Today’s big news was the FOMC release:

Consistent with its statutory mandate, the Committee seeks to foster maximum employment and price stability. The Committee currently expects that, with gradual adjustments in the stance of monetary policy, economic activity will expand at a moderate pace and labor market indicators will continue to strengthen. Inflation is expected to remain low in the near term, in part because of the further declines in energy prices, but to rise to 2 percent over the medium term as the transitory effects of declines in energy and import prices dissipate and the labor market strengthens further. The Committee is closely monitoring global economic and financial developments and is assessing their implications for the labor market and inflation, and for the balance of risks to the outlook.

Given the economic outlook, the Committee decided to maintain the target range for the federal funds rate at 1/4 to 1/2 percent. The stance of monetary policy remains accommodative, thereby supporting further improvement in labor market conditions and a return to 2 percent inflation.

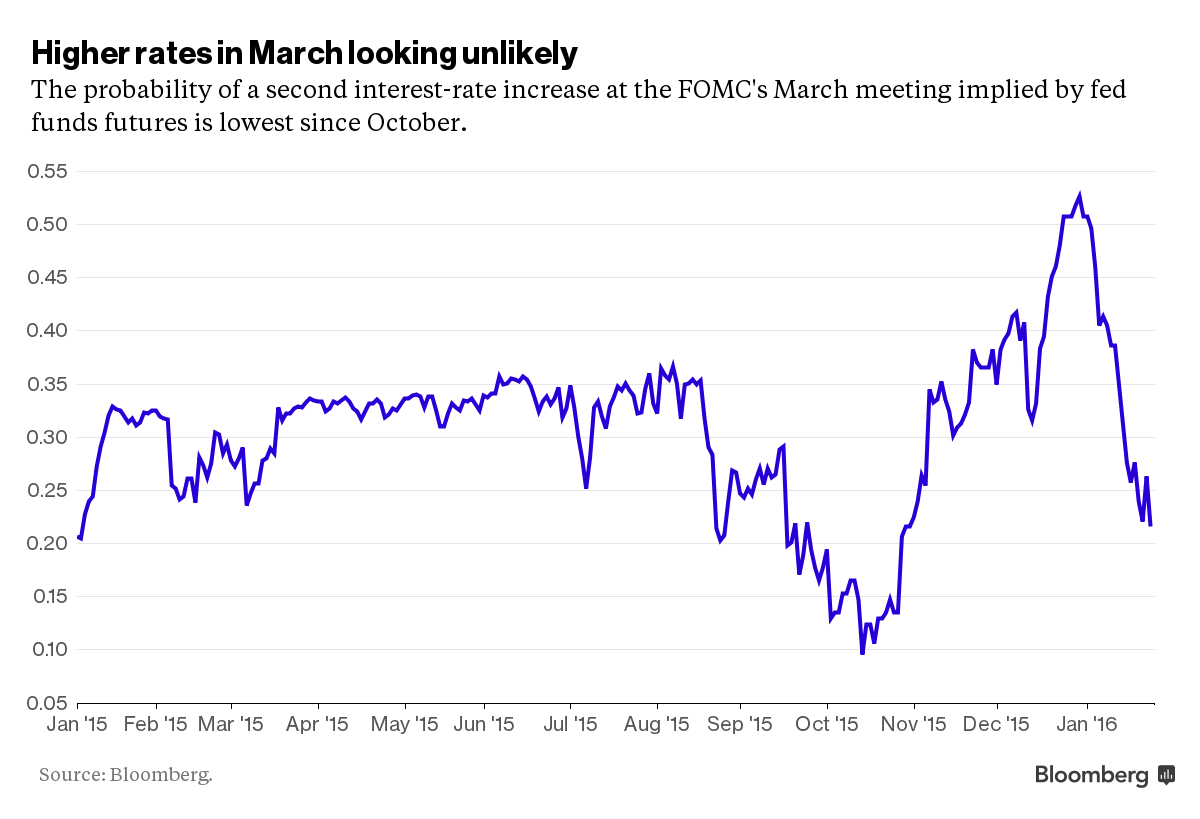

The important part was the emphasis on global conditions:

The FOMC said Wednesday it is “closely monitoring global economic and financial developments” while “assessing their implications for the labor market and inflation, and for the balance of risks to the outlook” in their statement after a two-day meeting in Washington.

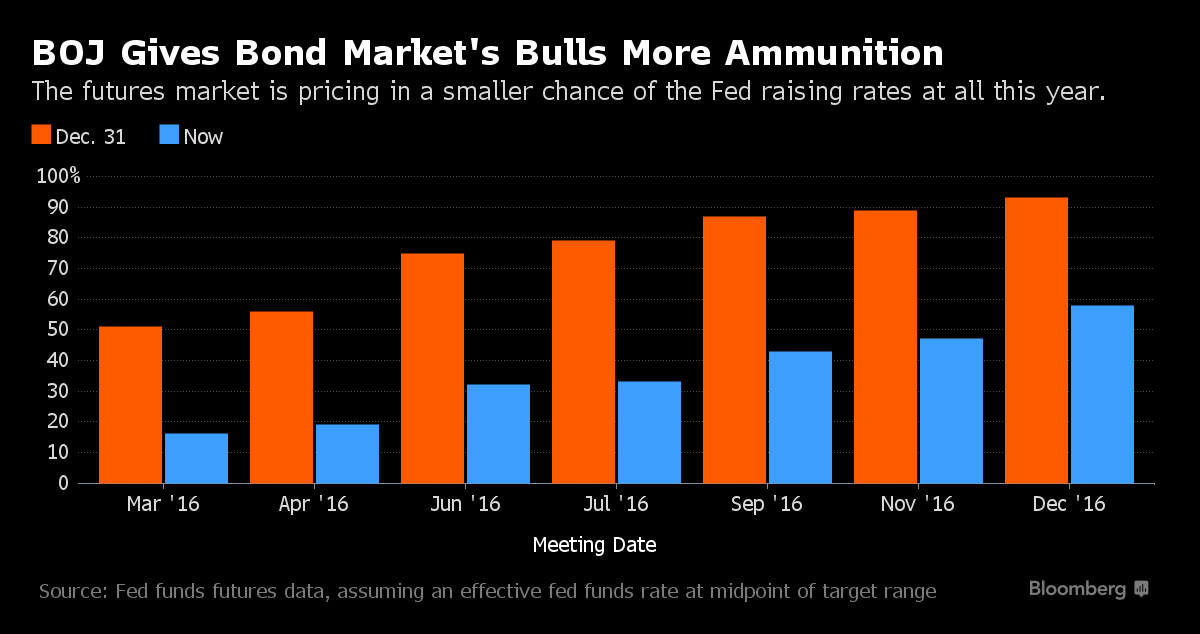

That was a soft back-pedal from December when they said risks were “balanced,” and some economists said it makes an interest-rate hike at the next FOMC meeting in March less likely, while not precluding it. The FOMC left the target for their benchmark rate unchanged at 0.25 percent to 0.5 percent.

Click for Big

Click for Big… and the markets were volatile:

U.S. stocks retreated as the Federal Reserve signaled that financial-market turmoil may pose risks to its outlook for the U.S. economy, while largely maintaining its policy stance. The dollar extended losses versus the euro, while two-year Treasuries rose.

The Standard & Poor’s 500 Index sank as the Fed said it is “closely monitoring” developments from China to Europe as well as oil for any adverse impact on the U.S. economy. Apple Inc. and Boeing Co. plunged on disappointing results as the two accounted for more than half of the Dow Jones Industrial Average’s 223-point slide. Yields on two-year Treasury notes fell a third day, as the Fed kept benchmark rates unchanged and said any future hikes would be gradual. Oil rose past $32 a barrel, and gold gained.

…

The S&P 500 fell 1.1 percent to 1,882.95 as of 4 p.m. in New York, and is headed for a January loss of 7.9 percent, the most since May 2010, with anxiety over global growth wiping as much as $2.4 trillion from the value of U.S. equities this year.

…

In Canada, Bombardier Inc.’s shares fell below C$1, the latest blow for the iconic Canadian manufacturer as it buckles under $9 billion in debt. The nation’s equity benchmark advanced 0.3 percent as energy producers and banks climbed.

Treasuries recovered from their weakest levels of the day. Led by shorter maturities, yields retreated from their Wednesday highs as stocks fell following the Fed’s decision to keep its target range at 0.25 percent to 0.5 percent, as predicted by Wall Street analysts.

The Fed also emphasized that its policy on inflation is symmetrical:

As part of its annual organizational meeting actions, the Federal Open Market Committee reaffirmed its “Statement on Longer-Run Goals and Monetary Policy Strategy,” with a revision to clarify that it views its inflation objective as symmetric, and with an updated reference to participants’ estimates of the longer-run normal unemployment rate in the most recent Summary of Economic Projections (December 2015).

…

Voting against was James Bullard, who agreed the Committee’s inflation goal is symmetric, but believed the amended language is not sufficiently focused on expected future deviations of inflation from the goal.

Meanwhile, there’s a move afoot to increase the paperwork inherent in giving advice:

Canada’s mutual fund regulator is looking into whether fees charged by fund companies – such as management fees – should be included in regulatory changes that will provide investors with greater transparency concerning the cost of financial advice and of their investments.

The changes, known as the second phase of the client relationship model (CRM2), are slated for July 16, 2016, and currently do not include the costs imposed by mutual fund managers.

The focus of CRM2 is to provide disclosure of the cost of advice rather than the overall cost of an investment product. Currently – under CRM2 rules – the Mutual Fund Dealers Association will require wealth management companies to provide each investor with an annual summary of charges paid by the investor and compensation received by the firm.

Although the changes have yet to come into effect, the MFDA received feedback from financial advisers, investment dealers, fund companies and investor advocates asking to consider expanding the reporting rules to require disclosure of the other costs of owning investment funds that are not paid to the investment firm – or the financial adviser – such as management fees, fund operating costs, redemption fees and short-term trading fees.

This will help build on the biggest regulatory success story in Canadian history:

In 2000, banks controlled 23 per cent of all Canadian long-term mutual fund assets, with independents controlling 64 per cent. By the end of 2015, the banks had more than doubled their market share to nearly 50 per cent.

The banks have an enormous advantage: distribution through their branch networks. They have also been building – and buying – fund manufacturing businesses. In many cases, they now control which funds are created and where they are sold.

So buy GICs, people! They’re FREE!

Meanwhile, bond investors aren’t getting away with much:

While not as pronounced as the rout in global equity markets, losses are beginning to pile up in the bond market too. The average spread over benchmark government yields for highly rated debt has widened to 1.83 percentage points, the most in three years, from 1.18 percentage points in March, according to Bank of America Merrill Lynch indexes. Investors lost 0.2 percent on global corporate bonds in 2015, snapping a string of annual gains that averaged 7.9 percent over the previous six years, the data show.

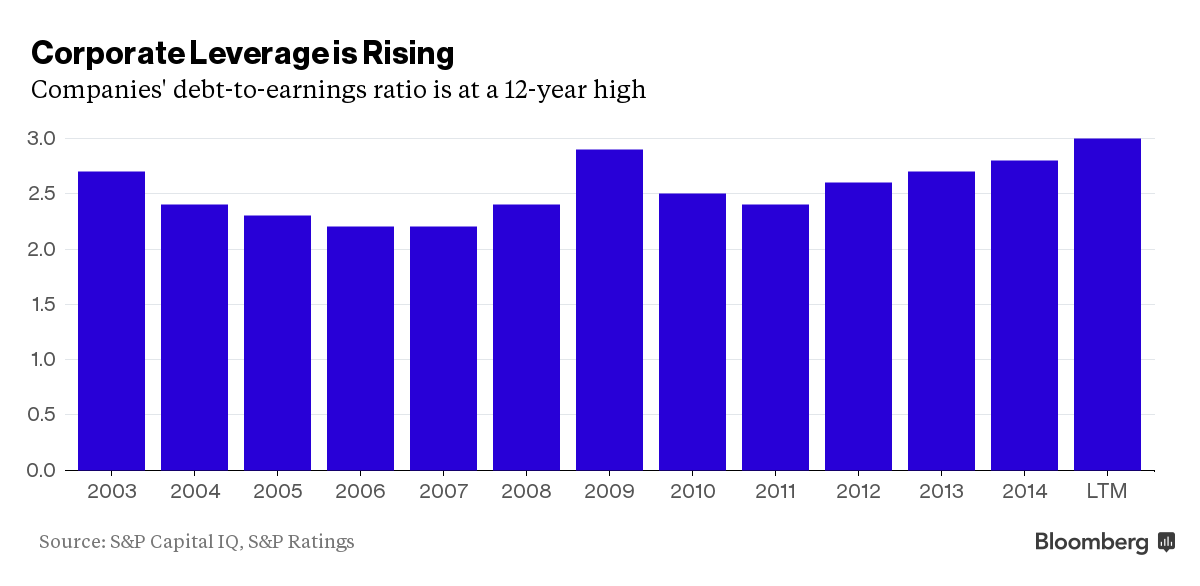

Debt at global companies rated by Standard & Poor’s reached three times earnings before interest, tax, depreciation and amortization in 2015, the highest in data going back to 2003 and up from 2.8 times last year, according to the ratings company. Total debt at listed companies in China, the world’s second-largest economy, has climbed to the highest level in three years, according to data compiled by Bloomberg.

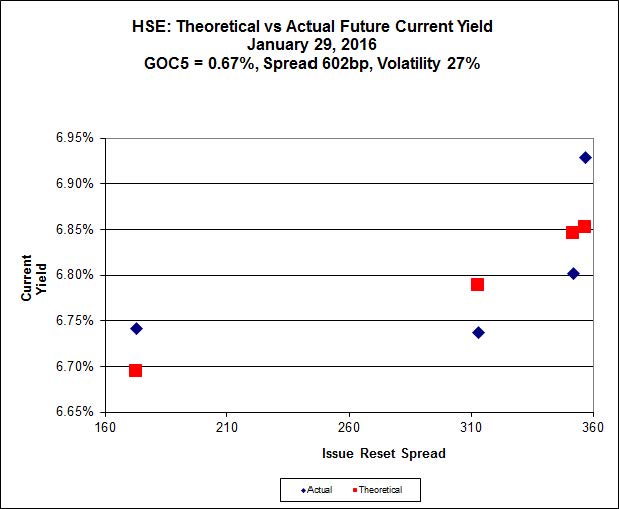

Click for Big

Click for BigBest of all, there are high hopes that soon all those pesky non-banks will be gone:

Bombardier class B shares sank below $1 in Toronto trading Wednesday, less than half the price of its $2.21-a-share equity offering a year ago. The drop raises the possibility the company will be ejected from Canada’s main S&P/TSX stock index. To be eligible for inclusion in the index, which is reviewed quarterly, a security has to have a minimum volume-weighted average price of $1 over the past three months and must represent a minimum weight of 0.05 per cent of the index.

Tomorrow is the long awaited vote on the murky DC.PR.C Exchange Offer. One must carefully guard against human propensity to form patterns from unconnected events … but Dundee just raised a bunch of cash:

Euro Pacific Canada (“Euro Pacific”) and Dundee Securities Ltd., have entered into a definitive agreement, in which Euro Pacific will acquire Dundee Goodman Private Wealth (“DGPW”), a division of Dundee Securities Ltd. Upon completion of this transaction 78 investment advisors and related support teams will move from DGPW to Euro Pacific. Approximately $3.5 billion of investible client assets will also be transferred to Euro Pacific. Euro Pacific will also acquire Dundee Securities’ separately managed account program as well as employees related to its fixed income, foreign exchange and insurance businesses. DGPW and Euro Pacific are both members of the Investment Industry Regulatory Organization of Canada (“IIROC”) and the Canadian Investor Protection Fund (“CIPF”).

Transaction Highlights:

•Increases Euro Pacific Assets Under Management and Administration to approximately $4.2 billion;

•Euro Pacific triples in size to 100 investment advisors along with related support staff and adds offices in Toronto, Montreal, Ottawa, Calgary, Vancouver and Victoria;

•Advances Dundee’s focus of growing its alternative asset management and private investment counsel business lines;

•Dundee and Euro Pacific will enter into a distribution agreement for future differentiated products; and

•The transaction is expected to result in approximately $40 million of additional liquidity and ongoing cost savings to Dundee, which will support strategic priorities.

It was a mixed day for the Canadian preferred share market, with PerpetualDiscounts off 27bp, FixedResets up 14bp and DeemedRetractibles gaining 12bp. The Performance Highlights table is its usual jolly self. Volume was above average.

PerpetualDiscounts now yield 5.96%, equivalent to 7.75% at the standard equivalency factor of 1.3x. Long corporates now yield about 4.25% (maybe a little more) so the pre-tax interest-equivalent spread (in this context, the “Seniority Spread”) is now about 350bp, a slight (and perhaps spurious) decline from the 355bp reported January 13. Incredibly elevated!

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

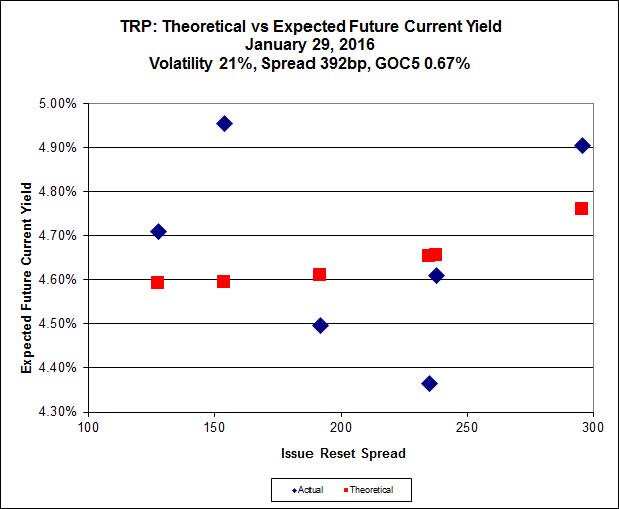

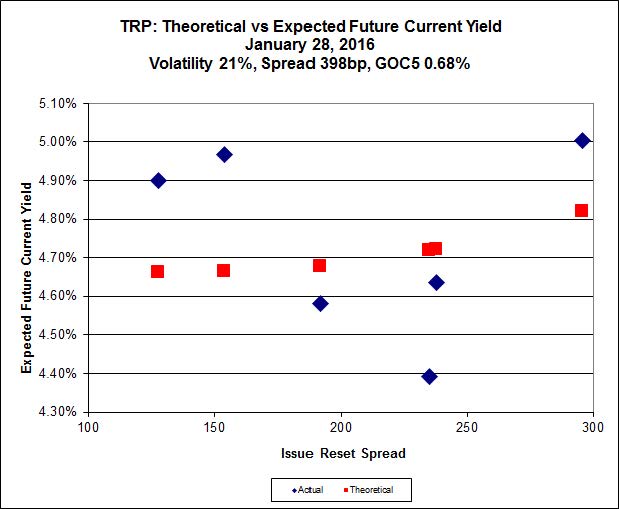

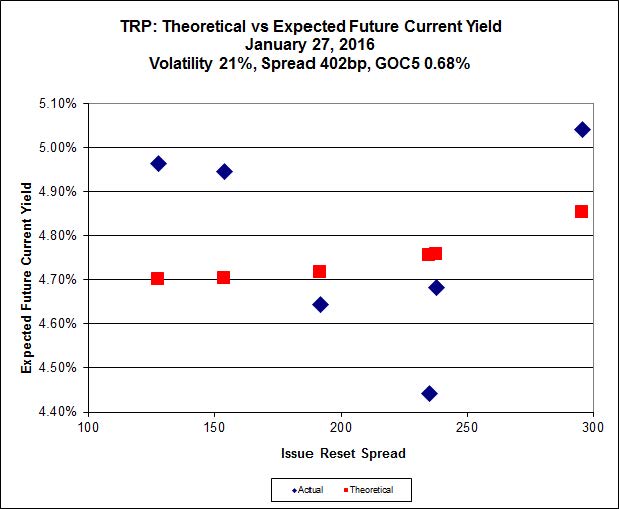

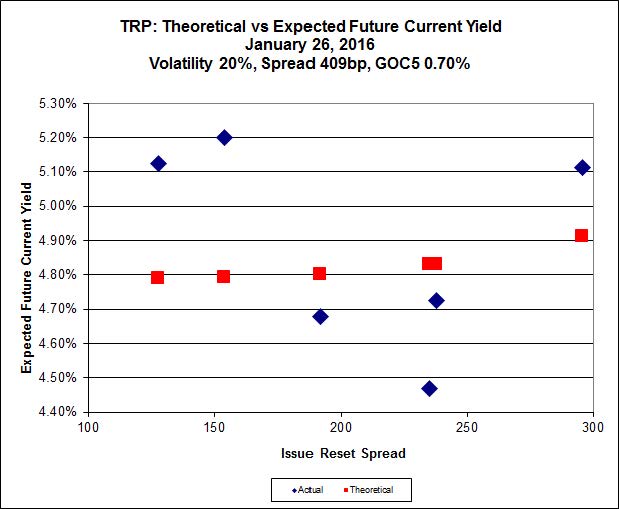

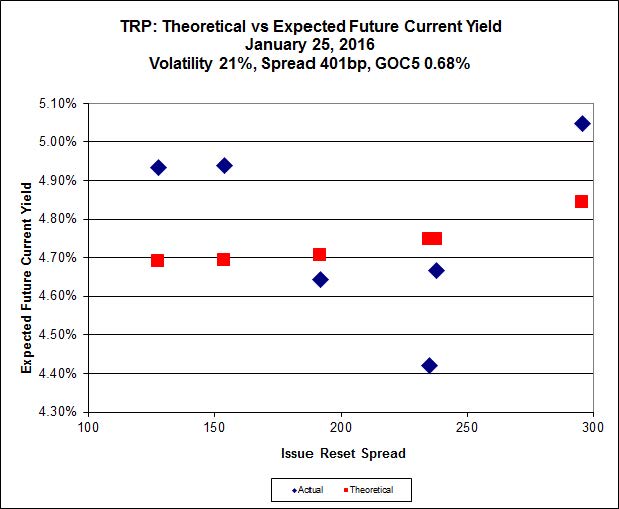

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 17.05 to be $1.12 rich, while TRP.PR.G, resetting 2020-11-30 at +296, is $0.70 cheap at its bid price of 18.05.

Click for Big

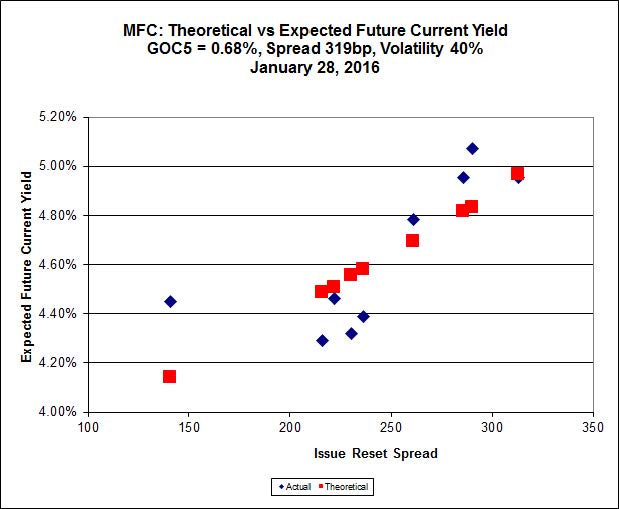

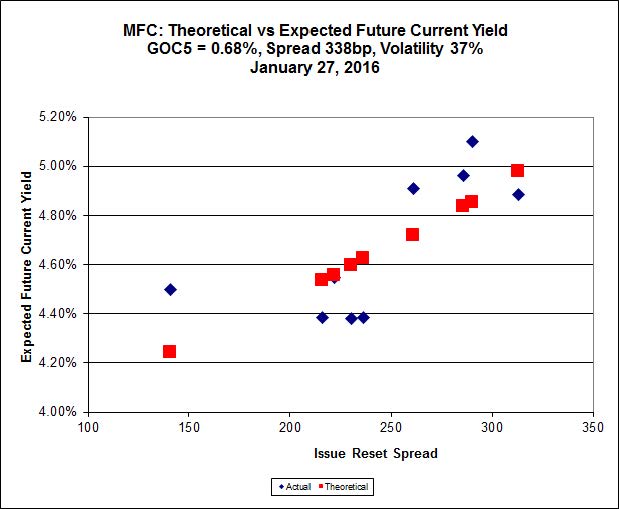

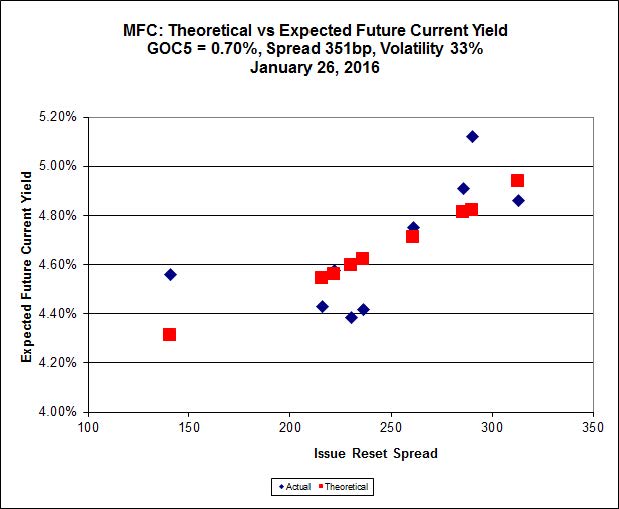

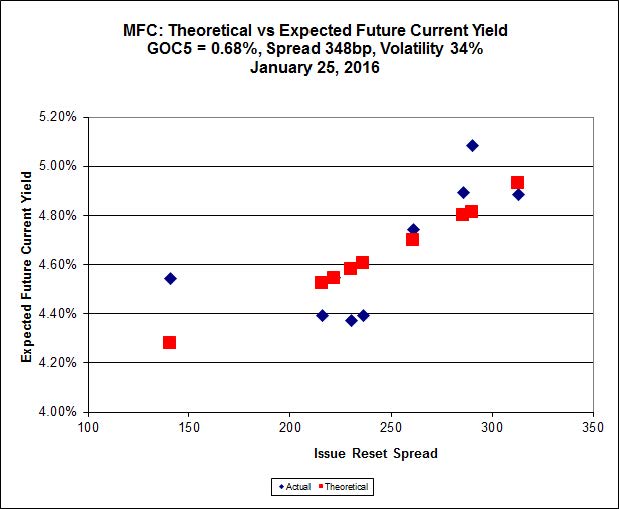

Click for BigMost expensive is MFC.PR.M, resetting at +236bp on 2019-12-19, bid at 17.33 to be 0.89 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 17.55 to be 0.90 cheap.

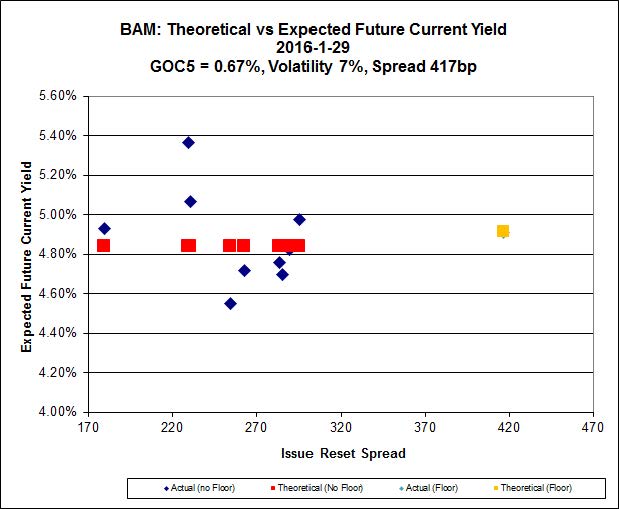

Click for Big

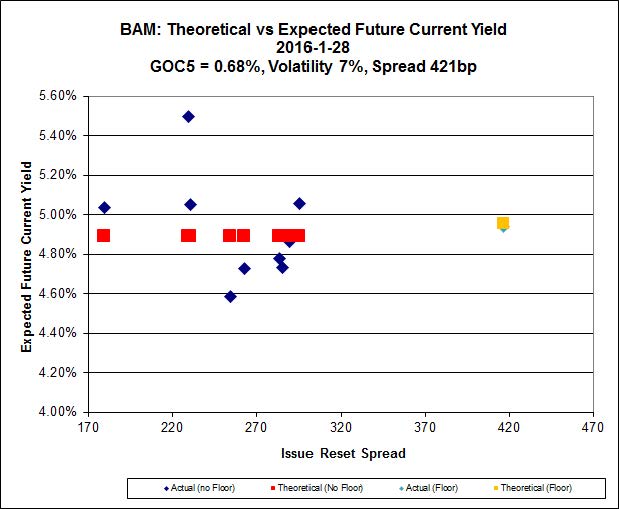

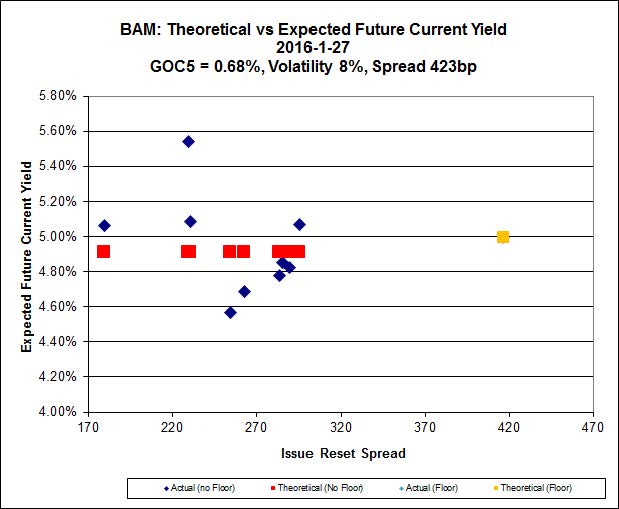

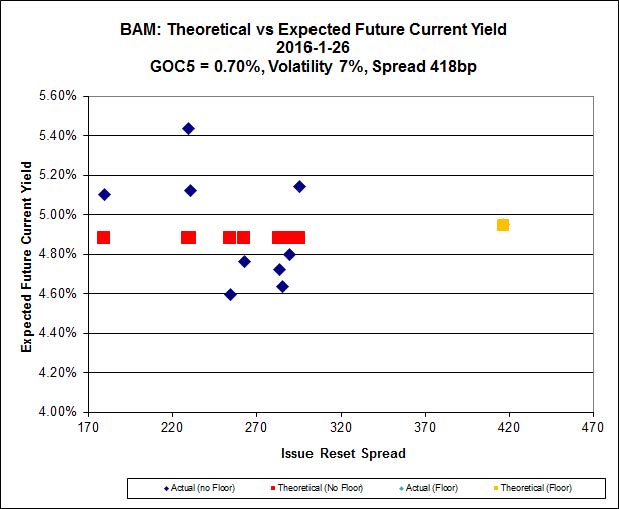

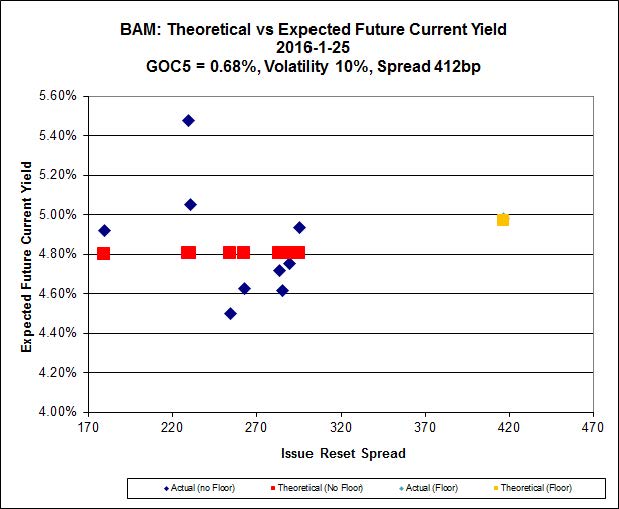

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 13.45 to be $1.72 cheap. BAM.PF.E, resetting at +255bp on 2020-3-31 is bid at 17.69 and appears to be $1.24 rich.

Click for Big

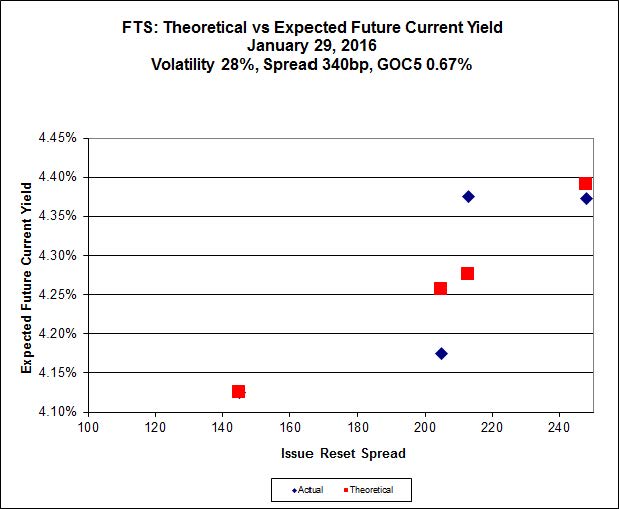

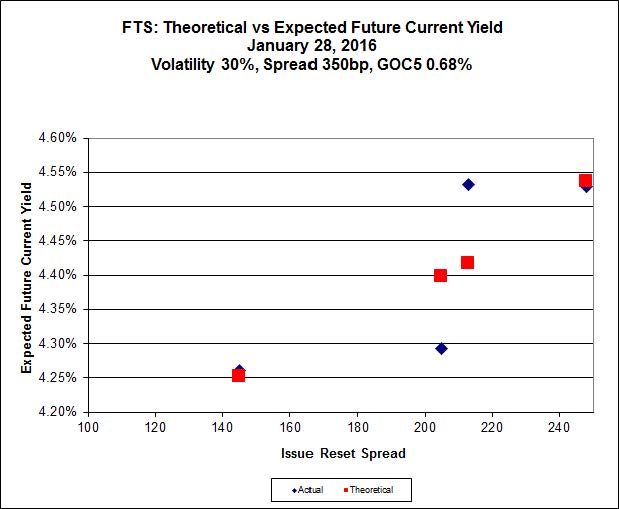

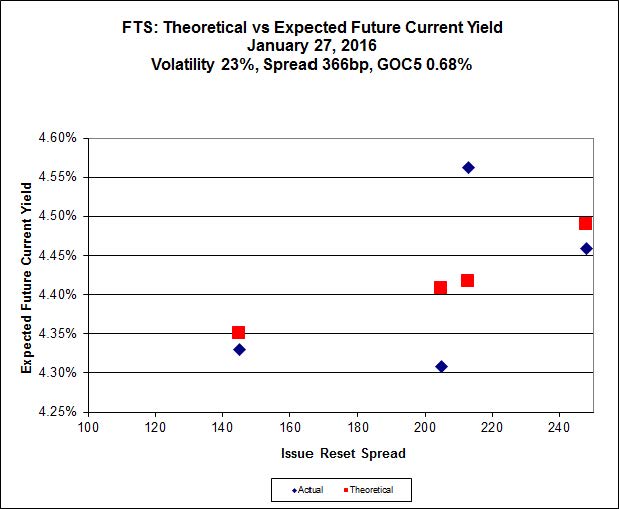

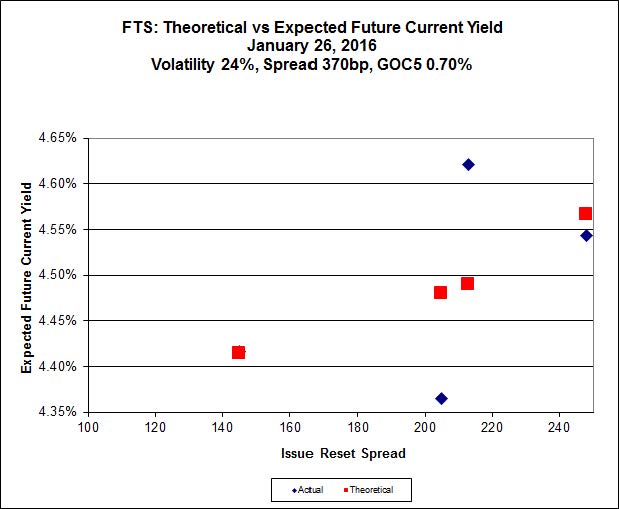

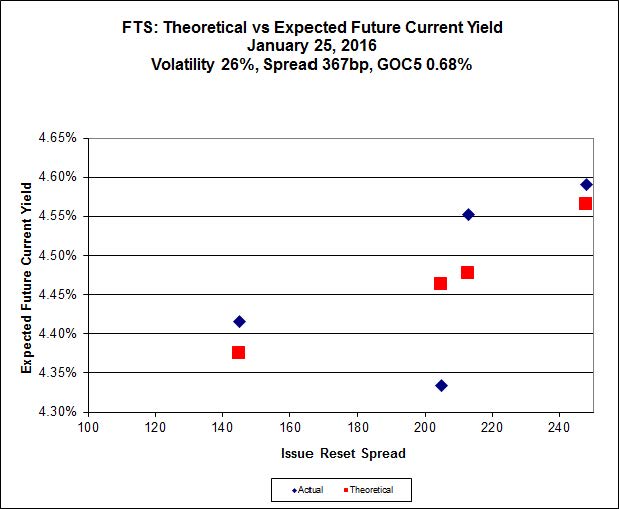

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 15.84, looks $0.36 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 15.40 and is $0.50 cheap.

Click for Big

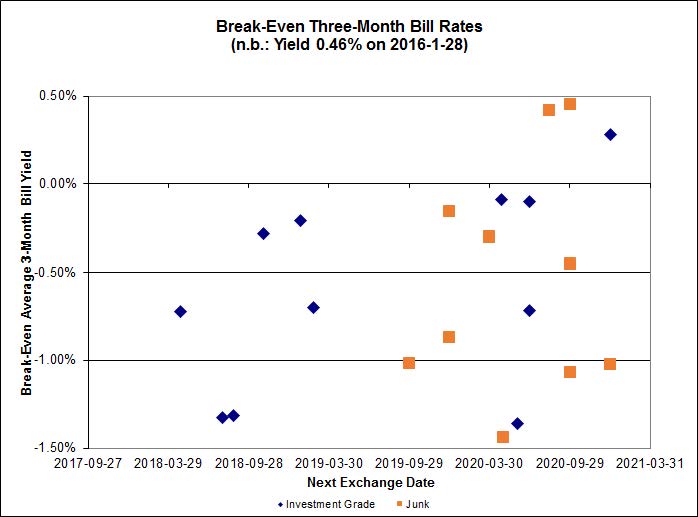

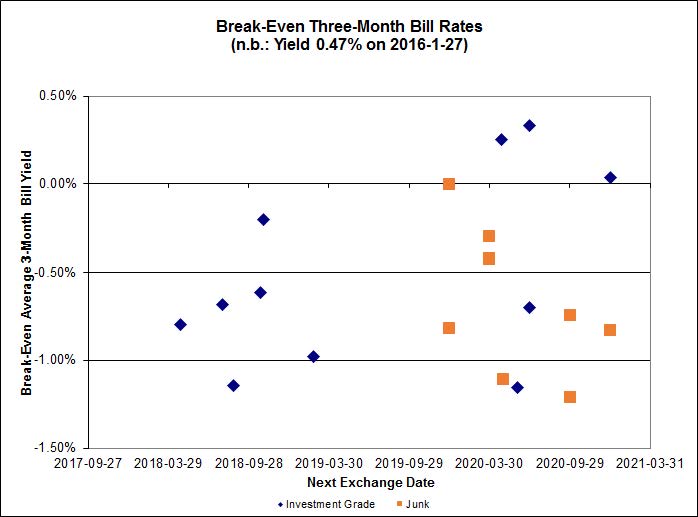

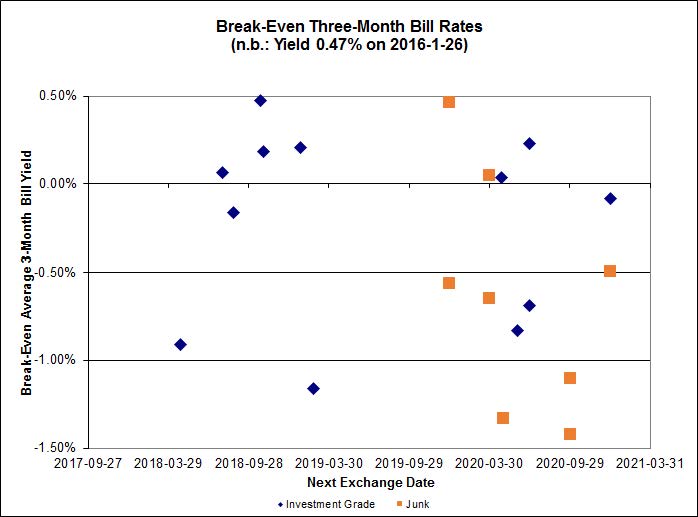

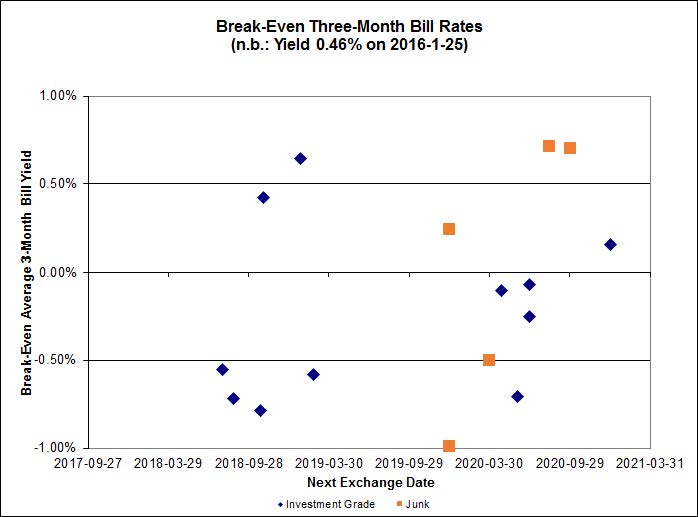

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.52%, with one outlier below -1.50% and one above +0.50%. There is one junk outlier below -1.50% and two above +0.50%.

Click for Big

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

5.21 % |

6.33 % |

20,027 |

16.30 |

1 |

1.6537 % |

1,497.7 |

| FixedFloater |

7.71 % |

6.73 % |

28,687 |

15.54 |

1 |

-1.0442 % |

2,578.3 |

| Floater |

4.77 % |

5.01 % |

73,237 |

15.47 |

4 |

1.5897 % |

1,607.3 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3917 % |

2,693.7 |

| SplitShare |

4.90 % |

6.74 % |

77,690 |

2.72 |

6 |

0.3917 % |

3,152.1 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.3917 % |

2,459.4 |

| Perpetual-Premium |

5.92 % |

5.92 % |

87,378 |

13.96 |

6 |

0.4741 % |

2,491.7 |

| Perpetual-Discount |

5.91 % |

5.96 % |

102,059 |

13.97 |

33 |

-0.2657 % |

2,440.0 |

| FixedReset |

5.69 % |

5.10 % |

235,170 |

14.64 |

83 |

0.1390 % |

1,812.0 |

| Deemed-Retractible |

5.31 % |

5.86 % |

130,509 |

6.95 |

34 |

0.1222 % |

2,542.8 |

| FloatingReset |

2.98 % |

4.80 % |

59,349 |

5.57 |

13 |

0.1601 % |

2,014.0 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| BAM.PF.F |

FixedReset |

-4.95 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 18.25

Evaluated at bid price : 18.25

Bid-YTW : 5.22 % |

| MFC.PR.J |

FixedReset |

-3.85 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.75

Bid-YTW : 9.06 % |

| BIP.PR.B |

FixedReset |

-3.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 21.85

Evaluated at bid price : 22.30

Bid-YTW : 6.25 % |

| BAM.PR.R |

FixedReset |

-2.54 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 13.45

Evaluated at bid price : 13.45

Bid-YTW : 5.74 % |

| CIU.PR.A |

Perpetual-Discount |

-2.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 19.10

Evaluated at bid price : 19.10

Bid-YTW : 6.14 % |

| BNS.PR.B |

FloatingReset |

-1.98 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.25

Bid-YTW : 5.01 % |

| ELF.PR.G |

Perpetual-Discount |

-1.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 5.99 % |

| BAM.PF.G |

FixedReset |

-1.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 18.41

Evaluated at bid price : 18.41

Bid-YTW : 5.20 % |

| BAM.PR.M |

Perpetual-Discount |

-1.74 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 18.61

Evaluated at bid price : 18.61

Bid-YTW : 6.47 % |

| MFC.PR.I |

FixedReset |

-1.60 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.84

Bid-YTW : 8.47 % |

| PWF.PR.P |

FixedReset |

-1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 10.93

Evaluated at bid price : 10.93

Bid-YTW : 5.33 % |

| FTS.PR.I |

FloatingReset |

-1.52 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 10.34

Evaluated at bid price : 10.34

Bid-YTW : 4.68 % |

| TD.PF.C |

FixedReset |

-1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 17.06

Evaluated at bid price : 17.06

Bid-YTW : 4.61 % |

| BNS.PR.R |

FixedReset |

-1.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.51

Bid-YTW : 5.21 % |

| PWF.PR.E |

Perpetual-Discount |

-1.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 22.83

Evaluated at bid price : 23.11

Bid-YTW : 5.97 % |

| BAM.PR.N |

Perpetual-Discount |

-1.27 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 18.73

Evaluated at bid price : 18.73

Bid-YTW : 6.43 % |

| BAM.PF.D |

Perpetual-Discount |

-1.19 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 19.16

Evaluated at bid price : 19.16

Bid-YTW : 6.48 % |

| GWO.PR.P |

Deemed-Retractible |

-1.18 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.50

Bid-YTW : 6.39 % |

| RY.PR.M |

FixedReset |

-1.10 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 18.05

Evaluated at bid price : 18.05

Bid-YTW : 4.71 % |

| RY.PR.F |

Deemed-Retractible |

-1.09 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.60

Bid-YTW : 5.52 % |

| RY.PR.I |

FixedReset |

-1.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.17

Bid-YTW : 4.48 % |

| BAM.PR.G |

FixedFloater |

-1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 25.00

Evaluated at bid price : 12.32

Bid-YTW : 6.73 % |

| MFC.PR.H |

FixedReset |

-1.02 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.50

Bid-YTW : 7.45 % |

| BAM.PF.A |

FixedReset |

-1.01 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 18.56

Evaluated at bid price : 18.56

Bid-YTW : 5.10 % |

| BAM.PF.B |

FixedReset |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 17.66

Evaluated at bid price : 17.66

Bid-YTW : 5.00 % |

| TD.PR.Y |

FixedReset |

1.04 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.30

Bid-YTW : 4.26 % |

| POW.PR.D |

Perpetual-Discount |

1.05 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 21.17

Evaluated at bid price : 21.17

Bid-YTW : 5.96 % |

| BNS.PR.Q |

FixedReset |

1.06 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.81

Bid-YTW : 4.69 % |

| FTS.PR.H |

FixedReset |

1.07 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 12.30

Evaluated at bid price : 12.30

Bid-YTW : 4.63 % |

| PWF.PR.I |

Perpetual-Premium |

1.11 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2016-02-26

Maturity Price : 25.00

Evaluated at bid price : 25.40

Bid-YTW : -13.83 % |

| RY.PR.P |

Perpetual-Discount |

1.14 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 23.55

Evaluated at bid price : 23.87

Bid-YTW : 5.49 % |

| BMO.PR.Q |

FixedReset |

1.15 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.51

Bid-YTW : 7.68 % |

| BAM.PR.K |

Floater |

1.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 9.51

Evaluated at bid price : 9.51

Bid-YTW : 5.02 % |

| TD.PR.T |

FloatingReset |

1.24 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.09

Bid-YTW : 4.20 % |

| BNS.PR.D |

FloatingReset |

1.25 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.63

Bid-YTW : 6.62 % |

| FTS.PR.M |

FixedReset |

1.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 17.72

Evaluated at bid price : 17.72

Bid-YTW : 4.86 % |

| SLF.PR.D |

Deemed-Retractible |

1.29 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.43

Bid-YTW : 7.35 % |

| SLF.PR.B |

Deemed-Retractible |

1.39 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.85

Bid-YTW : 6.78 % |

| RY.PR.L |

FixedReset |

1.44 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.60

Bid-YTW : 4.11 % |

| IAG.PR.G |

FixedReset |

1.59 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.20

Bid-YTW : 7.34 % |

| IFC.PR.C |

FixedReset |

1.60 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.90

Bid-YTW : 9.67 % |

| BNS.PR.Z |

FixedReset |

1.64 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 18.60

Bid-YTW : 7.48 % |

| BAM.PR.E |

Ratchet |

1.65 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 25.00

Evaluated at bid price : 13.00

Bid-YTW : 6.33 % |

| IGM.PR.B |

Perpetual-Premium |

1.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 23.98

Evaluated at bid price : 24.44

Bid-YTW : 6.05 % |

| SLF.PR.I |

FixedReset |

1.74 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 16.95

Bid-YTW : 8.89 % |

| SLF.PR.E |

Deemed-Retractible |

1.77 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.66

Bid-YTW : 7.25 % |

| PWF.PR.A |

Floater |

1.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 11.15

Evaluated at bid price : 11.15

Bid-YTW : 4.23 % |

| SLF.PR.A |

Deemed-Retractible |

1.96 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.87

Bid-YTW : 6.71 % |

| NA.PR.W |

FixedReset |

2.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 16.34

Evaluated at bid price : 16.34

Bid-YTW : 4.86 % |

| PVS.PR.B |

SplitShare |

2.16 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2019-01-10

Maturity Price : 25.00

Evaluated at bid price : 23.60

Bid-YTW : 6.74 % |

| TRP.PR.B |

FixedReset |

2.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 9.87

Evaluated at bid price : 9.87

Bid-YTW : 5.20 % |

| BAM.PR.C |

Floater |

2.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 9.44

Evaluated at bid price : 9.44

Bid-YTW : 5.06 % |

| CU.PR.C |

FixedReset |

2.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 17.05

Evaluated at bid price : 17.05

Bid-YTW : 4.73 % |

| BMO.PR.M |

FixedReset |

2.77 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.40

Bid-YTW : 4.16 % |

| VNR.PR.A |

FixedReset |

2.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 16.45

Evaluated at bid price : 16.45

Bid-YTW : 5.52 % |

| TD.PR.S |

FixedReset |

3.07 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.50

Bid-YTW : 3.91 % |

| TRP.PR.H |

FloatingReset |

3.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 9.39

Evaluated at bid price : 9.39

Bid-YTW : 4.68 % |

| TRP.PR.C |

FixedReset |

4.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 11.22

Evaluated at bid price : 11.22

Bid-YTW : 5.06 % |

| PWF.PR.T |

FixedReset |

4.71 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 20.45

Evaluated at bid price : 20.45

Bid-YTW : 3.99 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| SLF.PR.A |

Deemed-Retractible |

98,602 |

RBC bought 26,100 from Desjardins at 21.71 and another 10,000 from TD at 22.00.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.87

Bid-YTW : 6.71 % |

| NA.PR.X |

FixedReset |

96,928 |

>Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 23.10

Evaluated at bid price : 24.87

Bid-YTW : 5.59 % |

| RY.PR.O |

Perpetual-Discount |

78,130 |

TD bought three blocks of 10,000 each from RBC, all at 21.90.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 21.58

Evaluated at bid price : 21.90

Bid-YTW : 5.58 % |

| BMO.PR.W |

FixedReset |

57,258 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 16.89

Evaluated at bid price : 16.89

Bid-YTW : 4.69 % |

| CU.PR.C |

FixedReset |

55,539 |

Scotia crossed blocks of 25,000 and 16,100, both at 16.73.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 17.05

Evaluated at bid price : 17.05

Bid-YTW : 4.73 % |

| TD.PF.G |

FixedReset |

48,550 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-04-30

Maturity Price : 25.00

Evaluated at bid price : 25.45

Bid-YTW : 5.18 % |

| There were 40 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| CIU.PR.A |

Perpetual-Discount |

Quote: 19.10 – 20.25

Spot Rate : 1.1500

Average : 0.7867

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 19.10

Evaluated at bid price : 19.10

Bid-YTW : 6.14 % |

| BNS.PR.R |

FixedReset |

Quote: 22.51 – 23.80

Spot Rate : 1.2900

Average : 1.0317

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.51

Bid-YTW : 5.21 % |

| RY.PR.F |

Deemed-Retractible |

Quote: 23.60 – 24.20

Spot Rate : 0.6000

Average : 0.3537

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 23.60

Bid-YTW : 5.52 % |

| RY.PR.P |

Perpetual-Discount |

Quote: 23.87 – 24.65

Spot Rate : 0.7800

Average : 0.5734

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 23.55

Evaluated at bid price : 23.87

Bid-YTW : 5.49 % |

| BIP.PR.B |

FixedReset |

Quote: 22.30 – 22.87

Spot Rate : 0.5700

Average : 0.3806

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-27

Maturity Price : 21.85

Evaluated at bid price : 22.30

Bid-YTW : 6.25 % |

| SLF.PR.C |

Deemed-Retractible |

Quote: 20.51 – 21.10

Spot Rate : 0.5900

Average : 0.4012

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.51

Bid-YTW : 7.29 % |