Pundits are saying the money market shows the worst is over for credit:

The worst of the credit crisis that prompted banks to restrict lending and the Federal Reserve to rescue Bear Stearns Cos. may be over, short-term borrowing rates show.

The difference between the yield on three-month Treasury bills and the rate on dollar-denominated loans in London, an indication of credit risk known as the TED spread, narrowed 7 basis points to 0.93 basis points, the smallest since Feb. 25. The gap reached 2 percentage points on March 19.

… but the visible effects may be just getting under weigh:

As the Fed’s latest loan survey makes clear, lenders have dropped the guillotine. With the usual delay, the poison is spreading from banks to the real world.

Diane Vazza, S&P’s credit chief, says defaults are rising at almost twice the rate of past downturns. “Companies are heading into this recession with a much more toxic mix. Their margin for error is razor-thin,” she said.

Two-thirds have a “speculative” rating, compared to 50pc before the dotcom bust, and 40pc in the early 1990s. The culprit is debt. “They ramped it up in the last 18 months of the credit boom. A lot of deals were funded that should not have been funded,” she said.

Some 174 US companies are trading at “distress levels”. Spreads on their bonds have rocketed above 1,000 basis points. This does not cover the carnage among smaller firms outside the rating universe.

Meanwhile, some research is being done into the Equity premium in Victorian England:

The stock market experienced negative total returns in only four years between 1825 and 1870. Three of these years (1825, 1826 and 1847) had financial crashes after a period of promotional mania on the stock market. The negative returns in 1853 can be attributed to concerns over the impending Crimean war.

Despite the serious financial crisis of 1866 following the collapse of several banks, the market produced positive total returns in that year.

Those were the good old days, eh? The 1866 crisis was the collapse of Overend-Gurney, which I promised to discuss on March 31, but is still … er … pending.

I have updated the post on the BoE Financial Stability Report to acknowledge Willem Buiter’s objections to the BoE methodology in forecasting ultimate sub-prime losses.

MBIA, whose delays in transferring $1.1-billion from the parent to the insurance subsidiary was reported on May 7 has (as passed on by Naked Capitalism) finally made a move:

MBIA Inc., the ailing bond insurer, rose in New York Stock Exchange trading after saying it will pump $900 million into its insurance unit and reporting a first-quarter loss that was narrower than some analysts’ estimates.

Those who have been taking the Clear Channel takeover as a template for the unfolding of the BCE / Teachers’ deal will no doubt be highly interested in rumours of funding at a reduced price:

Clear Channel Communications Inc. surged as much as 18 percent on reports of settlement talks with six banks on a proposal to finance the radio broadcaster’s acquisition by two buyout firms at a reduced price.

Citigroup Inc. and five other banks may fund the buyout for $36 a share as part of a settlement of lawsuits pending in New York and Texas state courts, the Wall Street Journal reported, without saying where it got the information. That’s below the $39.20 price buyout firms agreed to pay last year and more than an intraday high of $35.30 in New York Stock Exchange trading.

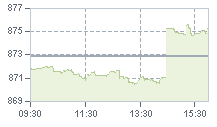

Yet another day with a mysterious discontinuity in the TXPR index:

The jump was probably partly due to BAM.PR.K, which traded 300 shares at $19.40 at 9:30am, then 100 shares at $20.32 at 2:37pm. Ain’t it wonderful! Closing quotation was 19.58-20.49, 1×5. This issue comprises 1.46% of CPD (which can be assumed to be a reasonable proxy for the index, so this 4.74% jump in trading price translates to 6.9bp on the index, or about one-seventh of the total jump. Analysis of the other elements of the discontinuity is left as an exercise for the student.

All in all, though, it was a quiet day.

| Note that these indices are experimental; the absolute and relative daily values are expected to change in the final version. In this version, index values are based at 1,000.0 on 2006-6-30 | |||||||

| Index | Mean Current Yield (at bid) | Mean YTW | Mean Average Trading Value | Mean Mod Dur (YTW) | Issues | Day’s Perf. | Index Value |

| Ratchet | 4.94% | 4.97% | 43,845 | 15.61 | 1 | -0.7997% | 1,083.2 |

| Fixed-Floater | 4.68% | 4.69% | 61,190 | 15.95 | 7 | +0.7567% | 1,066.6 |

| Floater | 4.18% | 4.22% | 61,441 | 16.93 | 2 | +1.5967% | 902.9 |

| Op. Retract | 4.83% | 3.15% | 87,702 | 2.60 | 15 | +0.0831% | 1,054.5 |

| Split-Share | 5.27% | 5.55% | 71,195 | 4.15 | 13 | +0.0374% | 1,050.9 |

| Interest Bearing | 6.13% | 6.06% | 54,004 | 3.82 | 3 | 0.0000% | 1,105.9 |

| Perpetual-Premium | 5.89% | 5.66% | 141,742 | 6.42 | 9 | -0.0253% | 1,020.8 |

| Perpetual-Discount | 5.69% | 5.74% | 307,011 | 14.28 | 63 | -0.0336% | 919.3 |

| Major Price Changes | |||

| Issue | Index | Change | Notes |

| PWF.PR.E | PerpetualDiscount | -1.5422% | Now with a pre-tax bid-YTW of 5.65% based on a bid of 24.26 and a limitMaturity. |

| RY.PR.F | PerpetualDiscount | -1.3951% | Now with a pre-tax bid-YTW of 5.65% based on a bid of 19.78 and a limitMaturity. |

| CIU.PR.A | PerpetualDiscount | -1.1707% | Now with a pre-tax bid-YTW of 5.69% based on a bid of 20.26 and a limitMaturity. |

| FFN.PR.A | SplitShare | +1.1964% | Asset coverage of 2.0+:1 as of April 30, according to the company. Now with a pre-tax bid-YTW of 5.04% based on a bid of 10.15 and a hardMaturity 2014-12-1 at 10.00. |

| FAL.PR.B | FixFloat | +1.2170% | |

| BMO.PR.H | PerpetualDiscount | +1.9450% | Now with a pre-tax bid-YTW of 5.45% based on a bid of 24.11 and a limitMaturity. |

| BAM.PR.K | Floater | +2.7822% | |

| BCE.PR.G | FixFloat | +3.2120% | |

| Volume Highlights | |||

| Issue | Index | Volume | Notes |

| NTL.PR.G | Scraps (Would be Ratchet, but there are credit concerns) | 110,736 | |

| IGM.PR.A | OpRet | 52,532 | CIBC crossed 50,000 at 26.95. Now with a pre-tax bid-YTW of 3.32% based on a bid of 26.85 and a call 2009-7-30 at 26.00. |

| RY.PR.K | OpRet | 50,345 | Now with a pre-tax bid-YTW of 1.03% based on a bid of 25.04 and a call 2008-6-11 at 25.00. |

| PWF.PR.D | OpRet | 45,100 | CIBC crossed 45,100 at 26.00 in the only trade of the day. Now with a pre-tax bid-YTW of 4.29% based on a bid of 25.95 and a call 2008-11-30 at 25.80. |

| CM.PR.A | OpRet | 26,170 | Nesbitt bought 12,500 from RBC at 25.95. Now with a pre-tax bid-YTW of -2.18% based on a bid of 25.96 and a call 2008-6-11 at 25.75. |

| TD.PR.P | PerpetualDiscount | 25,693 | Desjardins was buyer on the last ten trades, totalling 20,850, starting at 24.18, going as high as 24.50, ending with 24.30 (odd lot). Now with a pre-tax bid-YTW of 5.52% based on a bid of 23.94 and a limitMaturity. |

There were eleven other index-included $25-pv-equivalent issues trading over 10,000 shares today.

“Those who have been taking the Clear Channel takeover as a template for the unfolding of the BCE / Teachers’ deal will no doubt be highly interested in rumours of funding at a reduced price:”

——————–

“dream on” is the only thing that comes to mind with the suggestion of BCE repricing.

2 key differences between the BCE deal, and the Clear Channel deal:

first, BCE shareholders would have to vote again, and since BCE is widespread amongst “widows, orphans, and generally naive investors”, any reduction in price would not be well received. Beyond that, Canadian investment houses have done a lovely job recruiting this money for re-investment, and a large element of the proceeds of this deal has already been committed (although obviously not yet placed).

second item, and this one is the most important one . . . unlike Clear Channel that nobody else really wanted in the first place, BCE was picked over like buzzards on road kill; any repricing would re-mobilize the first round losers, not to mention Telus, who was only slightly disqualified the first time around on the issue of . . . price.

BCE repricing? Don’t even think about it Mr. Leech.

madequota

Well … place yer bets, gents! By me, it’s all speculation.

no kidding, eh?! . . . and there’s still the bondholder wildcard as well!

this thing’s been “in play” now for better part of a full year . . . kind of sad comment once again on securities regulation in Canada

hats off to Jim Leech though; he’s taken a large, but relatively unknown entity in the Teacher’s Pension Fund, and for little or no cost, catapulted it into the position of being responsible for the largest leveraged buyout of all time.

when you look at the taxpayers’ potential liability on this one, I continue to be amazed that the Feds haven’t poo-pooed the deal. Oh well, that’s the Harper/Flaherty team for you.

madequota

no kidding, eh?! . . . and there’s still the bondholder wildcard as well!

I am advised that the Clear Channel news caused Credit Default Swaps on BCE to gap wider by about 60bp as some players, anyway, felt the chance of the deal closing (and credit quality of the bonds declining) had improved substantially.

when you look at the taxpayers’ potential liability on this one, I continue to be amazed that the Feds haven’t poo-pooed the deal. Oh well, that’s the Harper/Flaherty team for you.

I don’t understand this part. What taxpayer potential liability? What do the Feds/Harper/Flaherty have to do with it?

Well, the government has an obligation to ensure that certain essential services are maintained. Although they may not have ownership of same, it is their responsibility to not have these services fail.

BCE is Canada’s largest, and main, telecommunications provider. They run the country’s telephone network in a nutshell. It’s common knowledge that Bell’s infrastructure is outdated, decaying, and faulty. If this situation should progress to the downside, at some point the government would have no choice but to step in, with some kind of support, at the very least to ensure that telecommunications links are maintained.

As such, having this organization become a debt-laden privately owned squashball with deteriorating and unsustainable assets would ultimately come back to the taxpayer to fix. Look at McDonald – Det. . . . government didn’t see transfer of ownership in the best interests of the taxpayer . . . so the deal was halted. So should BCE.

madequota