I’m taking up a collection to save the endangered FX trader:

A widening probe of the foreign-exchange market is roiling an industry already under pressure to reduce costs as computer platforms displace human traders.

Electronic dealing, which accounted for 66 percent of all currency transactions in 2013 and 20 percent in 2001, will increase to 76 percent within five years, according to Aite Group LLC, a Boston-based consulting firm that reviewed Bank for International Settlements data. About 81 percent of spot trading — the buying and selling of currency for immediate delivery — will be electronic by 2018, Aite said.

…

The push toward electronic trading probably will lower costs for customers and boost transparency of pricing, according to Cormac Leech, an analyst at Liberum Capital Ltd. in London. It may also squeeze margins for banks, he said.Human traders have maintained their role in the foreign-exchange market while disappearing in areas such as equities because most trading takes place away from exchanges. That means clients don’t have a central repository showing the flow of completed orders, forcing them to piece together information about the direction of rates from traders and salesmen with knowledge of other clients’ orders. People were also needed because early computerized trading systems weren’t reliable and couldn’t handle larger transactions, according to dealers.

If Cormac Leech in the third paragraph is right, it will be the first time transparency has helped customers as a whole in a financial market. In all other markets, such a transition results in dealers holding less inventory and spreads narrowing but becoming much more brittle – more intra-day volatility. We will see!

It was a positive day for the Canadian preferred share market, with PerpetualDiscounts up 10bp, FixedResets gaining 7bp and DeemedRetractibles winning 11bp. Volatility was minimal. Volume was average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.2001 % | 2,415.8 |

| FixedFloater | 4.76 % | 4.35 % | 30,960 | 17.72 | 1 | -0.1502 % | 3,563.8 |

| Floater | 3.00 % | 3.11 % | 53,570 | 19.40 | 4 | 0.2001 % | 2,608.4 |

| OpRet | 4.61 % | -0.30 % | 67,536 | 0.11 | 3 | -0.0256 % | 2,687.8 |

| SplitShare | 4.87 % | 5.01 % | 59,885 | 4.32 | 5 | 0.0241 % | 3,012.1 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.0256 % | 2,457.7 |

| Perpetual-Premium | 5.67 % | 1.45 % | 96,759 | 0.08 | 12 | 0.0364 % | 2,335.4 |

| Perpetual-Discount | 5.55 % | 5.64 % | 151,194 | 14.40 | 26 | 0.0951 % | 2,389.4 |

| FixedReset | 4.85 % | 3.71 % | 211,849 | 6.49 | 80 | 0.0699 % | 2,490.9 |

| Deemed-Retractible | 5.11 % | 4.08 % | 161,436 | 1.69 | 42 | 0.1131 % | 2,426.8 |

| FloatingReset | 2.65 % | 2.68 % | 162,170 | 7.10 | 6 | 0.1477 % | 2,438.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| PWF.PR.A | Floater | 1.15 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-18 Maturity Price : 19.29 Evaluated at bid price : 19.29 Bid-YTW : 2.73 % |

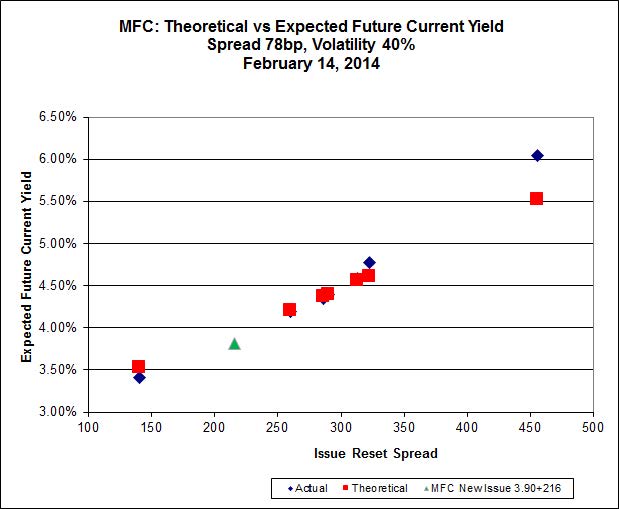

| MFC.PR.F | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.70 Bid-YTW : 4.51 % |

| BAM.PR.X | FixedReset | 1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-18 Maturity Price : 21.19 Evaluated at bid price : 21.19 Bid-YTW : 4.38 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.Z | FixedReset | 289,384 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-18 Maturity Price : 23.23 Evaluated at bid price : 25.25 Bid-YTW : 3.74 % |

| MFC.PR.I | FixedReset | 68,150 | Scotia crossed 50,000 at 26.05. YTW SCENARIO Maturity Type : Call Maturity Date : 2017-09-19 Maturity Price : 25.00 Evaluated at bid price : 26.00 Bid-YTW : 3.44 % |

| NA.PR.S | FixedReset | 65,946 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-18 Maturity Price : 23.19 Evaluated at bid price : 25.12 Bid-YTW : 3.93 % |

| MFC.PR.E | FixedReset | 64,875 | TD crossed 50,000 at 25.59. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-09-19 Maturity Price : 25.00 Evaluated at bid price : 25.59 Bid-YTW : 3.15 % |

| ENB.PR.P | FixedReset | 57,345 | Nesbitt crossed 47,300 at 24.10. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-18 Maturity Price : 22.79 Evaluated at bid price : 24.04 Bid-YTW : 4.20 % |

| CU.PR.E | Perpetual-Discount | 50,640 | Scotia crossed 42,600 at 22.90. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-02-18 Maturity Price : 22.52 Evaluated at bid price : 22.90 Bid-YTW : 5.35 % |

| There were 36 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PR.N | Perpetual-Discount | Quote: 19.90 – 20.10 Spot Rate : 0.2000 Average : 0.1218 YTW SCENARIO |

| PWF.PR.R | Perpetual-Discount | Quote: 24.55 – 24.75 Spot Rate : 0.2000 Average : 0.1250 YTW SCENARIO |

| BAM.PR.R | FixedReset | Quote: 25.02 – 25.24 Spot Rate : 0.2200 Average : 0.1579 YTW SCENARIO |

| SLF.PR.D | Deemed-Retractible | Quote: 21.10 – 21.33 Spot Rate : 0.2300 Average : 0.1704 YTW SCENARIO |

| CIU.PR.C | FixedReset | Quote: 20.10 – 20.50 Spot Rate : 0.4000 Average : 0.3471 YTW SCENARIO |

| GWO.PR.M | Deemed-Retractible | Quote: 25.69 – 25.87 Spot Rate : 0.1800 Average : 0.1309 YTW SCENARIO |