Advanced students of economics, confidently exploring the most arcane niches of their field, will be fascinated to learn that after an extensive investigation, a US Senate committee has learned that private companies seek to maximize revenue:

The makers of a breakthrough drug for hepatitis C put profits before patients in pricing the $1,000 pill that cures the liver-wasting disease, U.S. Senate investigators said Tuesday.

A bipartisan report from the Senate Finance Committee concluded that California-based Gilead Sciences was focused on maximizing revenue even as the company’s own analysis showed a lower price would allow more patients to be treated.

Although the report focused on just one drug that has made headlines in the last few years, the lawmakers who led the investigation said their findings are a warning about what’s to come with other high-priced treatments for cancer, diabetes, Alzheimer’s and HIV.

…

“Gilead responsibly and thoughtfully priced Sovaldi and Harvoni,” said the company’s statement, noting that more than 600,000 patients have been treated worldwide since the introduction of Sovaldi two years ago.

But Wyden and Sen. Chuck Grassley, a Republican, said their 18-month investigation found that the high price tag significantly limited patient access and heaped huge costs on federal and state health care programs.

…

Other conclusions from the report:

— Gilead priced its first hepatitis C drug — Sovaldi — with an eye toward maximizing future returns from its follow-on medication, Harvoni.

— Gilead offered only meagre supplemental discounts to state Medicaid programs, and conditioned those on the states’ dropping any restrictions on patient access. The supplemental discounts of around 10 per cent would have been on top off other discounts that Medicaid programs get by law.

“The evidence shows the company pursued a calculated scheme for pricing and marketing its hepatitis C drug based on one primary goal – maximizing revenue – regardless of the human consequences,” said Wyden.

This startling conclusion will have the economics field abuzz for years – it’s revolutionary!

There will, of course, be the usual grousers who don’t like this idea; PrefBlog humbly suggests that they fund development of their own damn drugs:

A global coalition of charities and funding bodies has been formed to invest up to £30 million into restarting the development of promising drug candidates for neurodegenerative conditions such as dementia, motor neurone disease and Parkinson’s disease. The Neurodegeneration Medicines Acceleration Programme (Neuro-MAP), led by medical research charity MRC Technology, will identify promising drug projects that are no longer in development by the industry and help scientists to take them forward to the next stage, before returning them to pharmaceutical companies for further development into marketable treatments.

…

As a coalition of 9 charities and funders, Neuro-MAP will help ensure that the potential of fundamental early stage research into neurodegenerative disease is realised, taking promising drug candidates forward towards clinical testing. It will also look to repurpose existing drugs and compounds for other conditions, for example, the use of hypertension drugs for the treatment of vascular dementia. The programme protects both charities’ and pharma’s investment and allows charities to maximise their impact on patient’s quality of life.

Partners in the Neuro–MAP are: Alzheimer’s Association US, Alzheimer Research UK, Alzheimer’s Society UK, ALS Association, Michael J Fox Foundation, MND Association, MRC Technology, Northern Health Science Alliance and Parkinson’s UK.

Some pioneering cranks have been doing this for some time:

The Cystic Fibrosis (CF) Foundation has sold royalty rights to treatments developed with support from its ‘venture philantrophy’ model. Royalty pharma – which accumulates royalty payments from established drugs – paid $3.3 billion for royalties on Vertex pharmaceuticals’ Kalydeco (ivacaftor).

The venture philanthropy model, adopted in the late 1990s, sees the foundation provide upfront funding for pharmaceutical companies to help reduce the financial risk of developing drugs to treat CF. It gave a total of $150 million to Vertex to support the company’s CF drug development program.

…

The funding provided by the CF Foundation is exclusively for the use of specific, negotiated CF research projects with a biotech or pharmaceutical company. ‘We negotiate legal agreements with strict parameters to ensure that every dollar invested is in the best interest of advancing [our] mission,’ a foundation spokesperson explained. ‘Virtually every CF drug available to patients in the US was made possible because of Foundation support.’

In an exclusive interview, a PrefBlog spokesman stated “I don’t expect anything much to come of it in Canada. People aren’t too bright and would rather pay crackheads to sleep on the streets.”

I am happy to report that the Sprott Silver battle continues, with a press release yesterday from Sprott:

Desperate Attempt by the Spicers to Preserve Fees

Proposed Transaction Betrays the Principles of Physical Bullion Investing and Subjects Unitholders to Increased Risks, Including Risk of Significant Redemptions

Previous Bullion Fund to ETF Conversion by Purpose’s Predecessor Resulted in Immediate and Massive Redemptions

Purpose Investments Can Walk Away With no Penalty After April 30, 2016, and GTU and SBT’s Paid Financial Advisor Hasn’t Provided a Fairness Opinion on the Transaction

No Credible Reason to Believe That the Proposed ETF Conversions Can be Completed – the Transaction May be Nothing More Than a Defensive Tactic

…

John Wilson, CEO of Sprott Asset Management, said, “The Purpose Investments transaction is an illogical proposition for GTU and SBT unitholders who made the choice to invest in a security fully backed by physical bullion. Unitholders should feel betrayed by the Trustees. After suffering from significant underperformance, gross mismanagement and questionable side payments to the Trustees and other friends of the Spicer family, unitholders are now faced with a Spicer-negotiated transaction that protects their fees and hypocritically tries to promote liquidity, marketing support and enhanced asset scale. These qualities are just a few of the benefits that Sprott is offering GTU and SBT unitholders, but at a premium and with certainty. Most importantly, through the Sprott offers, unitholders do not lose the distinct investment quality of holding bullion directly.”

Silver Bullion Trust has fired back:

Bruce Heagle, Chair of the Special Committee of Independent Trustees, stated: “It is regrettable but not surprising that Sprott’s latest press commentary delivers alarmist criticism and confusion in order to forward their own agenda. Sprott is the desperate party in this debate – they are seeking to draw attention away from the obvious deficiencies of their offer relative to the proposed ETF conversion. Your Independent Trustees recommend that unitholders ignore Sprott’s fear-mongering accusations, as Sprott is seeking to prevent unitholders from considering a better alternative to their inadequate, self-serving offer, which has yet to garner sufficient unitholder support despite seven extensions. All of the pertinent information regarding the proposed ETF conversion and its benefits to unitholders relative to Sprott’s offer will be in the Information Circular, which will be sent to unitholders shortly. Upon review of the forthcoming Information Circular and the benefits of the ETF conversion, I am confident that you will reach the same conclusion as your Independent Trustees: that the proposed ETF conversion in partnership with Purpose Investments is clearly a superior alternative to Sprott’s deficient offer. We thank unitholders for their patience and continued support of Silver Bullion Trust.”

There were two issues of bank NVCC-compliant sub-debt today – one from BMO:

Bank of Montreal (TSX:BMO)(NYSE:BMO) today announced a domestic public offering of $1 billion of subordinated notes (Non-Viability Contingent Capital (NVCC)) (the “Notes”) through its Canadian Medium-Term Note Program. The net proceeds from this offering will be used for general corporate purposes.

The Notes bear interest at a fixed rate of 3.34 per cent per annum (paid semi-annually) until December 8, 2020, and at the three-month Bankers’ Acceptance Rate plus 2.18 per cent thereafter (paid quarterly) until their maturity on December 8, 2025. The expected closing date is December 8, 2015. BMO Capital Markets is acting as lead agent on the issue.

… and one from Scotia:

The Bank of Nova Scotia (“Scotiabank”) (TSX:BNS) (NYSE:BNS) today announced a Basel III-compliant offering of $750 million of 3.367% Subordinated Debentures due 2025 (the “Debentures”) pursuant to its June 27, 2014 base shelf prospectus.

The Debentures, to be sold through an agency syndicate led by Scotiabank Global Banking and Markets, are expected to be issued on December 8, 2015. Interest will be payable semi-annually from the date of issue until December 8, 2020 at 3.367% per annum. From December 8, 2020 to maturity on December 8, 2025, the Debentures will pay a quarterly coupon at a rate of the 90 day bankers’ acceptance plus 2.19%, beginning March 8, 2021.

The mechanics of NVCC-compliant sub-debt were discussed in the post Royal Bank Issues NVCC-Compliant Sub-Debt. It’s interesting to see that that issue, from July 2014, was issued at 3.04%, resetting ha-ha to BAs+108 after their pretend-maturity. That was at a time when:

[July, 2014] The Canada 10-year is trading at around 2.20%, the five year around 1.55% and three-month BAs a little above 1.20%.

Great-West Lifeco was supposed to have supposed to have advised bank-owned CDS of the reset rate on GWO.PR.N today, but neither the company, nor bank-owned CDS, nor regulatorally run SEDAR has any news for you, you disgusting retail scum. Phone your broker and ask this simple question if you can get through the voice-menu, and while you’re at it, be sure to ask if he has any new issues he can sell you; if not, mail him a cheque anyway. This will help build a stronger Canada.

It was another mixed, mostly negative day for the Canadian preferred share market, with PerpetualDiscounts off 12bp, FixedResets down 33bp and DeemedRetractibles gaining 5bp. The Performance Highlights table is dominated by losers. Volume continued to be extremely high.

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

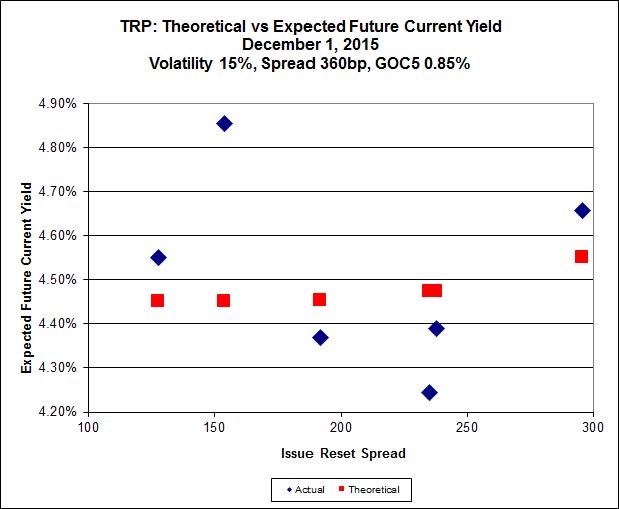

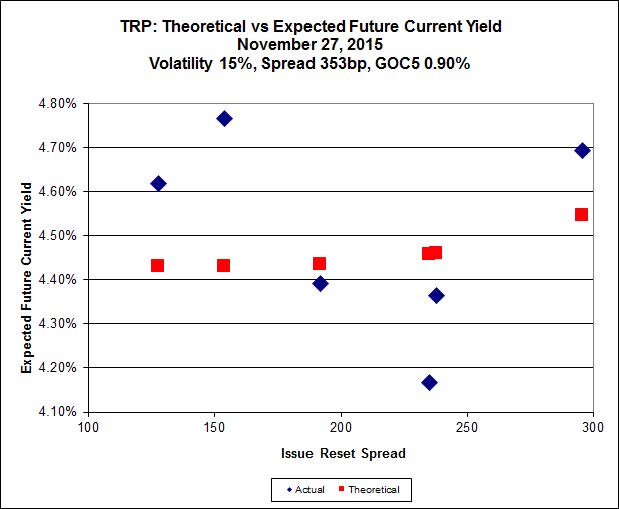

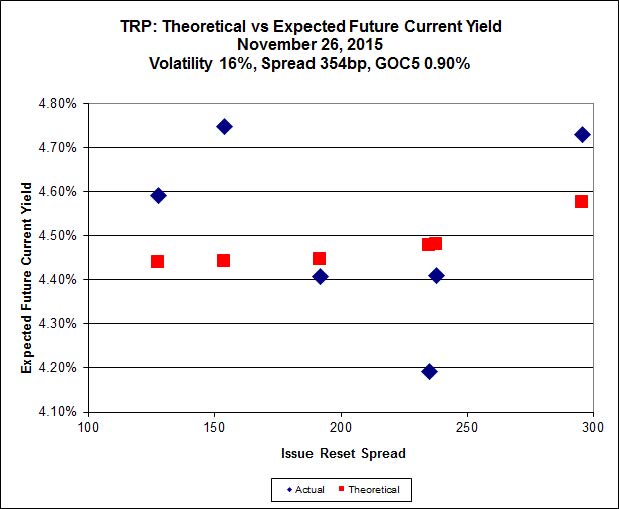

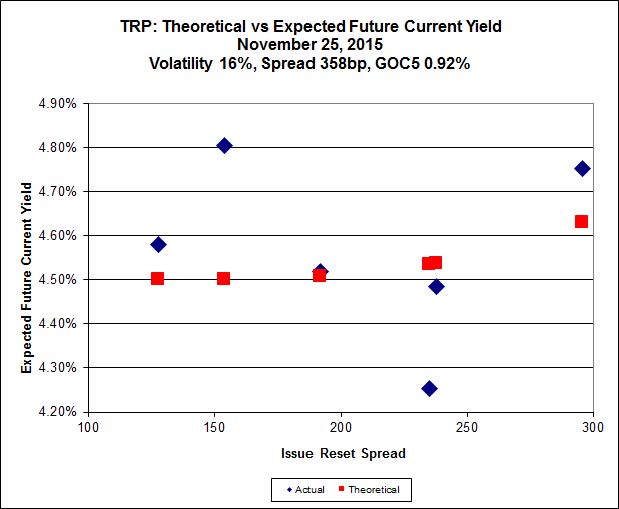

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.85 to be $0.96 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.12 cheap at its bid price of 12.31.

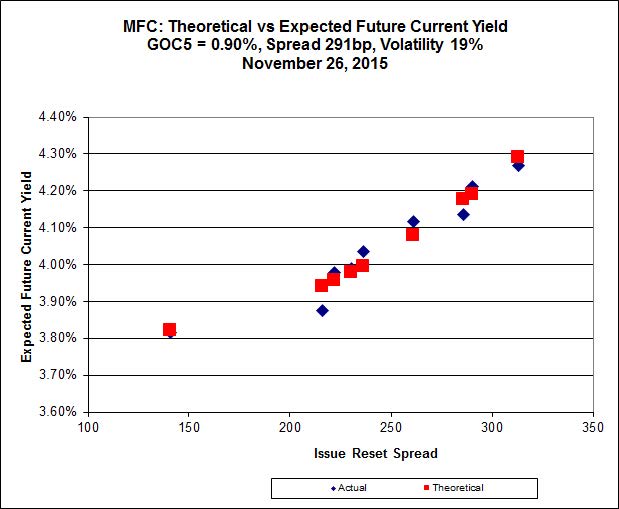

Click for Big

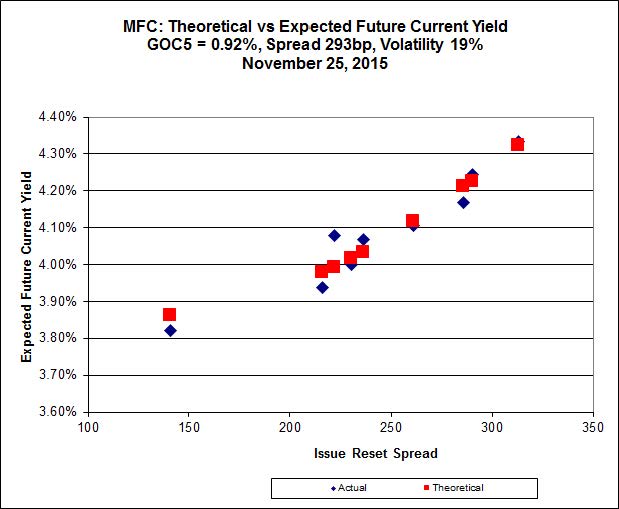

Click for BigMost expensive is MFC.PR.H, resetting at +313bp on 2017-3-19, bid at 23.92 to be 0.54 rich, while MFC.PR.G, resetting at +290bp on 2018-3-19, is bid at 22.13 to be 0.43 cheap.

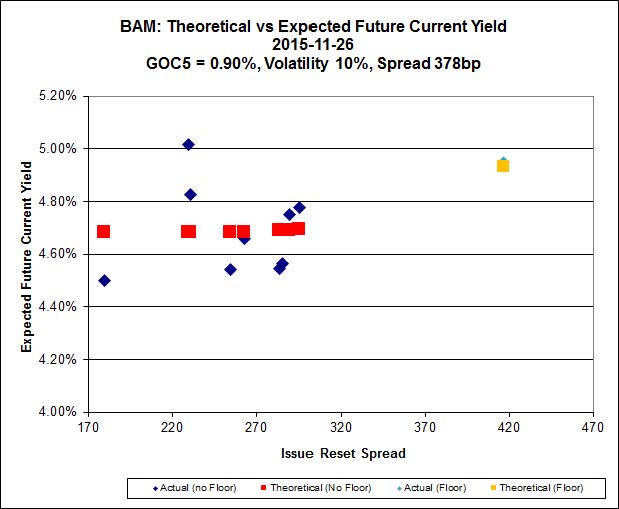

Click for Big

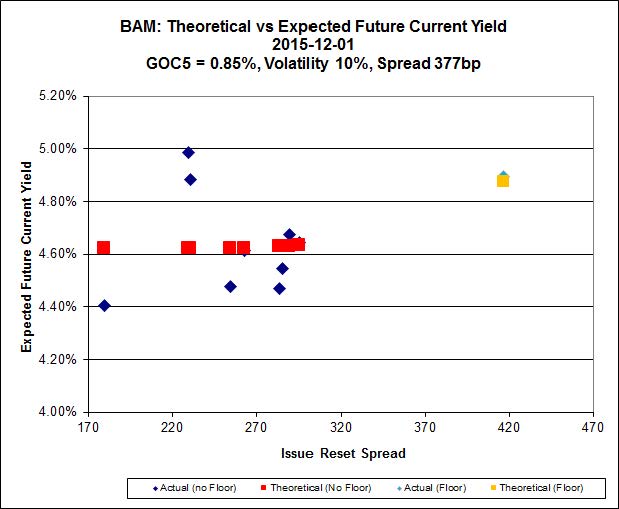

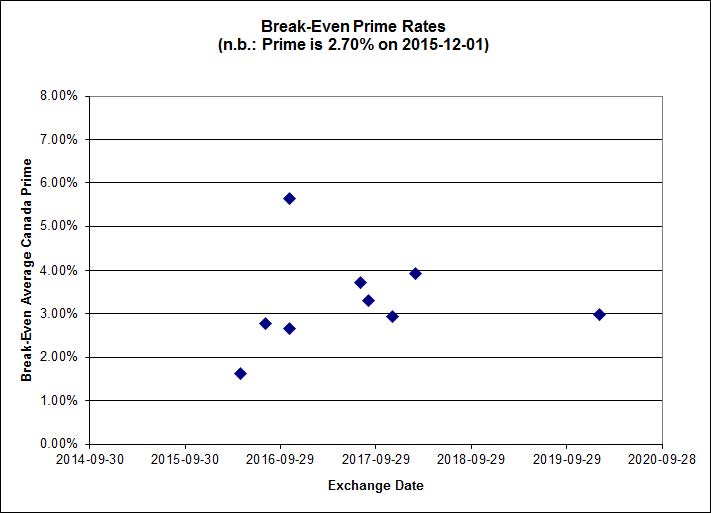

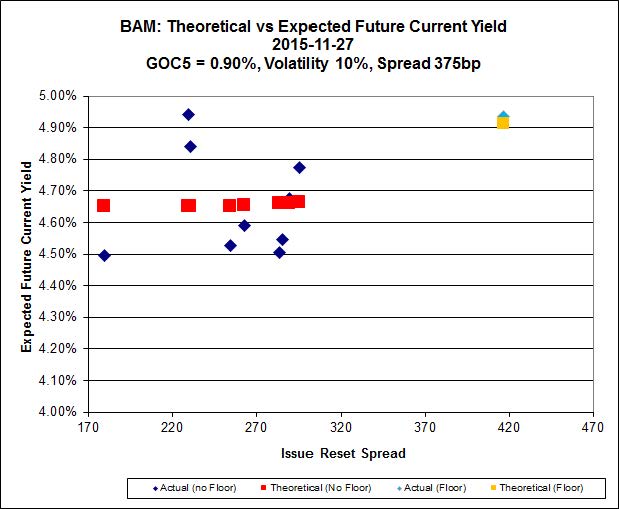

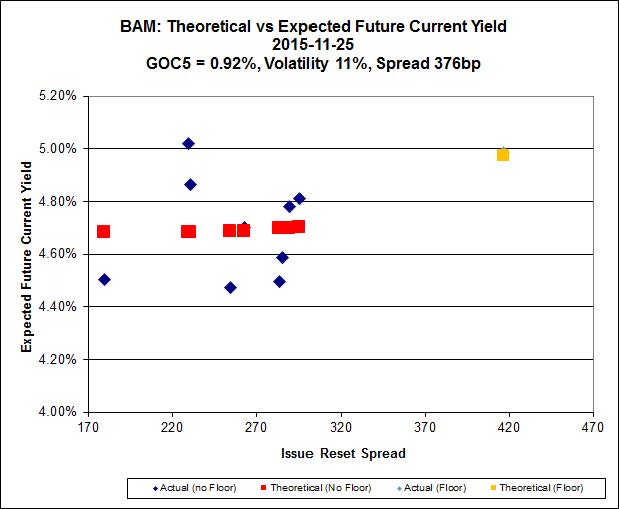

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 15.79 to be $1.25 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 20.65 and appears to be $0.72 rich.

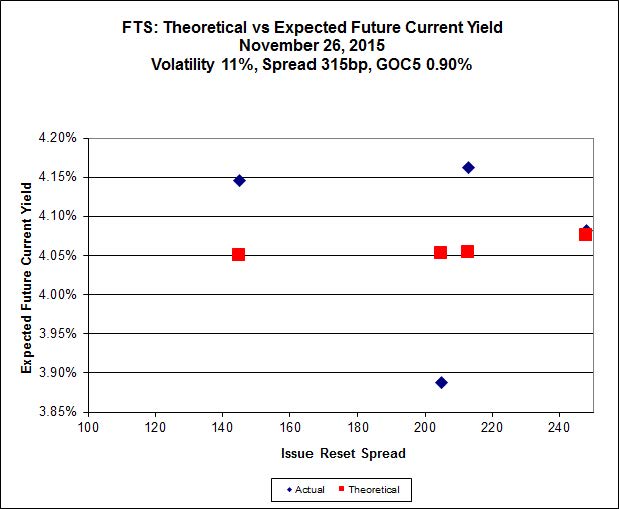

Click for Big

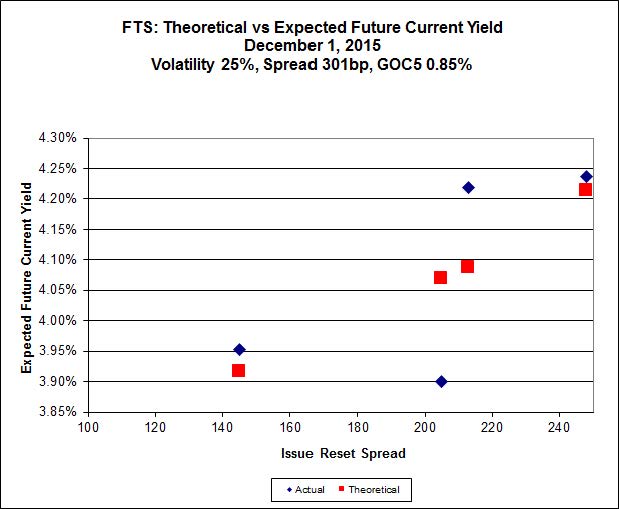

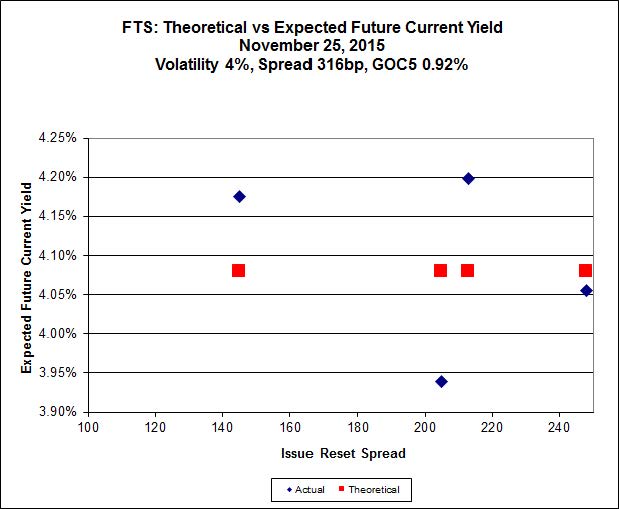

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 18.59, looks $0.77 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.66 and is $0.57 cheap.

Click for Big

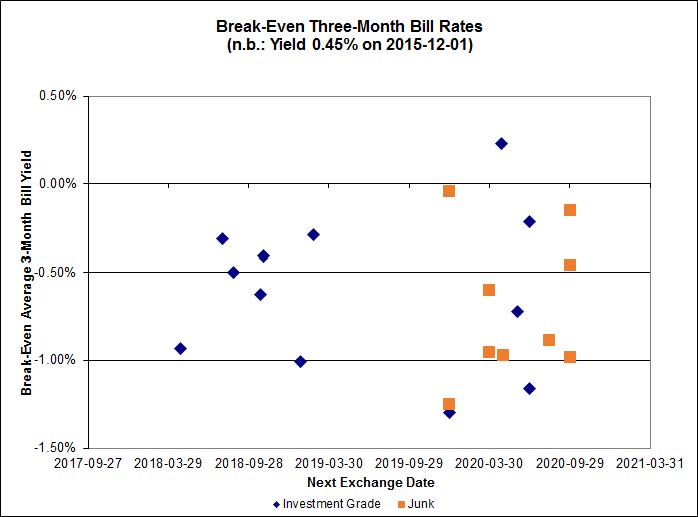

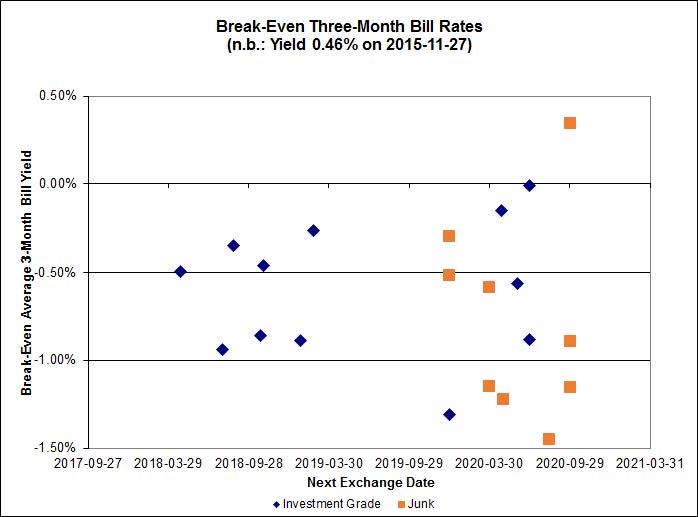

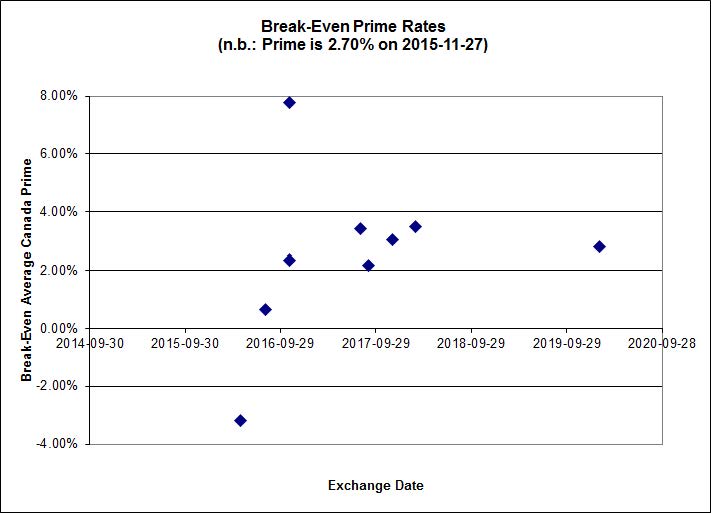

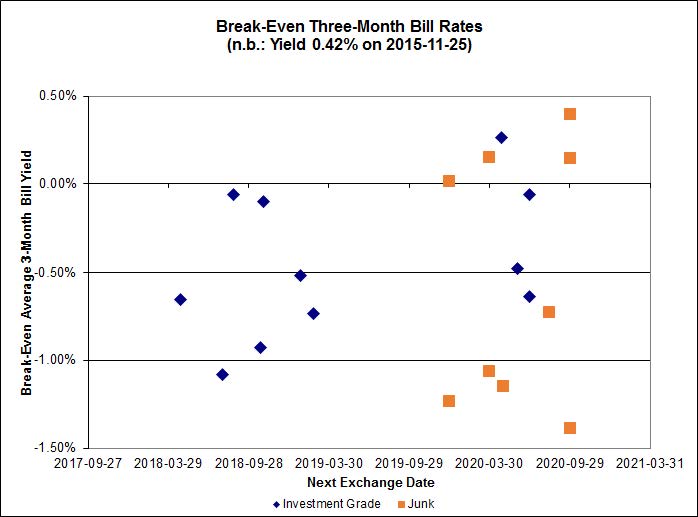

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.60%, with no outliers. There is one junk outlier below -1.50%.

Click for Big

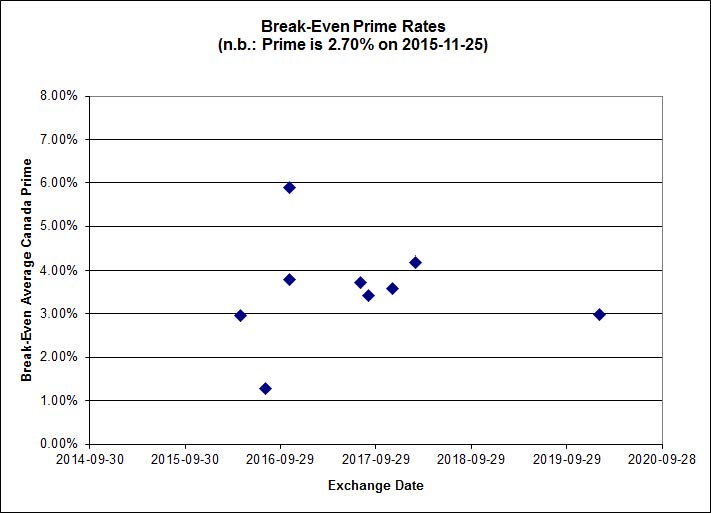

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

4.39 % |

5.29 % |

35,553 |

17.52 |

1 |

-0.6410 % |

1,769.2 |

| FixedFloater |

6.29 % |

5.53 % |

29,440 |

16.85 |

1 |

-0.1323 % |

3,101.9 |

| Floater |

4.26 % |

4.31 % |

84,461 |

16.71 |

3 |

-0.1200 % |

1,854.5 |

| OpRet |

4.86 % |

3.93 % |

28,900 |

0.73 |

1 |

-0.2772 % |

2,736.5 |

| SplitShare |

4.76 % |

5.45 % |

128,859 |

4.32 |

5 |

0.2219 % |

3,221.1 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.2219 % |

2,513.3 |

| Perpetual-Premium |

5.75 % |

-2.12 % |

89,722 |

0.09 |

6 |

-0.1241 % |

2,528.9 |

| Perpetual-Discount |

5.56 % |

5.63 % |

93,562 |

14.44 |

33 |

-0.1153 % |

2,575.6 |

| FixedReset |

5.04 % |

4.68 % |

225,378 |

15.09 |

76 |

-0.3315 % |

2,037.0 |

| Deemed-Retractible |

5.16 % |

4.74 % |

123,395 |

5.36 |

33 |

0.0458 % |

2,598.9 |

| FloatingReset |

2.65 % |

3.74 % |

64,767 |

5.73 |

10 |

-0.7126 % |

2,180.6 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| TRP.PR.C |

FixedReset |

-2.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 12.31

Evaluated at bid price : 12.31

Bid-YTW : 5.06 % |

| MFC.PR.N |

FixedReset |

-2.57 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.07

Bid-YTW : 6.40 % |

| MFC.PR.M |

FixedReset |

-2.42 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.20

Bid-YTW : 6.39 % |

| TRP.PR.E |

FixedReset |

-2.33 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.85

Evaluated at bid price : 18.85

Bid-YTW : 4.66 % |

| MFC.PR.G |

FixedReset |

-2.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.13

Bid-YTW : 5.50 % |

| TRP.PR.F |

FloatingReset |

-2.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 13.62

Evaluated at bid price : 13.62

Bid-YTW : 4.34 % |

| RY.PR.H |

FixedReset |

-1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.21

Evaluated at bid price : 18.21

Bid-YTW : 4.59 % |

| NA.PR.W |

FixedReset |

-1.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.03

Evaluated at bid price : 18.03

Bid-YTW : 4.66 % |

| NA.PR.S |

FixedReset |

-1.60 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.42

Evaluated at bid price : 18.42

Bid-YTW : 4.74 % |

| FTS.PR.K |

FixedReset |

-1.59 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.59

Evaluated at bid price : 18.59

Bid-YTW : 4.25 % |

| BIP.PR.A |

FixedReset |

-1.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 20.40

Evaluated at bid price : 20.40

Bid-YTW : 5.50 % |

| MFC.PR.I |

FixedReset |

-1.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.48

Bid-YTW : 5.31 % |

| BNS.PR.C |

FloatingReset |

-1.22 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.72

Bid-YTW : 3.97 % |

| TRP.PR.H |

FloatingReset |

-1.20 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 10.67

Evaluated at bid price : 10.67

Bid-YTW : 4.04 % |

| PWF.PR.P |

FixedReset |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 14.44

Evaluated at bid price : 14.44

Bid-YTW : 4.41 % |

| BAM.PR.T |

FixedReset |

-1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 16.18

Evaluated at bid price : 16.18

Bid-YTW : 5.27 % |

| HSE.PR.A |

FixedReset |

-1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 12.98

Evaluated at bid price : 12.98

Bid-YTW : 5.12 % |

| CM.PR.P |

FixedReset |

-1.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 17.76

Evaluated at bid price : 17.76

Bid-YTW : 4.70 % |

| IGM.PR.B |

Perpetual-Premium |

-1.01 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2017-12-31

Maturity Price : 25.25

Evaluated at bid price : 25.54

Bid-YTW : 5.53 % |

| CU.PR.C |

FixedReset |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 19.56

Evaluated at bid price : 19.56

Bid-YTW : 4.33 % |

| HSE.PR.G |

FixedReset |

1.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 21.36

Evaluated at bid price : 21.36

Bid-YTW : 5.25 % |

| HSE.PR.C |

FixedReset |

2.41 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 5.19 % |

| SLF.PR.G |

FixedReset |

2.70 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.20

Bid-YTW : 8.55 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BNS.PR.R |

FixedReset |

89,000 |

Nesbitt crossed 30,000 at 24.80; TD crossed 49,900 at the same price.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.80

Bid-YTW : 3.57 % |

| IFC.PR.A |

FixedReset |

61,200 |

Desjardins crossed 50,000 at 16.45.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.50

Bid-YTW : 8.73 % |

| TRP.PR.D |

FixedReset |

53,830 |

RBC crossed 25,000 at 18.58.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.40

Evaluated at bid price : 18.40

Bid-YTW : 4.71 % |

| TRP.PR.B |

FixedReset |

52,226 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 11.70

Evaluated at bid price : 11.70

Bid-YTW : 4.68 % |

| FTS.PR.M |

FixedReset |

32,436 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 19.65

Evaluated at bid price : 19.65

Bid-YTW : 4.54 % |

| TD.PF.B |

FixedReset |

30,295 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.45

Evaluated at bid price : 18.45

Bid-YTW : 4.53 % |

| There were 64 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| TRP.PR.E |

FixedReset |

Quote: 18.85 – 19.31

Spot Rate : 0.4600

Average : 0.2872

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 18.85

Evaluated at bid price : 18.85

Bid-YTW : 4.66 % |

| BNS.PR.C |

FloatingReset |

Quote: 22.72 – 23.13

Spot Rate : 0.4100

Average : 0.3019

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.72

Bid-YTW : 3.97 % |

| RY.PR.J |

FixedReset |

Quote: 20.30 – 20.59

Spot Rate : 0.2900

Average : 0.1837

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 20.30

Evaluated at bid price : 20.30

Bid-YTW : 4.52 % |

| GWO.PR.F |

Deemed-Retractible |

Quote: 25.37 – 25.67

Spot Rate : 0.3000

Average : 0.2000

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2015-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.37

Bid-YTW : -17.11 % |

| TD.PF.F |

Perpetual-Discount |

Quote: 23.25 – 23.50

Spot Rate : 0.2500

Average : 0.1549

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2045-12-01

Maturity Price : 22.87

Evaluated at bid price : 23.25

Bid-YTW : 5.31 % |

| TD.PR.S |

FixedReset |

Quote: 24.33 – 24.66

Spot Rate : 0.3300

Average : 0.2355

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.33

Bid-YTW : 3.45 % |