On April 15 I mentioned the Lortie attack on unbundled fees; now Rob Carrick of the Globe pens an essay attacking the report’s conclusions:

Investors, you’ll be fine. Already, a new generation of advisers is emerging to serve clients of any wealth level, rich or not, experienced investor or beginner. These online advisers, also called robo-advisers, provide an effective retirement savings foundation. First, they find an appropriate mix of stocks, bonds and cash for your needs, then they build a simple portfolio using exchange-traded funds. Fees are clearly displayed and paid upfront by investors.

…

The early narrative on online advisers was that they were primarily something for millennials. However, some firms operating in the Canadian market say their average client age is between 40 and 50. Online advisers themselves are diverse – some are simply about helping you invest intelligently, while at least one is building a specialty in retirement income planning.

This repeats the assumption of the unbundlers that every small investor now served by an advisor will, after such a change is enacted, rush right out and sign up with an on-line service. I’m not convinced of that. Remember the adage ‘mutual funds are sold, not bought’? There’s a lot of truth in that.

There is a great swath of people who don’t decide that they’ve got to do something about their savings plan and then do it. I suggest that there is a huge population of (mainly) small investors, who are aware they ought to be doing something (this is a result of all the generic advertising done by the fund and advice companies) and finally decide … ‘Frank at the club does stocks and bonds. I’ll talk to Frank next time I see him.’ So he talks to Frank and Frank gets another little client and the client gets an equity allocation in his portfolio that wouldn’t have been there otherwise.

With unbundling, a lot of that generic advertising is going to disappear (unless the selfless population of self-styled investor advocates puts some actual time and money on the table to pick up the slack. Ha-ha.) and Frank at the club will go start driving for Uber instead. The money will remain in a package of GICs at the bank; the banks, of course, have no problem with this change because guess what? They’ve got a full time captive sales force and distribution channels out the wazoo! So the change will be a competitive advantage for the banks, which is why the regulators are promoting the idea.

OK, so maybe I’m wrong on this. I’m not an investor advocate, I’m willing to accept that sometimes my gut reaction might be wrong. But that gets us to what really bothers me about the whole deal: it’s not necessary. Fee bundling has been banned in the UK and market adjustments are proceeding there. Why don’t we just put this idea on the back burner for ten years and see what happens in Britain?

Such an approach involves things like ‘evidence’, however, and the regulators don’t like that sort of crap.

On another note, OSFI Deputy Superintendent Mark Zelmer gave a speech titled A New Chapter in Life Insurance Capital Requirements:

I will then briefly explain how the draft LICAT guideline compares at a high level with the Solvency II insurance capital framework recently introduced in Europe, and the new international capital standard that is currently under construction by the International Association of Insurance Supervisors (IAIS).

…

When the MCCSR was first introduced it was an international pioneer in many respects in applying a risk-based solvency framework to life insurers. Newer frameworks like Solvency II in Europe have gone further in this respect, and our development of the draft LICAT guideline has certainly benefitted from lessons learned in the construction of those frameworks. Indeed, newer insurance capital frameworks around the world are generally converging towards more sophisticated risk-based frameworks. Thus, it is no surprise that the LICAT is largely consistent with Solvency II and the proposed new Insurance Capital Standard (ICS) currently being developed by the IAIS.Important differences remain. Nowhere is that more apparent than in how different capital frameworks handle the current environment of exceptionally low interest rates and interest rate volatility more generally. One notable approach is the US capital framework, where Pillar 1 regulatory capital requirements and available capital only adjust to interest rate movements when insurance liabilities and their supporting assets mature and are replaced with new assets and liabilities. Another important point of reference is Solvency II, where initial versions of that regulatory capital framework were very sensitive to interest rates due to their heavier reliance on fair-valuation of cash flows on both sides of the balance sheet. However, more recent versions now include several measures that serve to mitigate excessive volatility in regulatory capital positions.

The parallels with Solvency II are important – Solvency II imposes the NVCC rule on insurers!

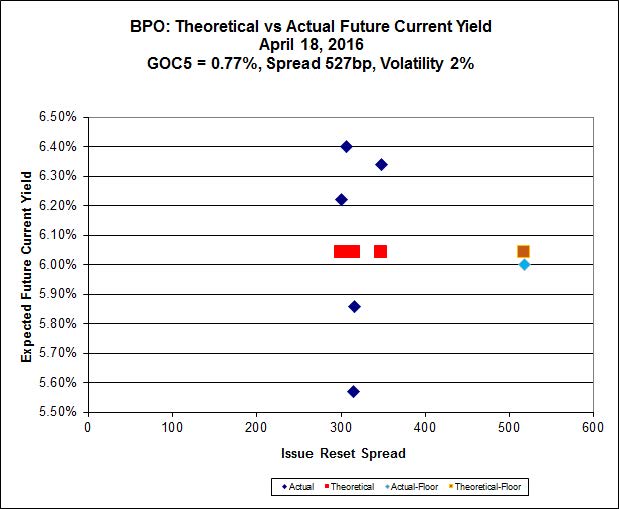

And here’s another bare-bones market report. I’m sorry about this, guys, but I’m really busy!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.69 % | 5.71 % | 10,592 | 17.00 | 1 | -0.6897 % | 1,675.4 |

| FixedFloater | 6.55 % | 5.67 % | 19,948 | 16.95 | 1 | 0.0000 % | 3,084.7 |

| Floater | 4.42 % | 4.59 % | 54,065 | 16.26 | 4 | 3.0071 % | 1,755.5 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1013 % | 2,810.5 |

| SplitShare | 4.71 % | 4.98 % | 82,640 | 2.53 | 6 | 0.1013 % | 3,288.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.1013 % | 2,566.1 |

| Perpetual-Premium | 5.78 % | -10.65 % | 83,145 | 0.09 | 6 | -0.0197 % | 2,591.5 |

| Perpetual-Discount | 5.56 % | 5.60 % | 95,179 | 14.48 | 33 | 0.1076 % | 2,627.6 |

| FixedReset | 5.15 % | 4.69 % | 180,045 | 14.06 | 88 | -0.2800 % | 1,983.5 |

| Deemed-Retractible | 5.18 % | 5.50 % | 128,414 | 5.08 | 34 | 0.0559 % | 2,639.1 |

| FloatingReset | 3.15 % | 4.86 % | 29,845 | 5.35 | 17 | -0.0296 % | 2,068.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| GWO.PR.O | FloatingReset | -5.28 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 12.02 Bid-YTW : 11.31 % |

| PWF.PR.T | FixedReset | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 20.40 Evaluated at bid price : 20.40 Bid-YTW : 4.06 % |

| MFC.PR.M | FixedReset | -1.91 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.05 Bid-YTW : 6.57 % |

| BNS.PR.Q | FixedReset | -1.85 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.76 Bid-YTW : 4.75 % |

| BNS.PR.D | FloatingReset | -1.83 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.75 Bid-YTW : 6.81 % |

| BAM.PF.E | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 18.67 Evaluated at bid price : 18.67 Bid-YTW : 4.80 % |

| BAM.PR.X | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 14.23 Evaluated at bid price : 14.23 Bid-YTW : 4.78 % |

| BMO.PR.M | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 23.57 Bid-YTW : 4.06 % |

| TD.PF.A | FixedReset | -1.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 18.97 Evaluated at bid price : 18.97 Bid-YTW : 4.21 % |

| BAM.PF.A | FixedReset | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 19.13 Evaluated at bid price : 19.13 Bid-YTW : 4.99 % |

| HSE.PR.B | FloatingReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 9.65 Evaluated at bid price : 9.65 Bid-YTW : 5.84 % |

| MFC.PR.H | FixedReset | -1.29 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.35 Bid-YTW : 6.25 % |

| BAM.PF.H | FixedReset | -1.28 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2020-12-31 Maturity Price : 25.00 Evaluated at bid price : 25.50 Bid-YTW : 4.61 % |

| BNS.PR.Z | FixedReset | -1.27 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.25 Bid-YTW : 6.02 % |

| HSE.PR.C | FixedReset | -1.20 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 17.29 Evaluated at bid price : 17.29 Bid-YTW : 5.90 % |

| MFC.PR.J | FixedReset | -1.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.75 Bid-YTW : 6.84 % |

| RY.PR.K | FloatingReset | 1.07 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.19 Bid-YTW : 4.56 % |

| BAM.PF.C | Perpetual-Discount | 1.13 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 20.58 Evaluated at bid price : 20.58 Bid-YTW : 5.96 % |

| TRP.PR.E | FixedReset | 1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 17.87 Evaluated at bid price : 17.87 Bid-YTW : 4.68 % |

| FTS.PR.H | FixedReset | 1.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 13.50 Evaluated at bid price : 13.50 Bid-YTW : 4.28 % |

| TRP.PR.B | FixedReset | 1.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 11.50 Evaluated at bid price : 11.50 Bid-YTW : 4.55 % |

| VNR.PR.A | FixedReset | 1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 18.25 Evaluated at bid price : 18.25 Bid-YTW : 5.02 % |

| BAM.PR.B | Floater | 1.66 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 10.39 Evaluated at bid price : 10.39 Bid-YTW : 4.59 % |

| TD.PF.D | FixedReset | 1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 20.35 Evaluated at bid price : 20.35 Bid-YTW : 4.40 % |

| BAM.PR.C | Floater | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 10.24 Evaluated at bid price : 10.24 Bid-YTW : 4.65 % |

| BAM.PR.K | Floater | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 10.30 Evaluated at bid price : 10.30 Bid-YTW : 4.63 % |

| PWF.PR.A | Floater | 5.77 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 4.00 % |

| TRP.PR.I | FloatingReset | 5.83 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 11.25 Evaluated at bid price : 11.25 Bid-YTW : 4.54 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TRP.PR.J | FixedReset | 220,394 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-31 Maturity Price : 25.00 Evaluated at bid price : 25.61 Bid-YTW : 4.99 % |

| RY.PR.Q | FixedReset | 181,975 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-05-24 Maturity Price : 25.00 Evaluated at bid price : 25.90 Bid-YTW : 4.61 % |

| RY.PR.R | FixedReset | 147,023 | YTW SCENARIO Maturity Type : Call Maturity Date : 2021-08-24 Maturity Price : 25.00 Evaluated at bid price : 26.18 Bid-YTW : 4.67 % |

| MFC.PR.N | FixedReset | 53,130 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.92 Bid-YTW : 6.60 % |

| FTS.PR.M | FixedReset | 51,615 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2046-04-21 Maturity Price : 19.10 Evaluated at bid price : 19.10 Bid-YTW : 4.54 % |

| IFC.PR.C | FixedReset | 50,508 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 17.94 Bid-YTW : 8.08 % |

| There were 17 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.O | FloatingReset | Quote: 12.02 – 13.50 Spot Rate : 1.4800 Average : 0.9763 YTW SCENARIO |

| BNS.PR.Q | FixedReset | Quote: 22.76 – 23.25 Spot Rate : 0.4900 Average : 0.2967 YTW SCENARIO |

| HSE.PR.E | FixedReset | Quote: 19.30 – 19.99 Spot Rate : 0.6900 Average : 0.5067 YTW SCENARIO |

| PWF.PR.T | FixedReset | Quote: 20.40 – 21.10 Spot Rate : 0.7000 Average : 0.5181 YTW SCENARIO |

| RY.PR.K | FloatingReset | Quote: 22.19 – 23.00 Spot Rate : 0.8100 Average : 0.6431 YTW SCENARIO |

| HSE.PR.B | FloatingReset | Quote: 9.65 – 10.49 Spot Rate : 0.8400 Average : 0.6827 YTW SCENARIO |