The Fed stood pat:

Although swings in net exports continue to affect the data, recent indicators suggest that growth of economic activity moderated in the first half of the year. The unemployment rate remains low, and labor market conditions remain solid. Inflation remains somewhat elevated.

The Committee seeks to achieve maximum employment and inflation at the rate of 2 percent over the longer run. Uncertainty about the economic outlook remains elevated. The Committee is attentive to the risks to both sides of its dual mandate.

In support of its goals, the Committee decided to maintain the target range for the federal funds rate at 4-1/4 to 4-1/2 percent. In considering the extent and timing of additional adjustments to the target range for the federal funds rate, the Committee will carefully assess incoming data, the evolving outlook, and the balance of risks. The Committee will continue reducing its holdings of Treasury securities and agency debt and agency mortgage‑backed securities. The Committee is strongly committed to supporting maximum employment and returning inflation to its 2 percent objective.

In assessing the appropriate stance of monetary policy, the Committee will continue to monitor the implications of incoming information for the economic outlook. The Committee would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could impede the attainment of the Committee’s goals. The Committee’s assessments will take into account a wide range of information, including readings on labor market conditions, inflation pressures and inflation expectations, and financial and international developments.

Voting for the monetary policy action were Jerome H. Powell, Chair; John C. Williams, Vice Chair; Michael S. Barr; Susan M. Collins; Lisa D. Cook; Austan D. Goolsbee; Philip N. Jefferson; Alberto G. Musalem; and Jeffrey R. Schmid. Voting against this action were Michelle W. Bowman and Christopher J. Waller, who preferred to lower the target range for the federal funds rate by 1/4 percentage point at this meeting. Absent and not voting was Adriana D. Kugler.

The newspapers are full of references to:

There were some signs of splits in the Fed’s ranks: Governors Christopher Waller and Michelle Bowman voted to reduce borrowing costs, while 9 officials, including Powell, favoured standing pat. It is the first time in more than three decades that two of the seven Washington-based governors have dissented.

Waller and Bowman will have arguable reasons for their dissent, but such things are always arguable; the dissent is tainted due to suspicions that they are merely pandering to the idiot in chief:

Just two weeks after President Donald Trump sent a handwritten letter to Powell demanding lower interest rates, Russell Vought, Trump’s director of the Office of Management and Budget (OMB), accused Powell of breaking the law by failing to comply with government oversight regulations and lying to Congress about details of an approximately $2.5 billion planned renovation of the Fed’s headquarters.

“The President is extremely troubled by your management of the Federal Reserve System,” Vought wrote in a letter he posted to social media Thursday. “Instead of attempting to right the Fed’s fiscal ship, you have plowed ahead with an ostentatious overhaul of your Washington D.C. headquarters.”

For months, Trump has berated Powell, whom he appointed during his first term, and called him insulting names. The president has lately taken to calling Powell by the nickname “Too Late” for failing to recognize the 2022 inflation crisis fast enough and failing to slash interest rates as inflation has cooled down. Earlier this month, Trump suggested that Powell should resign in a social media post.

Canada has similar idiots, but similarly ignored them:

The Bank of Canada today maintained its target for the overnight rate at 2.75%, with the Bank Rate at 3% and the deposit rate at 2.70%.

While some elements of US trade policy have started to become more concrete in recent weeks, trade negotiations are fluid, threats of new sectoral tariffs continue, and US trade actions remain unpredictable. Against this backdrop, the July Monetary Policy Report (MPR) does not present conventional base case projections for GDP growth and inflation in Canada and globally. Instead, it presents a current tariff scenario based on tariffs in place or agreed as of July 27, and two alternative scenarios—one with an escalation and another with a de-escalation of tariffs.

While US tariffs have created volatility in global trade, the global economy has been reasonably resilient. In the United States, the pace of growth moderated in the first half of 2025, but the labour market has remained solid. US CPI inflation ticked up in June with some evidence that tariffs are starting to be passed on to consumer prices. The euro area economy grew modestly in the first half of the year. In China, the decline in exports to the United States has been largely offset by an increase in exports to the rest of the world. Global oil prices are close to their levels in April despite some volatility. Global equity markets have risen, and corporate credit spreads have narrowed. Longer-term government bond yields have moved up. Canada’s exchange rate has appreciated against a broadly weaker US dollar.

The current tariff scenario has global growth slowing modestly to around 2½% by the end of 2025 before returning to around 3% over 2026 and 2027.

In Canada, US tariffs are disrupting trade but overall, the economy is showing some resilience so far. After robust growth in the first quarter of 2025 due to a pull-forward in exports to get ahead of tariffs, GDP likely declined by about 1.5% in the second quarter. This contraction is mostly due to a sharp reversal in exports following the pull-forward, as well as lower US demand for Canadian goods due to tariffs. Growth in business and household spending is being restrained by uncertainty. Labour market conditions have weakened in sectors affected by trade, but employment has held up in other parts of the economy. The unemployment rate has moved up gradually since the beginning of the year to 6.9% in June and wage growth has continued to ease. A number of economic indicators suggest excess supply in the economy has increased since January.

In the current tariff scenario, after contracting in the second quarter, GDP growth picks up to about 1% in the second half of this year as exports stabilize and household spending increases gradually. In this scenario, economic slack persists in 2026 and diminishes as growth picks up to close to 2% in 2027. In the de-escalation scenario, economic growth rebounds faster, while in the escalation scenario, the economy contracts through the rest of this year.

CPI inflation was 1.9% in June, up slightly from the previous month. Excluding taxes, inflation rose to 2.5% in June, up from around 2% in the second half of last year. This largely reflects an increase in non-energy goods prices. High shelter price inflation remains the main contributor to overall inflation, but it continues to ease. Based on a range of indicators, underlying inflation is assessed to be around 2½%.

In the current tariff scenario, total inflation stays close to 2% over the scenario horizon as the upward and downward pressures on inflation roughly offset. There are risks around this inflation scenario. As the alternative scenarios illustrate, lower tariffs would reduce the direct upward pressure on inflation and higher tariffs would increase it. In addition, many businesses are reporting costs related to sourcing new suppliers and developing new markets. These costs could add upward pressure to consumer prices.

With still high uncertainty, the Canadian economy showing some resilience, and ongoing pressures on underlying inflation, Governing Council decided to hold the policy interest rate unchanged. We will continue to assess the timing and strength of both the downward pressures on inflation from a weaker economy and the upward pressures on inflation from higher costs related to tariffs and the reconfiguration of trade. If a weakening economy puts further downward pressure on inflation and the upward price pressures from the trade disruptions are contained, there may be a need for a reduction in the policy interest rate.

Governing Council is proceeding carefully, with particular attention to the risks and uncertainties facing the Canadian economy. These include: the extent to which higher US tariffs reduce demand for Canadian exports; how much this spills over into business investment, employment and household spending; how much and how quickly cost increases from tariffs and trade disruptions are passed on to consumer prices; and how inflation expectations evolve.

We are focused on ensuring that Canadians continue to have confidence in price stability through this period of global upheaval. We will support economic growth while ensuring inflation remains well controlled.

Every day I get more astonished that Social Security isn’t a gigantic issue in the States. It’s going broke – in about 10 years it won’t be able to pay its obligations, as disbursements outpace contributions and the buffer is running out. And yet, nobody seems to care. I don’t understand why the Democrats aren’t banging this drum at every opportunity – it might be because any solution will necessarily involve hikes in the contribution rate and nobody wants to be the bearer of bad news, but are they all really that craven? Perhaps Bessent’s remarks represent an attempt to set the foundations for a political defence:

Treasury Secretary Scott Bessent on Wednesday likened the Trump accounts created by Republicans’ massive new domestic policy law to “a backdoor for privatizing Social Security.” Democrats are already launching political attacks.

Bessent was discussing the Trump accounts at a Breitbart policy panel. The federal government will contribute $1,000 into these new tax-deferred investment accounts for US citizen children born between 2025 and 2028, while parents and others can contribute up to $5,000 annually. The funds are intended to be used for higher education, buying a home or starting a small business.

The accounts can also be used to help Americans better understand investing and serve as a way to save for retirement, Bessent said. Then he threw out a comment that had Democrats immediately up in arms.

“In a way, it is a backdoor for privatizing Social Security,” he said. “Social Security is a defined benefit plan paid out. To the extent that if, all of a sudden, these accounts grow and you have in the hundreds of thousands of dollars for your retirement, then that’s a game changer, too.”

There was some mock outrage, but it will be noted that no actual solution was offered by the Dems:

“Donald Trump’s Treasury Secretary Scott Bessent just said the quiet part out loud: The administration is scheming to privatize Social Security,” Tim Hogan, the Democratic National Committee’s senior adviser for messaging, mobilization and strategy, said in a statement. “Trump is now coming after American seniors with a ‘backdoor’ scam to take away the benefits they earned.”

…

“Republicans’ ultimate goal is to privatize Social Security, and there isn’t a backdoor they won’t try to make Wall Street’s dream a reality,” Neal said in a statement. “For everyone else though, it’s yet another warning sign that they cannot be trusted to safeguard the program millions rely on and have paid into over a lifetime of work.”

Current proposals are simply a joke:

Cassidy and Kaine outlined their proposal last week in a Washington Post op-ed, describing a new $1.5 trillion investment fund separate from the current Social Security Trust Fund. The new fund would be structured as a sovereign wealth fund, similar to those used by other countries or the U.S. government’s own Thrift Savings Plan.

Instead of relying only on payroll taxes and low-return government bonds, this fund would be invested in a mix of stocks, bonds, and other assets.

The goal? Generate higher long-term returns to help close the projected funding gap without cutting benefits.

According to the senators, the fund would be given 75 years to grow. During that time, the U.S. Treasury would continue to pay Social Security benefits and would later be repaid by the fund once it matures.

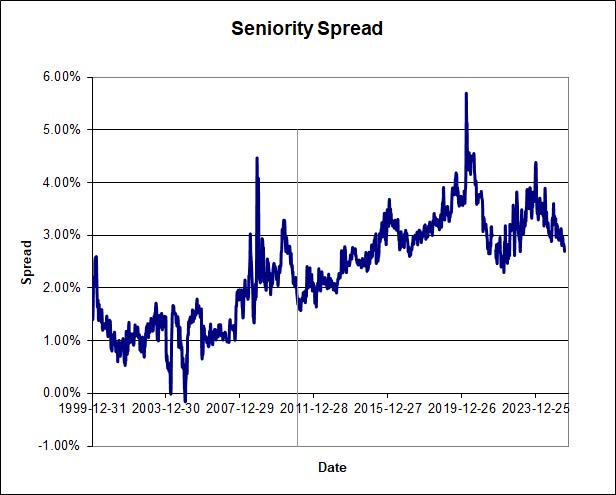

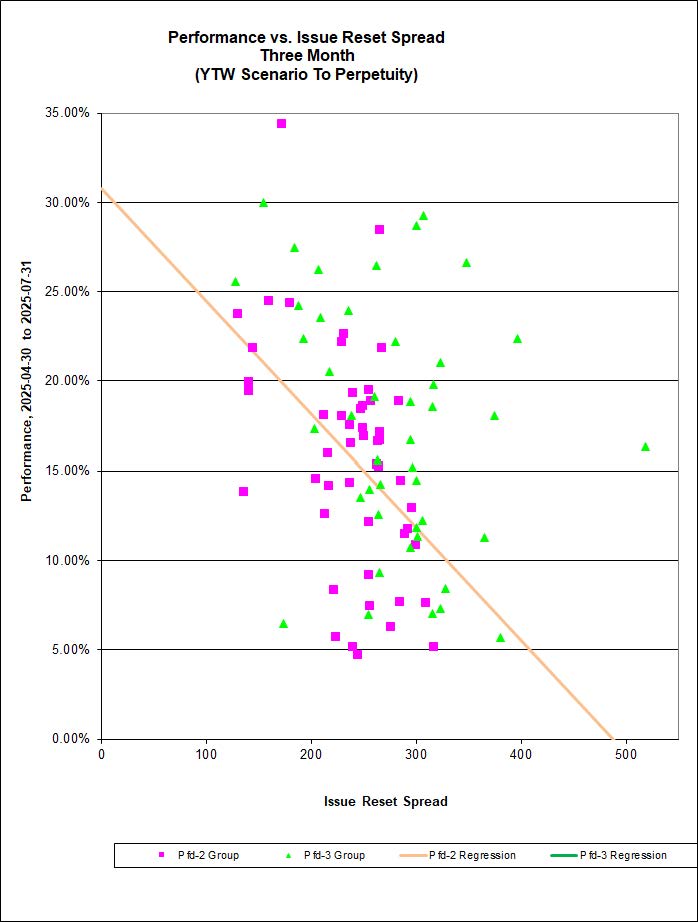

PerpetualDiscounts now yield 5.79%, equivalent to 7.53% interest at the standard conversion factor of 1.3x. Long corporates now yield 4.96%, so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now 255bp, a slight (and perhaps spurious) widening from the 250bp reported July 23.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0392 % |

2,349.6 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0392 % |

4,573.8 |

| Floater |

6.80 % |

6.90 % |

46,205 |

12.66 |

2 |

-0.0392 % |

2,635.9 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.1348 % |

3,681.7 |

| SplitShare |

4.75 % |

4.16 % |

55,178 |

2.42 |

7 |

0.1348 % |

4,396.7 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.1348 % |

3,430.5 |

| Perpetual-Premium |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0553 % |

3,029.7 |

| Perpetual-Discount |

5.68 % |

5.79 % |

46,219 |

14.19 |

32 |

0.0553 % |

3,303.8 |

| FixedReset Disc |

5.55 % |

6.24 % |

123,224 |

13.24 |

40 |

0.4611 % |

3,030.8 |

| Insurance Straight |

5.55 % |

5.67 % |

56,464 |

14.35 |

19 |

0.2279 % |

3,262.7 |

| FloatingReset |

5.49 % |

5.35 % |

37,572 |

14.86 |

2 |

0.2124 % |

3,720.8 |

| FixedReset Prem |

5.73 % |

5.03 % |

108,450 |

2.95 |

16 |

-0.1184 % |

2,630.1 |

| FixedReset Bank Non |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.4611 % |

3,098.1 |

| FixedReset Ins Non |

5.24 % |

5.69 % |

69,697 |

14.10 |

14 |

-0.1878 % |

3,051.8 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| GWO.PR.R |

Insurance Straight |

-1.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.11

Evaluated at bid price : 21.11

Bid-YTW : 5.76 % |

| CU.PR.H |

Perpetual-Discount |

-1.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 23.14

Evaluated at bid price : 23.40

Bid-YTW : 5.70 % |

| PWF.PF.A |

Perpetual-Discount |

-1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 19.85

Evaluated at bid price : 19.85

Bid-YTW : 5.71 % |

| ENB.PR.J |

FixedReset Disc |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 22.13

Evaluated at bid price : 22.60

Bid-YTW : 6.46 % |

| GWO.PR.I |

Insurance Straight |

1.08 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 20.50

Evaluated at bid price : 20.50

Bid-YTW : 5.56 % |

| TD.PF.I |

FixedReset Prem |

1.10 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2027-10-31

Maturity Price : 25.00

Evaluated at bid price : 26.54

Bid-YTW : 3.45 % |

| SLF.PR.D |

Insurance Straight |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.23

Evaluated at bid price : 21.23

Bid-YTW : 5.30 % |

| ENB.PR.N |

FixedReset Disc |

1.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 23.02

Evaluated at bid price : 24.20

Bid-YTW : 6.22 % |

| FTS.PR.J |

Perpetual-Discount |

1.37 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.91

Evaluated at bid price : 22.15

Bid-YTW : 5.44 % |

| BN.PF.F |

FixedReset Disc |

1.48 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 22.47

Evaluated at bid price : 23.26

Bid-YTW : 6.41 % |

| MFC.PR.C |

Insurance Straight |

1.51 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.25

Evaluated at bid price : 21.52

Bid-YTW : 5.28 % |

| BN.PF.E |

FixedReset Disc |

1.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.42

Evaluated at bid price : 21.68

Bid-YTW : 6.42 % |

| GWO.PR.P |

Insurance Straight |

2.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 23.64

Evaluated at bid price : 23.91

Bid-YTW : 5.70 % |

| SLF.PR.E |

Insurance Straight |

2.70 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.31

Evaluated at bid price : 21.31

Bid-YTW : 5.34 % |

| BN.PR.R |

FixedReset Disc |

8.63 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 20.26

Evaluated at bid price : 20.26

Bid-YTW : 6.55 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| BMO.PR.Y |

FixedReset Disc |

66,337 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2025-09-24

Maturity Price : 25.00

Evaluated at bid price : 24.95

Bid-YTW : 4.45 % |

| BN.PF.E |

FixedReset Disc |

29,767 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.42

Evaluated at bid price : 21.68

Bid-YTW : 6.42 % |

| SLF.PR.D |

Insurance Straight |

25,950 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.23

Evaluated at bid price : 21.23

Bid-YTW : 5.30 % |

| ENB.PR.N |

FixedReset Disc |

25,744 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 23.02

Evaluated at bid price : 24.20

Bid-YTW : 6.22 % |

| CU.PR.I |

FixedReset Prem |

23,706 |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2025-12-01

Maturity Price : 25.00

Evaluated at bid price : 25.32

Bid-YTW : 2.85 % |

| MFC.PR.C |

Insurance Straight |

23,243 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.25

Evaluated at bid price : 21.52

Bid-YTW : 5.28 % |

| There were 9 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. |

| Issue |

Index |

Quote Data and Yield Notes |

| ENB.PR.B |

FixedReset Disc |

Quote: 20.55 – 24.00

Spot Rate : 3.4500

Average : 1.8635

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 20.55

Evaluated at bid price : 20.55

Bid-YTW : 6.77 % |

| BN.PR.N |

Perpetual-Discount |

Quote: 20.45 – 21.88

Spot Rate : 1.4300

Average : 0.8260

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 20.45

Evaluated at bid price : 20.45

Bid-YTW : 5.88 % |

| MFC.PR.M |

FixedReset Ins Non |

Quote: 21.15 – 24.98

Spot Rate : 3.8300

Average : 3.4321

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.15

Evaluated at bid price : 21.15

Bid-YTW : 6.58 % |

| ENB.PF.A |

FixedReset Disc |

Quote: 21.55 – 22.55

Spot Rate : 1.0000

Average : 0.7036

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.28

Evaluated at bid price : 21.55

Bid-YTW : 6.77 % |

| ENB.PR.F |

FixedReset Disc |

Quote: 21.21 – 21.95

Spot Rate : 0.7400

Average : 0.4775

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 21.21

Evaluated at bid price : 21.21

Bid-YTW : 6.72 % |

| ENB.PR.D |

FixedReset Disc |

Quote: 20.55 – 21.50

Spot Rate : 0.9500

Average : 0.7590

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2055-07-30

Maturity Price : 20.55

Evaluated at bid price : 20.55

Bid-YTW : 6.77 % |