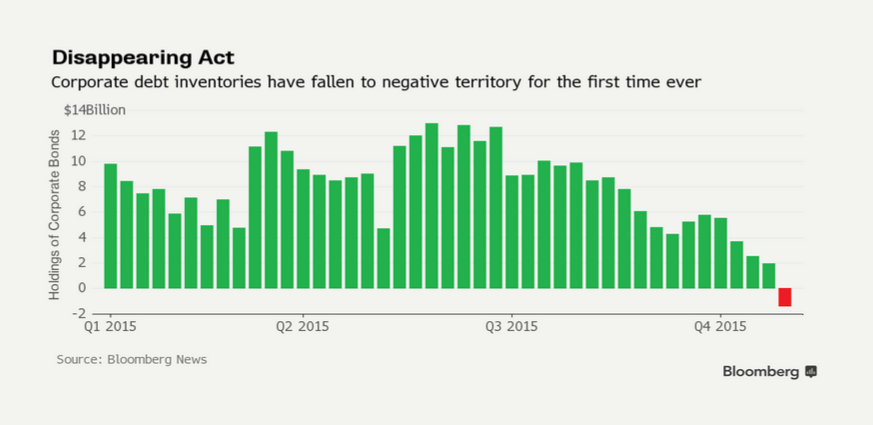

Assiduous Reader JP, who sends me more interesting links than all the rest of youse other bums combined, brings to my attention a popular press story on corporate bond liquidity:

Add one more name to the chorus of doom. Earlier this week, Andrew Tyrie, the Conservative MP and chairman of the Treasury Select Committee, wrote to Mark Carney, the Governor of the Bank of England, to express his concern about bond market liquidity – or, more precisely, the lack thereof.

…

In May, Nouriel Roubini, the US economist made famous for predicting the US housing problems that led to the financial crisis, wrote about “the liquidity timebomb”.In June, Stephen Schwarzman, the chief executive of private equity firm Blackstone, penned a comment piece for The Wall Street Journal on bond market liquidity entitled: “How the next financial crisis will happen”.

Why has what sounds like a pretty niche subject got so many knickers in such a twist?

…

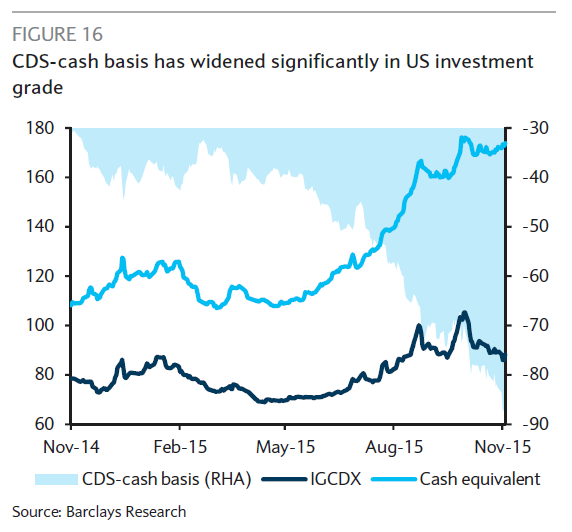

Regardless, there’s little appetite among regulators to row back on capital rules. So liquidity may need to come from somewhere else. One theory is that fund managers should try to trade directly with each other (although the fate of Bondcube, an online marketplace which tried to facilitate such transactions but went bust in July after only three months because investors couldn’t agree on prices without the involvement of a broker, doesn’t bode well).Or perhaps the amount of liquidity available before the crisis was the aberration and we now need to reset our expectations. Should, for example, investors be allowed to withdraw money, at a moment’s notice, from funds that invest in rarely-traded securities?

Regulators have made a trade-off. Banks have been made less risky. But, as Bill Gross, the famous bond investor, said earlier this year, that risk hasn’t been eliminated – it’s just moved elsewhere in the system.

Nouriel Roubini’s piece makes the point:

As a result, when surprises occur – for example, the Fed signals an earlier-than-expected exit from zero interest rates, oil prices spike, or eurozone growth starts to pick up – the re-rating of stocks and especially bonds can be abrupt and dramatic: everyone caught in the same crowded trades needs to get out fast. Herding in the opposite direction occurs, but, because many investments are in illiquid funds and the traditional market makers who smoothed volatility are nowhere to be found, the sellers are forced into fire sales.

This combination of macro liquidity and market illiquidity is a time bomb. So far, it has led only to volatile flash crashes and sudden changes in bond yields and stock prices. But, over time, the longer central banks create liquidity to suppress short-run volatility, the more they will feed price bubbles in equity, bond, and other asset markets. As more investors pile into overvalued, increasingly illiquid assets – such as bonds – the risk of a long-term crash increases.

This is the paradoxical result of the policy response to the financial crisis. Macro liquidity is feeding booms and bubbles; but market illiquidity will eventually trigger a bust and collapse.

Blackrock’s report is titled US EQUITY MARKET STRUCTURE: LESSONS FROM AUGUST 24:

Contributors to disruptions on the morning of August 24:

…

3.Excessive use of market and stop-loss orders that seek “liquidity at any price” inflamed the situation.

- When markets are volatile, liquidity can come at a cost.

- Market and stop-loss orders that demand “liquidity at any price” added to selling pressure and proved especially risky on the morning of August 24.

…

Recommendations for enhancing US equity market resiliency:

…

7.Educate investors on how to navigate the modern US equity market. Customer-facing broker-dealers should consider whether there is more to do to raise investor awareness regarding usage of market and stop-loss orders in volatile periods, especially at the open or close.

…

Orders that seek liquidity at any price may expose investors to prices which reflect the cost of liquidity at a given point in time as opposed to the underlying fundamental value of a security. Taken together, we believe that it is important that investors are educated about how to navigate today’s complex equity market and volatility. In particular, investors should have an understanding of the implications and potential risks associated with the use of “liquidity at any price” order types, such as market and stop-loss orders. We are supportive of ongoing cost/benefit analyses to determine whether certain constraints on market and stop-loss orders would be appropriate. Further discussion is needed to determine whether other protections should be implemented; for example, additional disclosure to customers regarding the potential risks associated with the use of market and stop-loss orders. Customer-facing broker-dealers are best positioned to consider ongoing investor education efforts.

Blackrock’s emphasis on investor education is very sweet and leaves me wondering how much of this was written to curry favour with the regulators. Retail, taken as a whole, is stupid and enjoys being stupid. There are about a bazillion pages on the Web touting stop-loss orders as the sure-fire way to get free money, such as Stops – Minimizing Losses And Protecting Gains:

Next time someone tells you their stock portfolio is up by 50%, congratulate them, then ask “What have you done to protect your profit?”

If they look at you with a puzzled expression on their face, then you know their 50% paper gain could easily be lost within a matter of days or weeks. If they tell you they have an exit strategy with Stop Losses in place to protect a large percentage of their gain, then you know they are probably prepared.

Investor education, hah! I’ve got news for Blackrock: you can lead a horse to water, but you can’t make it drink.

On another note, the NYSE is banning stop-loss orders:

Stop orders — or instructions to immediately trade once a stock hits a certain price, even if the price is far worse than the one on the order — will no longer be available starting on Feb. 26, NYSE said this week.

…

Brokerage firms can still program their systems to carry out orders that achieve the same results as a stop order for their clients, by entering a market order on the client’s behalf after a stock price reaches a specified threshold.Nonetheless, Cunningham said, the exchange wants “to raise the profile of the risks associated with this order type.”

One possibility for mitigating the volatility due to stop-loss orders is to make them transparent: the Exchanges could make public a list of trigger prices and stop volume throughout the trading day. This would, I think, lead to market players putting in limit bids somewhere below each stop-trigger in hopes of getting a lucky fill. Currently, the TSX (for example) does not provide pre-trade transparency on stop orders:

No pre-trade transparency of: i) orders entered in the MOC facility; ii) “On-Stop Book” orders, until the limit price of the order is triggered, at which point they become part of the “Regular Book”; and iii) dark orders are fully hidden until execution.

On the other hand, it would probably also lead to a thinning of the market immediately above the major trigger points, so maybe that’s not such a great idea. Another possibility is a new order type that would interact only with stop-loss orders; that is to say, instead of stop-loss orders turning into limit or market orders, they would retain their stop-identity for the purpose of interacting with this new, bottom-feeder, order type.

And on the other other hand, who cares? Players using stop-losses aren’t trading on fundamentals, so screw ’em! Vapourizing the investments of non-fundamental investors is a Public Good so let’s just do it, ride out the volatility and move on.

But perhaps the most effective argument against eliminating stop-loss as an order type is practical: the fact is that in the first place, such orders will simply move to the brokers’ books and in the second place will be available to anybody via a simple algorithm. The latter point means that you must accept that certain simple order types will suddenly be restricted to big players, which won’t be very popular with self-proclaimed Investor Activists or with regulators who stop and think about what it is they’re doing … well, OK, with self-proclaimed Investor Activists, anyway.

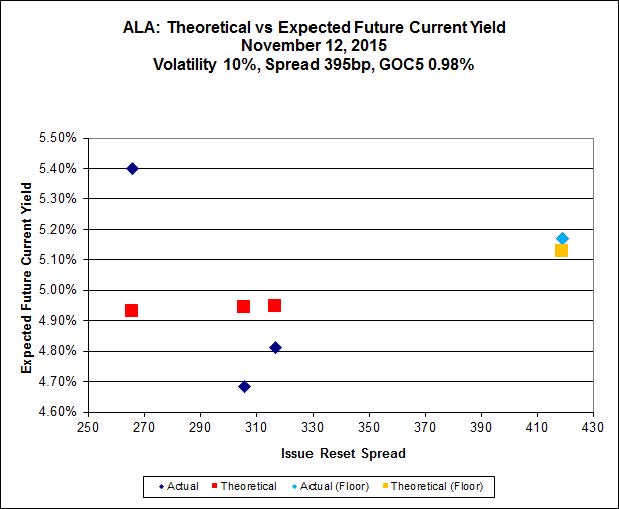

Veresen Inc., proud issuer of VSN.PR.A, was confirmed at Pfd-3 by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Senior Unsecured Notes rating of Veresen Inc. (Veresen or the Company) at BBB as well as its Preferred Shares rating at Pfd-3. The trend on the ratings is Stable. Veresen’s ratings are supported by firm take-or-pay and fee-based cash flows from a diversified portfolio of energy infrastructure assets; however, some of the Company’s midstream gas gathering and processing operations are exposed to volume and commodity price risks.

…

The Company’s non-consolidated financial profile remains reasonable for its current rating category. On a non-consolidated basis, the Company’s credit metrics improved in 2015 as debt relating to the Ruby acquisition in 2014 was fully repaid in 2015 with non-consolidated debt-to-capital at 24.1% and cash flow to debt at 32.5% as of Q3 2015. DBRS expects the Company to remain prudent in its future financing strategy to maintain its non-consolidated leverage at or near the 30.0% level.

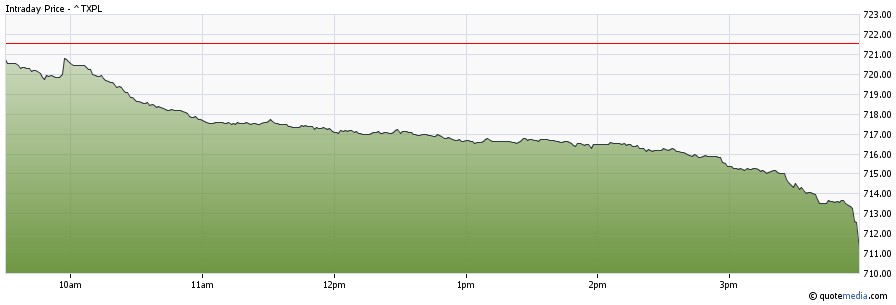

The market made a funny noise this afternoon:

Click for Big

No, I mean really, look at the TXPL chart:

Click for Big

So sure, it wasn’t a great day from the beginning, with the TXPL index down about half a point by about 11am and drifting slowly lower thereafter. Then the fun started at about 2:45pm, with the index losing an additional 14bp by 3:25pm, losing another 14bp by 3:39pm, and then just getting crushed, losing another 50bp by the close (to an index level of 710.46), for a total of 154bp on the day. Looks like we’re back to all that fun we had in September and early October, with motivated sellers waiting until late in the trading day to dump their holdings.

I’m not sure how that works. It seems to me that if I had a big sell order to execute, come hell or high water, I would try to take the market down earlier in the day, in order to attract some buyers at the lower prices. It seems to me that one possible – and I do mean possible, don’t anybody assume that this is what is actually happening – mechanism for this is that Joe Trader gets an order to sell 50,000 shares throughout the day, slaps it into a cautious, liquid-equity style algorithm and then finds out at 3pm that he’s only got fills on 5,000 and has to get cracking. I don’t like speculating about such micro-mechanisms, but … it just seems so wasteful to take the market down 50bp in the last five minutes-odd of the day, when relatively few participants will have a chance to react.

It was a rotten day for the Canadian preferred share market, with PerpetualDiscounts off 13bp, FixedResets losing 93bp and DeemedRetractibles down 36bp. The Performance Highlights table is suitably long, with a heavy load of TRP issues among the worst losers. Volume was extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

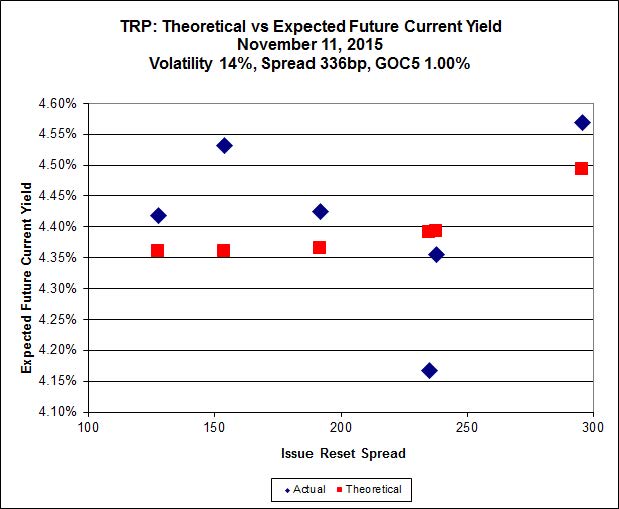

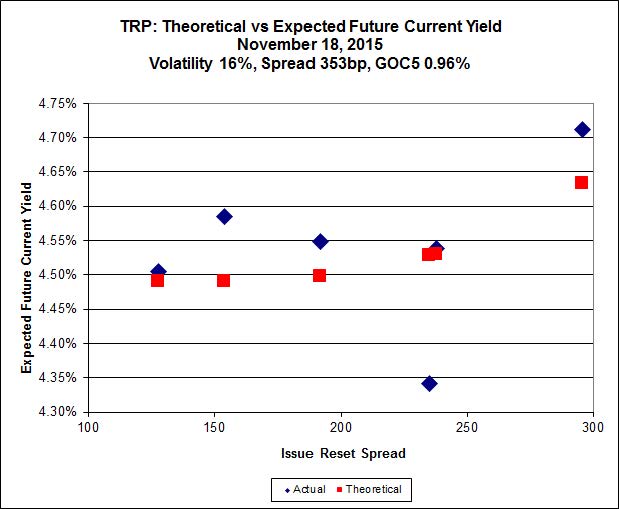

Here’s TRP:

Click for Big

TRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.06 to be $0.79 rich, while TRP.PR.G, resetting 2020-11-30 at +154, is $0.36 cheap at its bid price of 20.80.

Click for Big

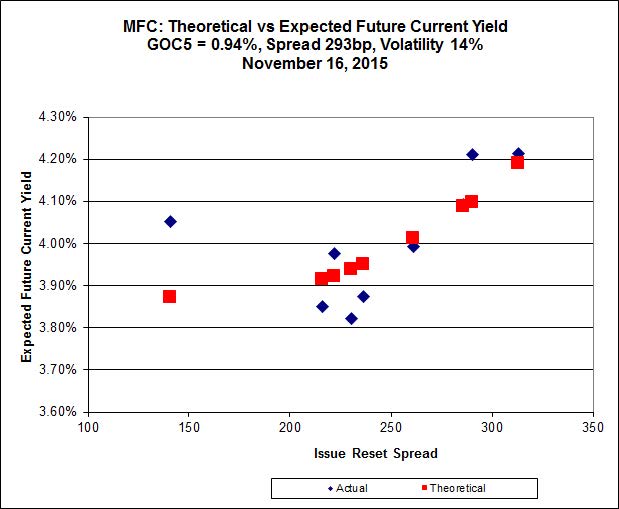

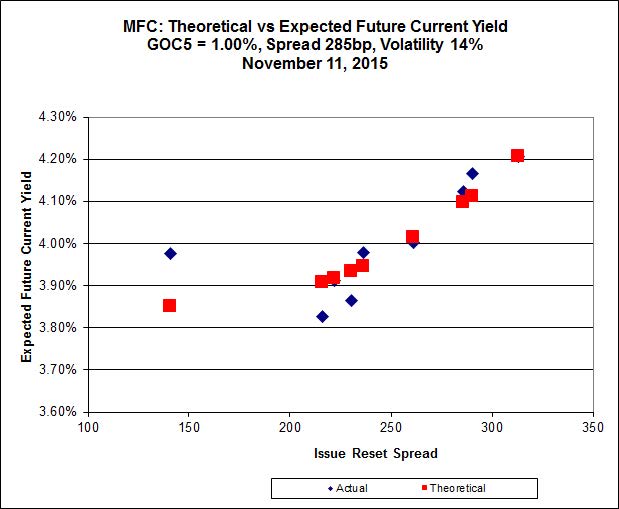

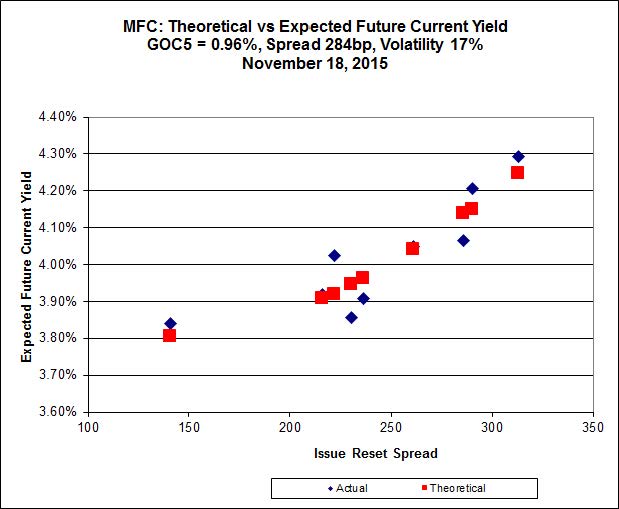

Most expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 21.13 to be 0.48 rich, while MFC.PR.K resetting at +222bp on 2018-9-19, is bid at 19.76 to be 0.52 cheap.

Click for Big

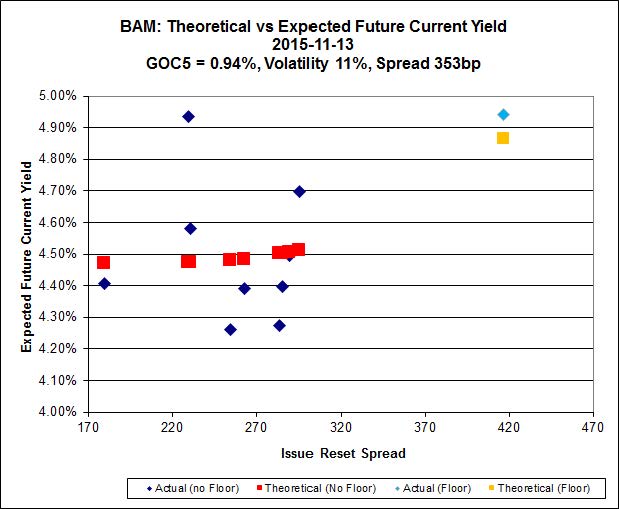

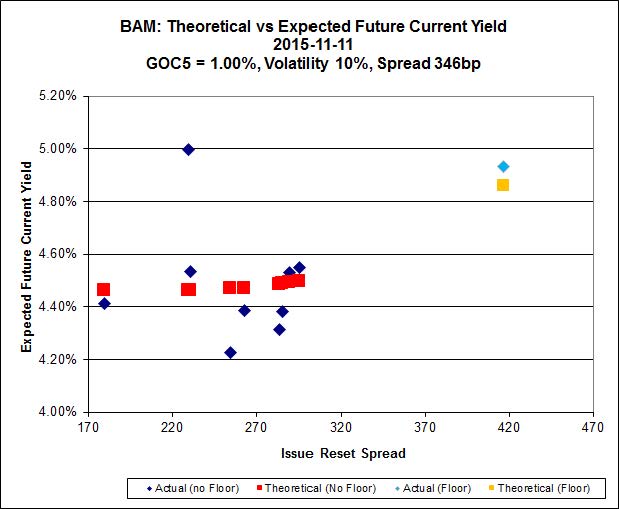

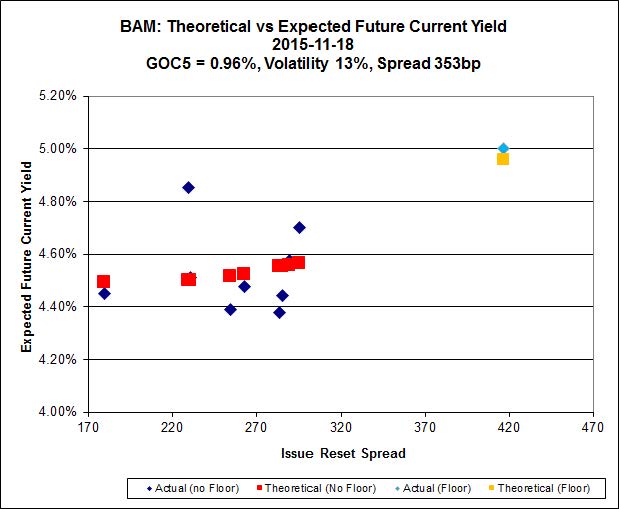

The cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.79 to be $1.33 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 21.70 and appears to be $0.83 rich.

Click for Big

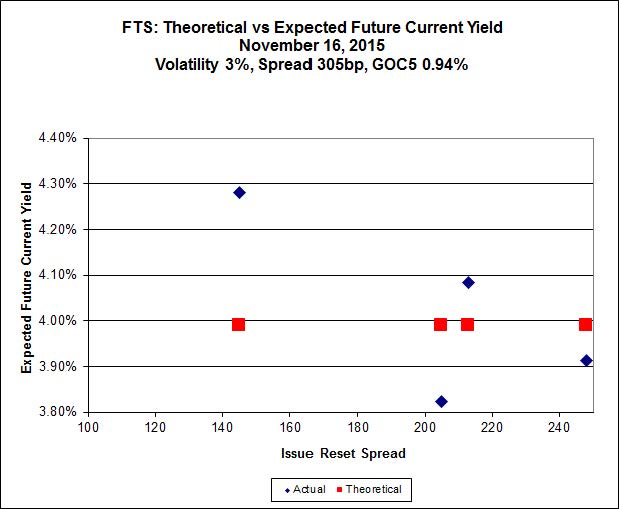

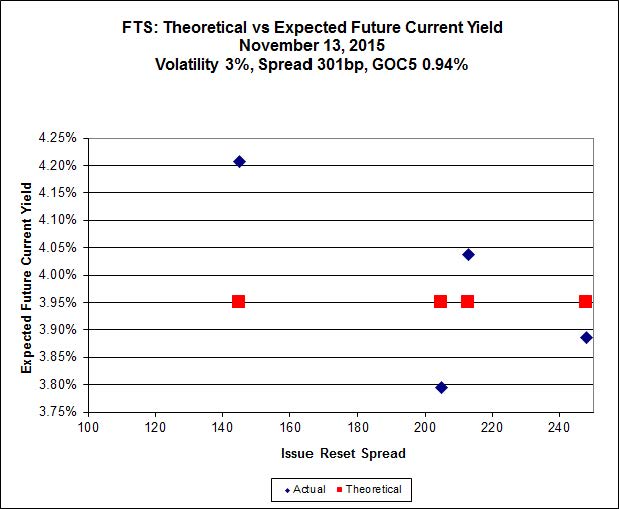

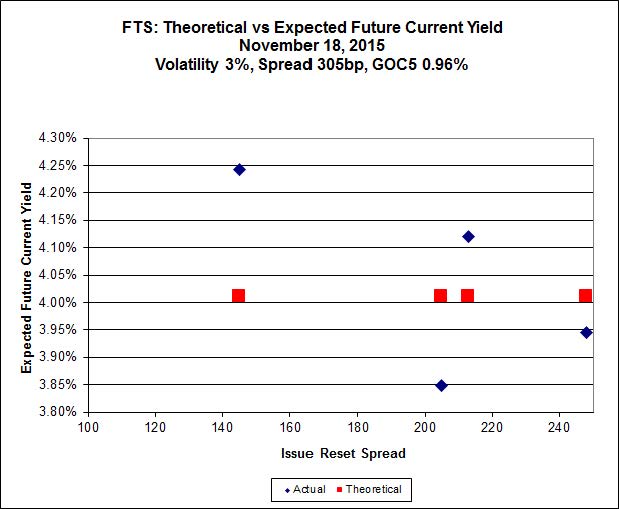

FTS.PR.K, with a spread of +205bp, and bid at 19.55, looks $0.78 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.20 and is $0.82 cheap.

Click for Big

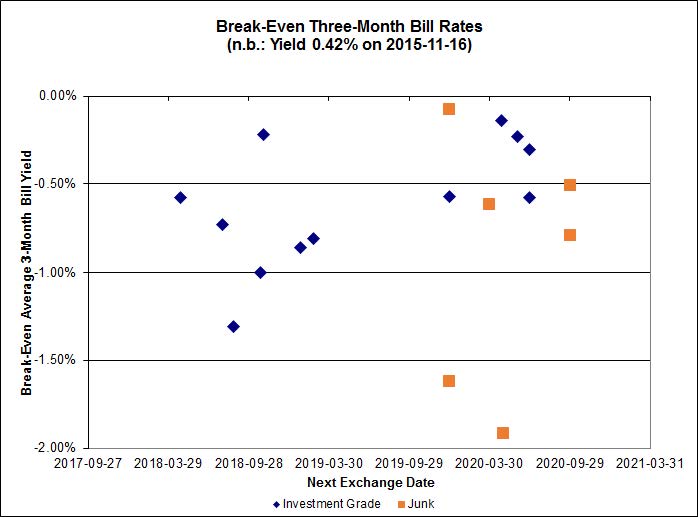

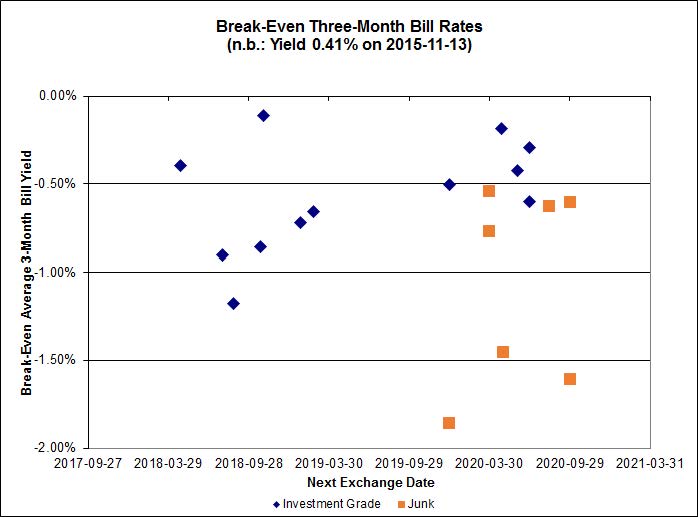

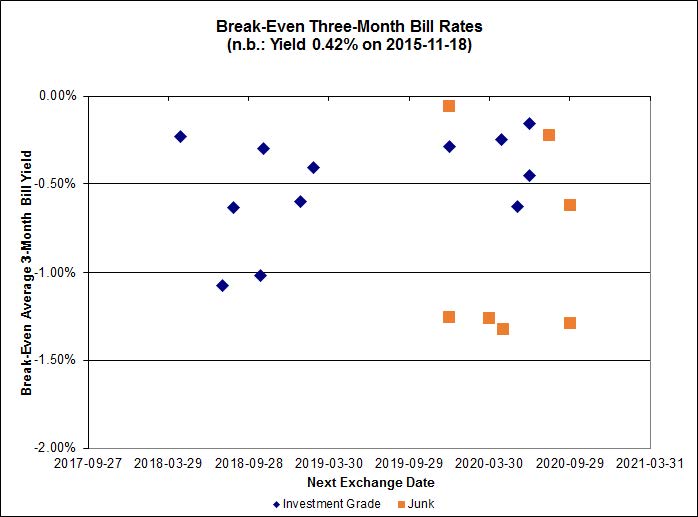

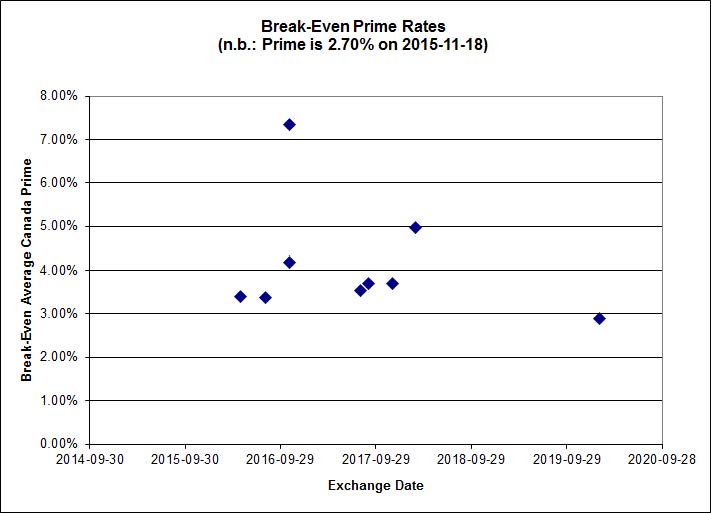

Investment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.50%, with no outliers. There are two junk outliers above 0.00% and one below -2.00%.

Click for Big

The BCE.PR.R / BCE.PF.Q pair is no longer being plotted as BCE.PF.Q will not be created, as pointed out by Assiduous Reader Peculiar_Investor.

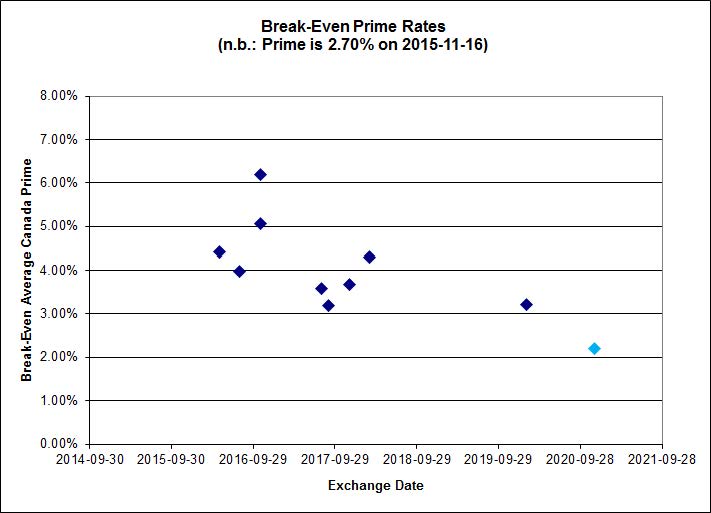

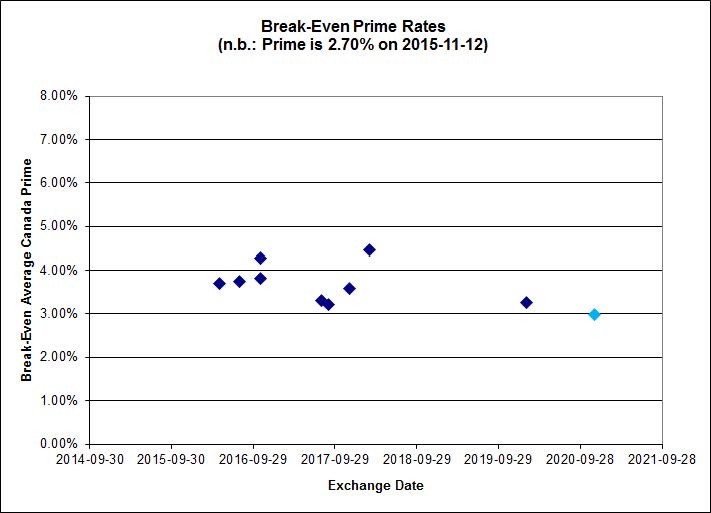

Shall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.19 % | 5.02 % | 33,409 | 17.81 | 1 | 0.8040 % | 1,853.3 |

| FixedFloater | 6.13 % | 5.37 % | 27,664 | 17.07 | 1 | 0.9115 % | 3,184.1 |

| Floater | 4.02 % | 4.05 % | 71,275 | 17.28 | 3 | -2.0267 % | 1,965.9 |

| OpRet | 4.87 % | 3.91 % | 33,654 | 0.77 | 1 | 0.0000 % | 2,733.2 |

| SplitShare | 4.77 % | 5.79 % | 139,572 | 2.92 | 5 | 0.1554 % | 3,209.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1554 % | 2,504.2 |

| Perpetual-Premium | 5.77 % | -3.17 % | 74,058 | 0.08 | 6 | -0.0983 % | 2,520.1 |

| Perpetual-Discount | 5.51 % | 5.56 % | 85,985 | 14.52 | 33 | -0.1288 % | 2,597.0 |

| FixedReset | 4.84 % | 4.57 % | 223,125 | 15.43 | 76 | -0.9315 % | 2,112.2 |

| Deemed-Retractible | 5.15 % | 5.15 % | 114,601 | 5.40 | 33 | -0.3563 % | 2,583.5 |

| FloatingReset | 2.57 % | 3.73 % | 55,485 | 5.77 | 10 | -0.1826 % | 2,195.6 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.B | FixedReset | -5.98 % | Only marginally real, since the issue traded 7,602 shares today in a range of 12.56-34, with a VWAP of 12.90. Every single one of the last 25 sales came out of Scotia, mostly in lots of 100 shares, taking the price down from 12.73 at 3:33 to 12.56 at 3:59 … but only the last four of these, totalling 900 shares, were at prices below 12.70. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 12.43 Evaluated at bid price : 12.43 Bid-YTW : 4.49 % |

| PWF.PR.P | FixedReset | -4.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 14.54 Evaluated at bid price : 14.54 Bid-YTW : 4.41 % |

| TRP.PR.C | FixedReset | -3.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 13.63 Evaluated at bid price : 13.63 Bid-YTW : 4.59 % |

| IAG.PR.G | FixedReset | -3.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.83 Bid-YTW : 5.19 % |

| TRP.PR.A | FixedReset | -3.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 15.83 Evaluated at bid price : 15.83 Bid-YTW : 4.74 % |

| GWO.PR.N | FixedReset | -3.19 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.65 Bid-YTW : 10.07 % |

| HSE.PR.E | FixedReset | -2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.84 Evaluated at bid price : 22.25 Bid-YTW : 5.11 % |

| TRP.PR.E | FixedReset | -2.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.06 Evaluated at bid price : 19.06 Bid-YTW : 4.62 % |

| VNR.PR.A | FixedReset | -2.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 4.57 % |

| TRP.PR.F | FloatingReset | -2.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 14.44 Evaluated at bid price : 14.44 Bid-YTW : 4.08 % |

| MFC.PR.J | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.05 Bid-YTW : 5.44 % |

| TRP.PR.D | FixedReset | -2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 18.40 Evaluated at bid price : 18.40 Bid-YTW : 4.73 % |

| BAM.PR.K | Floater | -2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 11.67 Evaluated at bid price : 11.67 Bid-YTW : 4.09 % |

| BMO.PR.T | FixedReset | -2.26 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.48 Evaluated at bid price : 19.48 Bid-YTW : 4.28 % |

| HSE.PR.A | FixedReset | -2.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 14.41 Evaluated at bid price : 14.41 Bid-YTW : 4.80 % |

| HSE.PR.C | FixedReset | -2.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 20.76 Evaluated at bid price : 20.76 Bid-YTW : 5.11 % |

| BAM.PR.B | Floater | -1.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 11.82 Evaluated at bid price : 11.82 Bid-YTW : 4.04 % |

| NA.PR.W | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 4.36 % |

| BMO.PR.Y | FixedReset | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.93 Evaluated at bid price : 22.41 Bid-YTW : 4.09 % |

| BAM.PR.C | Floater | -1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 4.05 % |

| FTS.PR.G | FixedReset | -1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.26 % |

| PWF.PR.T | FixedReset | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.93 Evaluated at bid price : 22.26 Bid-YTW : 3.88 % |

| BAM.PF.F | FixedReset | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 4.66 % |

| MFC.PR.H | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.82 Bid-YTW : 4.92 % |

| TRP.PR.H | FloatingReset | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 11.44 Evaluated at bid price : 11.44 Bid-YTW : 3.73 % |

| BMO.PR.W | FixedReset | -1.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.39 Evaluated at bid price : 19.39 Bid-YTW : 4.26 % |

| SLF.PR.H | FixedReset | -1.40 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.99 Bid-YTW : 6.85 % |

| W.PR.H | Perpetual-Discount | -1.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 23.57 Evaluated at bid price : 23.84 Bid-YTW : 5.83 % |

| W.PR.J | Perpetual-Discount | -1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 23.71 Evaluated at bid price : 23.98 Bid-YTW : 5.91 % |

| GWO.PR.Q | Deemed-Retractible | -1.35 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.37 Bid-YTW : 6.23 % |

| MFC.PR.G | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.95 Bid-YTW : 5.16 % |

| BMO.PR.S | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 20.09 Evaluated at bid price : 20.09 Bid-YTW : 4.25 % |

| BMO.PR.M | FixedReset | -1.30 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.35 Bid-YTW : 3.43 % |

| MFC.PR.N | FixedReset | -1.26 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.13 Bid-YTW : 5.84 % |

| TD.PF.E | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 22.23 Evaluated at bid price : 22.91 Bid-YTW : 4.11 % |

| MFC.PR.K | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.76 Bid-YTW : 6.58 % |

| CM.PR.O | FixedReset | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 4.31 % |

| PWF.PR.K | Perpetual-Discount | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 22.09 Evaluated at bid price : 22.37 Bid-YTW : 5.57 % |

| BAM.PR.Z | FixedReset | -1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 20.85 Evaluated at bid price : 20.85 Bid-YTW : 4.89 % |

| FTS.PR.K | FixedReset | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 4.05 % |

| TD.PF.C | FixedReset | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.55 Evaluated at bid price : 19.55 Bid-YTW : 4.27 % |

| MFC.PR.B | Deemed-Retractible | -1.06 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.57 Bid-YTW : 6.84 % |

| NA.PR.S | FixedReset | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.79 Evaluated at bid price : 19.79 Bid-YTW : 4.42 % |

| BAM.PR.M | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 5.80 % |

| BNS.PR.A | FloatingReset | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.67 Bid-YTW : 3.36 % |

| IFC.PR.A | FixedReset | 1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.55 Bid-YTW : 7.85 % |

| FTS.PR.J | Perpetual-Discount | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.63 Evaluated at bid price : 21.92 Bid-YTW : 5.42 % |

| FTS.PR.F | Perpetual-Discount | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 22.33 Evaluated at bid price : 22.60 Bid-YTW : 5.43 % |

| BNS.PR.Y | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.65 Bid-YTW : 5.20 % |

| BIP.PR.A | FixedReset | 1.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 21.35 Evaluated at bid price : 21.35 Bid-YTW : 5.35 % |

| SLF.PR.G | FixedReset | 1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.25 Bid-YTW : 8.60 % |

| MFC.PR.F | FixedReset | 2.87 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 15.43 Bid-YTW : 8.74 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.A | FixedReset | 109,290 | Nesbitt crossed 100,000 at 16.50. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 15.83 Evaluated at bid price : 15.83 Bid-YTW : 4.74 % |

| TRP.PR.C | FixedReset | 93,645 | Nesbitt crossed blocks of 18,800 and 59,900, both at 14.20. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 13.63 Evaluated at bid price : 13.63 Bid-YTW : 4.59 % |

| SLF.PR.I | FixedReset | 86,530 | TD crossed 18,500 at 22.39 and another 18,500 at 22.40, followed by two blocks of 18,600 each, both at 22.40. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.30 Bid-YTW : 5.34 % |

| TRP.PR.F | FloatingReset | 75,000 | RBC crossed 68,000 at 15.00. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 14.44 Evaluated at bid price : 14.44 Bid-YTW : 4.08 % |

| RY.PR.H | FixedReset | 57,874 | Scotia crossed 40,000 at 19.87. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-18 Maturity Price : 19.81 Evaluated at bid price : 19.81 Bid-YTW : 4.23 % |

| BNS.PR.M | Deemed-Retractible | 57,160 | TD crossed 50,000 at 25.15. YTW SCENARIO Maturity Type : Call Maturity Date : 2016-07-27 Maturity Price : 25.00 Evaluated at bid price : 25.10 Bid-YTW : 4.25 % |

| There were 56 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| TRP.PR.F | FloatingReset | Quote: 14.44 – 15.30 Spot Rate : 0.8600 Average : 0.5393 YTW SCENARIO |

| IAG.PR.G | FixedReset | Quote: 22.83 – 23.50 Spot Rate : 0.6700 Average : 0.4298 YTW SCENARIO |

| PWF.PR.P | FixedReset | Quote: 14.54 – 15.18 Spot Rate : 0.6400 Average : 0.4217 YTW SCENARIO |

| MFC.PR.J | FixedReset | Quote: 22.05 – 22.65 Spot Rate : 0.6000 Average : 0.3945 YTW SCENARIO |

| CU.PR.D | Perpetual-Discount | Quote: 22.22 – 22.73 Spot Rate : 0.5100 Average : 0.3289 YTW SCENARIO |

| GWO.PR.N | FixedReset | Quote: 13.65 – 14.23 Spot Rate : 0.5800 Average : 0.4034 YTW SCENARIO |