No sooner had I delivered my crushing retort to my cashless friends than I became aware of a piece in the Globe by Ian McGugan titled Why central bankers would like to trash your cash:

An end to folding money could offer many advantages, according to Kenneth Rogoff, a Harvard professor and former chief economist at the International Monetary Fund. The most immediate payoffs would come from cracking down on drug traffickers and tax evaders.

This could have surprisingly large benefits for government coffers. In a column in the Financial Times this week, Prof. Rogoff estimates that untaxed, underground transactions account for 7 to 8 per cent of the U.S. economy and probably even more of its European counterpart. Bringing all those cash-only transactions into the light by forcing them to be conducted through the banking system, where the taxman could track them, would provide governments with a nice revenue boost.

…

One option, in theory, would be to impose negative interest rates – to apply a penalty charge on bank balances to spur people to spend. One big problem with this in practice, however, is that it just won’t work because “people will start bailing out into cash,” as Prof. Rogoff writes.But what if there was no cash? Government could then adjust rates however it wanted, even well into negative territory, to force people to stop sitting on their wealth.

A miracle has occurred! Competition is having an effect on underwriting fees … maybe!

With trading profits dwindling, more dealers than ever are fighting for assignments managing U.S. corporate-bond sales, one of the few bright spots in fixed income. Companies from the most-creditworthy to the most-indebted have been selling trillions of dollars of debt, locking in record-low borrowing costs ahead of the anticipated rise in interest rates.

…

A record 144 underwriters for the period have split an estimated $4.2 billion of fees on U.S. sales, the data show.

…

The five most-active corporate-debt underwriters this year landed 47 percent of the business, the smallest share on record. That’s down from 59 percent of the assignments for all of 2009.

…

Smaller firms see an opportunity to break into the business as Wall Street’s behemoths unload inventories of riskier securities in the face of higher capital requirements and limits imposed by the U.S. Dodd-Frank Act’s Volcker Rule on the amount of their own money they can use to trade.Royal Bank of Canada has climbed to 11th most-active underwriter of corporate bonds in the U.S., from 14th place in the period four years earlier, Bloomberg data show.

…

Debt underwriting fees among the nine-biggest banks were 5.8 percent lower in the first three months of 2014 from the same period last year, according to data compiled by Bloomberg Industries. The slump in fees outpaced a 2.6 percent drop in the volume of global corporate bond sales.

The article isn’t all that clear on actual fees. The fee drop among the nine-biggest firms outpaces the drop in total issuance, but the market share of the five-biggest has dropped considerably. It is conceivable that prices haven’t dropped at all and that the quoted differences are due the changes in volume, market share and product mix. But we can hope!

Tobias Adrian, Richard Crump, Benjamin Mills and Emanuel Moench have been working on the Treasury term premium:

Treasury yields can be decomposed into two components: expectations of the future path of short-term Treasury yields and the Treasury term premium. The term premium is the compensation that investors require for bearing the risk that short-term Treasury yields do not evolve as they expected. Studying the term premium over a long time period allows us to investigate what has historically driven changes in Treasury yields. In this blog post, we estimate and analyze the Treasury term premium from 1961 to the present, and make these estimates available for download here.

…

In a previous post, we compared our estimated term premium to a number of observable variables. We showed that the term premium is a countercyclical variable which tends to move with measures of uncertainty and disagreement about the future level of yields.

…

The evolution of term premia has been of particular interest since the Federal Reserve began large-scale asset purchases. Over this time, short-term interest rates have been close to zero, and our estimates show that the term premium has been compressed and has at times even been negative. An advantage of our estimate is that it is available back to 1961. Hence, we can study the term premium at another time when short-term interest rates were close to zero. By comparing the ten-year ACM term premium of the past decade to that of the 1960s in the first chart, we find that the ten-year term premium was negative at times in the 1960s, but reverted back to positive. Similarly, our estimate of the term premium has risen above zero recently.Daily estimates of the ACM term premium from 1961 to the present are now available for download from the Data & Indicators section of the New York Fed’s website. The data are updated weekly and include estimates of the term premium for yearly Treasury maturities from one to ten years, as well as fitted yields and the expected average level of short-term interest rates.

I get lots of ‘friend’ requests on LinkedIn and Facebook from people whose names I don’t recognize. If I don’t recognize the name, I don’t respond; to me, that sounds basic. Some people disagree:

In an unprecedented, three-year cyber espionage campaign, Iranian hackers created false social networking accounts and a fake news website to spy on military and political leaders in the United States, Israel and other countries, a cyber intelligence firm said on Thursday.

ISight Partners, which uncovered the operation, said the hackers’ targets include a four-star U.S. Navy admiral, U.S. lawmakers and ambassadors, members of the U.S.-Israeli lobby, and personnel from Britain, Saudi Arabia, Syria, Iraq and Afghanistan.

…

The hackers set up false accounts on Facebook and other online social networks for these 14 personas, populated their profiles with fictitious personal content, and then tried to befriend target victims, according to iSight.

…

To build credibility, the hackers would approach high-value targets by first establishing ties with the victims’ friends, classmates, colleagues, relatives and other connections over social networks run by Facebook Inc., Google Inc. and its YouTube, LinkedIn Corp. and Twitter Inc.The hackers would initially send the targets content that was not malicious, such as links to news articles on NewsOnAir.org, in a bid to establish trust. Then they would send links that infected PCs with malicious software, or direct targets to web portals that ask for network log-in credentials, iSight said.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 20bp, FixedResets up 10bp and DeemedRetractibles gaining 1bp. The Performance Highlights table is of above-average length, with a preponderance of FixedReset issues on the winning side, bouncing back a bit from Friday‘s carnage. Volume was below average.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.7656 % | 2,513.7 |

| FixedFloater | 4.52 % | 3.77 % | 32,676 | 17.85 | 1 | 0.0000 % | 3,795.5 |

| Floater | 2.90 % | 3.03 % | 47,845 | 19.60 | 4 | 0.7656 % | 2,714.1 |

| OpRet | 4.38 % | -13.95 % | 31,765 | 0.09 | 2 | 0.0195 % | 2,710.5 |

| SplitShare | 4.82 % | 4.10 % | 62,358 | 4.16 | 5 | -0.1828 % | 3,112.5 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0195 % | 2,478.5 |

| Perpetual-Premium | 5.51 % | -5.26 % | 85,724 | 0.09 | 17 | -0.0438 % | 2,403.6 |

| Perpetual-Discount | 5.26 % | 5.26 % | 104,570 | 15.00 | 20 | -0.1965 % | 2,545.7 |

| FixedReset | 4.55 % | 3.73 % | 214,927 | 8.77 | 74 | 0.0995 % | 2,519.9 |

| Deemed-Retractible | 5.02 % | 2.20 % | 156,423 | 0.16 | 43 | 0.0149 % | 2,519.7 |

| FloatingReset | 2.67 % | 2.51 % | 142,182 | 3.99 | 6 | 0.0597 % | 2,482.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ELF.PR.G | Perpetual-Discount | -1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 21.76 Evaluated at bid price : 22.15 Bid-YTW : 5.42 % |

| PWF.PR.S | Perpetual-Discount | -1.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 23.14 Evaluated at bid price : 23.45 Bid-YTW : 5.16 % |

| RY.PR.Z | FixedReset | 1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 23.30 Evaluated at bid price : 25.45 Bid-YTW : 3.62 % |

| CU.PR.D | Perpetual-Discount | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 24.02 Evaluated at bid price : 24.42 Bid-YTW : 5.02 % |

| BAM.PR.R | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 23.69 Evaluated at bid price : 25.35 Bid-YTW : 3.92 % |

| IFC.PR.A | FixedReset | 2.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.88 Bid-YTW : 4.25 % |

| PWF.PR.A | Floater | 2.51 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 20.04 Evaluated at bid price : 20.04 Bid-YTW : 2.63 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| CM.PR.K | FixedReset | 86,855 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.29 Bid-YTW : 1.18 % |

| CM.PR.M | FixedReset | 86,080 | Called for redemption. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-31 Maturity Price : 25.00 Evaluated at bid price : 25.39 Bid-YTW : 0.51 % |

| SLF.PR.H | FixedReset | 84,905 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 3.75 % |

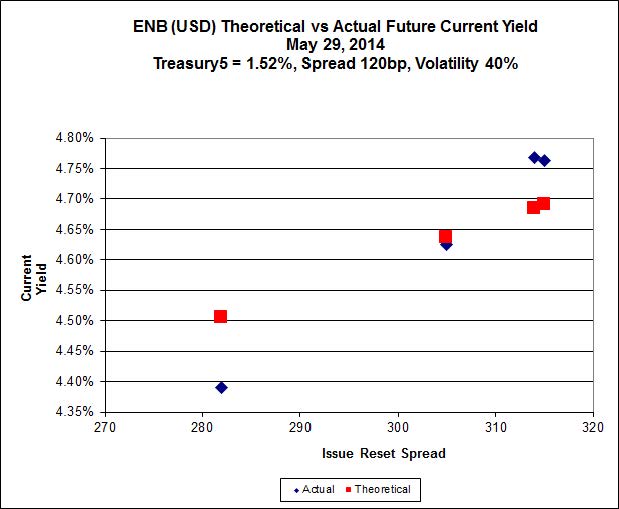

| ENB.PF.C | FixedReset | 81,159 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 23.10 Evaluated at bid price : 24.95 Bid-YTW : 4.17 % |

| CU.PR.E | Perpetual-Discount | 41,865 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-02 Maturity Price : 23.66 Evaluated at bid price : 24.03 Bid-YTW : 5.11 % |

| BMO.PR.P | FixedReset | 38,843 | YTW SCENARIO Maturity Type : Call Maturity Date : 2015-02-25 Maturity Price : 25.00 Evaluated at bid price : 25.60 Bid-YTW : 2.23 % |

| There were 25 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| MFC.PR.K | FixedReset | Quote: 24.60 – 25.00 Spot Rate : 0.4000 Average : 0.2562 YTW SCENARIO |

| TD.PR.R | Deemed-Retractible | Quote: 26.35 – 26.59 Spot Rate : 0.2400 Average : 0.1556 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 24.30 – 24.60 Spot Rate : 0.3000 Average : 0.2186 YTW SCENARIO |

| MFC.PR.L | FixedReset | Quote: 24.60 – 24.89 Spot Rate : 0.2900 Average : 0.2121 YTW SCENARIO |

| CU.PR.E | Perpetual-Discount | Quote: 24.03 – 24.54 Spot Rate : 0.5100 Average : 0.4379 YTW SCENARIO |

| ELF.PR.G | Perpetual-Discount | Quote: 22.15 – 22.38 Spot Rate : 0.2300 Average : 0.1591 YTW SCENARIO |