Guillermo Calvo of Columbia University writes an interesting piece for VoxEU, Dumping Russia in 1998 and Lehman ten years later: Triple time-inconsistency episodes:

This column introduces “triple time-inconsistent” episodes. First, a public institution is expected to cave in and offer a bailout to prevent a crisis. Then, in an attempt to regain credibility, it pulls back. Finally, it resumes bailing out the survivors of the wreckage caused by the policy surprise. This column characterises the 1998 Russian crisis and the current crisis as triple time-inconsistency episodes and says that a financial crisis may simply be a bad time to try to build credibility.

…

It is far from me to chastise or ridicule those involved in triple time inconsistency. There are always good reasons why bright and well-intentioned public officials make serious mistakes during major crises. The two cases singled out in this note took place in arguably “unprecedented” circumstances. In situations like these, “shooting from the hip” becomes the rule, and errors are to be expected. However, I believe that there are at least two lessons that we could draw from these episodes, which could help to lower the incidence of triple time inconsistency and other inefficiencies:

- •A financial crisis is not the best time for reform or building credibility, especially if those actions go against the private sector’s expectations. Policymakers should focus their attention on putting out the fires and minimise the short-run social costs.

- •Policymakers should spend more time discussing worst-case scenarios before crises occur. These discussions should be carried out with some regularity (much like fire drills) and involve a wide spectrum of public officials that might eventually have to be involved in rescue operations during crisis. This will ensure a better understanding of the involved risks and tradeoffs, and improve the effectiveness of policies that need to be implemented in the spur of a moment.

Fat chance of the second one! When was the last time you saw a ten-year government deficit projection that included a discussion of the projected effects of a severe recession?

CIT is going to defer interest payments on its sub-debt:

Commercial lender CIT Group Inc. said in a regulatory filing Tuesday it will defer interest payments on some outstanding junior notes.

CIT was to make the next interest payment on the junior notes on Sept. 15, according to the Securities and Exchange Commission filing. The deferred interest will continue to accrue and compound until payments are made, the company said.

Interest is being deferred on junior subordinated notes due March 15, 2067.

Deferring interest payments can help CIT Group continue to reduce its near-term debt burden, furthering its efforts to remain in business after nearly collapsing earlier in the year.

The SEC filing on CIT’s site is copy-protected – idiots.

The Boston Fed has published an interesting paper by Katharine Bradbury and Jane Katz, Trends in U.S. Family Income Mobility, 1967-2004:

Using data from the Panel Study of Income Dynamics and a number of mobility concepts and measures drawn from the literature, we examine mobility levels and trends for U.S. working-age families, overall and by race, during the time span 1967–2004. By most measures, we find that mobility is lower in more recent periods (the 1990s into the early 2000s) than in earlier periods (the 1970s). Most notably, mobility of families starting near the bottom has worsened over time. However, in recent years, the down-trend in mobility is more or less pronounced (or even non-existent) depending on the measure, although a decrease in the frequency with which panel data on family incomes are gathered makes it difficult to draw firm conclusions. Measured relative to the overall distribution or in absolute terms, black families exhibit substantially less mobility than whites in all periods; their mobility decreased between the 1970s and the 1990s, but no more than that of white families, although they lost ground in terms of relative income.

Taken together, this evidence suggests that over the 1967-to-2004 time span, a low-income family’s probability of moving up decreased, families’ later year incomes increasingly depended on their starting place, and the distribution of families’ lifetime incomes became less equal.

It should be noted, however, that:

We do not address shorter‐term “volatility”—shocks to family incomes from year to year—or longer‐term “intergenerational mobility”—how much a person’s adult family income level (or position) depends on the level (position) of his/her parents during childhood.

This is a shame, because it the latter measure that I find to be of most interest. The authors conclude, in part:

What are the implications for policy? Because we find no evidence to suggest that the typical poor family is more likely to move up and out of poverty within several years than it was 40 years ago, policy remedies for those at the bottom should aim beyond short‐term help, as the poor at any point in time are likely to have low long‐term incomes. Beyond short‐term relief, the choice of policy presumably hinges, at least in part, on the reasons for the decline in mobility, for example, whether it reflects rising barriers to opportunity or rising returns to highstakes labor market promotion practices, including tournament‐style regimes common in the professions.

I’m not sure how to take this report. It sees to me that the results could come from increased efficiency in determining the starting point – e.g., you get that good job right out of school instead of having to pay your dues for twenty years and waiting for your supervisor to die. As I noted, I am far more concerned by inter-generational income mobility.

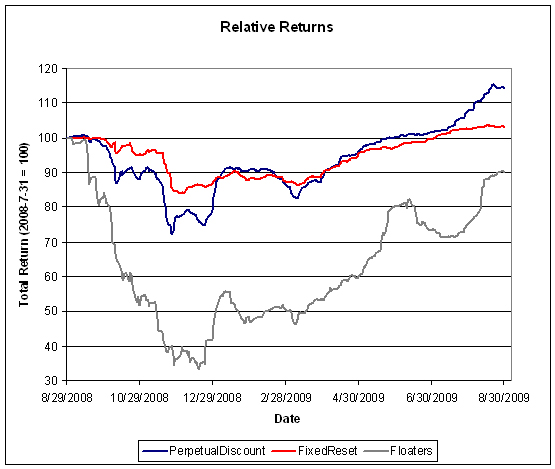

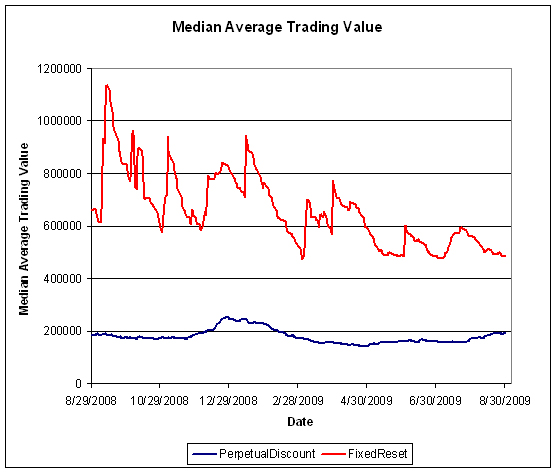

Volume picked up a little today, but the market didn’t, really, with PerpetualDiscounts down 19bp and FixedResets up 5bp. Just to make things more confusing, PerpetualPremiums were up 11bp … geez, it’s nice to see a healthy population in that slot!

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.7311 % |

1,446.6 |

| FixedFloater |

5.72 % |

4.00 % |

61,030 |

18.60 |

1 |

-0.0526 % |

2,683.1 |

| Floater |

2.52 % |

2.15 % |

32,002 |

22.07 |

4 |

-0.7311 % |

1,807.2 |

| OpRet |

4.86 % |

-13.60 % |

128,783 |

0.09 |

15 |

0.0765 % |

2,281.9 |

| SplitShare |

6.42 % |

6.55 % |

1,244,765 |

4.08 |

2 |

-0.5063 % |

2,061.2 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0765 % |

2,086.6 |

| Perpetual-Premium |

5.73 % |

5.34 % |

152,079 |

2.55 |

12 |

0.1083 % |

1,890.0 |

| Perpetual-Discount |

5.68 % |

5.69 % |

194,740 |

14.36 |

59 |

-0.1854 % |

1,809.1 |

| FixedReset |

5.50 % |

4.01 % |

478,982 |

4.11 |

40 |

0.0480 % |

2,105.2 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| SLF.PR.B |

Perpetual-Discount |

-1.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 20.88

Evaluated at bid price : 20.88

Bid-YTW : 5.76 % |

| TRI.PR.B |

Floater |

-1.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 2.09 % |

| CM.PR.P |

Perpetual-Discount |

-1.44 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 22.94

Evaluated at bid price : 24.00

Bid-YTW : 5.75 % |

| CM.PR.E |

Perpetual-Discount |

-1.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 24.11

Evaluated at bid price : 24.40

Bid-YTW : 5.80 % |

| SLF.PR.C |

Perpetual-Discount |

-1.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 19.51

Evaluated at bid price : 19.51

Bid-YTW : 5.71 % |

| CM.PR.R |

OpRet |

-1.19 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2009-10-01

Maturity Price : 25.60

Evaluated at bid price : 26.46

Bid-YTW : -28.10 % |

| BMO.PR.K |

Perpetual-Discount |

-1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 23.21

Evaluated at bid price : 23.38

Bid-YTW : 5.65 % |

| BNS.PR.J |

Perpetual-Discount |

-1.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 22.62

Evaluated at bid price : 23.54

Bid-YTW : 5.60 % |

| BNA.PR.D |

SplitShare |

-1.08 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2014-07-09

Maturity Price : 25.00

Evaluated at bid price : 25.75

Bid-YTW : 6.55 % |

| BAM.PR.N |

Perpetual-Discount |

-1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 18.34

Evaluated at bid price : 18.34

Bid-YTW : 6.61 % |

| BNS.PR.N |

Perpetual-Discount |

-1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 23.38

Evaluated at bid price : 23.56

Bid-YTW : 5.64 % |

| CIU.PR.B |

FixedReset |

1.05 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-07-01

Maturity Price : 25.00

Evaluated at bid price : 28.00

Bid-YTW : 4.01 % |

| NA.PR.L |

Perpetual-Discount |

1.60 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 21.65

Evaluated at bid price : 21.65

Bid-YTW : 5.66 % |

| BAM.PR.I |

OpRet |

1.80 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2009-10-01

Maturity Price : 25.75

Evaluated at bid price : 26.02

Bid-YTW : 3.65 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| TD.PR.E |

FixedReset |

242,062 |

TD crossed two blocks, 100,000 and 123,500 shares, both at 27.65. Nice tickets!

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-30

Maturity Price : 25.00

Evaluated at bid price : 27.65

Bid-YTW : 3.96 % |

| BAM.PR.P |

FixedReset |

50,620 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-10-30

Maturity Price : 25.00

Evaluated at bid price : 26.52

Bid-YTW : 6.05 % |

| BAM.PR.B |

Floater |

46,079 |

TD crossed 20,000 at 12.60.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 12.52

Evaluated at bid price : 12.52

Bid-YTW : 3.17 % |

| BAM.PR.N |

Perpetual-Discount |

43,059 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 18.34

Evaluated at bid price : 18.34

Bid-YTW : 6.61 % |

| SLF.PR.C |

Perpetual-Discount |

39,733 |

Scotia crossed 20,200 at 19.50.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2039-09-01

Maturity Price : 19.51

Evaluated at bid price : 19.51

Bid-YTW : 5.71 % |

| CM.PR.L |

FixedReset |

34,757 |

RBC crossed 23,000 at 27.80.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2014-05-30

Maturity Price : 25.00

Evaluated at bid price : 27.71

Bid-YTW : 4.15 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. |