things won’t always be this good … but for as long as it lasts the fund will attempt to make hay while the sun shines.

A good example of “selling liquidity” is the fund’s accumulation of a position in SLF.PR.B during the month.

| Trades Contributing to the Accumulation of SLF.PR.B July, 2009 |

||||

| Date | SLF.PR.C | SLF.PR.E | SLF.PR.B | |

| 6/30 Bid |

16.76 | 17.03 | 18.46 | |

| 7/20 | Sold 17.61 |

Bought 18.65 |

||

| 7/22 | Sold 18.06 |

Bought 18.98 |

||

| 7/23 | Sold 18.25 |

Sold 18.87 |

Bought 19.00 |

|

| 7/31 Closing Bid |

18.31 | 18.51 | 19.52 | |

| Dividends Ex-Date |

||||

| This is an attempt to show fairly the effect of numerous trades in tabular form. The trades shown are not necessarily precise dollar-for-dollar swaps. Trade details will be released on the main MAPF web page in the future. | ||||

It may also be noted that SLF.PR.B still has an elevated yield relative to the average level for the Sun Life PerpetualDiscount issues:

| SLF PerpetualDiscounts Comparison, 2009-7-31 At Closing Bid |

|

| Ticker | YTW |

| SLF.PR.A | 6.23% |

| SLF.PR.B | 6.24% |

| SLF.PR.C | 6.16% |

| SLF.PR.D | 6.15% |

| SLF.PR.E | 6.16% |

I believe that the trading opportunities amongst the SLF PerpetualDiscounts were triggered by a major seller of SLF.PR.A, which had an influence on the other issues that propogated at different rates while also influenced by a broad general demand for PerpetualDiscounts. In support of this hypothisis, I have uploaded three graphs (prepared by my firm’s analytical software, HIMIPref™):

This is mere explanation after the fact, however. At the time of trade, all that really mattered was that the fund could pick up yield by swapping between issues with identical credit quality and almost identical terms.

Another example of profitable trading was discussed as part of the post on portfolio composition.

There’s plenty of room for new money left in the fund. Just don’t expect the current level of outperformance every year, OK? While I will continue to exert utmost efforts to outperform, it should be borne in mind that beating the index by 500bp represents a good year, and there will almost inevitably be periods of underperformance in the future.

The yields available on high quality preferred shares remain elevated, which is reflected in the current estimate of sustainable income.

| Calculation of MAPF Sustainable Income Per Unit | |||||

| Month | NAVPU | Portfolio Average YTW |

Leverage Divisor |

Securities Average YTW |

Sustainable Income |

| June, 2007 | 9.3114 | 5.16% | 1.03 | 5.01% | 0.4665 |

| September | 9.1489 | 5.35% | 0.98 | 5.46% | 0.4995 |

| December, 2007 | 9.0070 | 5.53% | 0.942 | 5.87% | 0.5288 |

| March, 2008 | 8.8512 | 6.17% | 1.047 | 5.89% | 0.5216 |

| June | 8.3419 | 6.034% | 0.952 | 6.338% | $0.5287 |

| September | 8.1886 | 7.108% | 0.969 | 7.335% | $0.6006 |

| December, 2008 | 8.0464 | 9.24% | 1.008 | 9.166% | $0.7375 |

| March 2009 | $8.8317 | 8.60% | 0.995 | 8.802% | $0.7633 |

| June | 10.9846 | 7.05% | 0.999 | 7.057% | $0.7752 |

| July 2009 | 11.8181 | 6.44% | 0.993 | 6.485% | $0.7664 |

| NAVPU is shown after quarterly distributions. “Portfolio YTW” includes cash (or margin borrowing), with an assumed interest rate of 0.00% “Securities YTW” divides “Portfolio YTW” by the “Leverage Divisor” to show the average YTW on the securities held; this assumes that the cash is invested in (or raised from) all securities held, in proportion to their holdings. “Sustainable Income” is the resultant estimate of the fund’s dividend income per unit, before fees and expenses. |

|||||

As discussed in the post MAPF Portfolio Composition: July 2009, the fund has positions in splitShares (almost all BNA.PR.C) and an operating retractible, both of which have high yields that are not sustainable: at some point they will be called or mature and the funds will have to be reinvested. Therefore, both of these positions skew the calculation upwards.. Since the yield on these positions is higher than that of the perpetuals despite the fact that the term is limited, the sustainability of the calculated “sustainable yield” is suspect, as discussed in August, 2008.

Significant positions were also held in Fixed-Reset issues on July 31; all of which currently have their yields calculated with the presumption that they will be called by the issuers at par at the first possible opportunity. It is the increase in exposure to the lower-yielding Fixed-Reset class that accounts for the apparent stall in the increase of sustainable income per unit in the past seven months. In December 2008, FixedReset exposure was zero; it is now 11.3%. Exposure to the extraordinarily high-yielding SplitShare class has also been reduced since December due to credit concerns.

However, if the entire portfolio except for the PerpetualDiscounts were to be sold and reinvested in these issues, the yield of the portfolio would be the 6.14% shown in the July 31 Portfolio Composition analysis (which is in excess of the 6.06% index yield on July 31). Given such reinvestment, the sustainable yield would be 11.8181 * 0.0614 = $0.7256, an increase from the $0.7228 derived by a similar calculation last month.

Different assumptions lead to different results from the calculation, but the overall positive trend is apparent. I’m very pleased with the results! It will be noted that if there was no trading in the portfolio, one would expect the sustainable yield to be constant (before fees and expenses). The success of the fund’s trading is showing up in

As has been noted, the fund has maintained a credit quality equal to or better than the index; outperformance is due to constant exploitation of trading anomalies.

Again, there are no predictions for the future! The fund will continue to trade between issues in an attempt to exploit market gaps in liquidity, in an effort to outperform the index and keep the sustainable income per unit – however calculated! – growing.

Trading activity eased slightly in July, with portfolio turnover of about 100%, while the market extended its gains.

Trades were, as ever, triggered by a desire to exploit transient mispricing in the preferred share market (which may the thought of as “selling liquidity”), rather than any particular view being taken on market direction, sectoral performance or credit anticipation.

| MAPF Sectoral Analysis 2009-7-31 | |||

| HIMI Indices Sector | Weighting | YTW | ModDur |

| Ratchet | 0% | N/A | N/A |

| FixFloat | 0% | N/A | N/A |

| Floater | 0% | N/A | N/A |

| OpRet | 0% | N/A | N/A |

| SplitShare | 10.1% (-0.6) | 8.99%% | 7.01 |

| Interest Rearing | 0% | N/A | N/A |

| PerpetualPremium | 0.6% (+0.6) | 5.49% | 2.64 |

| PerpetualDiscount | 71.9 (-0.3) | 6.14% | 13.69 |

| Fixed-Reset | 11.3% (-0.2) | 4.18% | 4.22 |

| Scraps (OpRet) | 5.2% (-0.4) | 11.59% | 6.00 |

| Cash | +0.7% (+0.6) | 0.00% | 0.00 |

| Total | 100% | 6.44% | 11.37 |

| Totals and changes will not add precisely due to rounding. Bracketted figures represent change from June month-end. Cash is included in totals with duration and yield both equal to zero. | |||

The “total” reflects the un-leveraged total portfolio (i.e., cash is included in the portfolio calculations and is deemed to have a duration and yield of 0.00.). MAPF will often have relatively large cash balances, both credit and debit, to facilitate trading. Figures presented in the table have been rounded to the indicated precision.

Not much change in the sectoral distribution!

Credit distribution is:

| MAPF Credit Analysis 2009-7-31 | |

| DBRS Rating | Weighting |

| Pfd-1 | 0.3% (-0.1) |

| Pfd-1(low) | 81.5% (+14.3) |

| Pfd-2(high) | 2.0% (-11.8) |

| Pfd-2 | 0.3% (+0.3) |

| Pfd-2(low) | 9.8% (-3.4) |

| Pfd-3(high) | 5.2% (-0.4) |

| Cash | +0.7% (+0.6) |

| Totals will not add precisely due to rounding. Bracketted figures represent change from June month-end. | |

The shift from Pfd-2(high) to Pfd-1(low) is attributable to sale of some POW issues (Pfd-2(high)) in the PerpetualDiscount sector to fund the purchase of GWO PerpetualDiscounts (Pfd-1(low)):

| Trades Contributing to the Shift from Pfd-2(high) to Pfd-1(low) July, 2009 |

||||

| Date | POW.PR.B | GWO.PR.H | GWO.PR.G | |

| 6/30 Bid |

20.10 | 18.70 | 20.61 | |

| 7/16 | Sold 20.43 |

Bought 18.75 |

||

| 7/17 | Sold 20.46 |

Bought 18.75 |

||

| 7/23 | Sold 20.96 |

Bought 20.50 |

||

| 7/24 | Sold 21.00 |

Bought 20.75 |

||

| 7/31 Closing Bid |

21.45 | 20.10 | 21.78 | |

| Dividends Ex-Date |

||||

| This is an attempt to show fairly the effect of numerous trades in tabular form. The trades shown are not necessarily precise dollar-for-dollar swaps. Trade details will be released on the main MAPF web page in the future. | ||||

The fund does not set any targets for overall credit quality; trades are executed one by one. Variances in overall credit will be constant as opportunistic trades are executed. The overall credit quality of the portfolio is now superior to the credit quality of CPD at August month-end (when adjusted for the downgrades of BCE and the banks).

Claymore provides the following ratings breakdown:

| Ratings Breakdown as of 12/31/08 |

|

| Pfd-1 | 61.15% |

| Pfd-2 | 23.26% |

| Pfd-3 | 15.60% |

Three events have occurred since the Dec. 31 calculation date of CPD’s credit quality:

Liquidity Distribution is:

| MAPF Liquidity Analysis 2009-7-31 | |

| Average Daily Trading | Weighting |

| <$50,000 | 0.3% (-3.0) |

| $50,000 – $100,000 | 11.2% (-10.0) |

| $100,000 – $200,000 | 5.8% (-20.1) |

| $200,000 – $300,000 | 49.6% (+34.5) |

| >$300,000 | 31.9% (-1.6%) |

| Cash | +0.7% (+0.6) |

| Totals will not add precisely due to rounding. Bracketted figures represent change from June month-end. | |

There is no real pattern to the increase in liquidity experienced this month. For instance, a positions in SLF.PR.C (ATV = 167,986) and SLF.PR.E (ATV = 185,774) were swapped into SLF.PR.B (ATV = 239,639). The trades from POW to GWO (partially noted above) also contributed to the increase, as did trades from BPO into YPG.

MAPF is, of course, Malachite Aggressive Preferred Fund, a “unit trust” managed by Hymas Investment Management Inc. Further information and links to performance, audited financials and subscription information are available the fund’s web page. A “unit trust” is like a regular mutual fund, but is sold by offering memorandum rather than prospectus. This is cheaper, but means subscription is restricted to “accredited investors” (as defined by the Ontario Securities Commission) and those who subscribe for $150,000+. Fund past performances are not a guarantee of future performance. You can lose money investing in MAPF or any other fund.

A similar portfolio composition analysis has been performed on The Claymore Preferred Share ETF (symbol CPD) as of August 29. When comparing CPD and MAPF:

Performance of the HIMIPref™ Indices for July, 2009, was:

| Total Return | ||

| Index | Performance July 2009 |

Three Months to July 30, 2009 |

| Ratchet | +2.74% * | +25.62% * |

| FixFloat | +1.14% | +37.20% ** |

| Floater | +2.74% | +25.62% |

| OpRet | +1.91% | +5.28% |

| SplitShare | +4.48% | +12.48% |

| Interest | +1.91%**** | +3.98%**** |

| PerpetualPremium | +5.74%*** | +12.05%*** |

| PerpetualDiscount | +5.74% | +12.05% |

| FixedReset | +3.03% | +7.98% |

| * The last member of the RatchetRate index was transferred to Scraps at the February, 2009, rebalancing; subsequent performance figures are set equal to the Floater index | ||

| ** The last member of the FixedFloater index was transferred to Scraps at the February, 2009, rebalancing. Performance figures to 2009-5-29 are set equal to the Floater index. The FixedFloater index acquired a member on 2009-5-29. | ||

| *** The last member of the PerpetualPremium index was transferred to PerpetualDiscount at the October, 2008, rebalancing; subsequent performance figures are set equal to the PerpetualDiscount index. The PerpetualPremium index acquired four new members at the July, 2009, rebalancing. | ||

| **** The last member of the InterestBearing index was transferred to Scraps at the June, 2009, rebalancing; subsequent performance figures are set equal to the OperatingRetractible index | ||

| Passive Funds (see below for calculations) | ||

| CPD | +3.35% | +8.96% |

| DPS.UN | +4.45% | +13.62% |

| Index | ||

| BMO-CM 50 | +4.46% | +11.45% |

I believe the rather startling underperformance of CPD relative to DPS.UN is due to the former overweighting and the latter underweighting FixedReset issues which, while having (unsustainably!) strong results over the past three months, have underperformed PerpetualDiscounts. A measure of payback from the results for the period ending November, 2008 in which the relative performance of these two preferred share classes was … somewhat different!

Index performance over the trailing year is starting to look a little more normal – quite a feat when you consider that it includes the wild October-January period! Normal, that is, except for FloatingRate issues:

Claymore has published NAV and distribution data (problems with the page in IE8 can be kludged by using compatibility view) for its exchange traded fund (CPD) and I have derived the following table:

| CPD Return, 1- & 3-month, to July, 2009 | ||||

| Date | NAV | Distribution | Return for Sub-Period | Monthly Return |

| April 30 | 15.27 | |||

| May 29, 2009 | 15.88 | 0.00 | +3.99% | |

| June 25 | 15.88 | 0.2100 | +1.32% | +1.38% |

| June 30, 2009 | 15.89 | +0.06% | ||

| July 31, 2009 | 16.42 | +3.35% | ||

| Quarterly Return | +8.96% | |||

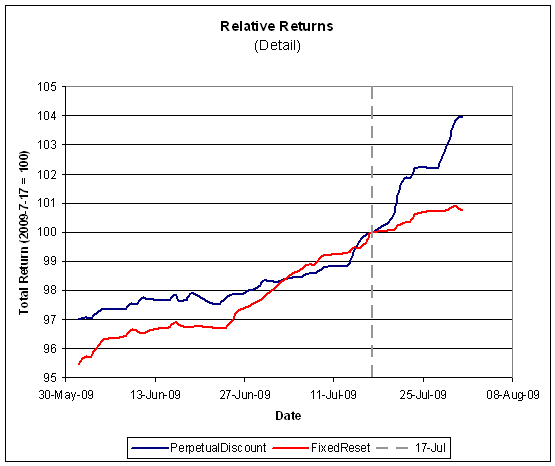

CPD was hurt by its July rebalancing, a phenomenon that I have remarked on previously. Assiduous Readers will recall that the July Rebalancing added (net) ten Fixed Resets vs a deletion of (net) six PerpetualDiscounts effective “at the open July 20”. Taking this as equivalent to the close on Friday July 17, let’s take a quick peek at how that particular decision has worked out.

Claymore currently holds $224,222,293 in CPD assets, a stunning increase from the $84,005,161 reported in the Dec 31/08 Annual Report. It may well be that CPD’s migration towards liquidity at all cost (as defined by the TXPR index) has an entirely valid rationale … but it sure ain’t doing returns much good! I will note that July’s index churn is nothing new considering that the portfolio has been churned on every semi-annual rebalancing since inception; so one cannot draw a straight line between the near-tripling of assets and the July rebalancing.

The DPS.UN NAV for July 29 has been published so we may calculate the approximate July returns – which is kind of a nightmare this month because it includes the June distribution. First, it is necessary to look at CPD for the period June 24-26 …

| CPD Return, June 24-26 | ||||

| Date | NAV | Distribution | Return for Sub-Period | Monthly Return |

| June 24, 2009 | 16.04 | |||

| June 25 | 15.88 | 0.21 | +0.31% | |

| June 26, 2009 | 15.87 | -0.06% | ||

| June 24-26 Return | +0.25% | |||

This figure is required in order to estimate the NAV for DPS.UN on June 26.

| DPS.UN NAV Return, July-ish 2009 | |||

| Date | NAV | Distribution | Return for period |

| Estimated June Ending Stub** | -0.375% | ||

| June 24, 2009 | 18.56 | ||

| June 26, 2009 | 18.3064*** | 0.30 | +0.25%*** |

| July 29, 2009 | 19.03 | +3.95% | |

| Estimated July Ending Stub | +0.61% * | ||

| Estimated July Return | +4.45% | ||

| ** CPD had a NAV of $16.04 on June 24, paid $0.21 June 25 with a NAV of 15.88 and a NAV of $15.89 on June 30. The return for the period was therefore +0.375%. This figure is subtracted the DPS.UN period return to arrive at an estimate for the calendar month. | |||

| * CPD had a NAV of $16.32 on July 29 and a NAV of $16.42 on July 31. The return for the period was therefore +0.61%. This figure is added to the DPS.UN period return to arrive at an estimate for the calendar month. | |||

| *** The June 26 NAV following the distribution has been estimated by assuming that DPS.UN and CPD had the same return for the period June 24-26; see table above. | |||

| The July return for DPS.UN’s NAV is therefore the product of three period returns, -0.375%, +0.25%, +3.95% and +0.61% to arrive at an estimate for the calendar month of +4.45% | |||

Now, to see the DPS.UN quarterly NAV approximate return, we refer to the calculations for May and June

| DPS.UN NAV Returns, three-month-ish to end-July-ish, 2009 | |

| May-ish | +6.35% |

| June-ish | +2.28% |

| July-ish | +4.45% |

| Three-months-ish | +13.62% |

These are total returns, with dividends presumed to have been reinvested at the bid price on the ex-date. The list has been restricted to issues in the HIMIPref™ indices.

| July 2009 | ||||

| Issue | Index | DBRS Rating | Monthly Performance | Notes (“Now” means “July 31”) |

| BAM.PR.K | Floater | Pfd-2(low) | -3.23% | Was the third-worst performer in June. |

| PWF.PR.J | OpRet | Pfd-1(low) | -0.27% | Now with a pre-tax bid-YTW of 3.37% based on a bid of 25.76 and a softMaturity 2013-7-30 at 25.00. |

| CM.PR.A | OpRet | Pfd-1(low) | +0.19% | Now with a pre-tax bid-YTW of –13.74% based on a bid of 25.91 and a call 2009-8-30 at 25.50. Since dividend is $1.325 and CM saves $0.25 p.a. on the redemption price, it will probably survive until softMaturity 2011-7-30, when it will have realized a yield of 3.42% … but you’re taking your chances! |

| BAM.PR.H | OpRet | Pfd-2(low) | +0.28% | Now with a pre-tax bid-YTW of 5.17% based on a bid of 25.50 and a softMaturity 2012-3-30 at 25.00. |

| MFC.PR.A | OpRet | Pfd-1(low) | +0.71% | Now with a pre-tax bid-YTW of 3.82% based on a bid of 25.54 and a softMaturity 2015-12-18 at 25.00. |

| … | … | … | … | … |

| SLF.PR.C | Perpetual-Discount | Pfd-1(low) | +9.25% | Now with a pre-tax bid-YTW of 6.16% based on a bid of 18.31 and a limitMaturity. |

| SLF.PR.D | Perpetua-lDiscount | Pfd-1(low) | +9.62% | Now with a pre-tax bid-YTW of 6.15% based on a bid of 18.35 and a limitMaturity. |

| CIU.PR.A | Perpetual-Discount | Pfd-2(high) | +9.92% | Now with a pre-tax bid-YTW of 5.81% based on a bid of 20.17 and a limitMaturity. Was the fourth-worst performer in June. |

| BNA.PR.C | SplitShare | Pfd-2(low) | +10.65% | Now with a pre-tax bid-YTW of 9.15% based on a bid of 17.76 and a hardMaturity 2019-1-10 at 25.00. Was the best performer in June. |

| TRI.PR.B | Floater | Pfd-2(low) | +10.93% | Moved to Scraps at July rebalancing on volume concerns. Was the worst performer in June. |

| HIMI Index Changes, July 31, 2009 | |||

| Issue | From | To | Because |

| TRI.PR.B | FloatingRate | Scraps | Volume |

| CU.PR.A | PerpetualDiscount | PerpetualPremium | Price |

| BMO.PR.L | PerpetualDiscount | PerpetualPremium | Price |

| ENB.PR.A | PerpetualDiscount | PerpetualPremium | Price |

| CU.PR.B | PerpetualDiscount | PerpetualPremium | Price |

At long last, the PerpetualPremium index has members again! It disappeared at the October 2008 Rebalancing, when CL.PR.B fell below 25.00. That issue nearly made it back into premium territory this month, but the bid at the close was exactly 25.00 … and when that happens, the issue in question doesn’t move.

There were the following intra-month changes:

The FDIC will now be separating good assets from bad when disposing of failed banks:

“FDIC staff has referred to a ‘good bank/bad bank’ model described as the sale of the failing bank’s better assets wrapped with loss-share coverage to another bank and the sale of the ‘bad’ assets,” into a limited liability company, spokesman Andrew Gray said today in an e-mail statement, adding the agency now plans to proceed with such sales.

Potential bidders may be interested in higher risks in the failed lender’s bad loans, while the agency auctions the remaining assets in combination with an agreement to share any losses with the buyer, he said.

…

Gray said loss-sharing arrangements and structured transactions “are proven ways to maximize bidder interest and value.”

I missed this when it was fresh … CalPERS is suing the rating agencies:

The California Public Employees’ Retirement System said in a lawsuit filed last week in California Superior Court in San Francisco that it might lose more than $1 billion from structured investment vehicles, or SIVs, that received top grades from Moody’s Investors Service Inc, Standard & Poor’s and Fitch Inc.

…

By giving these securities their highest ratings, the agencies “made negligent misrepresentations” to the pension fund, Calpers said. Such ratings, which typically accompany investments with almost no risk of loss, “proved to be wildly inaccurate and unreasonably high.”

In other words, CalPERS CEO Anne Stausboll, who ” oversees 2,300 employees, a budget of more than $332 million” in the course of managing USD 176.1-billion in assets, is grossly incompetent and should be fired. Taking $1-billion exposure in SIV’s without even a cursory due-diligence? She – and presumably a host of others at CalPERS – should be in jeopardy of not just getting fired, but of losing their licenses.

The target firms have noted that they were not responsible for CalPERS investment decisions – if Stausboll wants to abnegate fiduciary responsibility, she must at the very least pay for it.

ZeroHedge has some commentary as well as a copy of the lawsuit.

And … that’s it for another month! Quite a good month for preferreds, with CPD up about 3.33%. My fund, Malachite Aggressive Preferred Fund, will have outperformed CPD by a significant margin … but Assiduous Readers will have to wait until I post the performance review sometime within the next week.

Volume continued high to close the month, with FixedResets again being mostly elbowed out of the Volume Highlights table by PerpetualDiscounts. PerpetualDiscounts had a gain of almost 15bp on the day to close with a yield of 6.06%, equivalent to 8.48% interest at the standard equivalency factor of 1.4x. Long Corporates now yield about 6.3%, so the pre-tax interest-equivalent spread ends the month at about 218bp; basically unchanged from the 215bp spread reported on July 29.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.1503 % | 1,219.3 |

| FixedFloater | 7.13 % | 5.31 % | 39,931 | 16.89 | 1 | 0.0000 % | 2,153.6 |

| Floater | 3.12 % | 3.76 % | 72,219 | 17.93 | 3 | 1.1503 % | 1,523.2 |

| OpRet | 4.90 % | -3.49 % | 139,778 | 0.10 | 15 | 0.0721 % | 2,250.7 |

| SplitShare | 5.84 % | 6.66 % | 97,697 | 4.13 | 3 | 0.4190 % | 1,982.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0721 % | 2,058.0 |

| Perpetual-Premium | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1457 % | 1,849.3 |

| Perpetual-Discount | 6.00 % | 6.06 % | 162,866 | 13.80 | 71 | 0.1457 % | 1,703.2 |

| FixedReset | 5.51 % | 4.10 % | 559,666 | 4.18 | 40 | -0.1376 % | 2,094.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.E | Perpetual-Discount | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 21.60 Evaluated at bid price : 21.86 Bid-YTW : 6.33 % |

| POW.PR.D | Perpetual-Discount | -1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 20.50 Evaluated at bid price : 20.50 Bid-YTW : 6.16 % |

| IAG.PR.C | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2014-01-30 Maturity Price : 25.00 Evaluated at bid price : 27.10 Bid-YTW : 4.29 % |

| RY.PR.C | Perpetual-Discount | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 19.76 Evaluated at bid price : 19.76 Bid-YTW : 5.84 % |

| POW.PR.B | Perpetual-Discount | -1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 21.45 Evaluated at bid price : 21.45 Bid-YTW : 6.30 % |

| PWF.PR.K | Perpetual-Discount | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 20.25 Evaluated at bid price : 20.25 Bid-YTW : 6.16 % |

| CM.PR.P | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 22.20 Evaluated at bid price : 22.67 Bid-YTW : 6.09 % |

| BMO.PR.K | Perpetual-Discount | 1.01 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 22.86 Evaluated at bid price : 23.01 Bid-YTW : 5.81 % |

| HSB.PR.D | Perpetual-Discount | 1.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 20.51 Evaluated at bid price : 20.51 Bid-YTW : 6.18 % |

| RY.PR.G | Perpetual-Discount | 1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 19.53 Evaluated at bid price : 19.53 Bid-YTW : 5.78 % |

| BAM.PR.N | Perpetual-Discount | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 16.41 Evaluated at bid price : 16.41 Bid-YTW : 7.35 % |

| BNS.PR.M | Perpetual-Discount | 1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 19.69 Evaluated at bid price : 19.69 Bid-YTW : 5.76 % |

| GWO.PR.I | Perpetual-Discount | 1.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 6.07 % |

| GWO.PR.G | Perpetual-Discount | 1.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 21.50 Evaluated at bid price : 21.78 Bid-YTW : 6.03 % |

| BAM.PR.I | OpRet | 1.63 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2013-12-30 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 5.14 % |

| GWO.PR.H | Perpetual-Discount | 1.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 20.10 Evaluated at bid price : 20.10 Bid-YTW : 6.11 % |

| NA.PR.N | FixedReset | 1.98 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2013-09-14 Maturity Price : 25.00 Evaluated at bid price : 26.75 Bid-YTW : 3.47 % |

| TRI.PR.B | Floater | 3.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 16.75 Evaluated at bid price : 16.75 Bid-YTW : 2.36 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.L | FixedReset | 59,795 | RBC crossed 50,000 at 26.50. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-03-26 Maturity Price : 25.00 Evaluated at bid price : 26.45 Bid-YTW : 4.16 % |

| POW.PR.C | Perpetual-Discount | 59,419 | RBC crossed 25,000 at 23.05, then another 20,000 at 23.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 22.82 Evaluated at bid price : 23.07 Bid-YTW : 6.34 % |

| SLF.PR.B | Perpetual-Discount | 58,606 | Nesbitt crossed 50,000 at 19.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 19.51 Evaluated at bid price : 19.51 Bid-YTW : 6.24 % |

| RY.PR.G | Perpetual-Discount | 46,299 | Nesbitt crossed 30,000 at 19.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 19.53 Evaluated at bid price : 19.53 Bid-YTW : 5.78 % |

| CM.PR.J | Perpetual-Discount | 34,224 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 18.77 Evaluated at bid price : 18.77 Bid-YTW : 6.04 % |

| RY.PR.B | Perpetual-Discount | 32,350 | Nesbitt crossed 20,000 at 20.21. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2039-07-31 Maturity Price : 20.23 Evaluated at bid price : 20.23 Bid-YTW : 5.82 % |

| There were 41 other index-included issues trading in excess of 10,000 shares. | |||

| Quadravest SplitShare Corporations |

|||

| Ticker | Income Coverage 1H09 |

Asset Coverage 2009-7-15 |

Last PrefBlog Mention |

| LFE.PR.A | 1.2+:1 | 1.5+:1 | Capital Unit Dividends Reinstated |

| Quadravest SplitShare Corporations |

|||

| Ticker | Income Coverage 1H09 |

Asset Coverage 2009-7-15 |

Last PrefBlog Mention |

| BK.PR.A | 1.5+:1 | 1.9+:1 | Ticker Change from PPL.PR.A |

| Quadravest SplitShare Corporations |

|||

| Ticker | Income Coverage 1H09 |

Asset Coverage 2009-7-15 |

Last PrefBlog Mention |

| DFN.PR.A | 1.4-:1 | 1.9-:1 | Downgraded Pfd-3 |

DF.PR.A | 1.2-:1 | 1.6+ | Downgraded Pdf-3(low) |