The June 2015 Financial System Review released by the Bank of Canada had a few interesting nuggets.

For instance, a chart showing where the negative yields are in Europe:

Click for Big

Click for BigAnd there has been some concern expressed regarding the potential for negative yields on FixedResets, should five-year Canadas be greatly negative at the time of reset. This type of thing is being addressed in Europe:

Nevertheless, crossing the boundary marked by a zero interest rate creates distinct challenges, given the institutional, regulatory and accounting features of markets and contracts. For example, issuing bonds with a negative yield appears inconsistent with setting the issuing price at par value—a common convention—because these bonds would have to offer negative coupons. Collecting coupon payments from investors is probably too costly to be implemented and is unlikely to be accepted by investors. Instead, bonds can be issued at negative market yields if their price is above par. For example, current 1- and 2-year German bunds bear no coupons, but they are sold at a premium above par, implying negative yields to maturity. Similar adjustments may be needed in other markets, including modifications to pricing models for interest rate derivatives and to floating rate notes. For example, European investors are now seeking contractual guarantees that they are not liable to borrowers when floating rates become negative.

There are three things we have to worry about:

Key Vulnerabilities in the Canadian Financial System

The Bank continues to highlight three key areas of vulnerability:

- the elevated level of household indebtedness,

- imbalances in the housing market, and

- illiquidity and investor risk taking in financial markets.

Click for Big

Click for BigIndebted Alberta households have relatively low levels of liquid financial assets, carry more debt and have a higher debt-service ratio than indebted households in other areas of the country (Table 2). Moreover, the proportion of highly indebted households in Alberta—those with a ratio of debt to gross income above 250 per cent—is among the highest in the country. In addition, unlike other provinces in Canada, a sizable proportion of mortgages in Alberta (and Saskatchewan) permit no recourse against individual borrowers in the event of default.[Footnote]

Footnote reads: Creditors holding non-recourse mortgage loans are prevented from seizing other assets or incomes from borrowers in the event of a default if the proceeds from the sale of the house are not sufficient to pay off the loan and associated legal costs. Generally, mortgages to individuals that have a low loan-to-value ratio in Alberta and all mortgages in Saskatchewan are non-recourse loans while, in the rest of Canada, all mortgages are full-recourse loans. In Alberta, for example, about 35 per cent of mortgage loans held by federally regulated lenders are uninsured and non-recourse.

I hadn’t know that! Well, who knows … maybe the American custom of “jingle-mail” will make it to the Prairies!

Meanwhile fears of increasing policy yields have Canadians shortening term on their borrowing. Look, I know this makes no sense. Don’t blame me.

Click for Big

Click for BigAnd finally we get to my favourite topic:

Liquidity in fixed-income markets has become less reliable

Market liquidity has become less consistent in Canadian fixed-income markets, in both the government and corporate sectors, and could deteriorate rapidly during a financial stress event. While volatility may be gradually returning to more normal levels as a result of fundamental factors, a deterioration in market liquidity could amplify volatility if a large number of investors tried to unwind their positions in the same manner at the same time. This could lead to large investor losses and reduce investor confidence.

Certain trends observed in Canadian fixed-income markets are likely reducing market liquidity. First, the investor base in these markets has shifted. In particular, investment funds such as exchange-traded funds and mutual funds are now more important participants in the Canadian corporate bond market.[Footnote 17] In normal times, these funds hold sufficient cash buffers to cover investor redemptions. However, large redemptions may force funds to sell their assets, and the lack of market liquidity could intensify price movements. Bank of Canada analysis suggests that Canadian open-end mutual funds hold adequate amounts of cash buffers, which, coupled with low leverage, pose a limited risk of large sell-offs.[Footnote 18]

Similarly, foreign investors now hold a larger share of the Canadian federal government bond market. As such, a domestic shock could be the catalyst for a rapid sell-off of these bonds. If a sell-off were accompanied by a decline in market liquidity, it could cause discontinuous price movements.

However, many of the investors are foreign central banks and sovereign wealth funds, which tend to be patient, buy-and-hold investors aiming to diversify their portfolios. Their holdings therefore tend to be more stable. Second, market-making activity is evolving, owing to regulations and other changes in market structure, such as the growth in electronic trading in bond markets. Internationally and in Canada, the Basel III requirements compel institutions to hold more high-quality liquid assets. While these requirements should make banks more resilient to liquidity stress, they have reduced the willingness of banks to commit capital to make markets in fixed-income instruments.

[Footnote 17]: For example, mutual fund holdings of non-government bonds have increased from 7 per cent of outstanding bonds at the end of 2004 to 11 per cent at the end of 2014.

[Footnote 18]: For more details, see S. Ramirez, J. Sierra Jimenez and J. Witmer, “Canadian Open-End Mutual Funds: An Assessment of Potential Vulnerabilities,” in this report.

The report referenced in Footnote 18 is summarized as:

- Mutual funds provide retail investors with access to a broad range of investment opportunities. Globally, mutual funds have grown considerably in recent years and have become important players in many securities markets, prompting regulatory interest in vulnerabilities that could emanate from the sector.

- This report finds that vulnerabilities arising from Canadian mutual funds are currently limited:

- (i) Funds hold an adequate amount of cash, given the underlying liquidity of their investments, and have a stable investor base, limiting risks from liquidity and maturity transformation.

- (ii) Since the degree of leverage held by a fund is restricted by securities regulation, funds have low leverage ratios and limited derivatives exposures.

- (iii) Even the largest funds are not dominant players in the securities markets in which they invest.

Click for Big

Click for BigI think fund investors should be upset about the high proportion of cash in fixed income funds. Ten percent cash holdings is a bloody expensive liquidity buffer!

Click for Big

Click for BigThe average fixed-income fund keeps enough cash and equivalents to cover unusually large redemptions.[Footnote 10] In addition, Canadian mutual funds have a predominantly retail investor base that is focused mostly on long-term investing.[Footnote 11] Although it is theoretically possible, for example, for all investors in Canadian fixed income funds to redeem their shares en masse, Canadian fixed-income flows have been stable during past periods of stress (Chart 4).[Footnote 12]

[Footnote 10]: In 2013, the average fixed-income fund held about 10 per cent of its assets in cash equivalents, while only 5 per cent of fixed-income funds experienced monthly outflows greater than 6 per cent of their assets, on average, during this period.

[Footnote 11: During the financial crisis, institutional U.S. money market funds experienced more outflows than retail funds did during the run on the Reserve Primary Fund in September 2008 (McCabe 2010; Schmidt, Timmermann and Wermers 2014).

[Footnote 12: Chart 4 shows measures at the 5th and 95th percentiles of net flows across fixed-income funds for each month, together with industry total flows. For example, in December 2012 the 5th percentile of net flows was -4.2 per cent, indicating that 5 per cent of fixed-income funds had net flows less than -4.2 per cent (i.e., net outflows greater than 4.2 per cent) in that month.

Part of their conclusion reads:

Since fixed-income mutual funds represent a non-negligible proportion of Canadian corporate and government fixed-income markets, a sell-off triggered by outflows could, at least in principle, cause significant price volatility in these markets. Nevertheless, redemption behaviour during past periods of stress was contained, suggesting that this potential vulnerability is limited. Finally, although many Canadian fund management firms are affiliated with a major bank, these banks are unlikely to suffer losses from stress in any of the management firm’s funds, since funds and their management firms are separate legal entities and there is no implicit expectation that a long-term mutual fund’s price would be supported to maintain a certain value.

While that conclusion is mostly true, I suggest a reference to the disgusting precedent set by the regulatory response to the Asset-Backed Commercial Paper blow-up in the summer of 2007 would have been in order.

Meanwhile, a lot of US homeowners are still underwater:

It’s the one chart that keeps Stan Humphries up at night.

A decade after U.S. home sales peaked, 15.4 percent of owners in the first quarter owed more on their mortgages than their properties were worth, according to a report Friday by Zillow Inc. While that’s down from a high of 31.4 percent in 2012, it’s still alarmingly above the 1 or 2 percent that marks a healthy market, said Humphries, the chief economist at the Seattle-based real-estate data provider. Worse yet: The pace of healing is losing steam.

The blotch stains the economy by restraining the housing recovery and by preventing the job market from becoming even more vigorous. It also will probably exacerbate wealth inequality for years to come as homes valued in the bottom third of the market are more likely to be underwater.

Some more figures would be interesting; if I was underwater on my home, I’d consider any money spent paying down the mortgage to be so much money wasted; I’d want to know how my minimum required mortgage payment compared to rent.

A highly technical Fed research note by Andrew Figura and David Ratner titled The Labor Share of Income and Equilibrium Unemployment makes a very interesting point:

We argue that the recent secular decline in the labor share (shown in Figure 3) has been driven by structural factors that also tend to raise the vacancy-unemployment (V-U) ratio, and that this has, in turn, served to reduce the equilibrium unemployment rate. As shown in Figure 3, the labor share of income has moved noticeably below levels that prevailed until the early 2000s (see Elsby, Hobijn, and Şahin (2013) and Karabarbounis and Nieman (2014) for recent work on the labor share).2 Smoothing through some of the volatility in the data, the labor share has declined by roughly 6.5 percentage points since the early 2000s and now hovers around 63 percent. Through the lens of a standard labor market model, we argue that if the decline in the labor share has been driven by a reduction in worker bargaining power, the incentive for firms to post vacancies has increased and equilibrium unemployment will be lower as a result.

…

Going back to Figure 4, our results suggest that as the labor share has declined, the JC has rotated counterclockwise. Mapping this estimate into an effect on the unemployment rate, however, requires an estimate of the slope of the Beveridge curve. To derive an estimate, we regress log vacancies on log unemployment, allowing for a break in the intercept beginning in 2009. Our estimated coefficient suggests that a one percent increase in the V-U ratio along a BC will lead to about a one-half percent decrease in the unemployment rate. Thus, when combined with the 30% increase in the V-U ratio estimated above, we find the lower labor share would reduce the equilibrium unemployment rate by 15%, or by around two-thirds of a percentage point from an initial equilibrium unemployment rate of 5%.

Click for Big

Click for BigTheir argument is not just out of my field but, as I said, highly technical … so I’ll leave commentary on the matter up to the economists out there! Journalists Craig Torres and Jordan Yadoo of Bloomberg comment:

Next week, Federal Reserve officials publish new quarterly forecasts, and all eyes are going to be on where they set the job market’s Goldilocks rate.

That’s the estimated unemployment level officials figure is neither too high nor so low that it starts to drive wages and prices higher. To quote Goldilocks, it’s “just right.”

Fed officials in March estimated this “natural rate” of unemployment at 5 percent to 5.2 percent. Unemployment stood at 5.5 percent in May. A new paper by Fed board staff shakes up this view by suggesting the number could be as low as 4.3 percent.

That has implications for next week’s Fed policy meeting. If Fed Board economists Andrew Figura and David Ratner are right, the labor market has room to run. So there may be no need to raise interest rates soon, or fast.

…

Even if Fed officials do raise the benchmark lending rate in September, as about half the economists in a Bloomberg News survey this month expect, the research suggests the pace of tightening will be slow.

“It could mean that one percentage point of tightening per year is too steep in a world where” the rate of full employment is 4.25 percent, [chief U.S. economist at Barclays in New York Michael] Gapen said.

On the other hand consumers have lots of sentiment:

Bigger paychecks are giving American consumers reason to believe again.

The University of Michigan’s preliminary consumer sentiment index for June rose to 94.6, topping all estimates in a Bloomberg survey of economists, from a reading of 90.7 last month, figures showed Friday. Households were the most upbeat about their wage prospects in seven years.

As the ranks of the unemployed shrink, the competition for skilled workers is heating up and forcing employers to boost wages to attract and retain staff. Firming confidence makes it likely the recent pickup in consumer spending, which accounts for almost 70 percent of the economy, will be sustained.

Meanwhile, the Dimon – Warren pissing match continues:

U.S. Senator Elizabeth Warren shot back at criticism from JPMorgan Chase & Co. Chief Executive Officer Jamie Dimon, saying bankers don’t dislike her because she knows too little but because she knows too much.

“The problem for these guys is that I fully understand the system and I understand how they make their money, and that’s what they don’t like about me,” Warren told the Huffington Post in a podcast interview released Friday.

I reported on Round 1 of the battle on June 10.

I mentioned whispers of a decline in junk bond credit quality yesterday. Here’s another tidbit for the legions of doom:

U.S. junk-bond defaults rose to the highest level since October 2009 as depressed prices plague energy, metal and mining issuers that represent the largest contingent of debt from the riskiest companies.

There were nine defaults in May, including iron processor Magnetation LLC and Patriot Coal Corp., according to Fitch Ratings, with energy and metals and mining companies accounting for all of them. The two industries comprised 93 percent of defaults in the second quarter.

The Bloomberg Commodity Index of 22 raw materials has lost 25 percent in the past year, with the price of a barrel of oil plummeting by nearly half and iron falling by as much as a third.

Calgary housing is looking interesting, if not chaotic. On the one hand the high-end is tumbling:

Nationally, home prices rose 0.9 per cent from April, and 4.6 per cent from a year earlier.

Notable in that annual measure were a 7.6-per cent surge in Toronto, a 6.2-per-cent jump in Vancouver, and a similar rise in Hamilton.

“The 0.9-per-cent rise was slightly below the May average of 1.1 per cent over the last 14 years,” senior economist Marc Pinsonneault said in releasing the numbers.

“This was because Calgary prices fell 3.3 per cent from April, the largest monthly drop recorded for that region, subtracting 0.3 percentage points from the gain of the composite index,” he added.

On the other hand, condominiums are getting built:

As the population of Calgary continues its steep incline, the city’s downtown core is bracing itself for an influx of high-rise condominium developments to house its ever-increasing number of professionals.

In the city’s Beltline neighbourhood, the population has risen consistently by about 4 per cent a year between 2010 and 2014 according to the official city of Calgary census.

…

With a population increase of over 130,000 in five years, the Beltline and other downtown residential districts are prime candidates for large-scale condominiums, and the city’s continual growth, as well as its economic and socio-economic atmosphere, have attracted the eye of many Toronto-based developers.

In the past few years, firms such as Tribute Communities, Lamb Development Corp., and Great Gulf have been exploring the Calgary market for investment and development opportunities.

A Globe story on community mailboxes has brought to the fore my puzzlement over the issue:

Once Canada Post phases out door-to-door service across the country in favour of a new generation of CMBs, every neighbourhood, no matter how dense, will face the same problem: How many of these boxes will be needed – and where will they be installed?

Toronto residents will get their first look at that process next week, when city council’s planning and transportation committee considers an initial report on mailbox-location guidelines.

…

But when those estimates are extrapolated to the scale of the city as a whole, the numbers become formidable, indeed. The estimates to date vary widely. Canada Post estimates that it will have to deploy 2,500 to 11,000 CMBs across Toronto, as the Crown corporation ends door-to-door delivery by 2019. But according to the city’s staff report, Canada Post between 2017 and 2019 expects 565,784 “points of call” (i.e. individual delivery addresses) to be converted to community mailboxes – a figure that would require more than 35,000 new boxes. Residents who live in basement apartments, duplexes or laneway homes will also have their own slots in the boxes. Just over 22,000 downtown residential addresses will continue to get door-to-door delivery.

I don’t understand the issue, frankly. Look, if a postman cannot physically deliver enough mail to make it worth paying him, something has to change – I get it! Let’s say an individual postie has to deliver X pieces of mail every hour to make it worthwhile; for the sake of an argument, let’s say X = 1000.

So fine, out in the suburbs where he has to walk at least fifty feet between houses, he can only deliver 400 pieces per hour on the average day. To me, the obvious solution is to cut back to twice-weekly delivery. Then, on the two days delivery, he’ll hit the 1,000 piece threshold and we’re all happy. What comes in the mail, anyway? Bills and magazines. Nothing that can’t wait a day or two.

Eventually, once you’ve cut back to once a week delivery and you’re still below the 1,000 piece/hour threshold, that’s when you bring in a community box. But the way it stands, we’re all losing all service, regardless of whether we’re on a rural route or in the older sections of town where lot sizes are 20-feet frontage and there’s lots of businesses getting lots of mail. It makes no sense to me.

And, by the way, when Canada Post surveys you asking which of a few locations you think are good for your box, I have it on good authority that you should pick the spot furthest away. Apparently the area turns into a zoo when people come home from work at the same time and stop at the box on their way home. Lots of traffic, lots of mess, lots of aggravation.

It was, as usual, another poor day for the Canadian preferred share market, with PerpetualDiscounts down 37bp, FixedResets off 21bp and DeemedRetractibles flat. This is getting depressing. The Performance Highlights table is notable for its complement of FixedReset losers. Volume was very low; I assume everybody’s waiting for PrefLetter.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

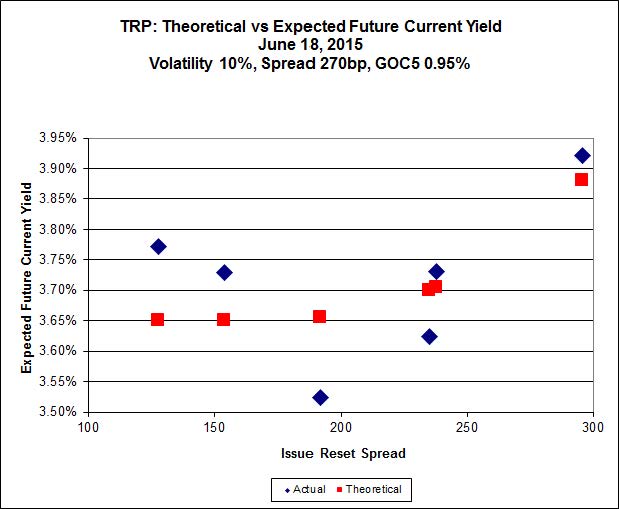

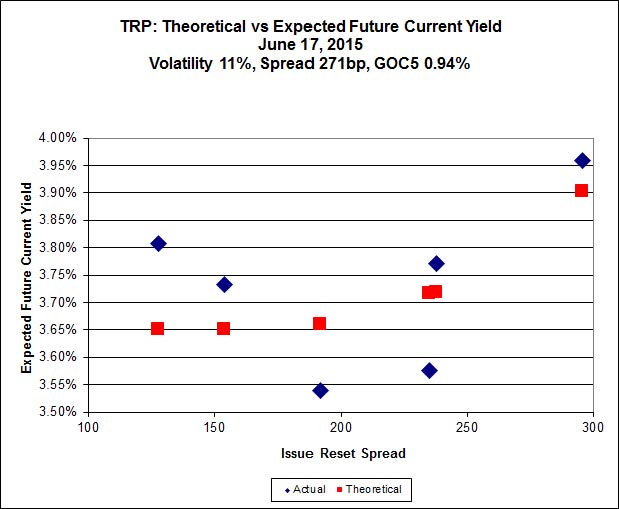

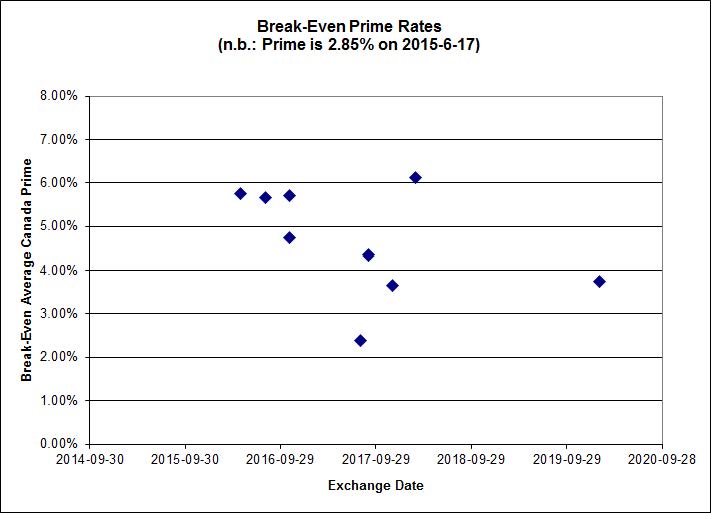

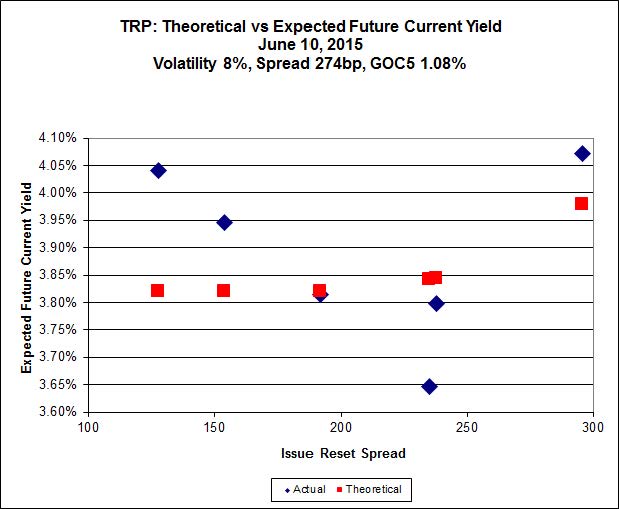

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 22.52 after horrible, worst-on-the-board performance today, to be $0.52 rich, while TRP.PR.B, which will reset June 30 at 2.152% (+128), is $0.49 cheap at its bid price of 14.61

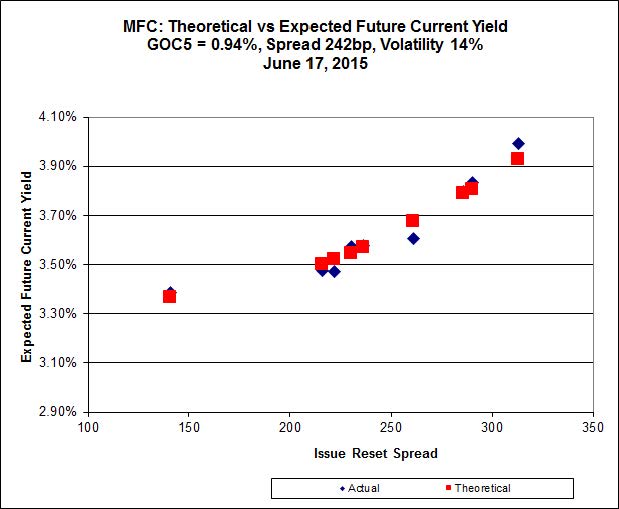

Click for Big

Click for BigAnother excellent fit, but the numbers are perplexing. Implied Volatility for MFC continues to be a conundrum. It is still too high if we consider that NVCC rules will never apply to these issues; it is still too low if we consider them to be NVCC non-compliant issues (and therefore with Deemed Maturities in the call schedule).

Most expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 23.63 to be $0.40 rich, while MFC.PR.H, resetting at +313bp on 2017-3-19, is bid at 25.36 to be $0.49 cheap.

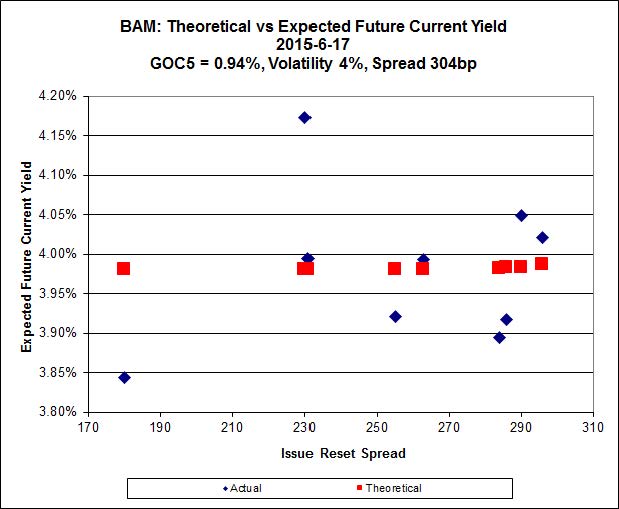

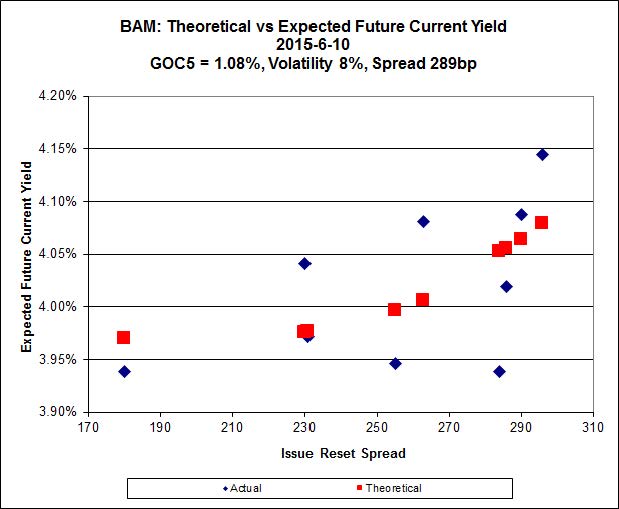

Click for Big

Click for BigThe cheapest issue relative to its peers is BAM.PF.B, resetting at +263bp on 2019-3-31, bid at 22.00 to be $0.66 cheap. BAM.PF.G, resetting at +284bp 2020-6-30 is bid at 24.40 and appears to be $0.53 rich.

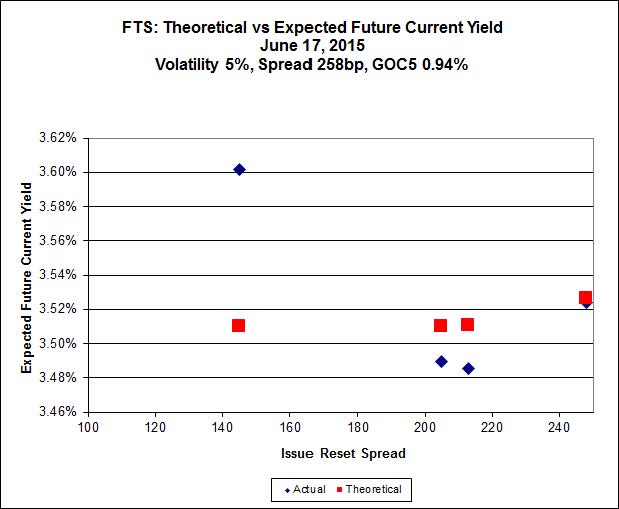

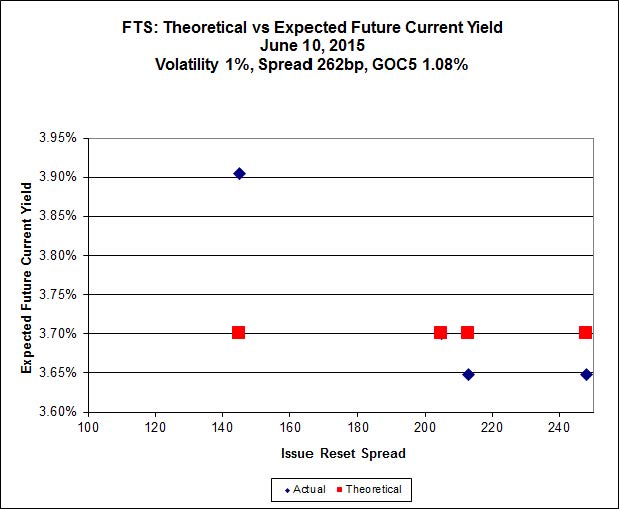

Click for Big

Click for BigFTS.PR.H, with a spread of +145bp, and bid at 16.25, looks $0.72 cheap and resets 2020-6-1. FTS.PR.M, with a spread of +248bp and resetting 2019-12-1, is bid at 24.40 and is $0.30 rich.

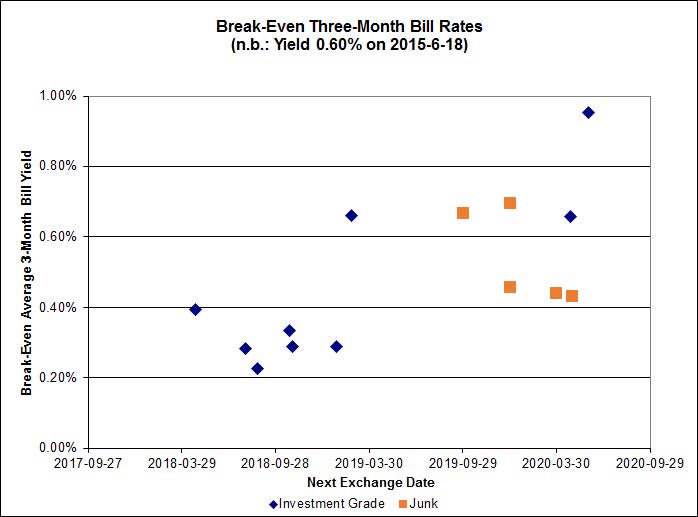

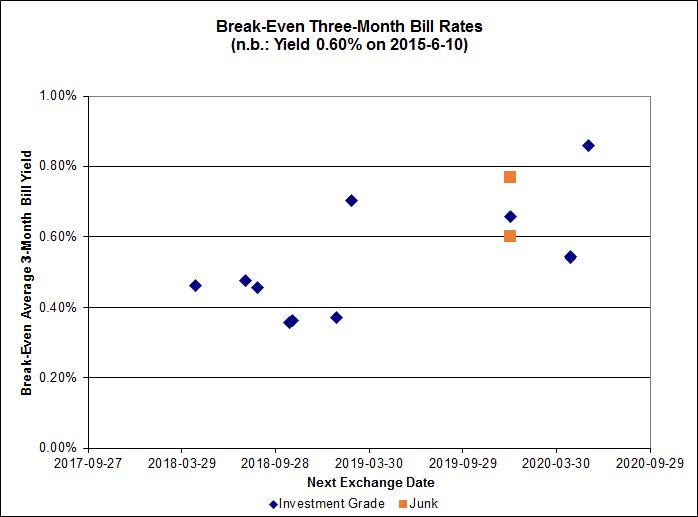

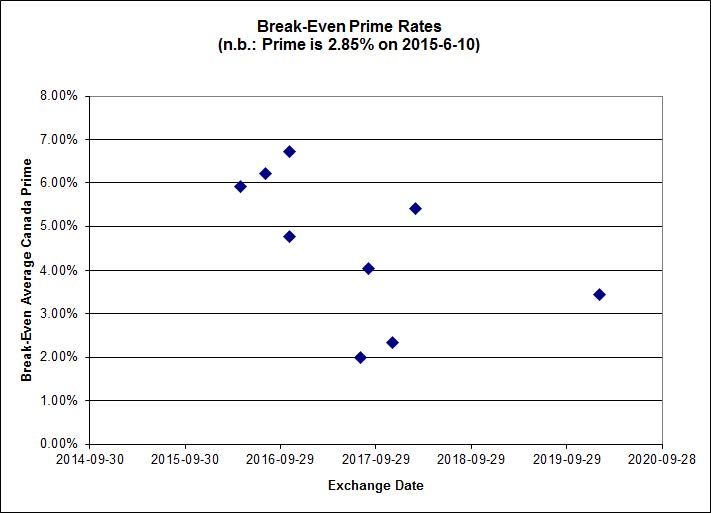

Click for Big

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of about 0.50%, with no ridiculous outliers. On the junk side, three out of the six pairs are outside the range of the graph: FFH.PR.E / FFH.PR.F at -1.16%; AIM.PR.A / AIM.PR.B at -0.38%; and DC.PR.B / DC.PR.D at -1.14%.

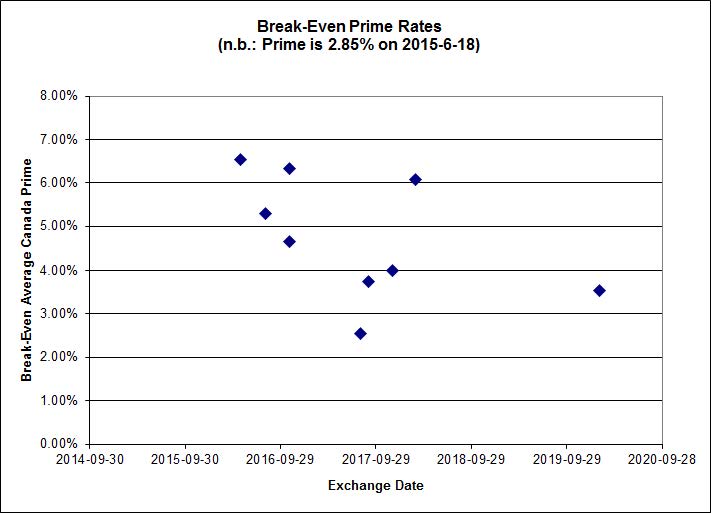

Click for Big

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.5533 % |

2,257.8 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.5533 % |

3,947.6 |

| Floater |

3.43 % |

3.41 % |

62,008 |

18.74 |

3 |

0.5533 % |

2,400.2 |

| OpRet |

4.44 % |

-12.14 % |

26,450 |

0.08 |

2 |

0.0000 % |

2,782.9 |

| SplitShare |

4.59 % |

4.83 % |

71,089 |

3.30 |

3 |

-0.0268 % |

3,248.8 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0000 % |

2,544.7 |

| Perpetual-Premium |

5.46 % |

4.91 % |

59,798 |

4.93 |

19 |

-0.0166 % |

2,513.0 |

| Perpetual-Discount |

5.12 % |

5.12 % |

105,361 |

15.24 |

15 |

-0.3681 % |

2,744.0 |

| FixedReset |

4.50 % |

3.89 % |

244,128 |

16.46 |

87 |

-0.2134 % |

2,354.6 |

| Deemed-Retractible |

5.01 % |

3.30 % |

107,705 |

0.69 |

34 |

0.0000 % |

2,621.3 |

| FloatingReset |

2.52 % |

2.89 % |

54,524 |

6.12 |

9 |

0.0591 % |

2,335.3 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TRP.PR.E |

FixedReset |

-3.76 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 22.02

Evaluated at bid price : 22.52

Bid-YTW : 3.95 % |

| MFC.PR.L |

FixedReset |

-3.17 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.30

Bid-YTW : 4.93 % |

| BAM.PF.D |

Perpetual-Discount |

-2.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.98

Evaluated at bid price : 22.32

Bid-YTW : 5.49 % |

| TRP.PR.D |

FixedReset |

-2.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.70

Evaluated at bid price : 22.01

Bid-YTW : 4.00 % |

| IFC.PR.C |

FixedReset |

-2.12 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.50

Bid-YTW : 4.50 % |

| BAM.PR.N |

Perpetual-Discount |

-1.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.62

Evaluated at bid price : 21.62

Bid-YTW : 5.51 % |

| BAM.PR.M |

Perpetual-Discount |

-1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.35

Evaluated at bid price : 21.63

Bid-YTW : 5.49 % |

| ENB.PR.H |

FixedReset |

-1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 17.23

Evaluated at bid price : 17.23

Bid-YTW : 4.79 % |

| BAM.PF.C |

Perpetual-Discount |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.87

Evaluated at bid price : 22.15

Bid-YTW : 5.48 % |

| BNS.PR.Y |

FixedReset |

-1.12 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.94

Bid-YTW : 3.30 % |

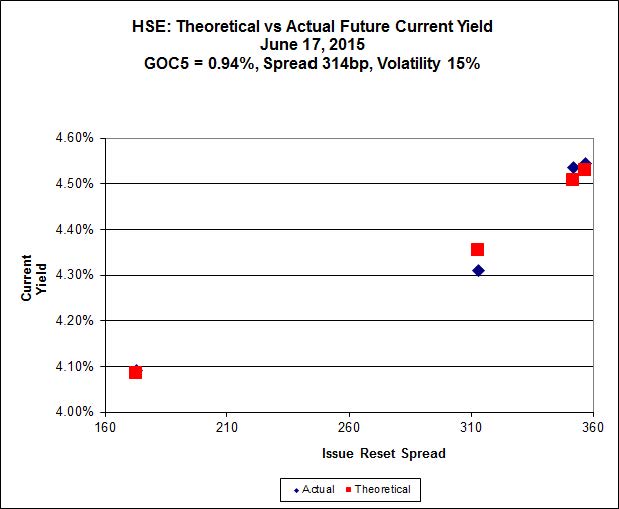

| HSE.PR.A |

FixedReset |

-1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 15.92

Evaluated at bid price : 15.92

Bid-YTW : 4.43 % |

| ENB.PR.P |

FixedReset |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 18.62

Evaluated at bid price : 18.62

Bid-YTW : 4.87 % |

| FTS.PR.K |

FixedReset |

1.00 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.20

Evaluated at bid price : 21.20

Bid-YTW : 3.83 % |

| RY.PR.M |

FixedReset |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 22.99

Evaluated at bid price : 24.60

Bid-YTW : 3.62 % |

| BAM.PR.K |

Floater |

1.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 14.58

Evaluated at bid price : 14.58

Bid-YTW : 3.41 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BMO.PR.Y |

FixedReset |

133,295 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 23.04

Evaluated at bid price : 24.69

Bid-YTW : 3.68 % |

| MFC.PR.I |

FixedReset |

58,700 |

RBC crossed 50,000 at 25.02.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 25.05

Bid-YTW : 3.98 % |

| TRP.PR.G |

FixedReset |

57,150 |

RBC crossed 50,000 at 24.88.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 23.08

Evaluated at bid price : 24.85

Bid-YTW : 3.84 % |

| PWF.PR.R |

Perpetual-Premium |

37,064 |

Nesbitt crossed 25,000 at 26.05.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-04-30

Maturity Price : 25.00

Evaluated at bid price : 26.05

Bid-YTW : 4.83 % |

| PWF.PR.P |

FixedReset |

32,000 |

RBC crossed 25,000 at 18.55.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 18.35

Evaluated at bid price : 18.35

Bid-YTW : 3.69 % |

| RY.PR.N |

Perpetual-Discount |

31,200 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2024-11-24

Maturity Price : 25.00

Evaluated at bid price : 25.11

Bid-YTW : 4.88 % |

| There were 14 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| MFC.PR.L |

FixedReset |

Quote: 22.30 – 23.25

Spot Rate : 0.9500

Average : 0.6185

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.30

Bid-YTW : 4.93 % |

| TRP.PR.E |

FixedReset |

Quote: 22.52 – 23.30

Spot Rate : 0.7800

Average : 0.5132

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 22.02

Evaluated at bid price : 22.52

Bid-YTW : 3.95 % |

| TRP.PR.D |

FixedReset |

Quote: 22.01 – 22.66

Spot Rate : 0.6500

Average : 0.4235

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 21.70

Evaluated at bid price : 22.01

Bid-YTW : 4.00 % |

| MFC.PR.M |

FixedReset |

Quote: 23.63 – 24.10

Spot Rate : 0.4700

Average : 0.3401

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.63

Bid-YTW : 4.34 % |

| BMO.PR.T |

FixedReset |

Quote: 23.41 – 23.85

Spot Rate : 0.4400

Average : 0.3147

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 22.55

Evaluated at bid price : 23.41

Bid-YTW : 3.56 % |

| BAM.PR.T |

FixedReset |

Quote: 20.83 – 21.20

Spot Rate : 0.3700

Average : 0.2490

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-06-12

Maturity Price : 20.83

Evaluated at bid price : 20.83

Bid-YTW : 4.13 % |