Canadian inflation was tamer than expected:

Canada’s inflation rate slowed more than economists forecast in November, returning to the central bank’s target on a drop in gasoline prices.

The consumer price index rose 2.0 percent from a year ago following the October pace of 2.4 percent, Statistics Canada said today from Ottawa. The core rate, which excludes eight volatile products including fruit, vegetables and gasoline, slowed to 2.1 percent following the October pace of 2.3 percent, which was the fastest in almost three years.

Economists forecast the total rate would rise 2.2 percent and core by 2.4 percent, according to median responses in separate Bloomberg News surveys.

Bank of Canada Governor Stephen Poloz has said inflation will slow to a 1.4 percent pace in the second quarter of next year, ending a period of faster-than-expected gains linked to temporary factors such as a weaker currency and price increases for products such as meat. Policy makers have kept their benchmark overnight lending rate at 1 percent for more than four years and economists surveyed by Bloomberg predict Poloz won’t tighten for about another year.

… which didn’t do the dollar much good:

Canada’s dollar approached a five-year low after a report showed inflation slowed more than forecast in November, adding to speculation slumping crude-oil prices will damp economic growth and keep interest rates low for longer.

The currency fell for a fourth week as crude, the nation’s biggest export, traded at almost the lowest since 2009. Canadian two-year government bonds’ yield advantage over U.S. peers shrank to the least since 2010 as traders priced in a rate increase by the Federal Reserve in the first half of 2015 and began to push chances for Bank of Canada rate action into 2016.

…

The loonie, as the Canadian dollar is known for the image of the aquatic bird on the C$1 coin, weakened 0.2 percent to C$1.1600 per U.S. dollar at 5 p.m. Toronto time. It touched C$1.1674 on Dec. 15, the weakest level since July 2009. One loonie purchases 86.21 U.S. cents.

…

Canada’s two-year debt yielded 37 basis points, or 0.37 percentage point, more than comparable-maturity Treasuries, compared with 63 basis points in October. The Canadian yields have been little changed during the period, while U.S. yields rose as investors sold Treasuries. Two-year securities are more sensitive to expectations for changes in central-bank policy than longer-maturity debt, which tends to reflect expectations for inflation.

…

Canadian retail sales were little changed in October at C$42.8 billion ($36.9 billion), Statistics Canada said in another report. A Bloomberg survey of economists forecast a 0.3 percent decrease.Ontario, Canada’s most populous province, had its credit rating downgraded to AA- from AA by Fitch Ratings. The company cited the difficult actions needed to meet the province’s goal for a balanced budget by 2017-18.

… but equities seemed pretty happy:

Canadian stocks rose for a fourth day, capping their best week in five years, as energy producers led gains in a rally ignited by the Federal Reserve’s pledge to be patient on boosting borrowing costs.

Energy stocks in the Standard & Poor’s/TSX Composite Index (SPTSX) rose 2.9 percent for a 13 percent gain this week, the most in five years. Trican Well Service Ltd. and TransGlobe Energy Corp. soared more than 8.8 percent. BlackBerry Ltd. dropped 1.2 percent after reporting third-quarter revenue short of analysts’ estimates.

The S&P/TSX index climbed 121.51 points, or 0.9 percent, to 14,468.26 at 4 p.m. in Toronto. The gauge surged 5.6 percent in the past four days as oil prices stabilized and Fed Chair Janet Yellen said the U.S. central bank will probably hold rates near zero at least through the first quarter.

MetLife has been designated a systemically important financial institution – and doesn’t like it:

The Financial Stability Oversight Council voted to designate New York-based MetLife a SIFI, the insurer said today in a statement. The ruling subjects MetLife to stricter Federal Reserve oversight that could include tougher capital, leverage and liquidity requirements. The company can appeal in U.S. district court within 30 days.

“We continue to believe that MetLife is not systemically important,” the insurer said in the statement. “The company will carefully review the designation rationale as it considers its next steps.”

…

The company has said that it wouldn’t pose a risk to the broader financial system even if it were to fail, and Kandarian has called the insurance industry a source of stability. MetLife, based in New York, didn’t take a bailout during the 2008 financial crisis.MetLife said today that FSOC should focus on activities that pose systemic risks, rather than on individual companies.

“FSOC has already embraced this activities-based approach for the asset-management industry but has rejected it for the life-insurance industry,” MetLife said in its statement.

U.S. lawmakers voted last week to give the Fed more flexibility in how it sets rules after insurers said they shouldn’t be subject to standards set for banks. Kandarian, in a Dec. 10 statement, praised Congress for passing the legislation, which he said would give the central bank the “opportunity to write rules that will preserve competition.”

Simon Kennedy of Bloomberg draws our attention to an interesting parallel to 1956:

The U.K., with France, followed Israel into Egypt in 1956 after President Gamal Abdel Nasser nationalized the global commercial lifeline and kicked out the consortium that had been running the canal.

Britain was exposed when sterling came under speculative attack. Investors targeted its $2.80 peg to the dollar, forcing the Bank of England to run down its reserves to defend it.

For the U.K., “Suez was also a financial crisis,” according to a 2001 study by IMF historian James M. Boughton.

As they struggled to maintain the $2 billion minimum viewed as necessary to stave off devaluation, British officials began looking for assistance. Knowing the U.S. was unlikely to help directly, they turned to the then decade-old IMF.

No dice. U.S. Treasury Secretary George M. Humphrey told the U.K. he would only back it at the IMF when it was “conforming to, rather than defying, the United Nations.”

On the verge of having to reveal its reserves had breached $2 billion, the British government buckled and announced a troop withdrawal from Egypt. That freed up $1.3 billion of international loans. Sterling was saved.

As noted very briefly above, Fitch downgraded Ontari-ari-ari-owe:

RATING DOWNGRADE: Difficult actions will be necessary to achieve the province’s deficit elimination goal of fiscal 2018 and budget options are likely to prove more limited given the extent of actions taken to date and use of one-time actions to achieve targets, in Fitch’s opinion. While the province is considering other fiscal options for fiscal 2016 should economic conditions restrain future revenue growth, the downgrade to ‘AA-‘ reflects Fitch’s concern that risks remain to achieving its goals and both debt burden and the accumulated deficit will remain significantly elevated, reflected in a rating level more consistent with an ‘AA-‘ rating.

…

SIGNIFICANT FINANCIAL IMBALANCE: The province had an accumulated deficit equal to 152% of operating revenues in fiscal 2014 (25.4% of gross domestic product [GDP]) due to, slow revenue growth, and increasing expenditures, and sizable capital borrowing. Annual deficits through the forecast period of fiscal 2018 will contribute to growth in the accumulated deficit.

…

LARGE AND GROWING DEBT BURDEN: The province has a high debt burden (net direct debt to GDP) with net debt to GDP at 38.4% for fiscal 2014, although debt service expense is a manageable 8% of annual expenditures. Fitch expects debt levels to increase through fiscal 2016, and then begin to decrease, given the province’s expectation of an annual deficit through that fiscal year and continued growth in GDP. Pensions are well funded.RATING SENSITIVITIES

The rating is sensitive to the province’s commitment and success in achieving deficit elimination targets and restoring fiscal balance. Failure to enact budgets that follow a path toward articulated deficit elimination targets would result in negative rating pressure. Reaching deficit elimination targets ahead of forecast, sizable growth in GDP, and steady progress on lowering debt burden and the accumulated deficit would be positive credit factors.

It was a good day for the Canadian preferred share market, with PerpetualDiscounts winning 37bp, FixedResets up 26bp and DeemedRetractibles gaining 13bp. Volatility was high (although low by recent standards!) and dominated by FixedResets – particularly the low-spread and credit-uncertain Enbridge issues which have been hit hard recently. Volume was average.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

- based on Implied Volatility Theory only

- are relative only to other FixedResets from the same issuer

- assume constant GOC-5 yield

- assume constant Implied Volatility

- assume constant spread

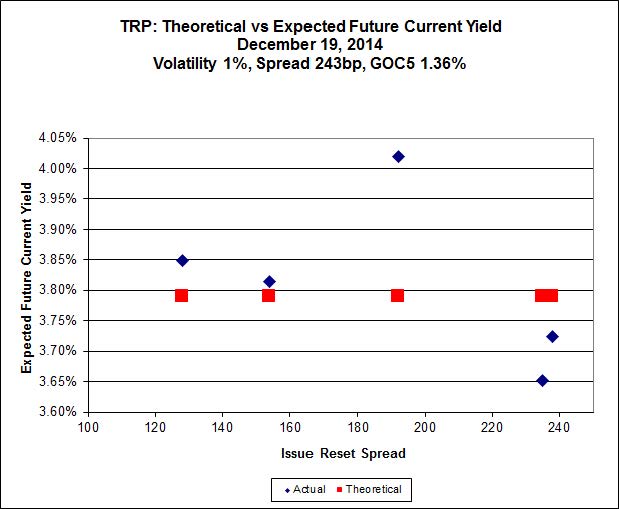

Here’s TRP:

Click for Big

So according to this, TRP.PR.A, bid at 20.40, is $1.24 cheap, but it has already reset (at +192). TRP.PR.D, bid at 25.11 and resetting at +238bp on 2019-4-30 is $0.44 rich and TRP.PR.E, bid at 25.40 and resetting at +235bp on 2019-10-30, is $0.93 rich.

This particular calculation is fascinating because it is apparent that – disregarding the TRP.PR.A outlier – the slope of the line used to calculate implied volatility is negative. I can’t remember seeing one of those since the Credit Crunch!

Click for Big

Here, as has often been the case lately, it is apparent that

- MFC.PR.F, resetting at 141bp on 2016-06-19 is in another world and distorting results again. It’s the only deep-discount issue, bid at 20.65 – everything else is above or near par.

- the slope determined by the higher-spread issues is unreasonably high if these are to be considered perpetual issues and unreasonably low if they are to be considered NVCC non-compliant issues

Click for Big

There continues to be extraordinary cheapness in the lowest-spread issue, BAM.PR.X, resetting at +180bp on 2017-6-30, which is bid at 20.26 and appears to be $0.95 cheap, while BAM.PR.R, resetting at +230bp 2016-6-30 is bid at 25.20 and appears to be $1.65 rich.

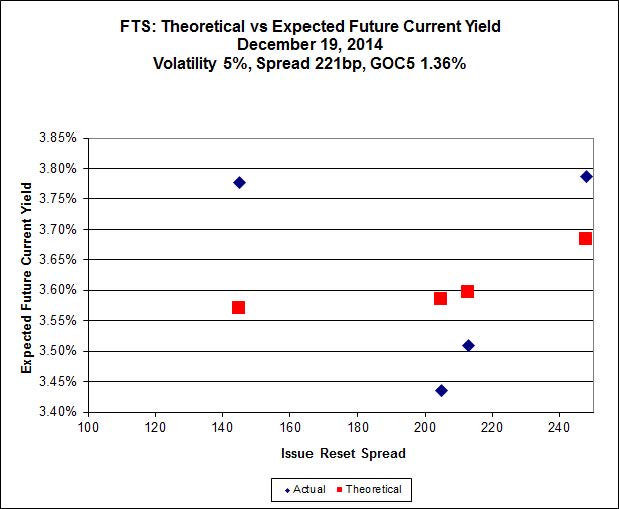

Click for Big

This is just weird because the middle is expensive and the ends are cheap but anyway … FTS.PR.H, with a spread of +145bp, and bid at 18.60, looks $1.08 cheap and resets 2015-6-1. FTS.PR.K, with a spread of +205bp, and bid at 24.81, looks $1.02 expensive and resets 2019-3-1

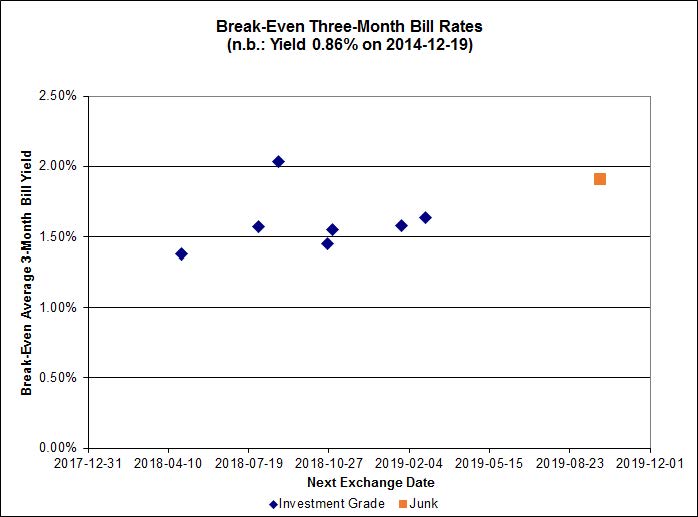

Click for Big

The average break-even rate has declined from 1.80%-2.00% at the time recent conversion decisions were made to a current range of 1.50%-1.60%. This decline means that the estimated profit on TRP.PR.A conversion has declined from $0.48 to a mere $0.16 (at the lower end of the range).

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.1782 % | 2,479.6 |

| FixedFloater | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 1.1782 % | 3,925.8 |

| Floater | 3.06 % | 3.16 % | 65,591 | 19.34 | 4 | 1.1782 % | 2,636.0 |

| OpRet | 4.41 % | -2.78 % | 26,566 | 0.08 | 2 | 0.0000 % | 2,748.8 |

| SplitShare | 4.31 % | 4.04 % | 39,459 | 3.70 | 5 | -0.1804 % | 3,176.6 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0000 % | 2,513.5 |

| Perpetual-Premium | 5.44 % | -3.14 % | 75,182 | 0.08 | 20 | -0.0196 % | 2,475.1 |

| Perpetual-Discount | 5.20 % | 5.11 % | 110,801 | 15.26 | 15 | 0.3683 % | 2,647.5 |

| FixedReset | 4.26 % | 3.58 % | 250,616 | 16.57 | 77 | 0.2554 % | 2,519.8 |

| Deemed-Retractible | 4.98 % | 1.11 % | 99,552 | 0.19 | 40 | 0.1252 % | 2,610.0 |

| FloatingReset | 2.56 % | 2.11 % | 63,285 | 3.51 | 5 | -0.1417 % | 2,535.4 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| ENB.PF.G | FixedReset | 1.18 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 22.74 Evaluated at bid price : 23.99 Bid-YTW : 4.23 % |

| GWO.PR.H | Deemed-Retractible | 1.25 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.28 Bid-YTW : 5.23 % |

| TRP.PR.E | FixedReset | 1.36 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 23.30 Evaluated at bid price : 25.40 Bid-YTW : 3.63 % |

| ENB.PF.E | FixedReset | 1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 22.63 Evaluated at bid price : 23.72 Bid-YTW : 4.27 % |

| PWF.PR.T | FixedReset | 1.49 % | YTW SCENARIO Maturity Type : Call Maturity Date : 2019-01-31 Maturity Price : 25.00 Evaluated at bid price : 25.83 Bid-YTW : 3.49 % |

| ENB.PR.Y | FixedReset | 1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 21.71 Evaluated at bid price : 22.08 Bid-YTW : 4.27 % |

| GWO.PR.N | FixedReset | 1.53 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.95 Bid-YTW : 5.33 % |

| FTS.PR.H | FixedReset | 1.58 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 18.60 Evaluated at bid price : 18.60 Bid-YTW : 3.77 % |

| PWF.PR.A | Floater | 5.56 % | Reasonably sort-of real. This reverses yesterday‘s loss, which was reasonably sort of real, but on trivial volume. Volume today was actually respectable, 5,776 shares, with the low for the day being 18.41 at the opening, with all subsequent trades near or above 19.00 – with a high of 19.98 for 500 shares late in the day. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 19.00 Evaluated at bid price : 19.00 Bid-YTW : 2.78 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| TD.PF.C | FixedReset | 140,825 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 23.07 Evaluated at bid price : 24.76 Bid-YTW : 3.53 % |

| ENB.PR.Y | FixedReset | 127,774 | Scotia crossed 100,000 at 21.98. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 21.71 Evaluated at bid price : 22.08 Bid-YTW : 4.27 % |

| ENB.PR.T | FixedReset | 113,374 | Scotia crossed 100,000 at 22.40. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 21.97 Evaluated at bid price : 22.45 Bid-YTW : 4.29 % |

| SLF.PR.A | Deemed-Retractible | 76,340 | Desjardins crossed 74,800 at 24.40. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.20 Bid-YTW : 5.17 % |

| HSE.PR.A | FixedReset | 74,639 | RBC crossed 46,200 at 19.55. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 19.66 Evaluated at bid price : 19.66 Bid-YTW : 3.99 % |

| BMO.PR.S | FixedReset | 63,578 | RBC crossed 50,000 at 25.53. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-12-19 Maturity Price : 23.36 Evaluated at bid price : 25.50 Bid-YTW : 3.51 % |

| There were 34 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| CGI.PR.D | SplitShare | Quote: 25.16 – 26.08 Spot Rate : 0.9200 Average : 0.7739 YTW SCENARIO |

| IAG.PR.A | Deemed-Retractible | Quote: 23.41 – 23.99 Spot Rate : 0.5800 Average : 0.4533 YTW SCENARIO |

| RY.PR.L | FixedReset | Quote: 26.02 – 26.34 Spot Rate : 0.3200 Average : 0.2162 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 24.86 – 25.19 Spot Rate : 0.3300 Average : 0.2354 YTW SCENARIO |

| BAM.PR.K | Floater | Quote: 16.55 – 16.95 Spot Rate : 0.4000 Average : 0.3074 YTW SCENARIO |

| NEW.PR.D | SplitShare | Quote: 32.17 – 33.09 Spot Rate : 0.9200 Average : 0.8327 YTW SCENARIO |