The hot news today was an unexpectedly high inflation number:

Inflation exceeded the Bank of Canada’s target last month for the first time in more than two years, an unexpected acceleration led by energy costs that sparked increases in the currency and bond yields.

The consumer price index rose 2.3 percent in May from a year ago following April’s 2 percent pace, Statistics Canada said today from Ottawa. The core rate, which excludes eight volatile products, increased 1.7 percent after a gain of 1.4 percent the prior month. Both increases were higher than all forecasts in Bloomberg economist surveys that called for total inflation of 2 percent and core prices to rise 1.5 percent.

Which had an effect on policy expectations which had an effect on the dollar:

The loonie, nicknamed for the image of the aquatic bird on the C$1 coin, appreciated 0.6 percent to C$1.0758 per U.S. dollar at 5 p.m. in Toronto. It touched C$1.0752, the strongest since Jan. 7, after weakening on March 20 to C$1.1279. One loonie buys 92.95 U.S. cents. The Canadian dollar gained 0.9 percent this week in its second five-day advance.

The currency is the top performer for the past three months in a basket of 10 developed-market currencies tracked by the Bloomberg Correlation Weighted Index, strengthening 4.5 percent. It has lost 2 percent this year.

…

The Canadian government’s two-year note dropped, pushing the yield to as high as 1.15 percent, the most since Jan. 6. Benchmark 10-year bond yields rose as much as seven basis points, or 0.07 percentage point, the most since March 19, to 2.33 percent before trading at 2.29 percent. The 2.5 percent security maturing in June 2024 lost 29 cents to C$101.84.

…

The yield on June 2015 bankers’ acceptance contracts reached 1.46 percent today, the highest since April 4, suggesting investors are moving up their expected date for the Bank of Canada to begin raising interest rates.

David Parkinson of the Globe dismisses Exchange Rate Pass Through (ERPT) as the rationale:

Meanwhile, one has to wonder how long “exchange-rate pass-through” should be expected to distort the inflation trend. The Canadian dollar did fall more than 10 cents against its U.S. counterpart in the span of a year – but for the past five months the currency has actually been stable, in the 90 to 92 cents (U.S.) range. Certainly it would take a while for last year’s decline in the loonie to work its way fully through pricing for imported goods (and goods dependent on imported inputs), but presumably the impact should already be softening in the month-to-month numbers as the currency continues to hold its footing. Yet on a month-to-month basis, core CPI was up 0.5 per cent (unadjusted for seasonal effects) in May, in a month when the dollar actually rose.

The BoC has lots of research that suggests ERPT is not really all that important. F’rinstance, a 2004 review by Jeannine Bailliu and Hafedh Bouakez titled Exchange Rate Pass-Through in Industrialized Countries:

• Although estimates of exchange rate passthrough vary both by industry and by country, it appears that the full effect of a depreciation or appreciation of the domestic currency is not passed through to local currency import prices across industrialized countries.

- • Many industrialized countries seem to have experienced a decline in exchange rate passthrough to consumer prices in the 1990s, despite large exchange rate depreciations in many of them.

- • The fact that this documented decline in exchange rate pass-through has coincided with the low-inflation period that most industrialized countries entered a decade or so ago has popularized the view that these two phenomena could be linked.

- • Assessing the extent of exchange rate passthrough, and whether it has indeed declined, has important implications for the conduct and design of monetary policy.

…

Assuming for a moment that the prices of domestically produced goods do not respond to exchange rate changes, there are at least two reasons why passthrough to consumer prices might not equal the share of imports in the consumption basket even if passthrough to import prices is complete. First, local distribution costs, such as transportation costs, marketing, and services, will cause import and consumer prices to diverge, and the wedge between the two prices will fluctuate if distributors adjust their profit margins in response to movements in the exchange rate. Second, as discussed in Bacchetta and vanWincoop (2002), differences in the optimal pricing strategies of foreign wholesalers and domestic retailers can explain why pass-through to consumer prices is lower than the share of imports in the CPI even when pass-through to import prices is complete. Indeed, this discrepancy can occur if foreign exporting firms price their goods in the exporter’s currency, while domestic retailers resell these goods priced in domestic currency

… and Stephen Murchison’s October 2009 paper Exchange Rate Pass-through and Monetary Policy: How Strong is the Link?:

Several authors have presented reduced-form evidence suggesting that the degree of exchange rate pass-through to the consumer price index has declined in Canada since the early 1980s and is currently close to zero. Taylor (2000) suggests that this phenomenon, which has been observed for several other countries, may be due to a change in the behaviour of inflation. Specifically, moving from a high to a low-inflation environment has reduced the expected persistence of cost changes and, by consequence, the degree of pass-through to prices. This paper extends his argument, suggesting that this change in persistence is due to a change in the parameters of the central bank’s policy rule. Evidence is presented for Canada indicating that policy has responded more aggressively to inflation deviations over the low pass-through period relative to the high pass-through period. We test the quantitative importance of this change in policy for exchange rate pass-through by varying the parameters of a simple monetary policy rule embedded in an open economy, dynamic stochastic general equilibrium model. Results suggest that increases in the aggressiveness of policy consistent with that observed for Canada are sufficient to effectively eliminate measured pass-through. However, this conclusion depends critically on the inclusion of price-mark-up shocks in the model. When these are excluded, a more modest decline to pass-through is predicted.

… and a review by Jeannine Bailliu, Wei Dong and John Murray titled Has Exchange Rate Pass-Through Really Declined? Some Recent Insights from the Literature:

- • A substantial empirical literature has shown that the correlation between changes in consumer prices and changes in the nominal exchange rate has been quite low and declining over the past two decades for a broad group of countries.

- • The issue of exchange rate pass-through (ERPT) has recently been explored more fully in the context of sticky-price, open-economy, dynamic stochastic general-equilibrium (DSGE) models. The findings of these studies put into question results from previous work based on reduced-form equations. In particular, ERPT to import prices may remain larger than the estimated parameters from

reduced-form regressions would indicate, owing to an econometric bias related to the endogeneity of the exchange rate.- • Nevertheless, there is fairly convincing evidence to suggest that measured short-term ERPT to consumer prices has declined because of a shift to more credible monetary policy regimes, and, in this case, the findings from DSGE models confirm the results of reduced-form models.

- • Studies using microdata are a promising area of research, since they provide additional insights that help us to better understand the phenomenon of ERPT by providing evidence of some of its drivers at the micro level.

…

If the price of an imported good rises because of a depreciation, domestic importers may simply switch suppliers. This would be measured as low pass-through, even though pass-through may be complete.

…

As discussed by Bacchetta and van Wincoop (2003), the insensitivity of consumer prices to changes in the exchange rate may be the outcome of an optimal strategy from the retailer’s perspective. Indeed, when there is rising competition in the local market, it may be optimal for retailers to absorb some of the fluctuations in the exchange rate into their margins, regardless of the sensitivity of border prices to exchange rates. Moreover, when there is limited substitution between non-tradable goods and imported goods, the prices of non-tradable goods can be very sticky, even after large exchange rate movements, leading to very little response in aggregate consumer prices.

… and a paper by Abdul ALEEM and Amine LAHIANI from 2010, Monetary Policy Credibility and Exchange Rate Pass-Through: Some evidence from Emerging Countries:

Considering external constraints on monetary policy in emerging countries, we propose a vector autoregressive model with exogenous variables (VARX) to examine the exchange rate pass-through to domestic prices. We demonstrate that a lower exchange rate pass-through is associated with a credible monetary policy aiming at price stability. The empirical results suggest that the exchange rate pass-through is higher in Latin American countries than in East Asian countries. The exchange rate pass-through has declined after the adoption of inflation targeting monetary policy.

All this talk of distributors and retailers absorbing exchange rate fluctuations is fascinating in view of the federal government’s musing on price controls:

Minister Flaherty has once again proven that the Competition Act is vulnerable to politically expedient amendments developed to respond to perceived exploitative conduct. Following on statements in the 2013 Throne Speech, Minister Flaherty indicated in the 2014 Budget that the government will introduce legislation to address geographic price discrimination “that is not justified by higher operating costs in Canada, and to empower the Commissioner of Competition to enforce the new framework.” While Canadians will not know what this really means until the proposed legislation is disclosed, the language in the 2014 Economic Action Plan suggests the Commissioner of Competition may become a price regulator in addition to its role as enforcer of Canada’s competition law.

The 2014 Budget tabled in Parliament on February 11 states that the Harper government

“proposes to address another source of the price gap identified by the Senate Committee: country pricing strategies—that is, when companies use their market power to charge higher prices in Canada that are not reflective of legitimate higher costs. Evidence suggests that some companies charge higher prices in Canada than in the U.S. for the same goods, beyond what could be justified by higher operating costs. Higher prices brought on by excessive market power hurt Canadian consumers.

The Government intends to introduce legislation to address price discrimination that is not justified by higher operating costs in Canada, and to empower the Commissioner of Competition to enforce the new framework. Details will be announced in the coming months.”

Not surprisingly, there was no mention of this mechanism in the Pack of Useless Hacks, Has-Beens and Bag-Men’s report The Canada-USA Price Gap, although it seems to me that if distribution/retail margins are reduced when purchasing power goes down, then distribution/retail margins should be _____________ when purchasing power goes up. [Fill in the blank: Three Marks]

The government’s plan was attacked by my old school buddy Andrew Coyne:

You might have wondered quite how this mad scheme could have been produced by a government that occasionally proclaims its belief in a free market economy, but only if you had not been paying attention: This was simply the latest expression of how far populism has displaced market liberalism in the Conservatives’ thinking. Still, this was taking things, as they say, to another level: an expensive, bureaucratic muddle that, on its own, would undo much of whatever good the late Jim Flaherty might have achieved in his time at Finance.

But don’t take my word on it. The C.D. Howe Institute has just released a report, drawing on the advice of a panel of the country’s foremost competition policy experts. They include three former directors of investigation at the Competition Bureau, a former Commissioner of Competition, as well as leading economists and practitioners in competition law. Their conclusion: the plan is “profoundly wrong-headed,” “wholly impractical,” “misguided” and “unenforceable” and probably illegal under international trade law. In sum, they said, it was “destined for costly failure” and “should be abandoned forthwith.”

…

It is, in sum, a thoroughgoing policy debacle in the making; the government would do well to heed to the panel’s advice, and deep-six it. Will it? Or will it once again treat overwhelming expert opposition to one of its policies as evidence, not that the policy is wrong, but that the experts are biased against it?

In other news, retail sales increased:

This came as a separate reading by the agency showed Canadian shoppers out in force in April, as retail sales climbed 1.1 per cent, driven by cars and car parts.

Still, the gains across Canada were exceptionally broad-based, with sales up in 10 of 11 sectors measured, or 98 per cent.

“The advance in retail volumes is welcome news, and suggest Canadian consumers are bouncing back after a tepid first quarter,” said senior economist Krishen Rangasamy of National Bank.

“The overall picture for April is good, with a trifecta of volume gains in retailing, wholesaling and manufacturing, enough in our view to prop up GDP by around 0.2 per cent in the month.”

Bloomberg carries an interesting exchange of views on High-Frequency Trading. In his piece Slow Your Judgments on Fast Trading, Noah Smith conflates slippage and market impact, claiming that:

Slippage, also called implementation shortfall, is the difference between the price that triggers the decision to trade and the actual execution price. It matters for people who use market orders, or the best immediate price. Price impact matters to people who split their trades into pieces.

This, not to put too fine a point on it, is bullshit. From the links:

slippage is the difference between where the computer signaled the entry and exit for a trade and where actual clients, with actual money, entered and exited the market using the computer’s signals.[1] Market-impacted, liquidity, and frictional costs may also contribute.

and

market impact is the effect that a market participant has when it buys or sells an asset. It is the extent to which the buying or selling moves the price against the buyer or seller, i.e. upward when buying and downward when selling. It is closely related to market liquidity; in many cases “liquidity” and “market impact” are synonymous.

So it should be clear that “slippage” is almost always merely bafflegab spouted by useless pseudo-quants of the ‘Look mummy, I gotta spreadsheet’ school of investing. Any trading decision is binary: you either do it or you don’t do it, given the market prices. If a properly written quantitative investment programme tells you it would be a good thing if you sold A and bought B at a take-out of $1.00 and no less, you can’t do the trade at $0.95 and then whimper to your gullible clients about “slippage”. If you can do some of the desired trade at a take-out of $1.00 or better, great! If the market impact of the first part of your trade moves the take-out to $0.95, YOU DON’T FUCKEN DO THE SECOND PART OF THE TRADE!

There is only sequence of events for which I can imagine “slippage” being a legitimate concept. Exchange trades are independent; you can’t make one contingent on another – you can do this with a dealer, but then he’s going to be building in a margin. So it is possible that you see your take-out of $1.00, execute your sale of A, and then be chagrined to learn that the offer of B you were counting on doesn’t exist any more, leaving you with the grim choice of buying back your A (almost certainly at a loss), or gritting your teeth and executing the purchase of B at the higher price anyway. This can be minimized by algorithmic trading, with which you can execute the two sides of the trade with as little time separation as possible, and by reducing your trade sizes to minimize the harmful impact of such a disappearance … and note that the latter strategy might give HFT the signals it needs to scoop things up, so be careful!

So “slippage” is not another word for “implementation shortfall”. “Slippage” is, in fact, another word for “gross incompetence”. And, in fact, the cited paper by Jones defines:

These price impacts can be measured by looking at the response of share prices to a particular trade. However, the preferred trading cost measure for institutions is known as implementation shortfall. It is calculated as the average execution price for the large order compared to the price of the stock prior to the start of execution. As with spreads, implementation shortfalls are usually calculated on a proportional basis relative to the amount traded, and implementation shortfall is usually reported in basis points.

This definition is OK, but brings with it the potential for more incompetent bafflegab. Let us say we are competent investment managers running assets as well as we can. “A” can be swapped into “B” on favourable terms with a take-out of $1.05, but we don’t do it, because we’re looking for $1.10. Suddenly there’s a discontinuity in the market – a policy announcement, or a large trade or new issue somewhere changes the overall pricing in an entire sector, could be anything – and our desired take-out changes to $1.00, even though the relative prices of A and B haven’t changed. Hurray! We’re generating a trade signal, so let’s get to work … we do half the desired trade size at $1.05, but then our price impact moves the price to takeout of $0.95. So what do you do?

If you are a moron, you do the other half at $0.95, and then ring up your mummy and tell her you just did a gigantic trade at an average take-out of your desired $1.00. If you are a reasonably rational person (not employed by a bank, obviously), you stop trading, satisfied that you did half the trade at better than necessary prices, and recommence running your programme, hoping for another opportunity. You don’t do a trade on unfavourable terms just because the price ten minutes ago, with your portfolio as of ten minutes ago, was favourable. That’s just stupid.

So the moral of the story is: let’s ignore Noah Smith’s use of the word slippage and see if his essay makes any sense with proper terminology.

As it turns out, it doesn’t really matter: one of the major assertions in his essay Slow Your Judgments on Fast Trading is:

If HFTs have big speed advantages and very good guesses about the decisions of non-HFT investors, they might theoretically be able to increase slippage and price impact for non-HFTs. That would increase total trading costs for non-HFTs, thus discouraging them from trading. If non-HFTs are bringing important information to the market by their trading, then the net effect of HFT could reduce the informational efficiency of markets.

…

But a word of caution — the decrease in slippage and price impact might be happening because informed traders are now staying out of the market in response to HFT itself. If that’s happening, it isn’t a reason for celebration — it’s like saying the Spanish flu decreased the death rate from heart disease. The problem is that it’s very hard, if not impossible, to tell how much information is getting pumped into market prices via trading. The increase in the use of dark pools might be the result of informed traders fleeing the public exchanges in an effort to escape HFTs.

OK, so yes, it is possible for an HFT to increase the price impact of the first moiety of my trade at $1.05; I could do a portion at $1.05, but before I can do my second portion at $1.04, HFT swoops in and the take-out is suddenly $0.95, even though I’ve traded a quarter of my desired size when in the absence of HFT I could have done half. The problem with his reasoning is the next sentence:

That would increase total trading costs for non-HFTs, thus discouraging them from trading.

No, it doesn’t increase total trading costs for all non-HFTs; it only increases the trading costs for morons, who insist on doing all their trade, even at prices that don’t make sense any more. It certainly doesn’t increase my trading costs; it might even be said to decrease them, since I did one-quarter of my desired trade at 1.05, instead of half at an average take-out of $1.045.

It would have been nicer, of course, to have scooped up all the available trade, but that’s my fault. If I had been a little quicker, a little smarter, then I actually would have scooped up everything available; but as it was, my sluggishness and stupidity gave HFT the opportunity the chance to (i) read my signal, (ii) interpret my signal and (iii) get his own trade in. So my clients are less happy than they might otherwise be and his clients are happier than they might otherwise be, and this has come about because he was smarter than me (this time!). And that’s exactly the way it should be. I see no problems here. I’ll just have to get better at what I do.

In his counterpoint Why I Love High-Speed Trading, Clifford S. Asness makes some very good points:

Smith’s lead point is that I claim HFTs don’t front-run because I used an outdated definition of the term. That is, I take “front-running” to mean using information you’ve been entrusted with and promised not to use to the disadvantage of whoever entrusted that information to you (usually a paying client). Smith says the definition must be broadened to encompass “order anticipation with speed advantages.” Therefore, he says, it is legitimate to say that HFTs engage in front-running.

He’s wrong. First, you can’t just change the definition of a word used to describe a crime and apply it to something that’s both legal and ethical. Perhaps all of us should have used the more straightforward term “guessing,” because that is all “order anticipation” means. Traders have always made educated guesses about who is going to buy and sell what, and they’ve always tried to do it faster than the other guy. They did this long before HFT. In fact, what are traders doing if not trying to make educated guesses about who plans to buy and sell what and then act before other traders? If these traders — HFT or not — are using legal, public information, this is exactly what they’re supposed to be doing. To say “we’ll call that front-running as we’ve broadened the term” is ridiculous.

Yes, very good. It’s much like the Peter ‘My Word Is My Bond, Sometimes’ MacKay’s attempt to reclassify prostitutes’ clients as “perverts”.

Asness’ other good point is:

But Smith is creative! He advances the untestable hypothesis that perhaps fewer people are bothering to become informed traders because HFTs will just take their profits, and as a result markets are less efficient. As we have pointed out, HFTs shouldn’t be judged against an unattainable nirvana of zero bid-ask spreads and infinite liquidity, but against the system that preceded it. Before the advent of HFTs, human market-makers engaged in order anticipation and moved prices away from large traders all while earning much fatter profits.1 Any informed trader discouraged because potential profits are syphoned away by HFTs would have been even more discouraged under the old trading regime.

Yes, yes and yes again! As I have often pointed out, much of the controversy regarding HFT is fuelled by the pique and despair of the old-money smiley-boy crowd, dismayed that some parvenus are eating their lunch. Since they don’t have the talent to do their jobs properly, they prefer to whine to teacher.

The paper on implementation costs was by Charles M. Jones, by the way, and titled What Do We Know About High-Frequency Trading?:

This paper reviews recent theoretical and empirical research on high-frequency trading (HFT). Economic theory identifies several ways that HFT could affect liquidity. The main positive is that HFT can intermediate trades at lower cost. However, HFT speed could disadvantage other investors, and the resulting adverse selection could reduce market quality.

Over the past decade, HFT has increased sharply, and liquidity has steadily improved. But correlation is not necessarily causation. Empirically, the challenge is to measure the incremental effect of HFT beyond other changes in equity markets. The best papers for this purpose isolate market structure changes that facilitate HFT. Virtually every time a market structure change results in more HFT, liquidity and market quality have improved because liquidity suppliers are better able to adjust their quotes in response to new information.

Does HFT make markets more fragile? In the May 6, 2010 Flash Crash, for example, HFT initially stabilized prices but were eventually overwhelmed, and in liquidating their positions, HFT exacerbated the downturn. This appears to be a generic feature of equity markets: similar events have occurred in manual markets, even with affirmative market-maker obligations. Well-crafted individual stock price limits and trading halts have been introduced since. Similarly, kill switches are a sensible response to the Knight trading episode.

Many of the regulatory issues associated with HFT are the same issues that arose in more manual markets. Now regulators in the US are appropriately relying on competition to minimize abuses. Other regulation is appropriate if there are market failures. For instance, consolidated order-level audit trails are key to robust enforcement. If excessive messages impose negative externalities on others, fees are appropriate. But a message tax may act like a transaction tax, reducing share prices, increasing volatility, and worsening liquidity. Minimum order exposure times would also severely discourage liquidity provision.

And in other, other news, Jed Kolko of Trulia addresses fears that boomer downsizing will devastate house prices in his piece Baby-Boomer Downsizing? Perhaps Not So Fast:

Let’s start by looking at the age when older households move from single-family homes to multi-unit buildings. Based on the 2013 Current Population Survey’s Annual Social and Economic Supplement (CPS ASEC) – the most recent detailed demographic data available – baby boomers (born between 1946 and 1964, which means 50-68 years old in 2014) are less likely than almost any other age group to live in multi-unit buildings as opposed to single-family homes. The only age group less likely to live in multi-unit buildings is 70-74 year-olds, which is the age group that baby boomers will start to enter in the coming years.

In later years, the share of households in multi-unit buildings rises, but by less than you might guess. Just 25% of households headed by 80-84 year-olds live in multi-unit buildings – which is a lower share than 40-44 year-olds. Even among households headed by adults aged 85 and older, only one-third live in multi-unit buildings – and that’s only counting those who head their own household are not living with adult children or in institutions.

Therefore, as today’s baby boomers age, they’ll grow into age groups first with a lower likelihood of living in multi-unit buildings (70-74 year-olds). Multi-unit living starts rising slightly at age 75-79, and rises more notably only when heads of household reach their 80s.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts down 6bp, FixedResets gaining 3bp and DeemedRetractibles off 1bp. Volatility wasn’t much – boosted by Floaters reversing yesterday’s jump. Volume was very low.

| HIMIPref™ Preferred Indices These values reflect the December 2008 revision of the HIMIPref™ Indices Values are provisional and are finalized monthly |

|||||||

| Index | Mean Current Yield (at bid) |

Median YTW |

Median Average Trading Value |

Median Mod Dur (YTW) |

Issues | Day’s Perf. | Index Value |

| Ratchet | 0.00 % | 0.00 % | 0 | 0.00 | 0 | -0.8239 % | 2,479.5 |

| FixedFloater | 4.43 % | 3.68 % | 29,984 | 17.97 | 1 | 0.1401 % | 3,876.9 |

| Floater | 2.96 % | 3.08 % | 44,727 | 19.52 | 4 | -0.8239 % | 2,677.2 |

| OpRet | 4.38 % | -8.59 % | 24,084 | 0.08 | 2 | 0.0779 % | 2,711.1 |

| SplitShare | 4.82 % | 4.30 % | 58,447 | 4.11 | 5 | -0.2307 % | 3,107.8 |

| Interest-Bearing | 0.00 % | 0.00 % | 0 | 0.00 | 0 | 0.0779 % | 2,479.0 |

| Perpetual-Premium | 5.52 % | -0.53 % | 81,978 | 0.08 | 17 | -0.1269 % | 2,404.9 |

| Perpetual-Discount | 5.26 % | 5.27 % | 113,553 | 14.97 | 20 | -0.0621 % | 2,554.4 |

| FixedReset | 4.46 % | 3.70 % | 208,740 | 6.68 | 78 | 0.0327 % | 2,541.6 |

| Deemed-Retractible | 4.99 % | -0.21 % | 132,821 | 0.11 | 43 | -0.0111 % | 2,536.7 |

| FloatingReset | 2.66 % | 2.33 % | 123,702 | 3.95 | 6 | 0.0000 % | 2,499.2 |

| Performance Highlights | |||

| Issue | Index | Change | Notes |

| MFC.PR.B | Deemed-Retractible | -1.93 % | YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 22.91 Bid-YTW : 5.75 % |

| FTS.PR.J | Perpetual-Discount | -1.55 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 23.18 Evaluated at bid price : 23.51 Bid-YTW : 5.08 % |

| BAM.PR.B | Floater | -1.46 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 16.88 Evaluated at bid price : 16.88 Bid-YTW : 3.10 % |

| W.PR.H | Perpetual-Premium | -1.39 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 24.51 Evaluated at bid price : 24.74 Bid-YTW : 5.65 % |

| BAM.PR.K | Floater | -1.34 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 16.90 Evaluated at bid price : 16.90 Bid-YTW : 3.10 % |

| BAM.PR.C | Floater | -1.16 % | YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 17.00 Evaluated at bid price : 17.00 Bid-YTW : 3.08 % |

| Volume Highlights | |||

| Issue | Index | Shares Traded |

Notes |

| RY.PR.H | FixedReset | 362,196 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 23.17 Evaluated at bid price : 25.05 Bid-YTW : 3.75 % |

| TD.PF.A | FixedReset | 314,340 | Recent new issue. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 23.20 Evaluated at bid price : 25.18 Bid-YTW : 3.70 % |

| BAM.PF.F | FixedReset | 62,801 | Recent new issue. YTW SCENARIO Maturity Type : Call Maturity Date : 2019-09-30 Maturity Price : 25.00 Evaluated at bid price : 25.35 Bid-YTW : 4.27 % |

| GWO.PR.N | FixedReset | 57,326 | Desjardins crossed 50,000 at 21.78. YTW SCENARIO Maturity Type : Hard Maturity Maturity Date : 2025-01-31 Maturity Price : 25.00 Evaluated at bid price : 21.50 Bid-YTW : 4.73 % |

| ENB.PR.J | FixedReset | 55,100 | Scotia crossed 48,900 at 25.27. YTW SCENARIO Maturity Type : Limit Maturity Maturity Date : 2044-06-20 Maturity Price : 23.27 Evaluated at bid price : 25.26 Bid-YTW : 4.07 % |

| TD.PR.R | Deemed-Retractible | 32,523 | Scotia crossed 31,100 at 26.45. YTW SCENARIO Maturity Type : Call Maturity Date : 2014-07-20 Maturity Price : 25.75 Evaluated at bid price : 26.43 Bid-YTW : -16.43 % |

| There were 17 other index-included issues trading in excess of 10,000 shares. | |||

| Wide Spread Highlights | ||

| Issue | Index | Quote Data and Yield Notes |

| BAM.PF.A | FixedReset | Quote: 25.55 – 26.24 Spot Rate : 0.6900 Average : 0.4175 YTW SCENARIO |

| MFC.PR.B | Deemed-Retractible | Quote: 22.91 – 23.55 Spot Rate : 0.6400 Average : 0.3998 YTW SCENARIO |

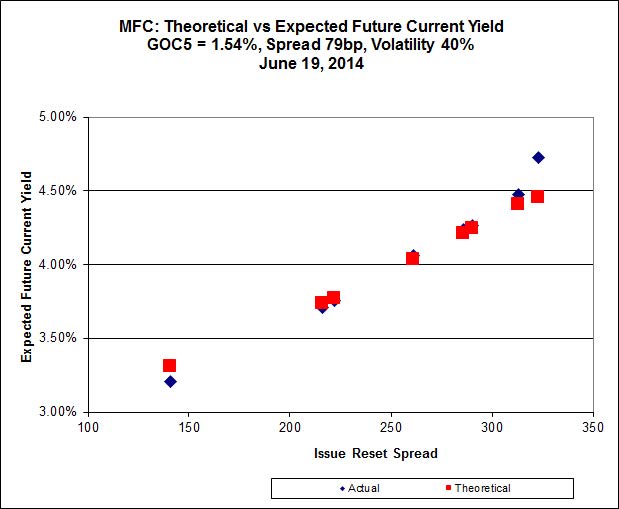

| MFC.PR.F | FixedReset | Quote: 23.00 – 23.65 Spot Rate : 0.6500 Average : 0.5143 YTW SCENARIO |

| FTS.PR.J | Perpetual-Discount | Quote: 23.51 – 23.90 Spot Rate : 0.3900 Average : 0.2645 YTW SCENARIO |

| FTS.PR.H | FixedReset | Quote: 21.40 – 21.75 Spot Rate : 0.3500 Average : 0.2363 YTW SCENARIO |

| W.PR.H | Perpetual-Premium | Quote: 24.74 – 25.10 Spot Rate : 0.3600 Average : 0.2470 YTW SCENARIO |