We have a new government, but the same old central planners:

Finance Minister Bill Morneau today announced changes to the rules for government-backed mortgage insurance to contain risks in the housing market, reduce taxpayer exposure and support long-term stability. Effective February 15, 2016, the minimum down payment for new insured mortgages will increase from 5 per cent to 10 per cent for the portion of the house price above $500,000. The 5 per cent minimum down payment for properties up to $500,000 remains unchanged.

Today’s announcement represents a graduated approach to increasing the down payment requirement proportionally to the cost of a home. Canadians who already hold mortgages will not be affected by this announcement.

The Government continuously monitors the housing market and is committed to implementing policy measures that maintain a healthy, competitive and stable housing market. Higher homeowner equity plays a key role in maintaining a stable and secure housing market.

The backgrounder reveals nothing relevant:

The Bank Act requires federally regulated lenders to obtain mortgage default insurance (“mortgage insurance”) for homebuyers who make a down payment of less than 20 per cent of the property purchase price. The homebuyer pays the premium for this insurance, which protects the lender against mortgage loan losses if the homebuyer defaults.

By reducing risk to lenders, mortgage insurance enables consumers to purchase homes with a down payment as low as 5 per cent of the property value and at lower mortgage interest rates that are comparable to those received by homebuyers with higher down payments.

…

The Government guarantee of mortgage insurance is intended to support access to homeownership for creditworthy buyers and promote stability in the housing market, financial system and economy. As part of its role to promote stability, and to protect taxpayers from potential mortgage loan losses, the Government sets the eligibility rules for new government-backed insured mortgages.Between 2008 and 2012, four rounds of changes were made to the eligibility rules, aimed at encouraging insured borrowers to build and retain housing equity and take on mortgage debt that they are able to service over the economic cycle.

And the FAQs are puerile:

Why is the Government making this change at this time?

The Government continuously monitors the housing market and is prepared to implement policy measures to maintain a healthy, competitive and stable housing market. The new measure reduces housing market risks by increasing borrower equity. This protects the stability of the housing market and the economy as a whole, as well as the interests of taxpayers who ultimately back government-guaranteed mortgage insurance.

What will be the impact of the higher down payment requirement on the Canadian economy?

Higher homeowner equity will help maintain a stable and secure housing market and balanced economic growth over the long-term. In the short term, this targeted measure will dampen somewhat the pace of housing activity over the next year, as some prospective homebuyers save for the increased minimum down payment.

There is no meat on these bones at all. There is nothing to quantify any improvement in government policy objectives that is served by this policy. It’s just another randomly chosen measure that will be touted as an indication to those who are unable to compete for housing that Your Government Is Doing Something.

But the cheerleaders were out in force:

Some new buyers in Toronto and Vancouver will be knocked out of the market temporarily.

But that’s a fair price for bringing some stability to a housing market where prices in many cities have for years risen far in excess of incomes.

…

Boomers in particular are living in homes that have increased many times in value. A big decline in house prices would be a shocking setback to these people and could negatively affect their financial health in retirement.Mild as it is, the new down payment rule could only momentarily slow hot markets. But at least the new Liberal government has shown that it’s monitoring housing and ready to act to keep it in line. For homeowners, that’s far better news than another month of big price gains.

As I have noted before, the fact that people are taking advantage of low interest rate to load up on non-productive housing assets instead of productive capital assets is a genuine concern for the western world. There was a story illustrating the process the other day:

It was after losing a huge chunk of money in the stock market, twice, that Ottawa couple Denise and Stuart MacPherson decided they needed to find a new way to save for retirement.

The first bath they took was during the dot-com bust at the start of the century, after getting caught up in the hype around technology stocks. The second was the global financial crisis in 2008, when they watched half of their investments go down the drain.

“That was a very hard lesson to learn, mostly because we didn’t really understand what we were investing in,” says Ms. MacPherson, 61. “It was a wake-up call for us.”

Instead of jumping back into the market, the couple, working then as civil servants, decided to start investing in something they could see and understand.

“That’s when we started looking at real estate,” Ms. MacPherson says.

I suggest that from a policy perspective, what we need is more housing price volatility, not less. Let’s wipe out a swath of real-estate entrepreneurs – as happened in the early eighties and again in the early nineties – pour encourager les autres. Trying to turn the housing market into a 5% GIC – as the repeated lauding of ‘stability’ implies – will have quite the opposite effect from that which is intended. The trouble is, of course, that the central planners and regulators want to turn everything into a 5% GIC, since they run into less criticism that way.

I was more impressed with OSFI’s note titled Updating capital requirements for residential mortgages:

OSFI is planning to update the regulatory capital requirements for loans secured by residential real estate properties (i.e. residential mortgages).

…

The purpose of OSFI’s regulatory capital framework is to ensure, as much as possible, that federally regulated financial institutions can absorb severe but plausible losses. The potential severity of loss scenarios in the residential mortgage market depends crucially on price developments. In particular, potential losses become more severe during extended periods where house prices have recently risen rapidly and/or are high relative to borrower incomes. As a result, the potential severity of losses may vary across Canada.Accordingly, for banks using internal models, OSFI will propose a risk-sensitive floor for one of the model inputs (losses in the event of default) that will be tied to increases in local property prices and/or to house prices that are high relative to borrower incomes. This will ensure a level of consistency and conservatism in the protection provided to depositors and unsecured creditors.

For federally regulated private mortgage insurers, we will introduce a new standardized approach that updates the capital requirements for mortgage guarantee insurance risk. It will require more capital when house prices are high relative to borrower incomes. This will ensure a level of conservatism in the protection provided to policyholders and unsecured creditors.

The part of this policy that looks back at past prices to determine risk is – in broad outlines – something I’ve been advocating for years, most recently on November 30:

There are two approaches that can be taken: the first is to insist that for risk-management purposes, the loan-to-value ratio of a mortgage be calculated not according to the sale price or to the appraised value, but to an estimate of what this would have been five or ten years ago, adjusted for inflation. So, for instance, if we have a house that sold in 2014 for $567,000 and has a mortgage of $400,000, we would now currently say the LTV is 71%. I suggest that for regulatory risk purposes we use the 2009 price of $395,000, add on 10% to reflect plain vanilla inflation for a notional value of $435,000, and say OK, you’ve got to put up capital reflecting this notional LTV of 92%, which is a different kettle of fish altogether.

The second approach would simply say … 40% of your balance sheet is now mortgages, the average over the last ten years is 30%, the difference is 10% and 10% of that is 1%, so there’s a countercyclical capital surcharge of 1% that will be applied to your risk weighted assets. A solution would need to be more detailed, with meaningful categorizations of bank assets and threshold values for surcharges so that slow change is not discouraged, but that’s the general idea.

Such broad-brush changes are strongly preferable to the micro-management of the economy implicit in down-payment rules.

Meanwhile Third Avenue Management rocked the junk market by liquidating its junk fund:

I am writing to inform you that the Board of Trustees of the Third Avenue Trust has adopted a Plan of Liquidation for the Third Avenue Focused Credit Fund (“FCF”). Pursuant to this Plan, on or about December 16, 2015, there will be a distribution to all FCF shareholders of the Fund’s cash assets not required for the expenses of the Fund and its liquidation. The remaining assets have been placed into a liquidating trust (the “Liquidating Trust”) and interests in that trust will also be distributed to FCF shareholders on or about December 16, 2015. These two distributions will constitute the full redemption for all shares of FCF and existing FCF shareholders will all become beneficiaries of the Liquidating Trust, which will make periodic distributions as cash is received for the remaining investments. The record date for these distributions is December 9, 2015, so no further subscriptions or redemptions will be accepted. Interests in the Liquidating Trust will not trade and will, in general, be transferable only by operation of law.

…

In line with its investment approach, FCF has some investments in companies that have undergone restructurings in the last eighteen months, and while we believe that these investments are likely to generate positive returns for shareholders over time, if FCF were forced to sell those investments immediately, it would only realize a portion of those investments’ fair value given current market conditions. We believe that doing so would be contrary to the interests of all of our shareholders, which is why we have taken steps to protect shareholder value by returning cash and implementing the Liquidating Trust to seek maximum value for these investments.

The past performance of this fund – which I have not examined in any detail at all – makes it seem like just another go-go fund:

In 2010, it earned 15.63%, according to Morningstar MORN +0.00%, outperforming the Barclays Aggregate Bond Index by over 900 basis points. That out-performance turned in 2011 when bond markets were spooked by the government’s near-breach of a debt limit, but it returned the following year. In 2013, the Third Avenue Credit Fund was the top fund in its category, according to Morningstar, returning 16.8%, outperforming its index by a whopping 1,800 basis points.

Over the past 24-months, Third Avenue’s performance turned sharply negative, testing investors’ patience. Part of the fund’s troubles come from owning debts in some of the largest leveraged buyouts that remain in the coffers of private equity firms, or stumbled in their return to public markets.

But, as a chart prepared by the WSJ indicates, go-go investing works really well for managers!

Click for Big

Look at all that money chasing performance! But all good things come to an end:

The fund, which had $3.5 billion in assets as recently as July of last year, suffered almost $1 billion in redemptions this year through November. The Third Avenue fund lost 13 percent in the past month and is down 27 percent this year, according to data compiled by Bloomberg. Assets have declined to $788 million as of Dec. 8 as clients pulled an estimated $979 million this year through November, according to Morningstar Inc.

“It’s significantly bad news for the market, and another straw on the camel’s back,” said Martin Fridson, a money manager at Lehmann Livian Fridson Advisors LLC. “It’s not typical, but it raises the question: Can this happen to the next-worst fund? You just don’t know. It certainly doesn’t encourage people to put money in, and that just exacerbates the liquidity problem there.”

The weakness in the market comes as credit quality in speculative-grade debt is falling. For every junk-bond issuer that had its rating boosted this year, two have been downgraded, a ratio not seen since 2009, according to data compiled by Bloomberg.

And companies are increasingly defaulting on their debt. Swift Energy Co.’s failure to make an $8.9 million interest payment last week raised the global tally of defaults to 102 issuers, a figure last exceeded in 2009, according to Standard & Poor’s.

And there is some credibility to the claim that the fund fell into a shark tank:

Mutual funds that own hard-to-trade debt are gunning for an advantage when it comes to returns, but they can face a big disadvantage when it comes time to sell.

They are often the weakest hand in a market of hungry experienced traders simply by virtue of their structure. They must publicly report their holdings, albeit on a delayed basis, and disclose information about investor inflows and outflows. Hedge funds, on the other hand, do not have to disclose nearly as much.

That’s like putting a huge “kick me” sign on these mutual funds when investors start asking for their money back. Because the debt these funds own may only trade a few times a year, prices are as reliant on supply and demand as the actual fundamentals of a given company.

…

Exhibit A of this phenomenon is Third Avenue Management. After it decided to liquidate its $788 million mutual fund that focuses on highly distressed debt — and to gate in remaining investors to avoid a fire sale of the remaining assets — its chief executive hinted that the fund was a victim of just such behavior.“Our portfolio was well known, it’s almost like we were targeted,” CEO David Barse said, according to the Wall Street Journal.

But misery loves company, and fund holders had that, all right:

Global financial markets turned gloomy as the prospects for a Federal Reserve interest-rate increase next week and a drop in oil helped spark a selloff in riskier assets, from equities to commodities to high-yield debt.

U.S. stocks tumbled to a two-month low, with the Dow Jones Industrial Average dropping more than 300 points, while shares in developing nations extended the longest slump since June. Oil plunged below $36 a barrel to cap its worst week in a year, and junk bonds had their worst day since December 2012. Treasuries rallied with the yen on haven demand.

…

The Standard & Poor’s 500 Index slumped 1.9 percent to 2,012.37 at 4 p.m. in New York, to the lowest level since Oct. 14. The gauge sank 3.8 percent in the week. That’s the most since Aug. 21, when signs of slowing growth from China to Europe rekindled concern that weakness could spread to America.

…

The iShares iBoxx $ High Yield Corporate Bond exchange-traded fund, known by its ticker of HYG, tumbled 2.7 percent as oil extended its loss. Trading in the high-yield ETF options surged as billionaire investor Carl Icahnsaid more pain is coming. “The meltdown in High Yield is just beginning,” he wrote on his verified Twitter account Friday.

…

Traders are pricing in a 72 percent chance that the Fed will raise rates at its Dec. 16 meeting, with data out of the U.S. Friday showing growth in retail sales and producer prices for November. That’s down from 80 percent earlier this week, amid the turmoil on financial markets.

…

The Stoxx Europe 600 Index tumbled 2 percent, taking its weekly loss to 4 percent. The regional benchmark fell to its lowest level since October and has sunk 7.7 in December amid a rout in commodity companies and disappointment over the European Central Bank’s last meeting.

…

The risk premium on the Markit CDX North American High Yield Index, a credit-default swaps benchmark tied to the debt of 100 speculative-grade companies, rose 36 basis points to 514.52 basis points, the highest since December 2012. BlackRock’s iShares iBoxx High Yield Corporate Bond ETF, the largest fund of its kind, fell to the lowest levels since 2009.U.S. 10-year yields fell nine basis points to 2.13 percent on Friday, compared with 2.17 percent on Dec. 31, 2014. The yield on similar-maturity German bunds was at 0.54 percent.

…

Oil declined to the lowest level since 2008 in London amid estimates that OPEC’s decision to scrap production limits will keep the market oversupplied. West Texas Intermediate for January delivery slipped to $35.62 a barrel for the lowest settlement since 2009.Crude capped its worst week in a year. The global oil surplus will persist at least until late 2016 as demand growth slows and OPEC shows “renewed determination” to maximize output, the International Energy Agency said in a report released Friday.

I ran across an interesting blog post today – CBO: Tangled Web of Welfare Programs Creates High Tax Rates on Participants, which included this chart:

Click for Big

… and this map of US federal programmes:

Click for Big

Despite all this there are still many people willing to snare people in the poverty trap; if this requires intellectual dishonesty when discussing a universal refundable tax credit, so what?

E-L Financial, proud issuer of ELF.PR.F, ELF.PR.G and ELF.PR.H, has Solidified its Long-term Interest in Empire Life:

Financial Corporation Limited (E-L Financial) (TSX:ELF) (TSX:ELF.PR.F) (TSX:ELF.PR.G) (TSX:ELF.PR.H) has agreed to purchase Guardian Assurance Limited’s (Guardian) 19% share of holding company E-L Financial Services Limited (ELFS). As a result of this agreement, E-L Financial will own 100% of ELFS, which owns 98.3% of The Empire Life Insurance Company (Empire Life).

The transaction will close next week, at a purchase price of approximately book value, or $200 million (CDN).

“For years, Empire Life has been an important long-term investment for E-L Financial,” said Mr. Duncan Jackman, Chairman and Chief Executive Officer of E-L Financial, “We are very excited about being able to increase our stake in this great company and reinforce our continued commitment to its ongoing success.” Mr. Jackman also acknowledged Guardian’s strong contribution to Empire Life.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 33bp, FixedResets off 15bp and DeemedRetractibles up 41bp. Today’s big move in government rates took the YTW of FixedResets below 5%. The Performance Highlights table continues to show a lot of churn. Volume was extremely high by all standards save those of the last few days.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

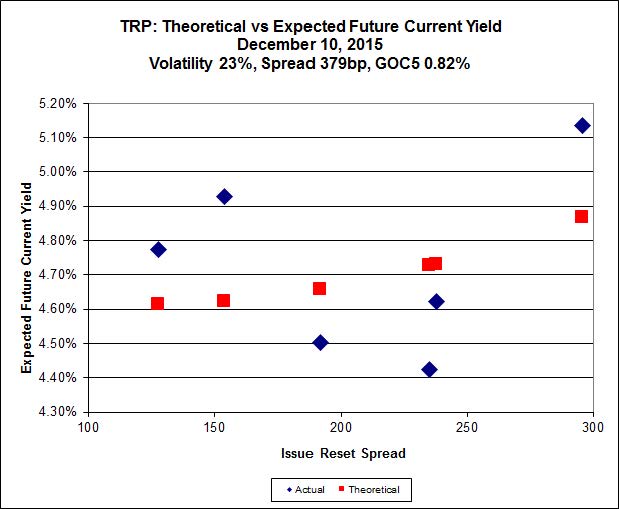

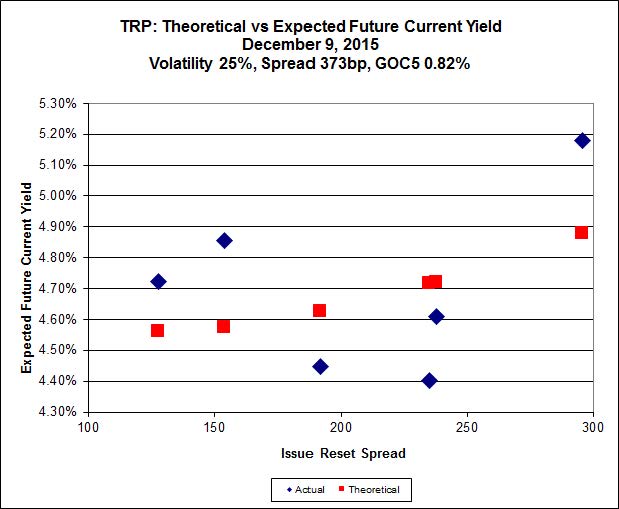

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.99 to be $1.14 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.89 cheap at its bid price of 11.81.

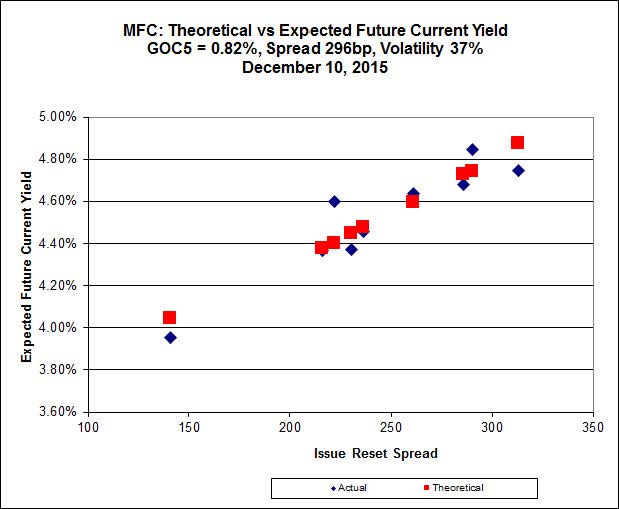

Click for Big

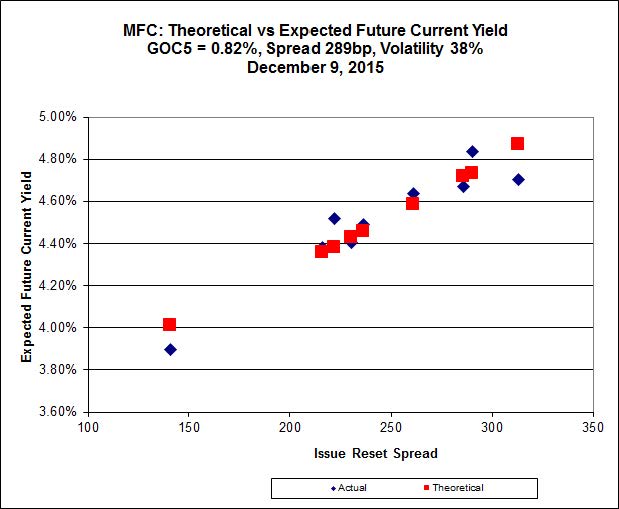

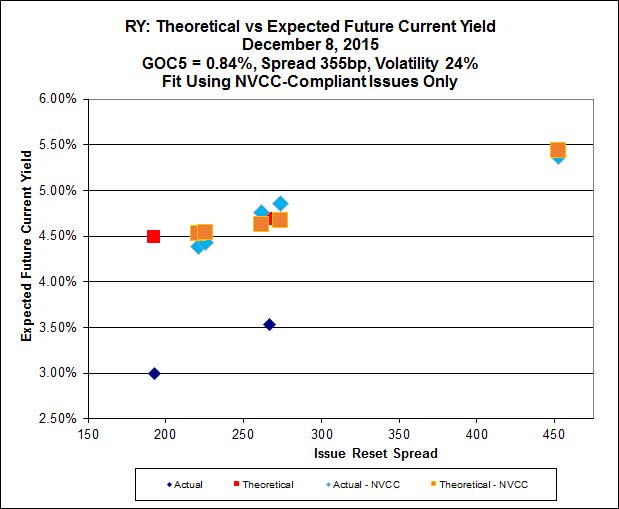

Mostexpensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 21.00 to be 0.57 rich, while MFC.PR.K, resetting at +222bp on 2018-9-19, is bid at 16.80 to be 0.59 cheap.

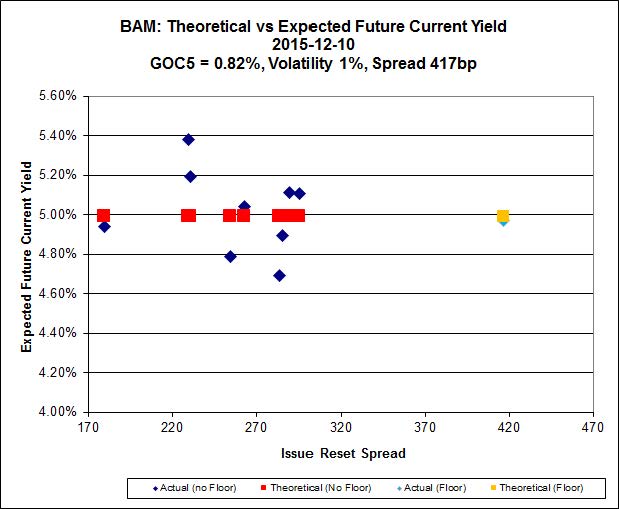

Click for Big

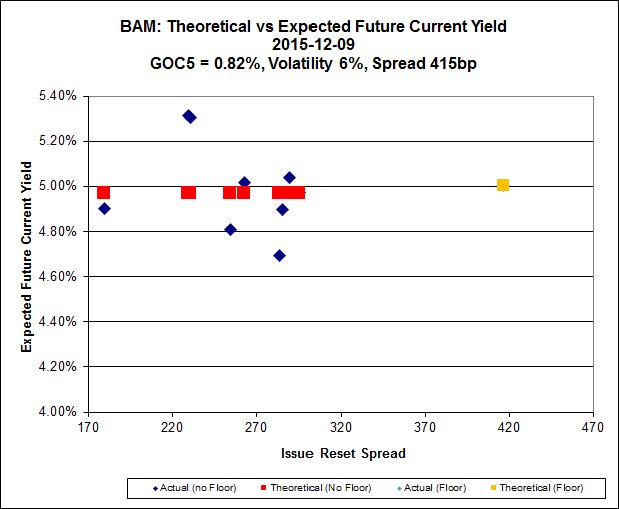

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 14.51 to be $0.83 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 19.50 and appears to be $1.44 rich.

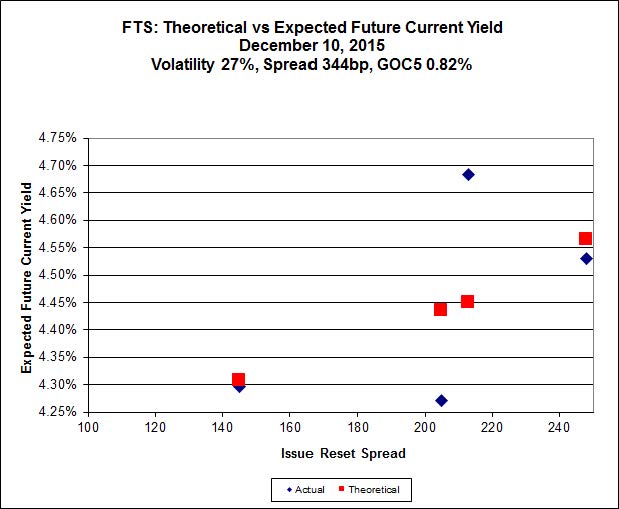

Click for Big

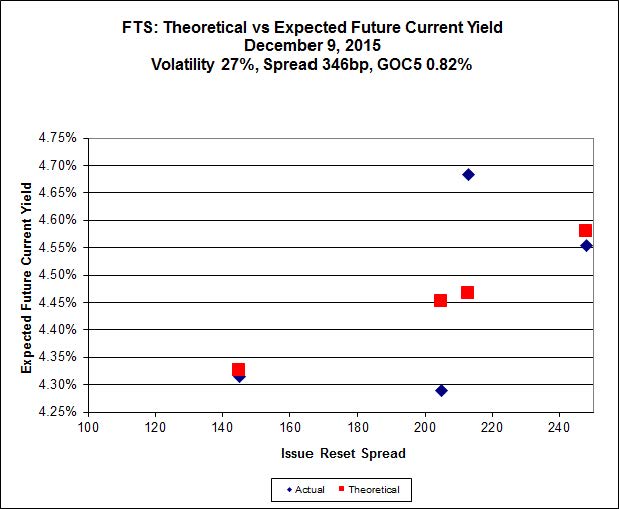

FTS.PR.K, with a spread of +205bp, and bid at 17.00, looks $0.75 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 16.00 and is $0.75 cheap.

Click for Big

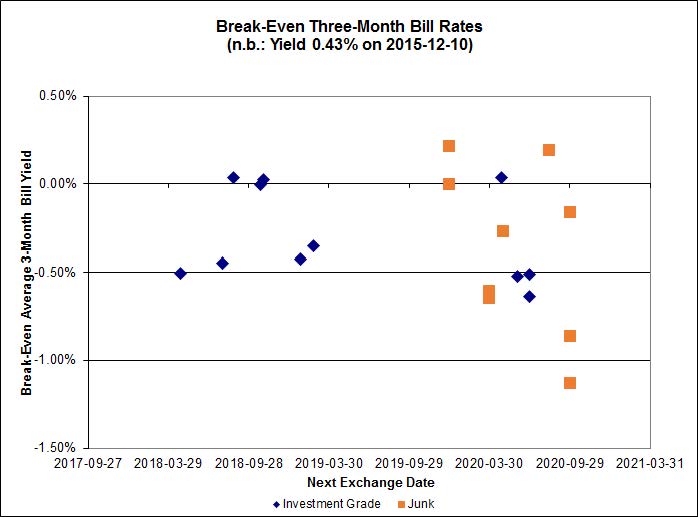

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.40%, with no outliers. There is one junk outlier below -1.50%.

Click for Big

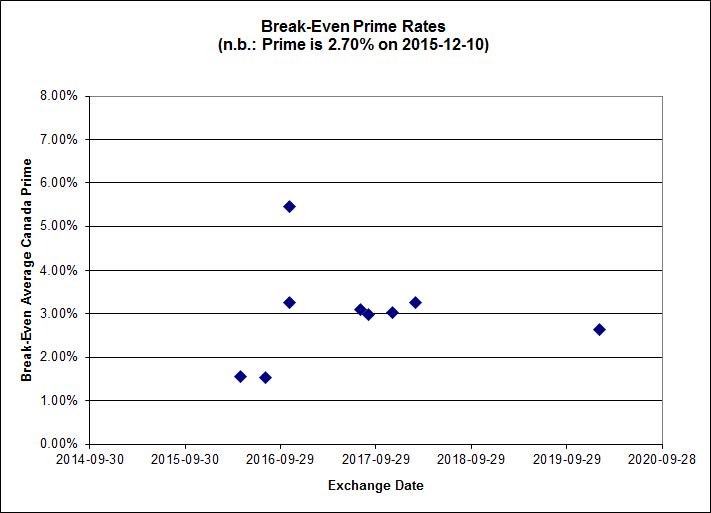

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 5.11 % | 6.21 % | 33,729 | 16.39 | 1 | 1.0638 % | 1,518.1 |

| FixedFloater | 7.39 % | 6.55 % | 33,493 | 15.58 | 1 | -2.5038 % | 2,639.7 |

| Floater | 4.45 % | 4.63 % | 86,239 | 16.21 | 4 | -1.5309 % | 1,716.8 |

| OpRet | 4.87 % | 4.20 % | 28,843 | 0.71 | 1 | 0.0000 % | 2,734.3 |

| SplitShare | 4.85 % | 5.62 % | 84,680 | 1.89 | 6 | -0.5335 % | 3,186.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.5335 % | 2,486.0 |

| Perpetual-Premium | 5.88 % | 5.94 % | 93,087 | 13.89 | 7 | 0.2430 % | 2,464.5 |

| Perpetual-Discount | 5.83 % | 5.91 % | 102,793 | 13.96 | 33 | 0.3315 % | 2,456.3 |

| FixedReset | 5.52 % | 4.90 % | 258,329 | 14.80 | 78 | -0.1508 % | 1,870.1 |

| Deemed-Retractible | 5.30 % | 5.46 % | 136,053 | 5.32 | 33 | 0.4072 % | 2,531.7 |

| FloatingReset | 2.85 % | 4.44 % | 64,555 | 5.68 | 11 | -0.4301 % | 2,070.3 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| BIP.PR.B | FixedReset | -3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 22.56 Evaluated at bid price : 23.55 Bid-YTW : 5.83 % |

| HSE.PR.A | FixedReset | -2.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 11.37 Evaluated at bid price : 11.37 Bid-YTW : 5.48 % |

| HSE.PR.G | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 6.15 % |

| BAM.PR.K | Floater | -2.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 10.10 Evaluated at bid price : 10.10 Bid-YTW : 4.68 % |

| BAM.PR.G | FixedFloater | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 25.00 Evaluated at bid price : 12.85 Bid-YTW : 6.55 % |

| BAM.PR.C | Floater | -2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 10.15 Evaluated at bid price : 10.15 Bid-YTW : 4.65 % |

| RY.PR.L | FixedReset | -2.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.37 Bid-YTW : 4.40 % |

| BNS.PR.B | FloatingReset | -1.90 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.15 Bid-YTW : 5.07 % |

| BAM.PR.B | Floater | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 10.20 Evaluated at bid price : 10.20 Bid-YTW : 4.63 % |

| BNS.PR.R | FixedReset | -1.69 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.30 Bid-YTW : 4.66 % |

| BIP.PR.A | FixedReset | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 18.70 Evaluated at bid price : 18.70 Bid-YTW : 5.85 % |

| BNS.PR.Q | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.77 Bid-YTW : 4.82 % |

| BNS.PR.D | FloatingReset | -1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.07 Bid-YTW : 7.08 % |

| CM.PR.Q | FixedReset | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 18.24 Evaluated at bid price : 18.24 Bid-YTW : 4.94 % |

| BAM.PR.Z | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.95 Evaluated at bid price : 17.95 Bid-YTW : 5.36 % |

| MFC.PR.M | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.59 Bid-YTW : 8.21 % |

| TRP.PR.C | FixedReset | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 11.81 Evaluated at bid price : 11.81 Bid-YTW : 4.92 % |

| FTS.PR.I | FloatingReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 11.55 Evaluated at bid price : 11.55 Bid-YTW : 4.12 % |

| NA.PR.S | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 16.98 Evaluated at bid price : 16.98 Bid-YTW : 4.96 % |

| TRP.PR.B | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 10.86 Evaluated at bid price : 10.86 Bid-YTW : 4.75 % |

| PVS.PR.E | SplitShare | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-10-31 Maturity Price : 25.00 Evaluated at bid price : 23.90 Bid-YTW : 6.35 % |

| PVS.PR.D | SplitShare | -1.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 22.42 Bid-YTW : 6.72 % |

| BMO.PR.S | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.50 Evaluated at bid price : 17.50 Bid-YTW : 4.68 % |

| MFC.PR.N | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.64 Bid-YTW : 8.10 % |

| HSE.PR.C | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 5.95 % |

| TD.PR.S | FixedReset | -1.04 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.91 Bid-YTW : 4.47 % |

| PVS.PR.B | SplitShare | -1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2019-01-10 Maturity Price : 25.00 Evaluated at bid price : 24.00 Bid-YTW : 5.83 % |

| SLF.PR.D | Deemed-Retractible | 1.03 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.64 Bid-YTW : 7.77 % |

| CU.PR.F | Perpetual-Discount | 1.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 19.40 Evaluated at bid price : 19.40 Bid-YTW : 5.85 % |

| BAM.PR.E | Ratchet | 1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 25.00 Evaluated at bid price : 13.30 Bid-YTW : 6.21 % |

| BMO.PR.Z | Perpetual-Discount | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 22.51 Evaluated at bid price : 22.84 Bid-YTW : 5.51 % |

| GWO.PR.S | Deemed-Retractible | 1.13 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.12 Bid-YTW : 5.75 % |

| GWO.PR.I | Deemed-Retractible | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.18 Bid-YTW : 7.45 % |

| SLF.PR.A | Deemed-Retractible | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.94 Bid-YTW : 7.21 % |

| GWO.PR.Q | Deemed-Retractible | 1.17 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.55 Bid-YTW : 6.59 % |

| FTS.PR.K | FixedReset | 1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 4.45 % |

| MFC.PR.G | FixedReset | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.43 Bid-YTW : 7.12 % |

| GWO.PR.R | Deemed-Retractible | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.01 Bid-YTW : 7.22 % |

| POW.PR.A | Perpetual-Discount | 1.22 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 23.74 Evaluated at bid price : 24.05 Bid-YTW : 5.91 % |

| IFC.PR.A | FixedReset | 1.22 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 14.85 Bid-YTW : 9.76 % |

| TRP.PR.H | FloatingReset | 1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 9.83 Evaluated at bid price : 9.83 Bid-YTW : 4.37 % |

| FTS.PR.J | Perpetual-Discount | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.62 % |

| GWO.PR.P | Deemed-Retractible | 1.37 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.65 Bid-YTW : 6.18 % |

| IFC.PR.C | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.31 Bid-YTW : 8.36 % |

| FTS.PR.G | FixedReset | 1.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 16.00 Evaluated at bid price : 16.00 Bid-YTW : 4.77 % |

| MFC.PR.K | FixedReset | 1.63 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 16.80 Bid-YTW : 8.53 % |

| SLF.PR.C | Deemed-Retractible | 1.65 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.74 Bid-YTW : 7.70 % |

| MFC.PR.L | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.35 Bid-YTW : 8.20 % |

| SLF.PR.J | FloatingReset | 1.73 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.92 Bid-YTW : 10.05 % |

| MFC.PR.J | FixedReset | 1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.85 Bid-YTW : 7.30 % |

| TRP.PR.G | FixedReset | 1.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 5.02 % |

| SLF.PR.H | FixedReset | 1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.85 Bid-YTW : 8.96 % |

| BAM.PR.R | FixedReset | 2.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 14.51 Evaluated at bid price : 14.51 Bid-YTW : 5.35 % |

| CU.PR.C | FixedReset | 4.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.80 Evaluated at bid price : 17.80 Bid-YTW : 4.55 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| BNS.PR.A | FloatingReset | 378,986 | TD crossed blocks of 80,476 and 284,943, both at 22.82. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.83 Bid-YTW : 4.07 % |

| PWF.PR.K | Perpetual-Discount | 305,430 | Nesbitt crossed 300,000 at 21.46. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 21.44 Evaluated at bid price : 21.44 Bid-YTW : 5.86 % |

| PWF.PR.E | Perpetual-Discount | 301,700 | Nesbitt crossed 300,000 at 23.36. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 23.10 Evaluated at bid price : 23.36 Bid-YTW : 5.96 % |

| PWF.PR.S | Perpetual-Discount | 213,165 | Nesbitt crossed 200,000 at 20.82. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 20.60 Evaluated at bid price : 20.60 Bid-YTW : 5.91 % |

| BAM.PR.K | Floater | 211,400 | TD crossed 200,000 at 10.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 10.10 Evaluated at bid price : 10.10 Bid-YTW : 4.68 % |

| BAM.PR.C | Floater | 207,699 | TD crossed 200,000 at 10.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 10.15 Evaluated at bid price : 10.15 Bid-YTW : 4.65 % |

| PWF.PR.L | Perpetual-Discount | 203,425 | Nesbitt crossed 200,000 at 21.82. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 21.57 Evaluated at bid price : 21.83 Bid-YTW : 5.91 % |

| CU.PR.I | FixedReset | 149,244 | Desardins crossed 50,000 at 24.90. Scotia crossed blocks of 25,000 and 50,000 at the same price. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 23.09 Evaluated at bid price : 24.80 Bid-YTW : 4.46 % |

| TD.PF.B | FixedReset | 109,519 | Nesbitt crossed 65,700 at 17.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-12-11 Maturity Price : 17.21 Evaluated at bid price : 17.21 Bid-YTW : 4.67 % |

| FTS.PR.E | OpRet | 100,400 | Scotia crossed 100,000 at 25.22. YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2016-08-31 Maturity Price : 25.00 Evaluated at bid price : 25.16 Bid-YTW : 4.20 % |

| There were 77 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| RY.PR.L | FixedReset | Quote: 24.37 – 25.00 Spot Rate : 0.6300 Average : 0.3805 YTW SCENARIO |

| CIU.PR.A | Perpetual-Discount | Quote: 20.36 – 21.19 Spot Rate : 0.8300 Average : 0.6453 YTW SCENARIO |

| HSE.PR.C | FixedReset | Quote: 17.00 – 17.50 Spot Rate : 0.5000 Average : 0.3312 YTW SCENARIO |

| GWO.PR.M | Deemed-Retractible | Quote: 24.81 – 25.26 Spot Rate : 0.4500 Average : 0.2836 YTW SCENARIO |

| TD.PF.E | FixedReset | Quote: 19.38 – 19.90 Spot Rate : 0.5200 Average : 0.3627 YTW SCENARIO |

| MFC.PR.G | FixedReset | Quote: 19.43 – 19.97 Spot Rate : 0.5400 Average : 0.4013 YTW SCENARIO |