The junk market is getting nervous:

Investors in the debt of junk-rated companies are showing little patience for even the slightest whiff of bad news as they seek to shield themselves from the market’s first annual loss since 2008. With the Federal Reserve poised to lift interest rates next month and a deepening commodities slump stirring fears that earnings growth will be squeezed, price swings in the market are intensifying.

…

Investors are shunning the lowest-rated junk bonds. That is underscored by the extra yield that investors are demanding to hold CCC rated credits relative to those rated BB. This has jumped to the most in six years.

…

One sometimes-overlooked element that’s contributing to the big price swings is the increasing concentration among investors, according to Stephen Antczak, head of credit strategy at Citigroup Inc. Mutual funds, insurance companies and foreign investors make up 68 percent of corporate bondholders compared with 52 percent at the end of 2007.That means that if one mutual fund investor wants to sell some holdings, there isn’t another one that’s ready to step in. That’s because they typically have similar mandates from investors and often need to sell for the same reasons.

“A less diverse group of investors hold a lot more bonds,” Antczak said. “The difference between incremental buyer is more now than it used to be. It takes a bigger move to get people interested.”

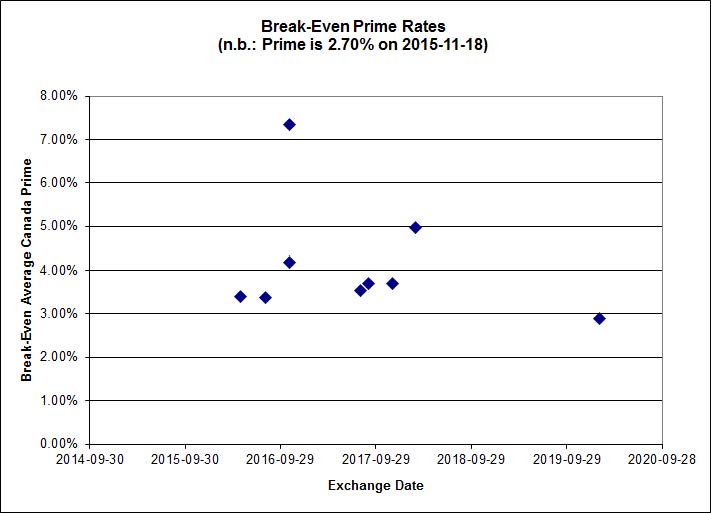

Click for Big

Repsol, which recently purchased Talisman Energy, has not seen much joy from its acquisition:

Repsol SA reported a 62 percent decline in third-quarter earnings as lower crude prices countered improved refining performance. The shares slumped the most in two weeks.

Adjusted net income fell to 159 million euros ($171 million) from 415 million euros a year earlier, Spain’s largest oil company said Thursday. That missed the average 201.6 million-euro estimate of 18 analysts surveyed by Bloomberg. It reported a net loss of 221 million euros after taking charges at units including gas and power.

Repsol is among international oil producers to suffer from a 40 percent decline in the price of Brent crude over the past year. Like its peers, it has sold assets and cut investments to weather the slowdown as a global supply glut persists. The Madrid-based company has also seen debts mount after acquiring Canada’s Talisman Energy Inc. for $13 billion in May.

…

Repsol last month unveiled a five-year plan to sell 6.2 billion euros of assets and reduce investments by as much as 38 percent as it deals with higher debt and the plunge in crude prices. The company announced more than $1 billion in asset sales in the third quarter, part of which was included in the five-year target.

So now they’ve announced a debt tender offer:

Talisman Energy Inc. (the “Offeror”) announced today that it has commenced a tender offer (the “Offer”) to purchase for cash up to $750 million aggregate principal amount (the “Maximum Tender Amount”) of the 5.85% Senior Notes due 2037 (CUSIP No. 87425E AJ2), 5.50% Senior Notes due 2042 (CUSIP No. 87425E AN3), 6.25% Senior Notes due 2038 (CUSIP No. 87425E AK9), 7.25% Debentures due 2027 (CUSIP No. 87425E AE3) and 5.75% Senior Notes due 2035 (CUSIP No. 87425E AH6) issued by the Offeror (collectively, the “Securities”). The amounts of each series of Securities that are purchased will be determined in accordance with the acceptance priority levels specified in the table below and on the cover page of the offer to purchase dated November 24, 2015 (the “Offer to Purchase”) in the column entitled “Acceptance Priority Level” (the “Acceptance Priority Level”), subject to the proration arrangements applicable to the Offer.

As with today’s coercive DC.PR.C exchange offer, they’re offering a premium for early tenders:

Holders of the Securities that are validly tendered and not withdrawn on or prior to 5:00 p.m., New York City time, on December 8, 2015 (the “Early Tender Date”) and accepted for purchase will receive the applicable Total Consideration, which includes an early tender premium of $50.00 per $1,000 principal amount of the Securities accepted for purchase (the “Early Tender Premium”).

S&P rates Repsol’s bonds at BBB- with a negative watch.

Rona Inc., proud issuer of RON.PR.A, was confirmed at Pfd-4[high] by DBRS:

DBRS Limited (DBRS) has today confirmed the Issuer Rating and Senior Unsecured Debt rating of RONA inc. (RONA or the Company) at BB (high), and the Preferred Shares rating at Pfd-4 (high). All trends are Stable. The Recovery Rating on the Senior Unsecured Debt remains RR3. The confirmation reflects RONA’s solid operating performance (growth in same-store sales and margin expansion) through the end of Q3 F2015 in the face of macroeconomic headwinds in certain regions of Canada and its reasonable leverage levels, balanced by rising balance-sheet debt used to finance share repurchases and complete the acquisitions of the 20 franchise stores in its network.

…

Despite the increase in balance-sheet debt, RONA’s credit risk profile and leverage metrics should remain within the range considered acceptable for the current rating over the medium term (i.e., lease-adjusted debt-to-EBITDAR below 4.0 times (x) and lease-adjusted EBITDA coverage above 4.5x).

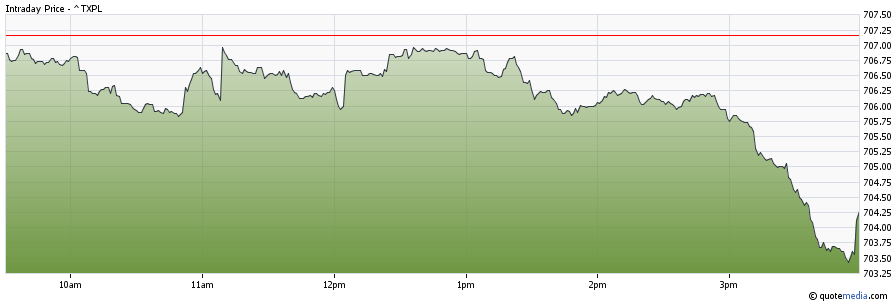

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts gaining 2bp, FixedResets off 63bp and DeemedRetractibles up 19bp. I note that the TXPL total return index now stands at 812.11, down from the October month-end figure of 814.94 … so all the gains of that wondrous first week of November have now evaporated. Easy come, easy go! The Performance Highlights table is its usual lengthy self, highlighting the churn in the market. Volume was very high.

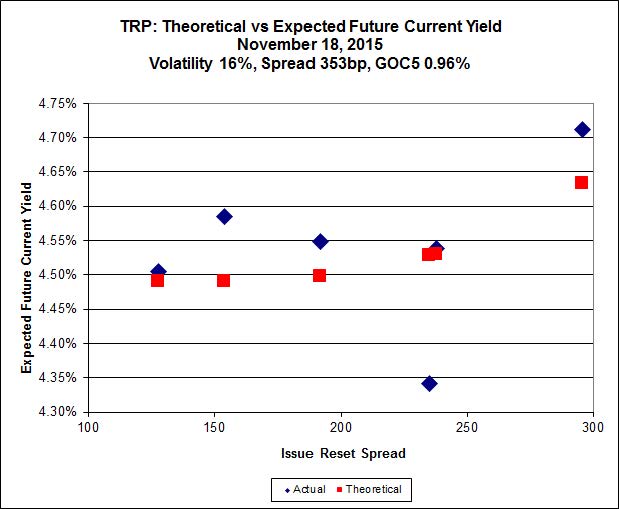

There won’t be any the usual volatility charts and block trading report today … sorry!

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 4.26 % | 5.12 % | 32,966 | 17.67 | 1 | 0.0000 % | 1,819.2 |

| FixedFloater | 6.15 % | 5.39 % | 27,798 | 17.03 | 1 | 2.2502 % | 3,173.8 |

| Floater | 4.25 % | 4.30 % | 82,547 | 16.76 | 3 | 3.3137 % | 1,858.4 |

| OpRet | 4.87 % | 3.99 % | 32,736 | 0.75 | 1 | 0.0000 % | 2,733.2 |

| SplitShare | 4.77 % | 5.61 % | 134,654 | 4.34 | 5 | 0.0886 % | 3,214.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0886 % | 2,508.3 |

| Perpetual-Premium | 5.79 % | 2.32 % | 88,238 | 0.08 | 6 | 0.1584 % | 2,509.5 |

| Perpetual-Discount | 5.57 % | 5.61 % | 87,723 | 14.48 | 33 | 0.0173 % | 2,571.1 |

| FixedReset | 4.97 % | 4.60 % | 224,043 | 15.13 | 76 | -0.6304 % | 2,063.7 |

| Deemed-Retractible | 5.17 % | 5.26 % | 118,086 | 5.38 | 33 | 0.1920 % | 2,580.1 |

| FloatingReset | 2.60 % | 3.78 % | 60,065 | 5.75 | 10 | 0.2509 % | 2,185.1 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| NA.PR.W | FixedReset | -3.68 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.59 Evaluated at bid price : 18.59 Bid-YTW : 4.52 % |

| MFC.PR.N | FixedReset | -3.15 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.01 Bid-YTW : 6.43 % |

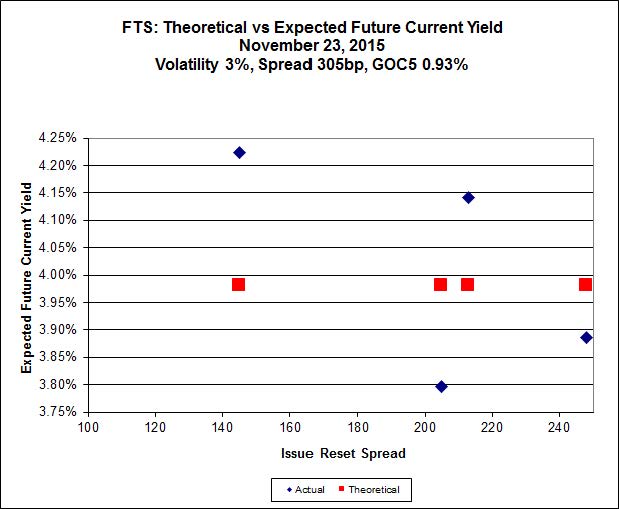

| FTS.PR.M | FixedReset | -3.10 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 21.26 Evaluated at bid price : 21.26 Bid-YTW : 4.19 % |

| NA.PR.S | FixedReset | -2.73 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.63 % |

| FTS.PR.K | FixedReset | -2.70 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 19.09 Evaluated at bid price : 19.09 Bid-YTW : 4.14 % |

| BAM.PR.Z | FixedReset | -2.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.20 Evaluated at bid price : 20.20 Bid-YTW : 5.05 % |

| HSE.PR.A | FixedReset | -2.43 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 13.68 Evaluated at bid price : 13.68 Bid-YTW : 5.00 % |

| BAM.PR.X | FixedReset | -1.98 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 15.35 Evaluated at bid price : 15.35 Bid-YTW : 4.80 % |

| BMO.PR.Q | FixedReset | -1.89 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 20.71 Bid-YTW : 5.63 % |

| BAM.PF.G | FixedReset | -1.65 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.86 Evaluated at bid price : 20.86 Bid-YTW : 4.82 % |

| TD.PF.C | FixedReset | -1.62 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.80 Evaluated at bid price : 18.80 Bid-YTW : 4.44 % |

| TD.PF.E | FixedReset | -1.57 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 21.57 Evaluated at bid price : 21.90 Bid-YTW : 4.32 % |

| RY.PR.Z | FixedReset | -1.56 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.91 Evaluated at bid price : 18.91 Bid-YTW : 4.38 % |

| BAM.PF.E | FixedReset | -1.53 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.89 % |

| CM.PR.P | FixedReset | -1.52 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.75 Evaluated at bid price : 18.75 Bid-YTW : 4.45 % |

| RY.PR.H | FixedReset | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.87 Evaluated at bid price : 18.87 Bid-YTW : 4.44 % |

| CU.PR.G | Perpetual-Discount | -1.41 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.27 Evaluated at bid price : 20.27 Bid-YTW : 5.58 % |

| CM.PR.O | FixedReset | -1.38 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 19.30 Evaluated at bid price : 19.30 Bid-YTW : 4.43 % |

| TD.PF.A | FixedReset | -1.35 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.99 Evaluated at bid price : 18.99 Bid-YTW : 4.41 % |

| BAM.PF.F | FixedReset | -1.33 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.73 Evaluated at bid price : 20.73 Bid-YTW : 4.83 % |

| FTS.PR.G | FixedReset | -1.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.24 Evaluated at bid price : 18.24 Bid-YTW : 4.38 % |

| GWO.PR.N | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 13.50 Bid-YTW : 10.22 % |

| TD.PF.B | FixedReset | -1.24 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 19.07 Evaluated at bid price : 19.07 Bid-YTW : 4.39 % |

| HSE.PR.G | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 21.69 Evaluated at bid price : 22.05 Bid-YTW : 5.15 % |

| HSE.PR.E | FixedReset | -1.21 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 21.30 Evaluated at bid price : 21.30 Bid-YTW : 5.37 % |

| ENB.PR.A | Perpetual-Discount | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 23.55 Evaluated at bid price : 23.82 Bid-YTW : 5.79 % |

| RY.PR.J | FixedReset | -1.14 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.80 Evaluated at bid price : 20.80 Bid-YTW : 4.41 % |

| BMO.PR.S | FixedReset | -1.11 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 19.65 Evaluated at bid price : 19.65 Bid-YTW : 4.34 % |

| W.PR.H | Perpetual-Discount | -1.09 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 23.32 Evaluated at bid price : 23.60 Bid-YTW : 5.90 % |

| BAM.PF.A | FixedReset | -1.02 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.30 Evaluated at bid price : 20.30 Bid-YTW : 4.93 % |

| MFC.PR.L | FixedReset | 1.05 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 19.31 Bid-YTW : 6.81 % |

| GWO.PR.S | Deemed-Retractible | 1.16 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.38 Bid-YTW : 5.75 % |

| BAM.PF.C | Perpetual-Discount | 1.17 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 20.75 Evaluated at bid price : 20.75 Bid-YTW : 5.95 % |

| PVS.PR.D | SplitShare | 1.20 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2021-10-08 Maturity Price : 25.00 Evaluated at bid price : 23.59 Bid-YTW : 5.64 % |

| PWF.PR.S | Perpetual-Discount | 1.40 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 21.45 Evaluated at bid price : 21.78 Bid-YTW : 5.55 % |

| SLF.PR.H | FixedReset | 1.95 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 18.26 Bid-YTW : 7.21 % |

| BAM.PR.G | FixedFloater | 2.25 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 25.00 Evaluated at bid price : 15.45 Bid-YTW : 5.39 % |

| BAM.PF.D | Perpetual-Discount | 2.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 21.01 Evaluated at bid price : 21.01 Bid-YTW : 5.94 % |

| BAM.PR.C | Floater | 2.96 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 11.13 Evaluated at bid price : 11.13 Bid-YTW : 4.30 % |

| BAM.PR.K | Floater | 3.29 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 11.00 Evaluated at bid price : 11.00 Bid-YTW : 4.35 % |

| BAM.PR.B | Floater | 3.69 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 11.23 Evaluated at bid price : 11.23 Bid-YTW : 4.26 % |

| TRP.PR.F | FloatingReset | 3.92 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 14.30 Evaluated at bid price : 14.30 Bid-YTW : 4.14 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| SLF.PR.A | Deemed-Retractible | 50,901 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.61 Bid-YTW : 6.72 % |

| RY.PR.B | Deemed-Retractible | 38,205 | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2022-01-31 Maturity Price : 25.00 Evaluated at bid price : 24.95 Bid-YTW : 4.76 % |

| FTS.PR.G | FixedReset | 31,900 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.24 Evaluated at bid price : 18.24 Bid-YTW : 4.38 % |

| RY.PR.Z | FixedReset | 31,259 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.91 Evaluated at bid price : 18.91 Bid-YTW : 4.38 % |

| PWF.PR.P | FixedReset | 30,060 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 14.53 Evaluated at bid price : 14.53 Bid-YTW : 4.40 % |

| NA.PR.S | FixedReset | 27,763 | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2045-11-24 Maturity Price : 18.90 Evaluated at bid price : 18.90 Bid-YTW : 4.63 % |

| There were 58 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| GWO.PR.Q | Deemed-Retractible | Quote: 23.45 – 24.44 Spot Rate : 0.9900 Average : 0.6712 YTW SCENARIO |

| FTS.PR.G | FixedReset | Quote: 18.24 – 18.62 Spot Rate : 0.3800 Average : 0.2508 YTW SCENARIO |

| CM.PR.O | FixedReset | Quote: 19.30 – 19.65 Spot Rate : 0.3500 Average : 0.2345 YTW SCENARIO |

| HSE.PR.A | FixedReset | Quote: 13.68 – 14.19 Spot Rate : 0.5100 Average : 0.4204 YTW SCENARIO |

| CU.PR.H | Perpetual-Discount | Quote: 23.54 – 23.92 Spot Rate : 0.3800 Average : 0.2910 YTW SCENARIO |

| BAM.PR.Z | FixedReset | Quote: 20.20 – 20.54 Spot Rate : 0.3400 Average : 0.2547 YTW SCENARIO |