Today’s post is dedicated to the snivelling cowards who don’t want to take in Syrian refugees because ISIS might get mad at us. Wear one of these on your lapel on future Remembrance Days instead of a poppy:

Click for Big

Click for BigToday’s sick joke has to do with money laundering – Assiduous Readers will recall that here in North America we are spending untold billions of dollars on a regulatory regime that causes massive inconvenience to honest citizens and has, so far, caught the notorious master-criminals Hastert and Switzer, last discussed in detail on October 19. So how does ISIS make its money and move it around? They’ve got a lot of oil and wheat money:

These airstrikes were launched not because U.S. officials were prescient. They came after the Obama administration found and quietly fixed a colossal miscalculation. U.S. intelligence had grossly overestimated the damage they’d inflicted during airstrikes on the militants’ oil production apparatus last year, while underestimating Islamic State’s oil revenue by $400 million. According to U.S. Department of the Treasury officials and data they released in the wake of the Paris mayhem, the terrorist group is actually taking in $500 million from oil a year. What’s more, just a few hours before the first Islamic State suicide bomber blew himself up outside the Stade de France on Nov. 13, U.S. Army Colonel Steve Warren conceded at a press briefing that some American airstrikes disrupted IS oil operations for no more than a day or two.

…

Arguably the least appreciated resource for Islamic State is its fertile farms. Before even starting the engine of a single tractor, the group is believed to have grabbed as much as $200 million in wheat from Iraqi silos alone. Beyond harvested grains, the acreage now controlled by militants across the Tigris and Euphrates river valleys has historically produced half of Syria’s annual wheat crop, about one-third of Iraq’s, and almost 40 percent of Iraqi barley, according to UN agricultural officials and a Syrian economist. Its fields could yield $200 million per year if those crops are sold, even at the cut rates paid on black markets. And how do you conduct airstrikes on farm fields?

But here’s the best part: when ISIS conquers territory in Iraq, the Iraqi government continues to pay the civil service in the area:

ISIS uses adjacent areas not only to access foreign funds, but also to cull money from Iraqi government officials still working in its territory. For example, Baghdad may be paying up to $130 million every month to government workers in Mosul alone.

The city’s formal banking system was shut down after ISIS took over, so “department emissaries are sent into Iraqi or Kurdish territory [to] collect salary money.” When these officials return to disburse the funds, ISIS naturally takes a cut off the top — according to the FATF report, the group “could potentially profit hundreds of millions of USD annually from taxing these salary payments.”

…

The goal here should be strict regulation and transparency, not eliminating all money flows into these border areas.

The latter is neither realistic nor advisable, as a collapsed economy would only worsen the humanitarian crisis and hurt innocent civilians who are effectively ISIS hostages trying to survive one day at a time.

But without greater oversight and control over the flow of funds to areas in the Islamic State’s “near abroad,” the group will continue using backdoors to fund its brutality and terrorism in Syria, Iraq, and elsewhere.

So let’s not hear any more crap about how our Canadian banking regulations are an important element in the fight against terrorism. It’s a joke.

Oh, and while we’re on the topic of Canadian financial regulation, let’s see what Christine Duhaime has to say:

Two weeks from now, I appear before the United Nations law and policy group to discuss the regulation of bitcoin, the blockchain and digital finance, which are at the cutting edge of financial technology.

It’s appropriate that they asked a Canadian lawyer to speak, because we know about balanced financial regulation – 18 months ago, Canada moved to overregulate fintech with the world’s first law governing digital currencies, enacted amid concerns about terrorist financing.

Overnight, we drove away hundreds of millions of investment dollars in fintech from Canada, money that went to Britain instead.

Assiduous Reader JP sends me another interesting link today, bringing the score for the month to date to: JP 2 Youse Other Bums 0. This one is an essay on the corporate savings glut by Martin Wolf of the Financial Times:

In the six largest high-income economies – the US, Japan, Germany, France, the UK and Italy – corporations accounted for between half and just over two-thirds of gross investment in 2013 (the lowest share being in Italy, the highest in Japan).

Because corporations are responsible for such a large share of investment, they are also, in aggregate, the largest users of available savings, but their own retained earnings are also a huge source of savings.

…

If the corporate sector runs a structural surplus of savings over investment, other sectors must run offsetting structural deficits. If the government is to be in financial balance, either households or foreigners must run these deficits.

In the euro zone, this logic has led to huge current account surpluses (a financial deficit for foreigners). For the UK and US, it is likely to mean renewed household deficits – a destabilising possibility.

Why is corporate investment structurally weak? The ageing of societies is one reason: by slowing potential growth, it lowers the level of investment needed.

Globalisation is another: it motivates relocation of investment from the high-income countries. Another reason is technological innovation. Much investment today is in IT, whose price is collapsing: constant nominal investment finances rising real investment. Again, much innovation seems to reduce the need for capital: consider the substitution of warehouses for retail stores. Another explanation could be that management is not rewarded for investing.

Together, all this might explain why, to take the US example, the ratio of corporate investment to profits has declined substantially since 2000.

…

Moreover, if the corporate sector is unable to invest even its own savings, savings in the rest of the economy are bound to have a low marginal value. In such a world, both ultra-low real interest rates and high equity prices are not at all surprising. They are to be expected. So stop complaining.

The Bank of Canada has released the Bank of Canada Review, Autumn 2015, with articles:

- Is Slower Growth the New Normal in Advanced Economies?

- A Survey of Consumer Expectations for Canada

- Measuring Durable Goods and Housing Prices in the CPI: An Empirical Assessment

- The Effect of Regulatory Changes on Monetary Policy Implementation Frameworks

- Recent Enhancements to the Management of Canada’s Foreign Exchange Reserves

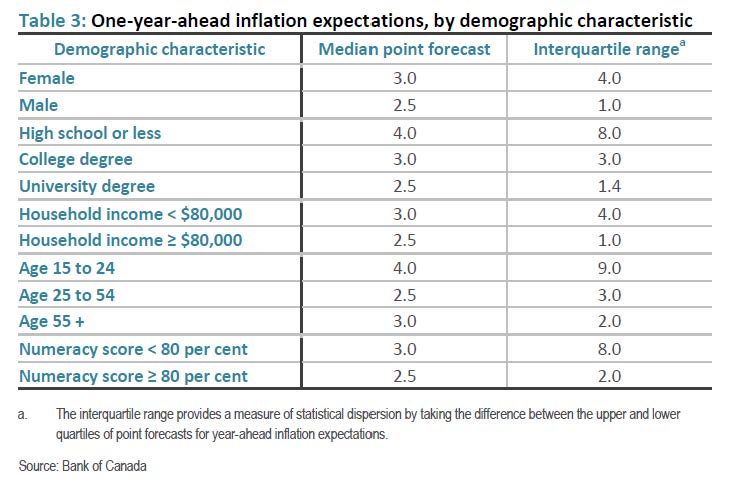

In the article A Survey of Consumer Expectations for Canada, the following table appears:

Click for Big

Click for BigThere have been two new developments in the fascinating Sprott Silver battle. First, the fund is proposing to become an ETF:

The Board of Trustees of Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (C$) (TSX:SBT.U) (US$) announced today that SBT has entered into a letter of intent with Purpose Investments Inc. (“Purpose”) regarding the proposed conversion of SBT into an exchange-traded silver bullion fund (“ETF”). The proposed conversion will involve certain amendments to SBT’s Declaration of Trust that will be subject to approval by SBT unitholders at a special unitholders’ meeting expected to be held by the end of January 2016. The proposal is also subject to the execution of definitive agreements, receipt of regulatory approvals and other customary conditions for transactions of this nature. Full details regarding the proposed conversion and its anticipated benefits will be outlined in a management information circular which will be mailed to unitholders in advance of the proposed special meeting.

Purpose is an independent, employee-owned Canadian investment management company established in January 2013 by Som Seif, founder and former CEO of Claymore Investments, a leading Canadian ETF provider, which was purchased by BlackRock, Inc. in 2012. Purpose, which has current assets under management of over $1.4 billion across 17 funds, is one of Canada’s most experienced ETF managers and has significant experience in managing bullion funds. Purpose and Silver Administrators Limited, SBT’s current administrator, will jointly administer SBT following approval of the conversion by SBT unitholders.

Second, the OSC has ordered enhanced disclosure from Sprott:

Silver Bullion Trust (“SBT”) (TSX:SBT.UN) (C$) (TSX:SBT.U) (US$) announced today that the Ontario Securities Commission (“OSC”) has issued an order requiring Sprott Asset Management Silver Bid LP and certain of its affiliates (collectively, “Sprott”) to issue a notice of change that provides enhanced disclosure to Unitholders regarding the amendments Sprott unilaterally made to the voting powers of attorney solicited by Sprott in connection with its unsolicited offer (the “Sprott Offer”) to acquire all of the units of SBT. The OSC also prohibited Sprott from exercising rights purportedly attaching to the voting powers of attorney before the expiry of 15 days after the notice of change is issued.

The November 4, 2015 Notice of Variation of the Sprott Offer unilaterally amended the intended use of the voting powers of attorney granted by those Unitholders who had tendered to the Sprott Offer. Sprott now intends to use the powers of attorney to replace the independent trustees of SBT, and to elect Sprott insiders as trustees, if more than 50.1% of the outstanding units of SBT are tendered to the Sprott Offer. These powers of attorney were originally intended to be used to replace the trustees if 66 2/3% of the units were tendered to the Sprott Offer to facilitate completion of the Sprott Offer. SBT applied to the OSC for an order, which among other things, would prevent Sprott from using the powers of attorney in this manner, in part because of the lack of proper disclosure about the change of intent. So long as the unsolicited Sprott Offer remains outstanding, Unitholders who have tendered their units will have conveyed their voting rights to Sprott and have forfeited their ability to consider the alternative transaction described below.

The OSC order has been published on the OSC site.

Capital Power is attempting to clean up its structure at the expense of bondholders:

Capital Power Corporation (“Capital Power”) (TSX: CPX) and Capital Power L.P. (“CPLP”) announced today that CPLP has called a meeting of the holders (“CPLP Noteholders”) of issued and outstanding 4.85% Medium Term Notes due February 21, 2019 (“Series 3”) and 5.276% Medium Term Notes due November 16, 2020 (“Series 1”) (collectively, the “CPLP Notes”) of CPLP. The principal amounts outstanding are $250 million for Series 3 and $300 million for Series 1.

The record date for determining CPLP Noteholders entitled to vote at the meeting is November 18, 2015 with the meeting to be held in Toronto on December 17, 2015 at the time set out in the Notice of Meeting. An information circular (“Circular) and related proxy materials will be mailed to CPLP Noteholders and also are available on SEDAR at www.sedar.com.

The meeting has been called to consider passing an extraordinary resolution to authorize CPLP to enter into a supplemental indenture amending the terms of the trust indenture dated April 14, 2010. In accordance with the steps described in the Circular, all issued and outstanding CPLP Notes would be exchanged for an equal principal amount of newly issued medium term notes of Capital Power having financial and other terms that are the same as those attached to the CPLP Notes and benefiting from a guarantee to be provided by CPLP (“Note Exchange Transaction”).

The Note Exchange Transaction and additional steps to reorganize CPLP’s capital structure are being undertaken to simplify the organizational structure and reduce reporting obligations. The cessation of CPLP as a reporting issuer and transition of long-term credit ratings to only Capital Power will result in efficiencies for CPLP while providing noteholders with better liquidity over time and structural enhancement. The timing of the Note Exchange Transaction follows the exchange of all remaining Exchangeable Common Limited Partnership Units of CPLP for shares of Capital Power by EPCOR Power Development Corporation on April 2, 2015.

RBC Capital Markets is the Solicitation Agent for the Note Exchange Transaction and Kingsdale Shareholder Services has been retained to act as Information Agent.

The Information Circular is not yet available, so I’m not sure how much is being paid to brokers for favourable votes from their clients. I have not seen any indication, so far, regarding the effect on the credit ratings of this structural subordination:

The Company’s power generation operations and assets are owned by Capital Power L.P. (CPLP), a subsidiary of the Company. As at December 31, 2014, the Company held 21.750 million general partnership units and 62.112 million common limited partnership units of CPLP which represented approximately 82% of CPLP’s total partnership units. EPCOR (in this MD&A, EPCOR refers to EPCOR Utilities Inc. collectively with its subsidiaries) held 18.841 million exchangeable common limited partnership units of CPLP which represented approximately 18% of CPLP. CPLP’s exchangeable common limited partnership units are exchangeable for common shares of Capital Power Corporation on a one-for-one basis.

Nonetheless, anybody who votes in favour of this arrangement without a sweetener is a fool. The position in the capital structure is worth … something and should not be given up without getting … something.

Big 8 Split Inc., proud issuer of BIG.PR.D (not tracked by HIMIPref™) was confirmed at Pfd-2(low) by DBRS:

DBRS Limited (DBRS) has today confirmed the rating of Class D Preferred Shares, Series 1 (the Preferred Shares) issued by Big 8 Split Inc. (the Company) at Pfd-2 (low).

…

Dividends received from the Portfolio are used to pay fixed cumulative quarterly distributions to holders of the Preferred Shares, yielding 4.50% per annum on the initial issue price of $10.00. The Capital Shares are expected to receive all excess dividend income after the Preferred Share distributions and other Company expenses have been paid. Based on the current dividend yield on the Portfolio, the Preferred Share dividend coverage ratio is approximately 1.5 times, and as such there is no grind on the portfolio.

…

Downside protection available to the Preferred Shares consists of the net asset value of the Capital Shares. As of November 11, 2015, the downside protection was approximately 55.6%.

5Banc Split Inc., proud issuer of FBS.PR.C (tracked by HIMIPref™ but relegated to the Scraps index on volume concerns) has been confirmed at Pfd-2 by DBRS:

DBRS Limited (DBRS) has today confirmed the rating of Class C Preferred Shares, Series 1 (the Preferred Shares) issued by 5Banc Split Inc. (the Company) at Pfd-2.

…

Dividends received from the Portfolio are used to pay a quarterly fixed, cumulative, preferential distribution of $0.11875 per Preferred Share to yield 4.75% per annum. As of November 11, 2015, the downside protection was approximately 69%. Based on the dividend yields on the underlying Portfolio holdings as of November 11, 2015, the Preferred Share dividend coverage ratio is approximately 2.5 times.

Brookfield Renewable announced the exercise of the underwriters’ option for their new issue. I have updated the PrefBlog announcement post.

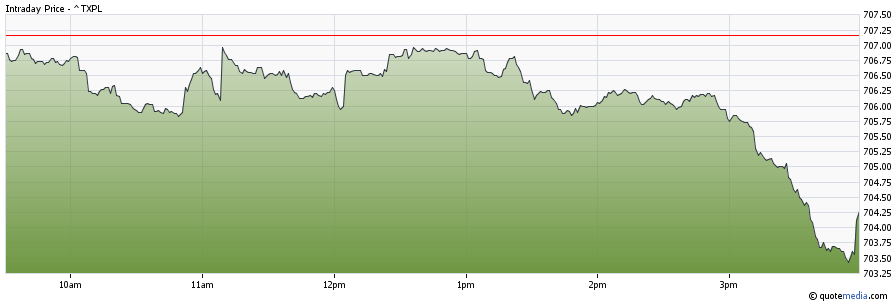

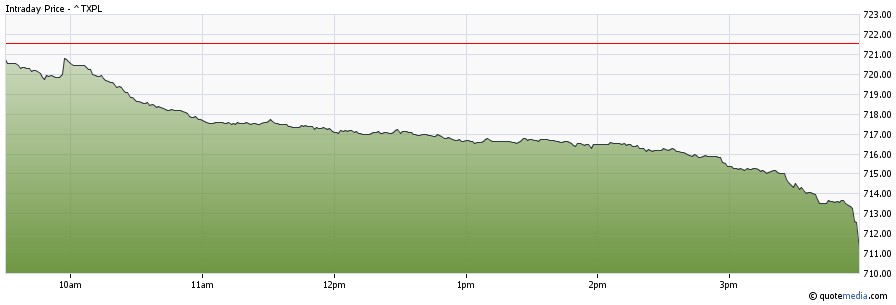

While today’s market swoon was nowhere near as dramatic as yesterday‘s, there was the same pattern of an exaggerated decline at the close, as the TXPL index moved from 708.63 at 3:56pm to 707.16 at the close:

Click for Big

Click for BigIt was a mixed but poor day for the Canadian preferred share market, with PerpetualDiscounts off 19bp, FixedResets down 46bp and DeemedRetractibles gaining 2bp. The Performance Highlights table is ridiculously long. Volume was very high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

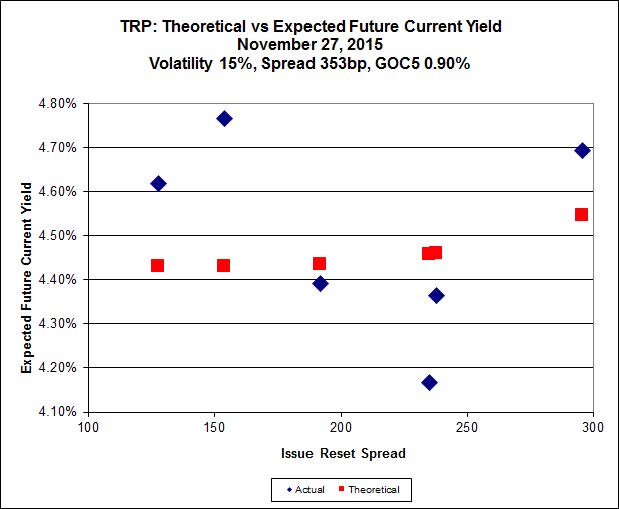

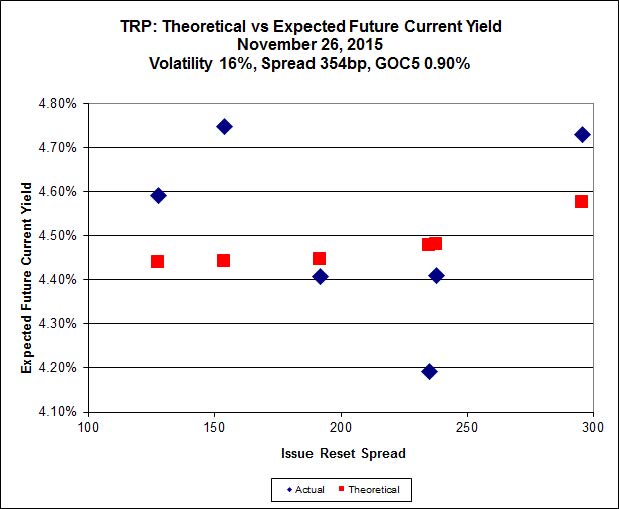

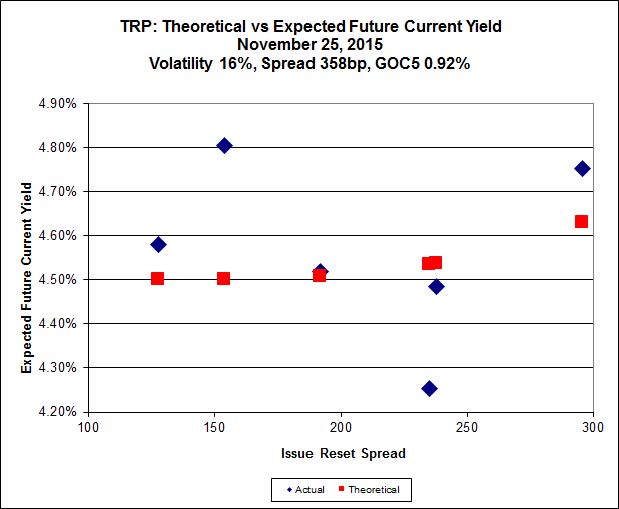

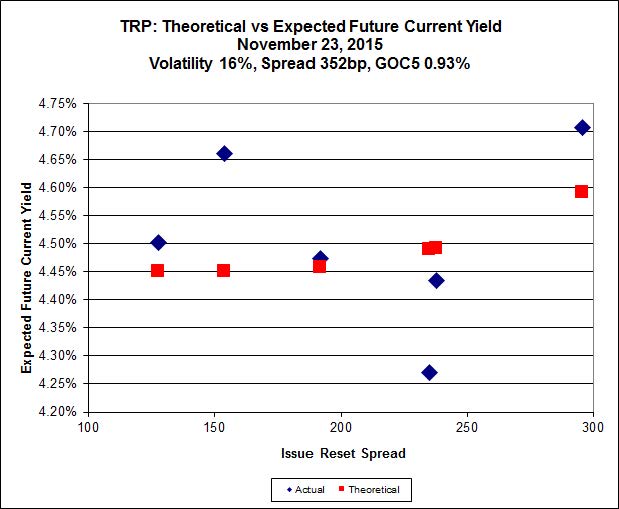

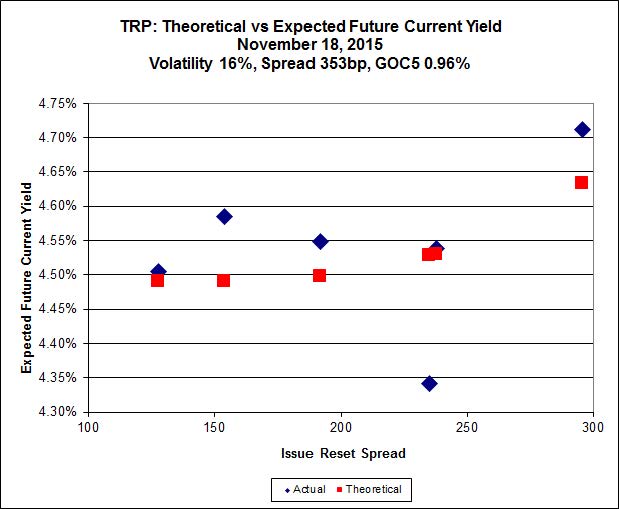

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 19.00 to be $0.82 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $0.59 cheap at its bid price of 13.25.

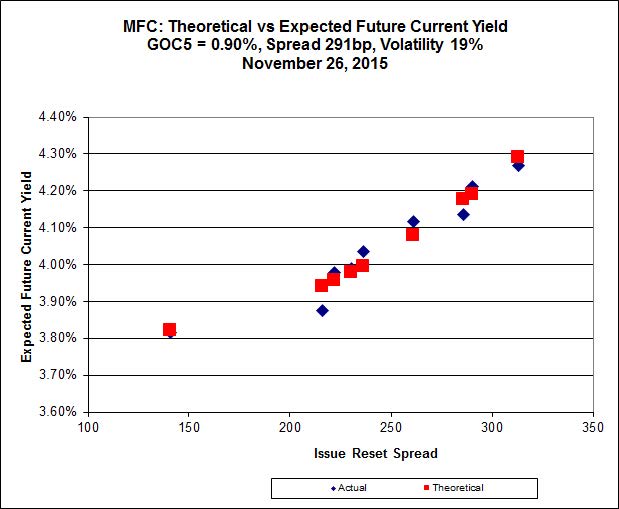

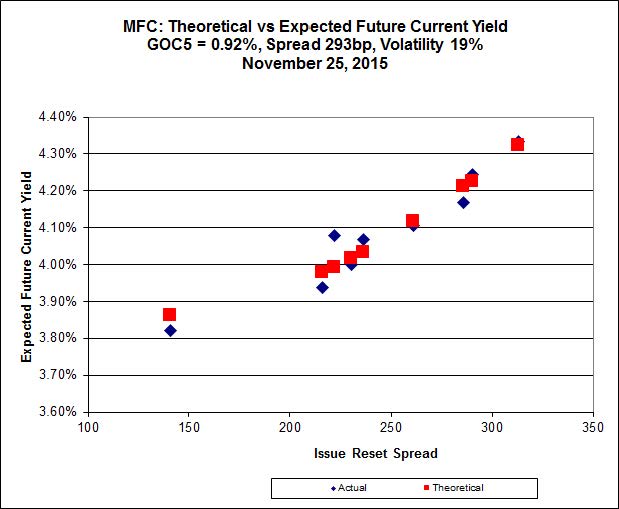

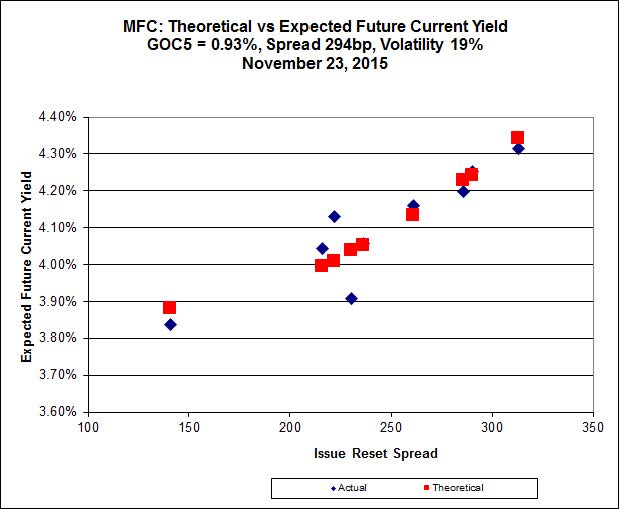

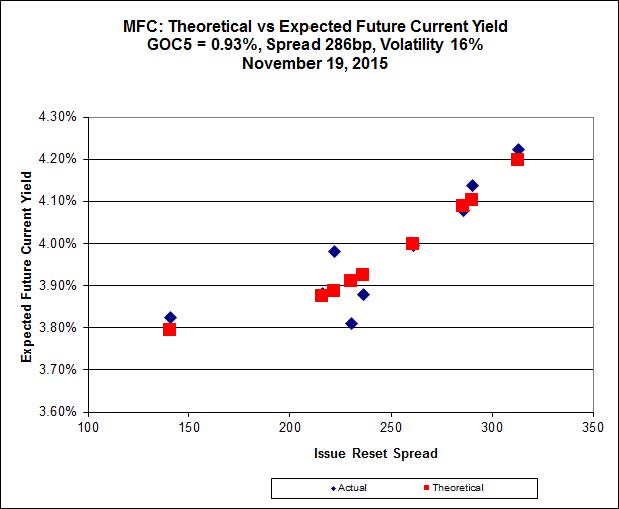

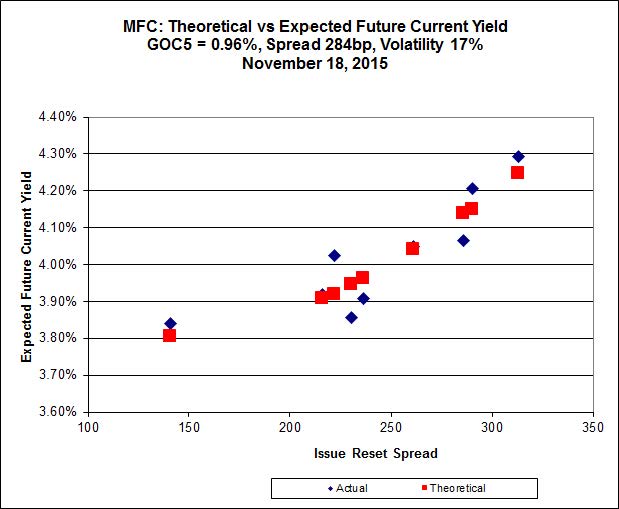

Click for Big

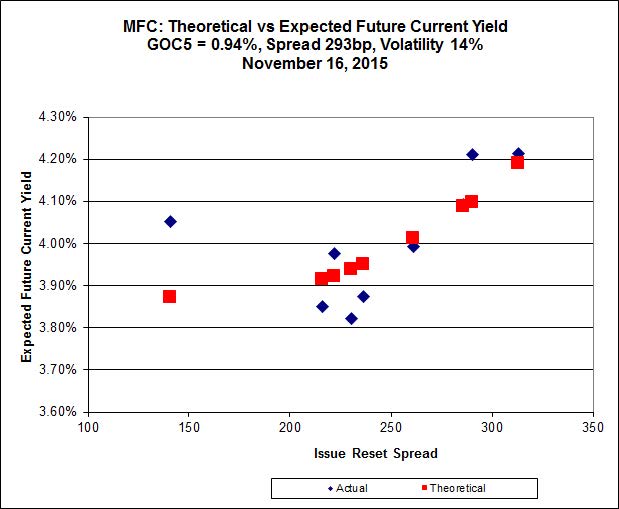

Click for BigMost expensive is MFC.PR.N, resetting at +230bp on 2020-3-19, bid at 21.20 to be 0.54 rich, while MFC.PR.K resetting at +222bp on 2018-9-19, is bid at 19.78 to be 0.49 cheap.

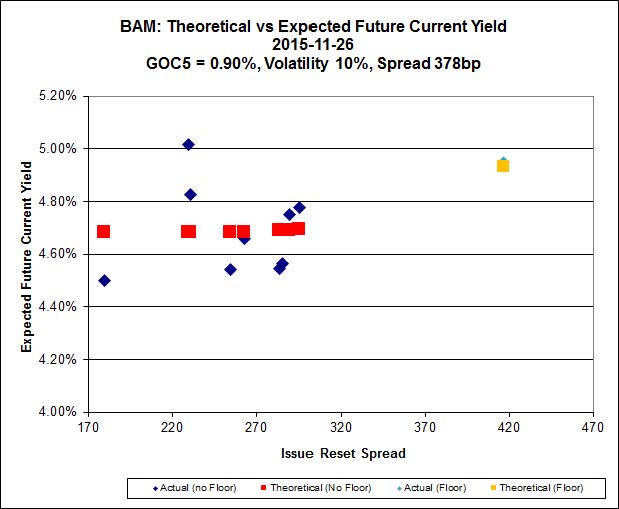

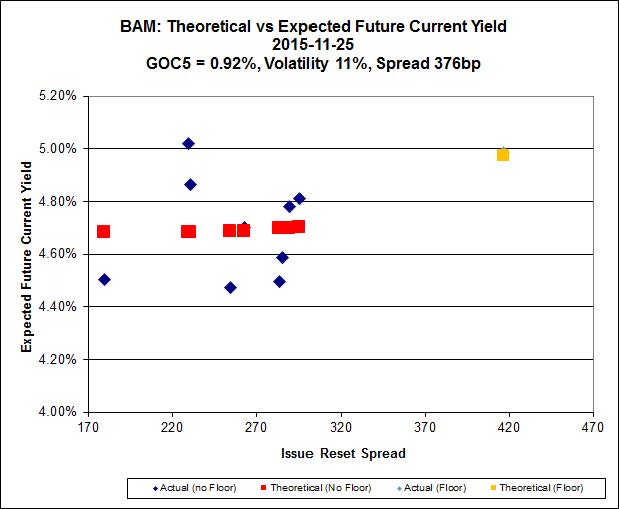

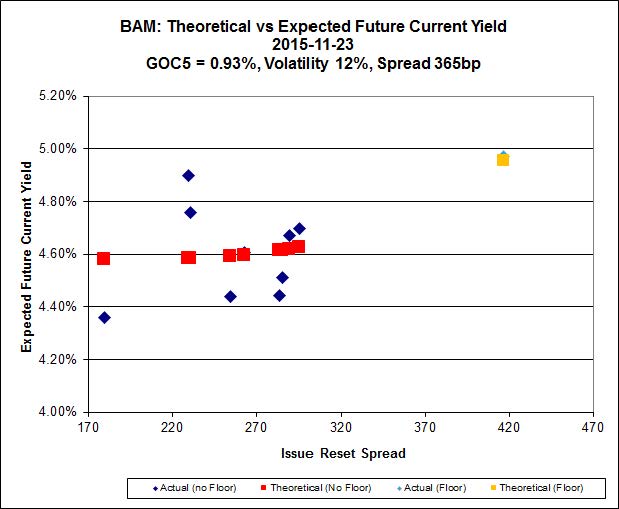

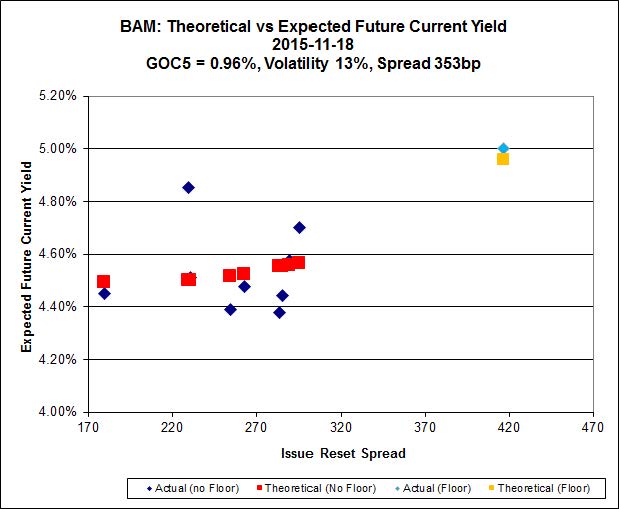

Click for Big

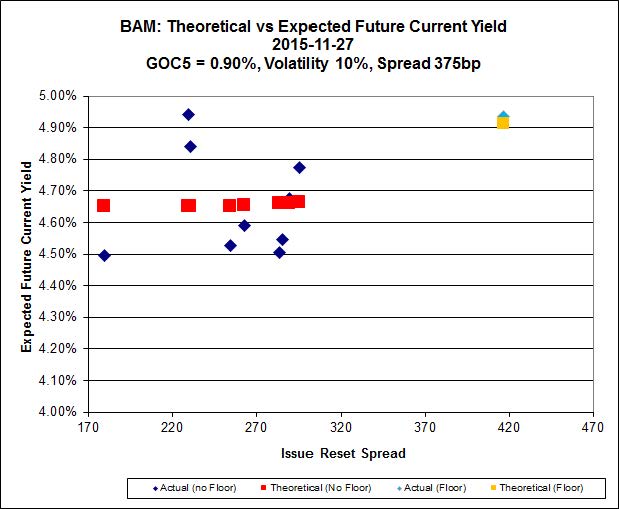

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.79 to be $1.21 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 21.50 and appears to be $0.73 rich.

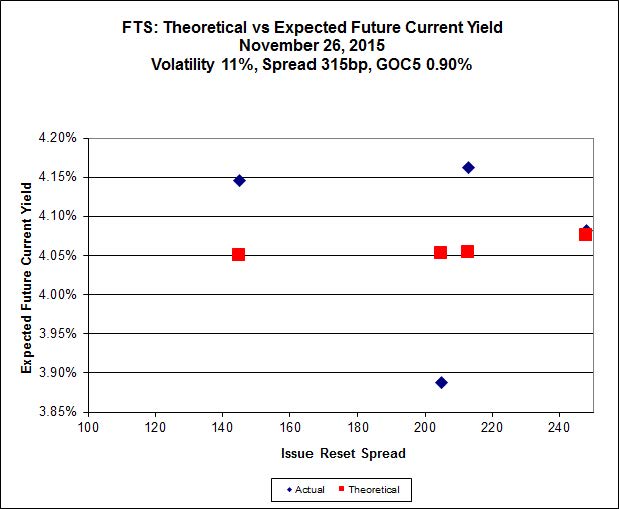

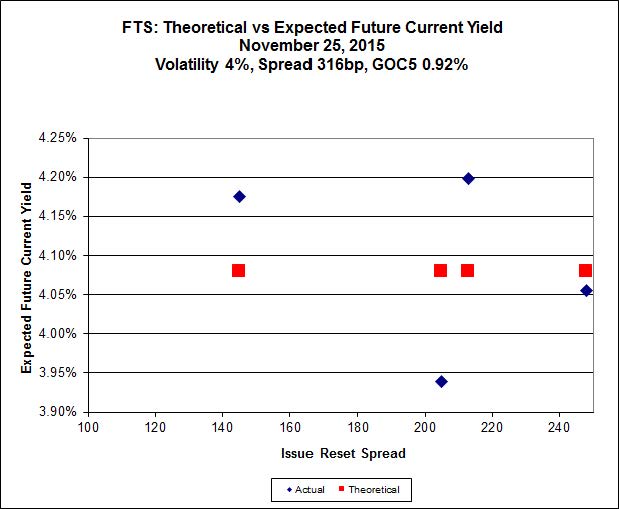

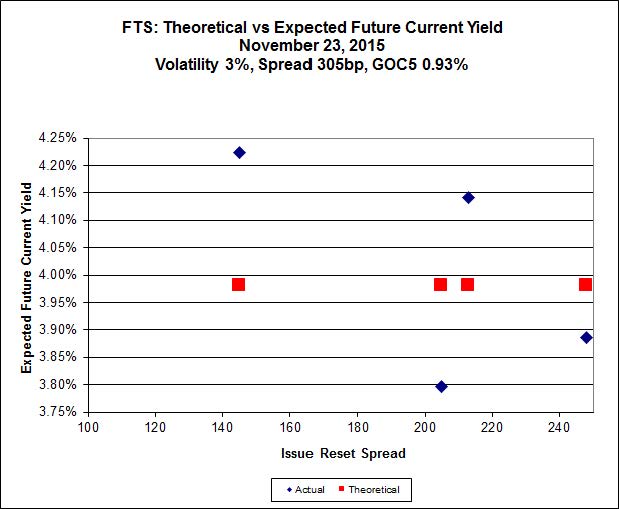

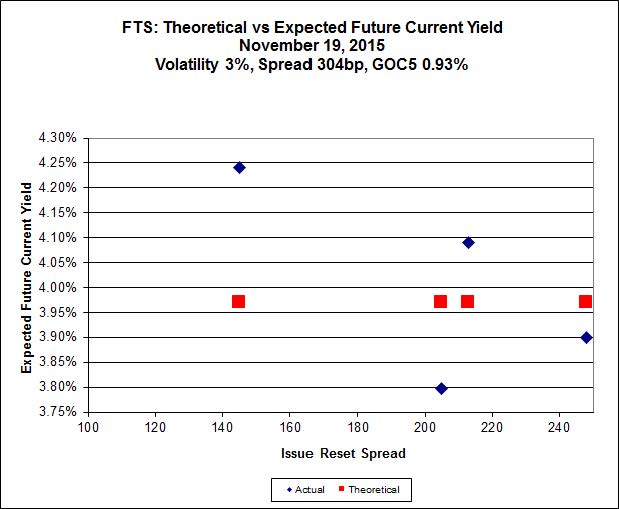

Click for Big

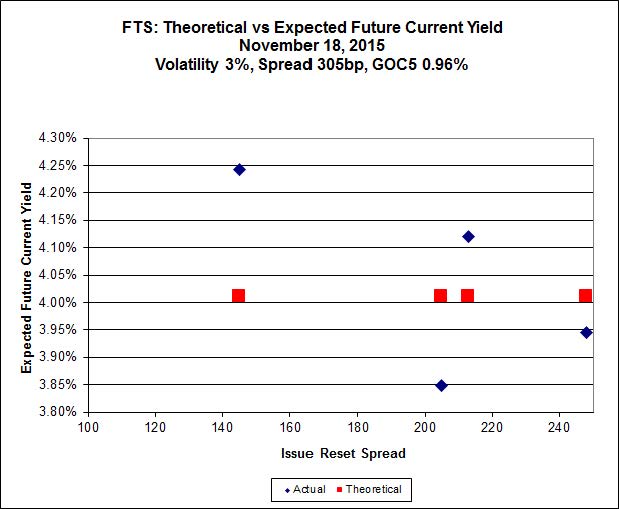

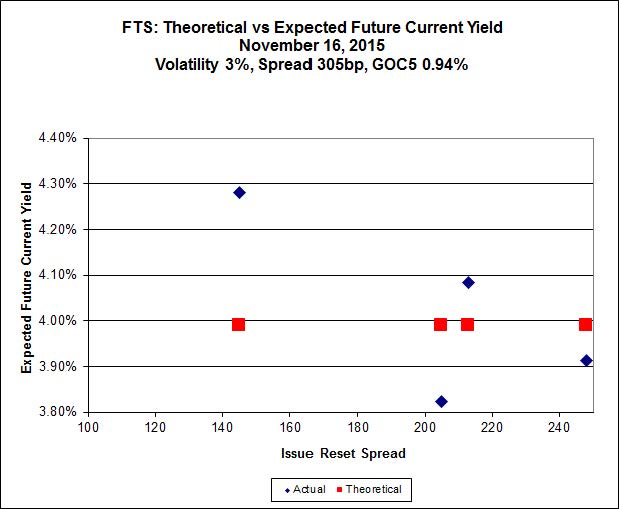

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 19.62, looks $0.85 expensive and resets 2019-3-1. FTS.PR.H, with a spread of +145bp and resetting 2020-6-1, is bid at 14.03 and is $0.96 cheap.

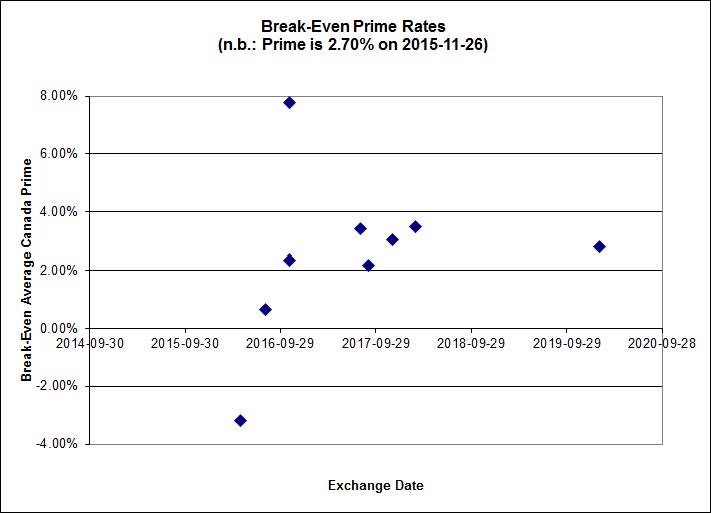

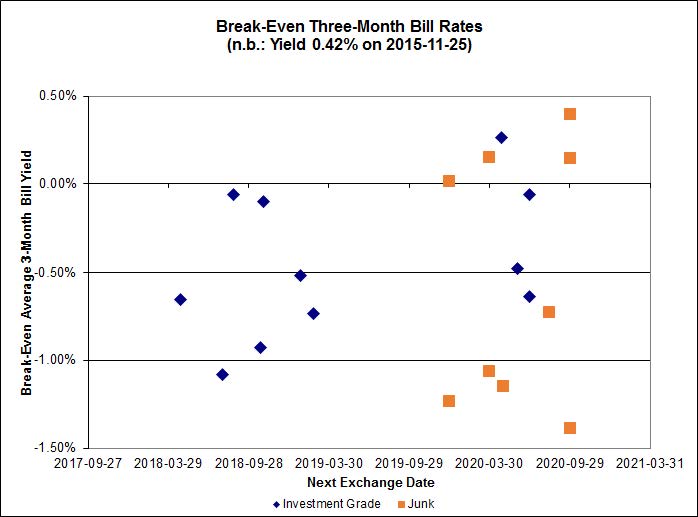

Click for Big

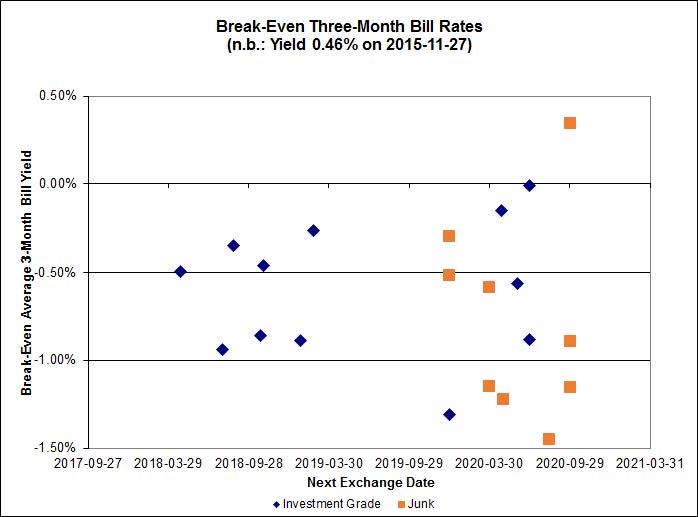

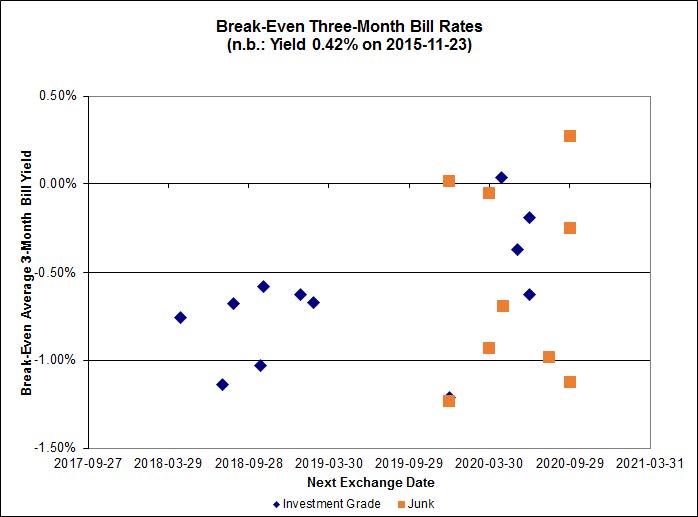

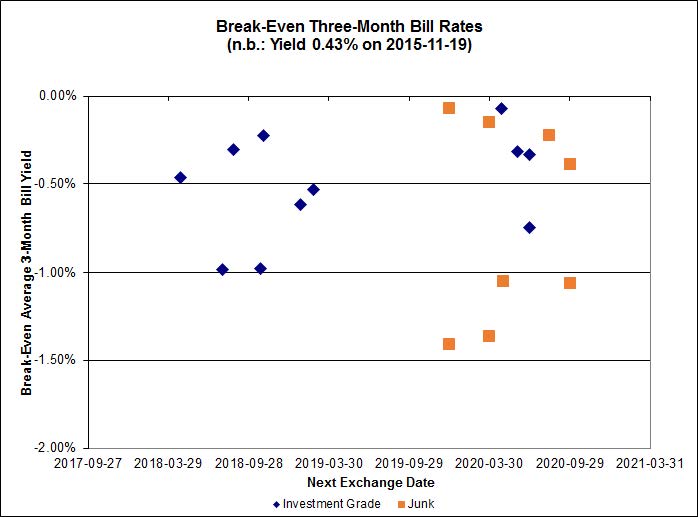

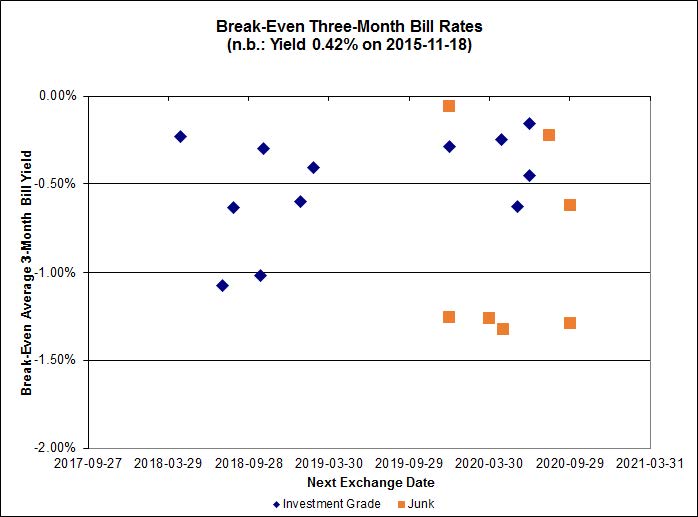

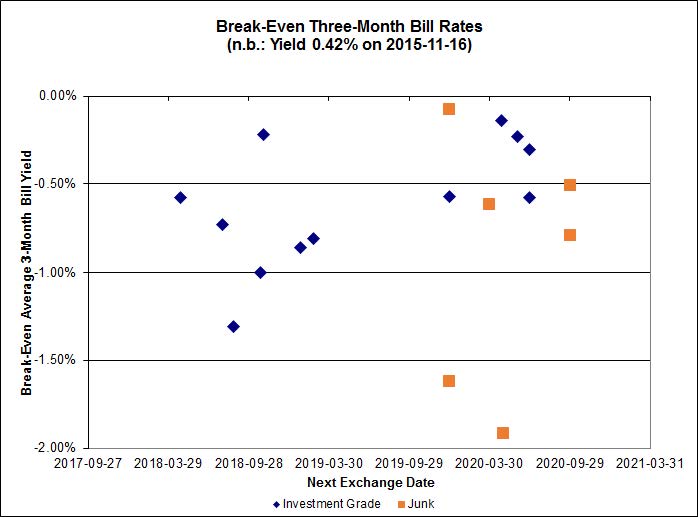

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.42%, with one outlier above 0.00%. There is one junk outlier above 0.00% and one below -2.00%.

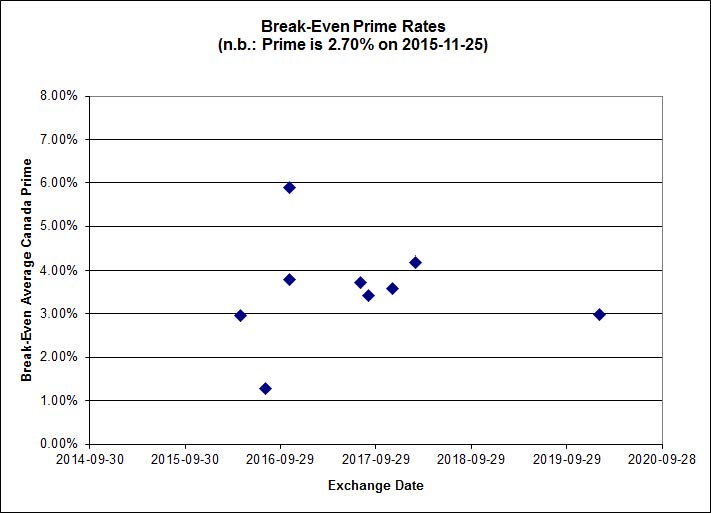

Click for Big

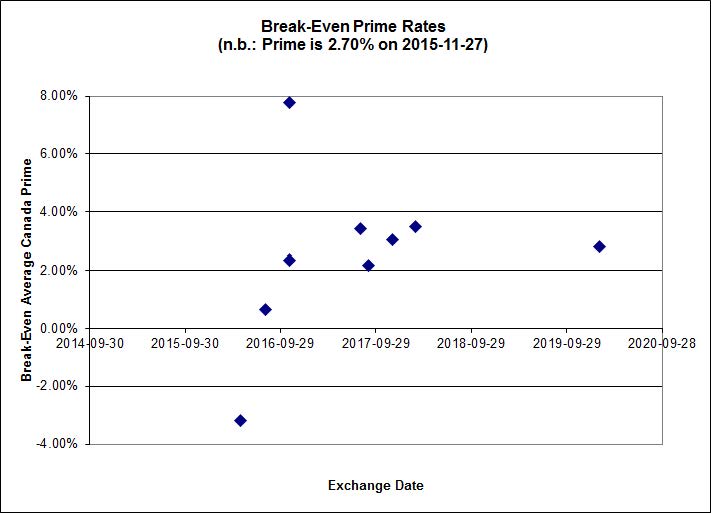

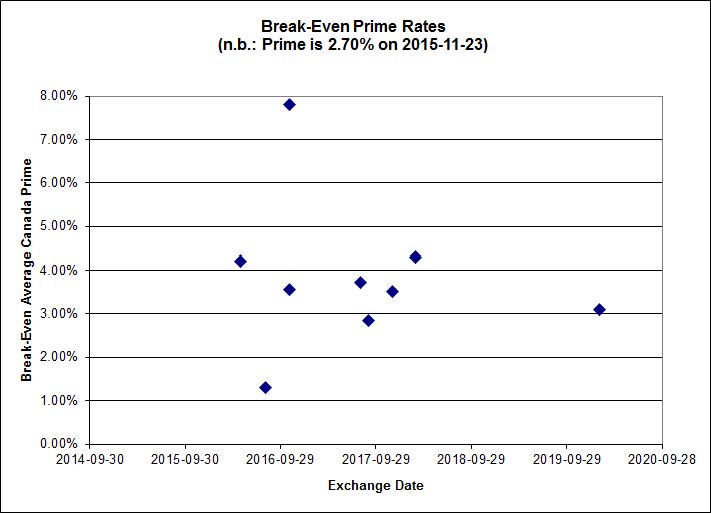

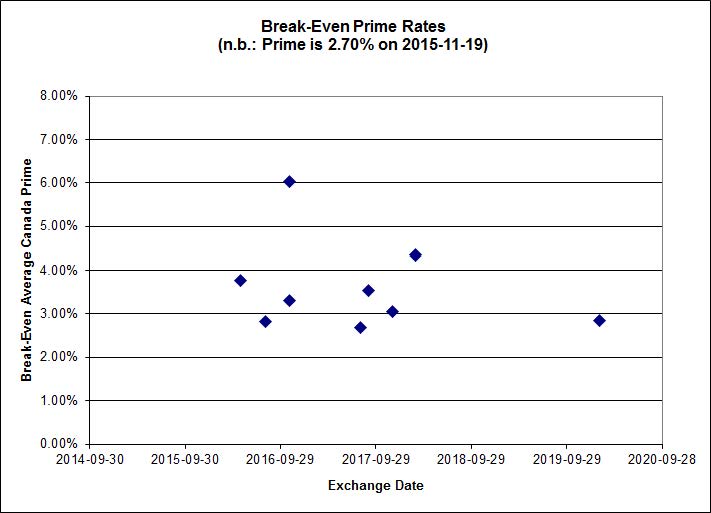

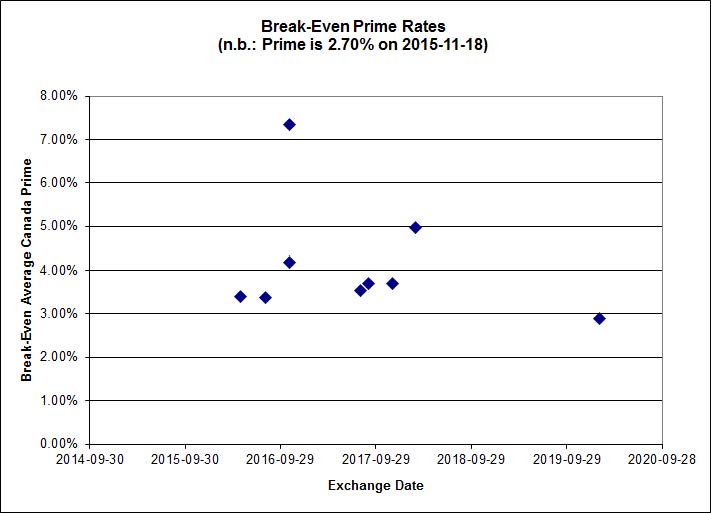

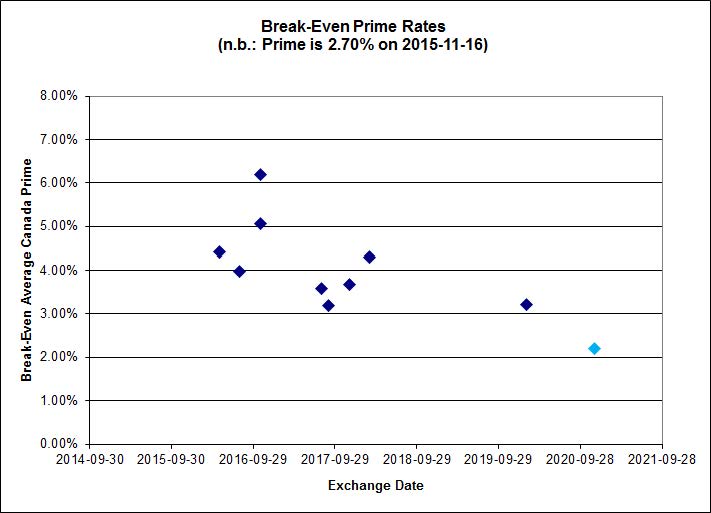

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

4.26 % |

5.12 % |

33,606 |

17.68 |

1 |

-1.8405 % |

1,819.2 |

| FixedFloater |

6.13 % |

5.37 % |

26,572 |

17.06 |

1 |

0.0000 % |

3,184.1 |

| Floater |

4.24 % |

4.32 % |

74,656 |

16.71 |

3 |

-5.2990 % |

1,861.8 |

| OpRet |

4.86 % |

3.66 % |

33,587 |

0.77 |

1 |

0.1988 % |

2,738.6 |

| SplitShare |

4.76 % |

5.71 % |

138,644 |

2.91 |

5 |

0.1975 % |

3,215.9 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.1975 % |

2,509.2 |

| Perpetual-Premium |

5.80 % |

-0.83 % |

89,865 |

0.08 |

6 |

-0.5710 % |

2,505.7 |

| Perpetual-Discount |

5.53 % |

5.61 % |

86,880 |

14.46 |

33 |

-0.1895 % |

2,592.1 |

| FixedReset |

4.87 % |

4.64 % |

222,470 |

15.43 |

76 |

-0.4579 % |

2,102.5 |

| Deemed-Retractible |

5.15 % |

5.25 % |

115,642 |

5.39 |

33 |

0.0153 % |

2,583.9 |

| FloatingReset |

2.57 % |

3.76 % |

59,939 |

5.77 |

10 |

0.1169 % |

2,198.2 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| BAM.PR.B |

Floater |

-6.77 % |

Exaggerated, but not completely wrong, as the issue traded 13,174 shares in a range of 11.03-99 before closing at 11.02-65, 4×1. The low of 11.03 was achieved by a single trade of 300 shares; 100 traded at 11.11; 200 at 11.25 and all the rest were above 11.30, with a VWAP of 11.60. So I’m guessing that the market maker got scared at around 3:30pm and took the rest of the day off. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 11.02

Evaluated at bid price : 11.02

Bid-YTW : 4.34 % |

| BAM.PR.K |

Floater |

-5.31 % |

This is much the same story as with BAM.PR.B, above, but this time there’s more excuse – there was a burst of small sells, possibly algorithmic, from National Bank that took the market down from 11.50 at 3:19 to 10.90 at 3:32. The issue traded 21,358 shares in a range of 10.90-85 before closing at 11.05-57, 1×1. The VWAP was 11.57. I have not checked whether this lamentable state of affairs is due to inadequate Toronto Stock Exchange reporting or inadequate Toronto Stock Exchange supervision of market-makers.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 11.05

Evaluated at bid price : 11.05

Bid-YTW : 4.32 % |

| BAM.PR.C |

Floater |

-3.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 11.35

Evaluated at bid price : 11.35

Bid-YTW : 4.21 % |

| TRP.PR.C |

FixedReset |

-2.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 13.25

Evaluated at bid price : 13.25

Bid-YTW : 4.72 % |

| VNR.PR.A |

FixedReset |

-2.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 20.53

Evaluated at bid price : 20.53

Bid-YTW : 4.70 % |

| SLF.PR.H |

FixedReset |

-2.53 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.51

Bid-YTW : 7.20 % |

| IFC.PR.A |

FixedReset |

-2.45 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.12

Bid-YTW : 8.20 % |

| PWF.PR.T |

FixedReset |

-2.29 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.41

Evaluated at bid price : 21.75

Bid-YTW : 3.97 % |

| BAM.PF.B |

FixedReset |

-2.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.62

Evaluated at bid price : 19.62

Bid-YTW : 4.78 % |

| SLF.PR.J |

FloatingReset |

-2.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.67

Bid-YTW : 9.31 % |

| BAM.PR.E |

Ratchet |

-1.84 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 25.00

Evaluated at bid price : 16.00

Bid-YTW : 5.12 % |

| TD.PF.E |

FixedReset |

-1.75 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.98

Evaluated at bid price : 22.51

Bid-YTW : 4.20 % |

| CM.PR.P |

FixedReset |

-1.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.16

Evaluated at bid price : 19.16

Bid-YTW : 4.36 % |

| BAM.PR.T |

FixedReset |

-1.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 17.86

Evaluated at bid price : 17.86

Bid-YTW : 4.78 % |

| BAM.PF.A |

FixedReset |

-1.42 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 20.80

Evaluated at bid price : 20.80

Bid-YTW : 4.81 % |

| TD.PF.B |

FixedReset |

-1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.57

Evaluated at bid price : 19.57

Bid-YTW : 4.28 % |

| RY.PR.J |

FixedReset |

-1.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.47

Evaluated at bid price : 21.75

Bid-YTW : 4.21 % |

| CU.PR.C |

FixedReset |

-1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.80

Evaluated at bid price : 19.80

Bid-YTW : 4.29 % |

| FTS.PR.H |

FixedReset |

-1.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 14.03

Evaluated at bid price : 14.03

Bid-YTW : 4.32 % |

| BAM.PF.C |

Perpetual-Discount |

-1.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.00

Evaluated at bid price : 21.00

Bid-YTW : 5.87 % |

| TD.PF.A |

FixedReset |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.62

Evaluated at bid price : 19.62

Bid-YTW : 4.27 % |

| MFC.PR.I |

FixedReset |

-1.15 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.23

Bid-YTW : 5.03 % |

| BAM.PF.D |

Perpetual-Discount |

-1.12 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.26

Evaluated at bid price : 21.26

Bid-YTW : 5.86 % |

| HSE.PR.A |

FixedReset |

-1.11 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 14.25

Evaluated at bid price : 14.25

Bid-YTW : 4.86 % |

| RY.PR.H |

FixedReset |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.60

Evaluated at bid price : 19.60

Bid-YTW : 4.27 % |

| PWF.PR.R |

Perpetual-Discount |

-1.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 24.10

Evaluated at bid price : 24.60

Bid-YTW : 5.62 % |

| BMO.PR.M |

FixedReset |

-1.03 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.10

Bid-YTW : 3.61 % |

| CM.PR.Q |

FixedReset |

-1.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.86

Evaluated at bid price : 22.30

Bid-YTW : 4.15 % |

| RY.PR.M |

FixedReset |

-1.02 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.34

Evaluated at bid price : 21.34

Bid-YTW : 4.20 % |

| CU.PR.D |

Perpetual-Discount |

1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 22.14

Evaluated at bid price : 22.45

Bid-YTW : 5.46 % |

| GWO.PR.N |

FixedReset |

1.47 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.85

Bid-YTW : 9.87 % |

| W.PR.J |

Perpetual-Discount |

1.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 24.08

Evaluated at bid price : 24.34

Bid-YTW : 5.82 % |

| TRP.PR.F |

FloatingReset |

4.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 15.11

Evaluated at bid price : 15.11

Bid-YTW : 3.89 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| NA.PR.S |

FixedReset |

214,079 |

Desjardins crossed 78,900 at 19.82. RBC crossed 112,000 at 19.79.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.68

Evaluated at bid price : 19.68

Bid-YTW : 4.45 % |

| TD.PF.B |

FixedReset |

164,220 |

Scotia crossed blocks of 50,000 and 35,000, both at 19.70. RBC crossed 50,000 at the same price.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.57

Evaluated at bid price : 19.57

Bid-YTW : 4.28 % |

| NA.PR.W |

FixedReset |

125,945 |

RBC crossed 112,000 at 19.59.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.33

Evaluated at bid price : 19.33

Bid-YTW : 4.35 % |

| RY.PR.H |

FixedReset |

119,197 |

Scotia crossed two blocks of 50,000 each, both at 19.80.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.60

Evaluated at bid price : 19.60

Bid-YTW : 4.27 % |

| BNS.PR.Z |

FixedReset |

87,857 |

Desjardins crossed 64,400 at 20.65.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.56

Bid-YTW : 5.90 % |

| BMO.PR.T |

FixedReset |

81,650 |

Scotia crossed 25,000 at 19.55. RBC crossed 29,600 at the same price.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 19.55

Evaluated at bid price : 19.55

Bid-YTW : 4.26 % |

| There were 59 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| BAM.PR.B |

Floater |

Quote: 11.02 – 11.65

Spot Rate : 0.6300

Average : 0.4234

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 11.02

Evaluated at bid price : 11.02

Bid-YTW : 4.34 % |

| BAM.PF.C |

Perpetual-Discount |

Quote: 21.00 – 21.55

Spot Rate : 0.5500

Average : 0.3491

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.00

Evaluated at bid price : 21.00

Bid-YTW : 5.87 % |

| BAM.PR.K |

Floater |

Quote: 11.05 – 11.57

Spot Rate : 0.5200

Average : 0.3392

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 11.05

Evaluated at bid price : 11.05

Bid-YTW : 4.32 % |

| TD.PF.E |

FixedReset |

Quote: 22.51 – 22.99

Spot Rate : 0.4800

Average : 0.3272

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.98

Evaluated at bid price : 22.51

Bid-YTW : 4.20 % |

| PWF.PR.R |

Perpetual-Discount |

Quote: 24.60 – 24.98

Spot Rate : 0.3800

Average : 0.2403

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 24.10

Evaluated at bid price : 24.60

Bid-YTW : 5.62 % |

| PWF.PR.T |

FixedReset |

Quote: 21.75 – 22.33

Spot Rate : 0.5800

Average : 0.4407

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-11-19

Maturity Price : 21.41

Evaluated at bid price : 21.75

Bid-YTW : 3.97 % |