Click for Big

The markets were highly relieved today to learn that coronavirus is no longer considered a Democrat/Media plot:

The stock market roared back to life on Friday, with the S&P surging 9.3 percent after President Trump said the government would speed up coronavirus testing for Americans. In doing so, he delivered investors exactly the message they had been waiting to hear — a half-hour before the market closed.

Just one day after tumbling 9.5 percent in what was its worst day in more than 30 years, the S&P 500 stock index rose by roughly the same amount. The market was up throughout the day, then dipped when the president started speaking, only to change direction once he began discussing the administration’s efforts to speed testing. Millions of virus testing kits would become available, he said — though he added that he did not think so many would be needed.

For investors starved for reassuring news, those promises were enough to ignite a rally that sent the S&P 500 to its best one-day performance since 2008.

This had an effect:

Canada’s main stock market notched on Friday its biggest gain since October 2008, as Canada ramped up stimulus to ease the economic impact of the coronavirus outbreak, while the Canadian dollar edged higher after hitting an earlier four-year low.

The Bank of Canada unexpectedly cut its overnight rate by 50 basis points to 0.75%, its second half-point cut in nine days, and the government said it would offer $10-billion in credit support to businesses.

…

The Toronto Stock Exchange Composite Index, was up 8% at 13,520.53, recovering some ground after a record decline on Thursday. For the week, the index was on track to fall about 15%, its biggest drop in Refinitiv Eikon data going back to July 1979.Nine of the TSX’s 10 main groups were higher, led by a 10.1% gain for the heavily-weighted financial services sector, while energy was up 5.6%.

The price of oil, one of Canada’s major exports, had its biggest weekly slide since the 2008 financial crisis despite settling 0.7% higher on Friday, as the coronavirus outbreak threatened demand and crude producers promised more supply.

…

The Canadian dollar was trading 0.1% higher at 1.3912 to the greenback, or 71.88 U.S. cents, having touched its weakest intraday level since February 2016 at 1.3996.Canadian government bond yields rose across a steeper yield curve, with the 10-year yield up 16.1 basis points at 0.754%. On Monday, the 10-year yield hit a record low at 0.233%.

In New York, the Dow Jones industrial average was up 1,985.00 points at 23,185.62. The S&P 500 index was up 230.38 points at 2,711.02, while the Nasdaq composite was up 673.07 points at 7,874.88.

U.S. 10-year Treasury yields jumped back over the 1% level on Friday after President Donald Trump declared a national emergency over the spreading coronavirus, a move that sent stocks soaring.

The 10-year note yield, which was at 0.934% before the president’s Rose Garden address, rose to 1.019%, up from 0.852% at Thursday’s close.

Finance Minister Bill Morneau announced that $10-billion of immediate credit will be available to Canadian businesses impacted by the coronavirus through Ottawa’s Business Development Bank and Export Development Canada

He also promised to unveil a “significant stimulus package” next week, well before the March 30 federal budget.

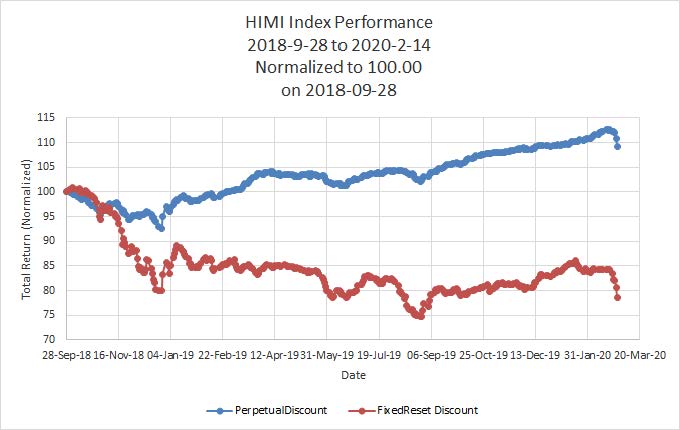

TXPR closed at 473.71, down 0.91% on the day. Volume today was 4.92-million, third-highest of the past thirty days, behind March 9 and March 10.

CPD closed at 9.45, down 0.63% on the day. Volume of 653,463 was the highest of the past thirty days, well ahead of second-place March 9.

ZPR closed at 7.32, up 0.55% on the day. Volume of 1,384,125 was only the fourth-highest of the past week.

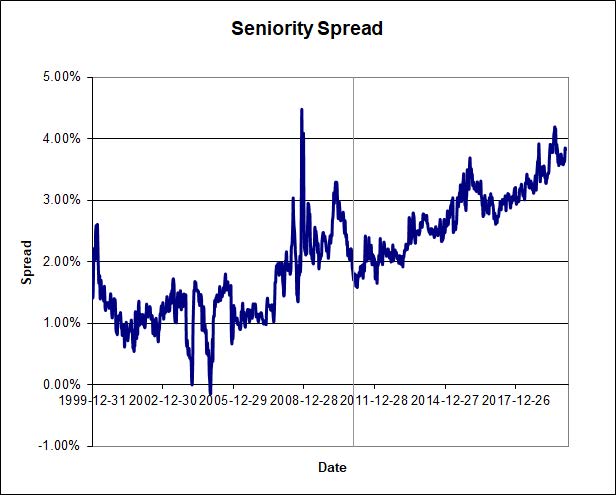

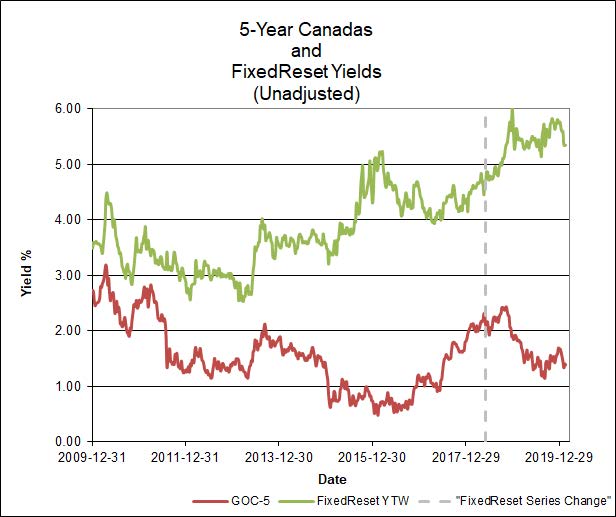

Five-year Canada yields were up 20bp to 0.67% today. Which sounds like an odd reaction to a Bank of Canada rate cut, but things have become so distorted in the past three weeks that unsnarling the mess will be a puzzle in itself.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading< br>Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.0 0 |

0 | 0.4627 % | 1,460.4 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.4627 % | 2,679.8 |

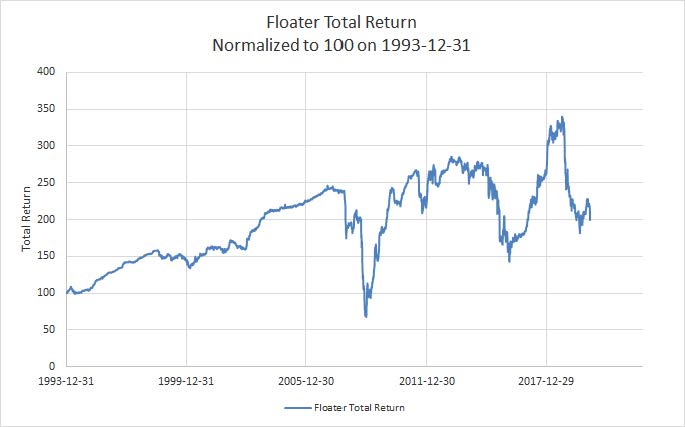

| Floater | 7.41 % | 7.43 % | 56,030 | 12.06 | 4 | 0.4627 % | 1,544.4 |

| OpRet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9327 % | 3,359.7 |

| SplitShare | 4.94 % | 5.49 % | 66,404 | 4.04 | 7 | 0.9327 % | 4,012.2 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.9327 % | 3,130.5 |

| Perpetu al-Premium |

6.28 % | 6.42 % | 89,931 | 13.22 | 12 | -0.3958 % | 2,714.5 |

| Perpetual-Discount | 6.06 % | 6 .05 % |

76,054 | 13.77 | 24 | -1.1134 % | 2,889.8 |

| FixedReset Disc | 7.71 % | 6.35 % | 206,984 | 12.92 | 64 | -1.8543 % | 1,560.6 |

| Deemed-Retractible | 5.95 % | 6.39 % | 86,545 | 13.40 | 27 | -1.8946 % | 2,842.0 |

| FloatingReset | 6.32 % | 6.17 % | 68,306 | 13.59 | 3 | -1.9252 % | 1,659.6 |

| FixedReset Prem | 6.09 % | 5.96 % | 169,081 | 13.87 | 22 | -0.6358 % | 2,227.4 |

| FixedReset Bank Non | 2.16 % | 10.48 % | 106,180 | 1.80 | 3 | 2.3444 % | 2,461.9 |

| FixedReset Ins Non | 7.71 % | 6.67 % | 112,472 | 12.78 | 22 | -3.1876 % | 1,541.9 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| TRP.PR.C | FixedReset Disc | -14.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 7.07 Evaluated at bid price : 7.07 Bid-YTW : 7.57 % |

| NA.PR.G | FixedReset Disc | -12.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.38 Evaluated at bid price : 12.38 Bid-YTW : 7.68 % |

| HSE.PR.G | FixedReset Disc | -8.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 9.35 Evaluated at bid price : 9.35 Bid-YTW : 11.33 % |

| PWF.PR.P | FixedReset Disc | -7.78 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 8.30 Evaluated at bid price : 8.30 Bid-YTW : 6.61 % |

| IFC.PR.G | FixedReset Ins Non | -7.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.55 Evaluated at bid price : 13.55 Bid-YTW : 6.43 % |

| TRP.PR.F | FloatingReset | -7.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 8.98 Evaluated at bid price : 8.98 Bid-YTW : 7.01 % |

| BAM.PR.R | FixedReset Disc | -6.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 10.79 Evaluated at bid price : 10.79 Bid-YTW : 6.66 % |

| MFC.PR.I | FixedReset Ins Non | -6.67 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.59 Evaluated at bid price : 12.59 Bid-YTW : 7.14 % |

| EMA.PR.H | FixedReset Prem | -6.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.44 Evaluated at bid price : 21.44 Bid-YTW : 5.79 % |

| BIP.PR.B | FixedReset Prem | -6.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 7.27 % |

| MFC.PR.N | FixedReset Ins Non | -6.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 11.40 Evaluated at bid price : 11.40 Bid-YTW : 6.30 % |

| BIP.PR.C | FixedReset Prem | -6.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.65 Evaluated at bid price : 18.65 Bid-YTW : 7.21 % |

| PWF.PR.S | Perpetual-Discount | -6.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 6.51 % |

| GWO.PR.R | Deemed-Retractible | -5.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 6.39 % |

| BAM.PF.G | FixedReset Disc | -5.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.36 Evaluated at bid price : 13.36 Bid-YTW : 6.37 % |

| CU.PR.E | Perpetual-Discount | -5.48 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 6.19 % |

| TRP.PR.E | FixedReset Disc | -5.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 10.96 Evaluated at bid price : 10.96 Bid-YTW : 7.37 % |

| CM.PR.Q | FixedReset Disc | -5.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.40 Evaluated at bid price : 12.40 Bid-YTW : 6.88 % |

| MFC.PR.L | FixedReset Ins Non | -5.03 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 10.95 Evaluated at bid price : 10.95 Bid-YTW : 6.91 % |

| CU.PR.C | FixedReset Disc | -4.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.79 Evaluated at bid price : 13.79 Bid-YTW : 5.50 % |

| SLF.PR.E | Deemed-Retractible | -4.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.65 Evaluated at bid price : 17.65 Bid-YTW : 6.40 % |

| BAM.PF.E | FixedReset Disc | -4.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.64 Evaluated at bid price : 12.64 Bid-YTW : 6.16 % |

| SLF.PR.B | Deemed-Retractible | -4.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.12 Evaluated at bid price : 19.12 Bid-YTW : 6.30 % |

| MFC.PR.M | FixedReset Ins Non | -4.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 11.78 Evaluated at bid price : 11.78 Bid-YTW : 6.79 % |

| EMA.PR.C | FixedReset Disc | -4.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.70 Evaluated at bid price : 14.70 Bid-YTW : 6.07 % |

| BIP.PR.D | FixedReset Disc | -4.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.60 Evaluated at bid price : 17.60 Bid-YTW : 7.14 % |

| POW.PR.D | Perpetual-Discount | -4.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.00 Evaluated at bid price : 20.00 Bid-YTW : 6.37 % |

| GWO.PR.S | Deemed-Retractible | -3.99 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 6.44 % |

| CM.PR.S | FixedReset Disc | -3.85 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.25 Evaluated at bid price : 13.25 Bid-YTW : 6.34 % |

| MFC.PR.H | FixedReset Ins Non | -3.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.52 Evaluated at bid price : 13.52 Bid-YTW : 7.01 % |

| SLF.PR.D | Deemed-Retractible | -3.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.70 Evaluated at bid price : 17.70 Bid-YTW : 6.31 % |

| BAM.PF.B | FixedReset Disc | -3.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.52 Evaluated at bid price : 13.52 Bid-YTW : 6.49 % |

| PWF.PR.F | Perpetual-Discount | -3.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.28 Evaluated at bid price : 20.28 Bid-YTW : 6.58 % |

| IAF.PR.I | FixedReset Ins Non | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.34 Evaluated at bid price : 13.34 Bid-YTW : 6.76 % |

| MFC.PR.C | Deemed-Retractible | -3.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.97 Evaluated at bid price : 17.97 Bid-YTW : 6.30 % |

| PWF.PR.L | Perpetual-Discount | -3.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.68 Evaluated at bid price : 19.68 Bid-YTW : 6.59 % |

| TD.PF.E | FixedReset Disc | -3.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.53 Evaluated at bid price : 14.53 Bid-YTW : 5.99 % |

| MFC.PR.O | FixedReset Ins Non | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.24 Evaluated at bid price : 21.24 Bid-YTW : 6.55 % |

| MFC.PR.J | FixedReset Ins Non | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 6.66 % |

| SLF.PR.I | FixedReset Ins Non | -3.32 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.81 Evaluated at bid price : 12.81 Bid-YTW : 6.54 % |

| MFC.PR.K | FixedReset Ins Non | -3.28 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 6.70 % |

| PVS.PR.G | SplitShare | -3.21 % | YTW SCENARIO Maturity Type : Option Certainty Maturity Date : 2026-02-28 Maturity Price : 25.00 Evaluated at bid price : 24.10 Bid-YTW : 5.67 % |

| POW.PR.G | Perpetual-Premium | -3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.61 Evaluated at bid price : 21.61 Bid-YTW : 6.61 % |

| GWO.PR.H | Deemed-Retractible | -3.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.14 Evaluated at bid price : 19.14 Bid-YTW : 6.36 % |

| CCS.PR.C | Deemed-Retractible | -3.08 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 6.05 % |

| MFC.PR.Q | FixedReset Ins Non | -3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.97 Evaluated at bid price : 12.97 Bid-YTW : 6.67 % |

| GWO.PR.L | Deemed-Retractible | -3.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.91 Evaluated at bid price : 22.15 Bid-YTW : 6.39 % |

| MFC.PR.G | FixedReset Ins Non | -2.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.02 Evaluated at bid price : 13.02 Bid-YTW : 6.77 % |

| PWF.PR.K | Perpetual-Discount | -2.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.31 Evaluated at bid price : 19.31 Bid-YTW : 6.52 % |

| POW.PR.B | Perpetual-Discount | -2.81 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.41 Evaluated at bid price : 20.41 Bid-YTW : 6.69 % |

| BMO.PR.E | FixedReset Disc | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.27 Evaluated at bid price : 14.27 Bid-YTW : 6.39 % |

| BNS.PR.I | FixedReset Disc | -2.64 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.75 Evaluated at bid price : 14.75 Bid-YTW : 5.90 % |

| TD.PF.H | FixedReset Prem | -2.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.45 Evaluated at bid price : 20.45 Bid-YTW : 5.82 % |

| RY.PR.Q | FixedReset Prem | -2.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.37 Evaluated at bid price : 21.67 Bid-YTW : 5.94 % |

| GWO.PR.M | Deemed-Retractible | -2.59 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 22.33 Evaluated at bid price : 22.60 Bid-YTW : 6.43 % |

| IFC.PR.E | Deemed-Retractible | -2.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.11 Evaluated at bid price : 21.11 Bid-YTW : 6.18 % |

| BAM.PF.F | FixedReset Disc | -2.44 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.00 Evaluated at bid price : 14.00 Bid-YTW : 6.42 % |

| GWO.PR.Q | Deemed-Retractible | -2.42 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.15 Evaluated at bid price : 20.15 Bid-YTW : 6.42 % |

| BMO.PR.W | FixedReset Disc | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.35 Evaluated at bid price : 12.35 Bid-YTW : 6.31 % |

| SLF.PR.C | Deemed-Retractible | -2.37 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.74 Evaluated at bid price : 17.74 Bid-YTW : 6.30 % |

| GWO.PR.I | Deemed-Retractible | -2.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.83 Evaluated at bid price : 17.83 Bid-YTW : 6.34 % |

| IFC.PR.F | Deemed-Retractible | -2.31 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.16 Evaluated at bid price : 21.16 Bid-YTW : 6.29 % |

| TD.PF.K | FixedReset Disc | -2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.46 Evaluated at bid price : 14.46 Bid-YTW : 6.16 % |

| NA.PR.X | FixedReset Prem | -2.30 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.39 Evaluated at bid price : 21.70 Bid-YTW : 6.36 % |

| PWF.PR.T | FixedReset Disc | -2.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.22 Evaluated at bid price : 12.22 Bid-YTW : 6.77 % |

| EML.PR.A | FixedReset Ins Non | -2.23 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2030-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.47 Bid-YTW : 7.83 % |

| CU.PR.F | Perpetual-Discount | -2.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.75 Evaluated at bid price : 19.75 Bid-YTW : 5.75 % |

| TD.PF.I | FixedReset Disc | -2.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 15.42 Evaluated at bid price : 15.42 Bid-YTW : 6.12 % |

| CU.PR.I | FixedReset Prem | -2.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 22.25 Evaluated at bid price : 23.01 Bid-YTW : 4.88 % |

| TRP.PR.D | FixedReset Disc | -2.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 11.80 Evaluated at bid price : 11.80 Bid-YTW : 6.89 % |

| RY.PR.N | Perpetual-Discount | -2.05 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 5.76 % |

| IFC.PR.C | FixedReset Ins Non | -2.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.95 Evaluated at bid price : 12.95 Bid-YTW : 6.24 % |

| RY.PR.S | FixedReset Disc | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.70 Evaluated at bid price : 14.70 Bid-YTW : 5.79 % |

| TD.PF.A | FixedReset Disc | -2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.26 Evaluated at bid price : 12.26 Bid-YTW : 6.31 % |

| EMA.PR.F | FixedReset Disc | -1.97 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.90 Evaluated at bid price : 14.90 Bid-YTW : 5.91 % |

| BAM.PF.A | FixedReset Disc | -1.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 15.00 Evaluated at bid price : 15.00 Bid-YTW : 6.37 % |

| RY.PR.J | FixedReset Disc | -1.93 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.71 Evaluated at bid price : 14.71 Bid-YTW : 5.65 % |

| CM.PR.O | FixedReset Disc | -1.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 11.78 Evaluated at bid price : 11.78 Bid-YTW : 6.74 % |

| GWO.PR.P | Deemed-Retractible | -1.91 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.10 Evaluated at bid price : 21.10 Bid-YTW : 6.42 % |

| IFC.PR.A | FixedReset Ins Non | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 10.04 Evaluated at bid price : 10.04 Bid-YTW : 6.15 % |

| BIP.PR.F | FixedReset Disc | -1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.20 Evaluated at bid price : 18.20 Bid-YTW : 7.04 % |

| TD.PF.L | FixedReset Disc | -1.84 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.58 Evaluated at bid price : 17.58 Bid-YTW : 6.03 % |

| PWF.PR.R | Perpetual-Premium | -1.80 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.26 Evaluated at bid price : 21.26 Bid-YTW : 6.58 % |

| IAF.PR.G | FixedReset Ins Non | -1.76 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.83 Evaluated at bid price : 12.83 Bid-YTW : 6.76 % |

| IFC.PR.I | Perpetual-Premium | -1.74 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.72 Evaluated at bid price : 22.01 Bid-YTW : 6.19 % |

| GWO.PR.T | Deemed-Retractible | -1.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.26 Evaluated at bid price : 20.26 Bid-YTW : 6.38 % |

| RY.PR.M | FixedReset Disc | -1.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.06 Evaluated at bid price : 14.06 Bid-YTW : 5.72 % |

| BMO.PR.D | FixedReset Disc | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 16.13 Evaluated at bid price : 16.13 Bid-YTW : 5.99 % |

| BIP.PR.E | FixedReset Disc | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.10 Evaluated at bid price : 18.10 Bid-YTW : 6.94 % |

| CU.PR.D | Perpetual-Discount | -1.63 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.15 Evaluated at bid price : 21.15 Bid-YTW : 5.85 % |

| TD.PF.J | FixedReset Disc | -1.61 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.66 Evaluated at bid price : 14.66 Bid-YTW : 6.13 % |

| MFC.PR.R | FixedReset Ins Non | -1.60 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 16.57 Evaluated at bid price : 16.57 Bid-YTW : 6.75 % |

| BNS.PR.E | FixedReset Prem | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.44 Evaluated at bid price : 21.44 Bid-YTW : 6.04 % |

| CU.PR.G | Perpetual-Discount | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.80 Evaluated at bid price : 19.80 Bid-YTW : 5.73 % |

| TD.PF.B | FixedReset Disc | -1.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.45 Evaluated at bid price : 12.45 Bid-YTW : 6.24 % |

| GWO.PR.G | Deemed-Retractible | -1.23 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.05 Evaluated at bid price : 20.05 Bid-YTW : 6.51 % |

| IAF.PR.B | Deemed-Retractible | -1.19 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.01 Evaluated at bid price : 20.01 Bid-YTW : 5.77 % |

| GWO.PR.N | FixedReset Ins Non | -1.07 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 9.25 Evaluated at bid price : 9.25 Bid-YTW : 5.05 % |

| W.PR.K | FixedReset Prem | -1.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 6.22 % |

| BAM.PF.J | FixedReset Prem | 1.12 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.41 Evaluated at bid price : 21.75 Bid-YTW : 5.46 % |

| EIT.PR.A | SplitShare | 1.34 % | YTW SCENARIO Maturity Type : Soft Maturity Maturity Date : 2024-03-14 Maturity Price : 25.00 Evaluated at bid price : 25.00 Bid-YTW : 4.82 % |

| BMO.PR.Y | FixedReset Disc | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.80 Evaluated at bid price : 13.80 Bid-YTW : 5.99 % |

| TRP.PR.G | FixedReset Disc | 1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.10 Evaluated at bid price : 13.10 Bid-YTW : 6.81 % |

| NA.PR.W | FixedReset Disc | 1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 11.95 Evaluated at bid price : 11.95 Bid-YTW : 6.63 % |

| BAM.PF.I | FixedReset Prem | 1.71 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.59 Evaluated at bid price : 22.00 Bid-YTW : 5.45 % |

| TD.PF.G | FixedReset Prem | 1.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.81 Evaluated at bid price : 22.30 Bid-YTW : 5.93 % |

| BAM.PR.B | Floater | 1.75 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 8.15 Evaluated at bid price : 8.15 Bid-YTW : 7.43 % |

| BAM.PF.D | Perpetual-Discount | 1.89 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.85 Evaluated at bid price : 18.85 Bid-YTW : 6.53 % |

| RY.PR.H | FixedReset Disc | 2.00 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.75 Evaluated at bid price : 12.75 Bid-YTW : 6.02 % |

| BNS.PR.H | FixedReset Prem | 2.04 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.03 Evaluated at bid price : 21.03 Bid-YTW : 5.74 % |

| TRP.PR.K | FixedReset Prem | 2.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 20.29 Evaluated at bid price : 20.29 Bid-YTW : 6.10 % |

| PWF.PR.Q | FloatingReset | 2.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 9.00 Evaluated at bid price : 9.00 Bid-YTW : 6.17 % |

| TRP.PR.J | FixedReset Prem | 2.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.50 Evaluated at bid price : 21.85 Bid-YTW : 6.34 % |

| BMO.PR.B | FixedReset Prem | 2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 19.85 Evaluated at bid price : 19.85 Bid-YTW : 5.90 % |

| W.PR.M | FixedReset Prem | 2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.50 Evaluated at bid price : 21.50 Bid-YTW : 6.16 % |

| GWO.PR.F | Deemed-Retractible | 2.72 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 22.72 Evaluated at bid price : 23.01 Bid-YTW : 6.42 % |

| CM.PR.Y | FixedReset Disc | 3.06 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 17.85 Evaluated at bid price : 17.85 Bid-YTW : 6.35 % |

| BIK.PR.A | FixedReset Prem | 3.45 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 22.03 Evaluated at bid price : 22.50 Bid-YTW : 6.50 % |

| RY.PR.P | Perpetual-Premium | 3.82 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 22.52 Evaluated at bid price : 22.85 Bid-YTW : 5.79 % |

| TD.PF.F | Perpetual-Discount | 3.90 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.84 % |

| RY.PR.W | Perpetual-Discount | 4.27 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.75 Evaluated at bid price : 22.00 Bid-YTW : 5.61 % |

| HSE.PR.A | FixedReset Disc | 4.50 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 6.27 Evaluated at bid price : 6.27 Bid-YTW : 9.43 % |

| TRP.PR.B | FixedReset Disc | 4.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 7.85 Evaluated at bid price : 7.85 Bid-YTW : 5.85 % |

| BNS.PR.Z | FixedReset Bank Non | 7.39 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 10.48 % |

| PVS.PR.H | SplitShare | 7.78 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2027-02-28 Maturity Price : 25.00 Evaluated at bid price : 24.25 Bid-YTW : 5.26 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.A | FixedReset Disc | 90,550 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.26 Evaluated at bid price : 12.26 Bid-YTW : 6.31 % |

| BMO.PR.S | FixedReset Disc | 78,590 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.50 Evaluated at bid price : 12.50 Bid-YTW : 6.34 % |

| BAM.PR.R | FixedReset Disc | 75,830 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 10.79 Evaluated at bid price : 10.79 Bid-YTW : 6.66 % |

| RY.PR.Z | FixedReset Disc | 73,867 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 12.55 Evaluated at bid price : 12.55 Bid-YTW : 6.04 % |

| TD.PF.I | FixedReset Disc | 71,200 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 15.42 Evaluated at bid price : 15.42 Bid-YTW : 6.12 % |

| TD.PF.J | FixedReset Disc | 67,705 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 14.66 Evaluated at bid price : 14.66 Bid-YTW : 6.13 % |

| There were 117 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| PWF.PR.S | Perpetual-Discount | Quote: 18.75 – 22.76 Spot Rate : 4.0100 Average : 2.2997 YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 6.51 % |

| NA.PR.A | FixedReset Prem | Quote: 21.00 – 24.50 Spot Rate : 3.5000 Average : 1.9650 YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 21.00 Evaluated at bid price : 21.00 Bid-YTW : 6.31 % |

| BAM.PF.B | FixedReset Disc | Quote: 13.52 – 16.50 Spot Rate : 2.9800 Average : 1.8339 YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 13.52 Evaluated at bid price : 13.52 Bid-YTW : 6.49 % |

| PWF.PR.Q | FloatingReset | Quote: 9.00 – 12.00 Spot Rate : 3.0000 Average : 1.9286 YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 9.00 Evaluated at bid price : 9.00 Bid-YTW : 6.17 % |

| BNS.PR.Z | FixedReset Bank Non | Quote: 21.52 – 24.00 Spot Rate : 2.4800 Average : 1.4548 YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.52 Bid-YTW : 10.48 % |

| PWF.PR.P | FixedReset Disc | Quote: 8.30 – 10.80 Spot Rate : 2.5000 Average : 1.5092 YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2050-03-13 Maturity Price : 8.30 Evaluated at bid price : 8.30 Bid-YTW : 6.61 % |