For many, the new year started with a hangover:

As losses snowballed in U.S. stocks around midday, the best thing U.S. bulls had to say about the worst start to a year since 2001 was that there are 248 more trading days to make it up.

…

Taking a break and breathing helped: the Dow added almost 150 points in the last 30 minutes to pare its loss to 276 points. Still, investors returning to work from holidays were greeted by the sixth-worst start to a year since 1927 for the Standard & Poor’s 500 Index, which plunged 1.5 percent to erase $289 billion in market value as weak Chinese manufacturing data unnerved equity markets.

The selloff started in China and persisted thanks to a flareup in tension between Saudi Arabia and Iran. A report in the U.S. showed manufacturing contracted at the fastest pace in more than six years added to concerns that growth is slowing.

The rout appears to have paused, due in part to decisive action from the Chinese securities regulator:

Asian stocks erased losses as a selloff in China abated after the regulator sought to reassure investors following Monday’s plunge. Oil and industrial metals rose.

The regional share gauge erased what would have been a second day of declines as Korean and Japanese equities rose. The Shanghai Composite Index wiped out an initial slump of more than 3 percent as China’s central bank injected cash into the banking system and the securities regulator pledged to keep improving its circuit-breaker system that saw stock trading halted amid Monday’s rout. West Texas Intermediate crude rose 0.6 percent.

…

A 7 percent slump in mainland China shares triggered a trading halt there on the first day of business in 2016. The rout, which spread throughout Asia, Europe and the U.S., was sparked by weak factory data in China and exacerbated by a slide in American manufacturing. China Securities Regulatory Commission said it’s studying measures to limit the pace of stock sales by major shareholders, while the central bank Monday conducted the biggest reverse-repurchase operations since September.

Good stuff! If the market’s going down due to selling pressure, make it illegal to sell! That will fix everything!

Meanwhile Federal Reserve Vice Chairman Stanley Fischer has given a boost to the central planners and micro-managers:

He told the American Economic Association on Sunday that the Fed is not as well-equipped with regulatory powers to rein in housing and other asset bubbles as some other central banks. And he questioned whether Congress had gone too far in limiting the Fed’s ability to intervene if a crisis erupted and threatened the financial system.

“We won’t know until it’s very late” whether the Fed has been constrained too much, Fischer said at the AEA’s annual meeting in San Francisco. That’s something “we have to worry about a great deal.”

Fischer’s comments suggest that the central bank may need to rely more on monetary policy to restrain financial excesses than it has in the past. In fact, he told the conference that it might be necessary for the Fed to increase interest rates if financial markets were overheating, though the first line of defense should be the use of regulatory measures to head off bubbles.

In arguing that the Fed has less leeway to restrain speculative excesses than other central banks, Fischer pointed in particular to the property market, the epicenter of the last financial crisis. Faced with run-away real estate prices, many other countries have tightened loan-to-value or debt-to-income ratios to curb borrowing.

“In the United States, responding to such problems with these tools would require inter-agency coordination” between the Fed and other government regulators, he said. That “could make their use cumbersome at critical moments.”

On Dec. 18 the Fed and other agencies issued a thinly veiled warning to banks in which it “reminded” them about “existing regulatory guidance on prudent risk management practices for commercial real estate lending.”

But when discussing Fischer we must remember that he’s basically sound:

Lesson T4: The lender of last resort, TBTF, and moral hazard.9 The role of the central bank as lender of last resort is a central theme in Walter Bagehot’s 1873 classic on central banking, Lombard Street. The case for the central bank to be the lender of last resort is clear in the case of a liquidity crisis–one that arises from a temporary shortage of liquidity, typically in a financial panic–but less so in the case of solvency crises.10

In principle the distinction between liquidity and solvency problems should guide the actions of the central bank and the government in a financial crisis. But in a crisis, the distinction between illiquidity and insolvency is rarely clear-cut–and whether a company goes bankrupt will depend on how the authorities respond to the crisis.

Further, one has to be clear about which aspects of government actions are critical in this regard. If a firm is bankrupt, it may well be optimal for the firm to continue to operate while being reorganized, as typically happens in bankruptcies. In such a case, in which the firm’s capital is negative, the ownership of the bankrupt firm should be changed–unless the owners succeed in mobilizing more capital, in which case the company was probably not bankrupt.

And this isn’t exactly drone news – which I am confident will be prominent on this blog in 2016, if not dominant – but close enough for Government Motors work:

General Motors Co. will invest $500 million in Lyft Inc., giving the ride-hailing startup a valuation of $5.5 billion and a major ally in the global battle against Uber Technologies Inc.

The investment, part of a $1 billion financing round for Lyft, is the biggest move by an automaker to date when it comes to grappling with the meteoric rise of the ride-hailing industry.

GM and Lyft said they will work together to develop a network of self-driving cars that riders can call up on-demand, a vision of the future shared by the likes of Uber Chief Executive Officer Travis Kalanick and Google-parent Alphabet Inc. More immediately, America’s largest automaker will offer Lyft drivers vehicles for short-term rent through various hubs in U.S. cities, the companies said in separate statements on Monday.

John Shmuel of the Financial Post recently touted the interest of institutional investors in the preferred market:

There are also signs that institutional players are taking notice of the market after the recent discounts. Retail investors are usually the biggest buyers of preferred shares, with institutional investors representing only 20 per cent of the buyers of an average issuance.

But that has changed with recent issues. In September, for example, Canadian Utilities Ltd. raised $250 million by offering a rate reset preferred share at a yield of 4.5 per cent, and 70 per cent of the buyers were institutional investors.

The issue also included a new minimum yield feature, offering investors a floor that will prevent the yield from going below what it was issued at.

More recently, Royal Bank of Canada came to market with one of the biggest preferred share issuances ever in Canada, offering investors a rate of 5.5 per cent, which will reset every five years at 4.53 per cent above the government five-year bond yield.

Institutional investors were again the biggest buyers in this issue, scooping up two-thirds of the shares.

Now, this is a little peculiar; something I would want to be asking questions about. As all Assiduous Readers know, new issues are generally deprecated on PrefBlog because they have a very high negative convexity. Sometimes – rarely – the concession makes them worth-while, but in general, the fact that long-term potential capital gains are tightly constrained and that potential capital losses are not make them poor investments. I will certainly agree that a market outlook of unchanging yields can make them more attractive, especially if there is a nice new-issue concession offered; and I will also agree that in an environment of rising yields there is a certain amount of loss-mitigation due to the erosion of the premium for the embedded call; but the article is touting the potential for capital gains, in which case deeply discounted issues are the way to go. It would be interesting to have an honest heart-to-heart with the players who scooped up these new issues … but an outsider will never get that!

Assiduous Reader SafetyinNumbers brings to my attention a Normal Course Issuer Bid for AZP.PR.A, AZP.PR.B and AZP.PR.C:

Atlantic Power Corporation (TSX: ATP) (NYSE: AT) (the “Company” or “Atlantic Power”) and Atlantic Power Preferred Equity Ltd (“APPEL”) announced today that Atlantic Power intends to make a normal course issuer bid (“NCIB”) for each of the following series of the Company’s convertible unsecured subordinated debentures and its common shares and that APPEL intends to make an NCIB for each of the following series of its preferred shares (collectively, the “Public Securities”):

…

Under its previous NCIB, Atlantic Power purchased Cdn$150,000 of its 6.25% debentures at an average price of Cdn$87.12; Cdn$4,661,000 of its 5.6% debentures at an average price of Cdn$91.71; US$13,000,000 of its 5.75% debentures at an average price of US$80.80; and Cdn$10,000,000 of its 6.0% debentures at an average price of Cdn$82.19.

It’s nice to see the company delivering, given its poor credit, but I suspect that prudence will dictate that the company only buys back the debentures.

In the week following Christmas, preferred share investors enjoyed fireworks. Now they get:

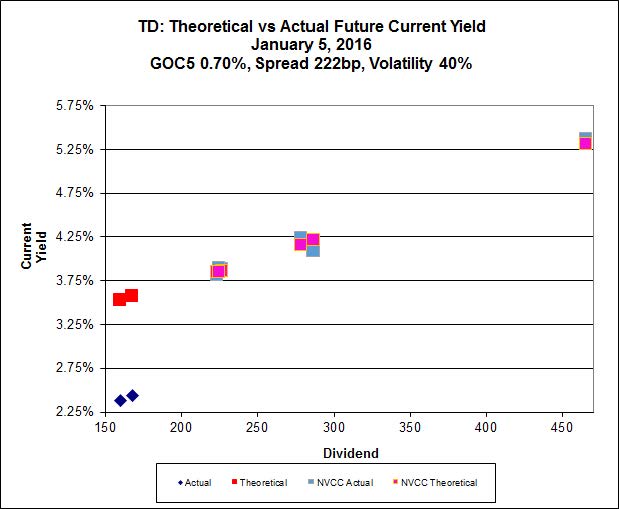

Click for Big

Click for BigIt was a horrible start to the year for the Canadian preferred share market, with PerpetualDiscounts off 41bp, FixedResets losing an incredible 297bp and DeemedRetractibles down 56bp. The Performance Highlights table is just silly, of course, with only one winner. Volume was very low – in fact, by my ‘breadth’ measure it wasn’t much more than we saw during the dead week of Christmas to New Year’s,

For as long as the FixedReset market is so violently unsettled, I’ll keep publishing updates of the more interesting and meaningful series of FixedResets’ Implied Volatilities. This doesn’t include Enbridge because although Enbridge has a large number of issues outstanding, all of which are quite liquid, the range of Issue Reset Spreads is too small for decent conclusions. The low is 212bp (ENB.PR.H; second-lowest is ENB.PR.D at 237bp) and the high is a mere 268 for ENB.PF.G.

Remember that all rich /cheap assessments are:

» based on Implied Volatility Theory only

» are relative only to other FixedResets from the same issuer

» assume constant GOC-5 yield

» assume constant Implied Volatility

» assume constant spread

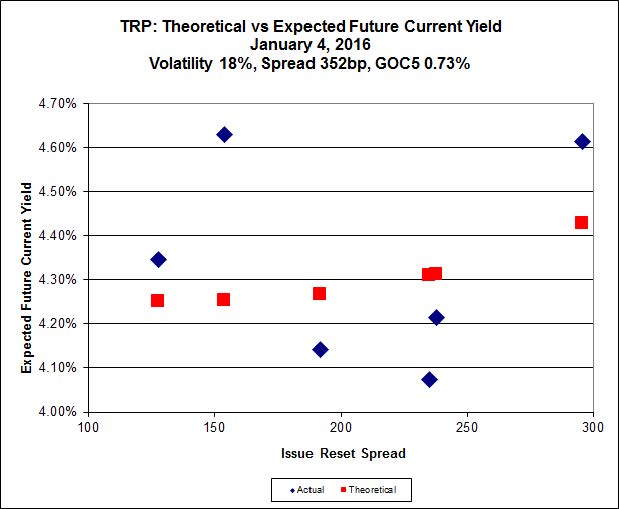

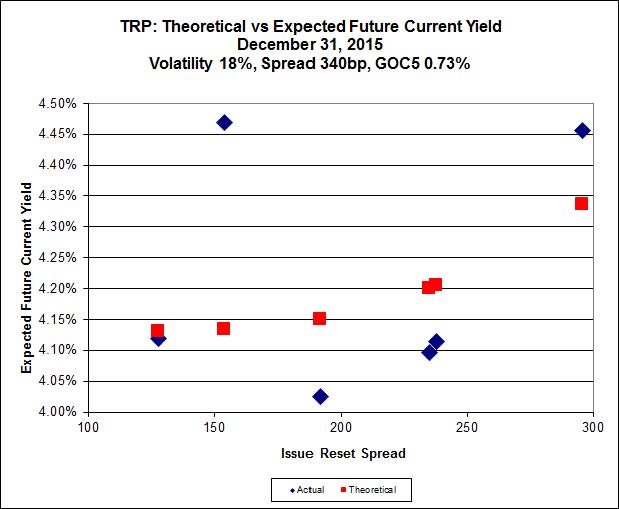

Here’s TRP:

Click for Big

Click for BigTRP.PR.E, which resets 2019-10-30 at +235, is bid at 18.90 to be $1.03 rich, while TRP.PR.C, resetting 2016-1-30 at +154, is $1.09 cheap at its bid price of 12.26.

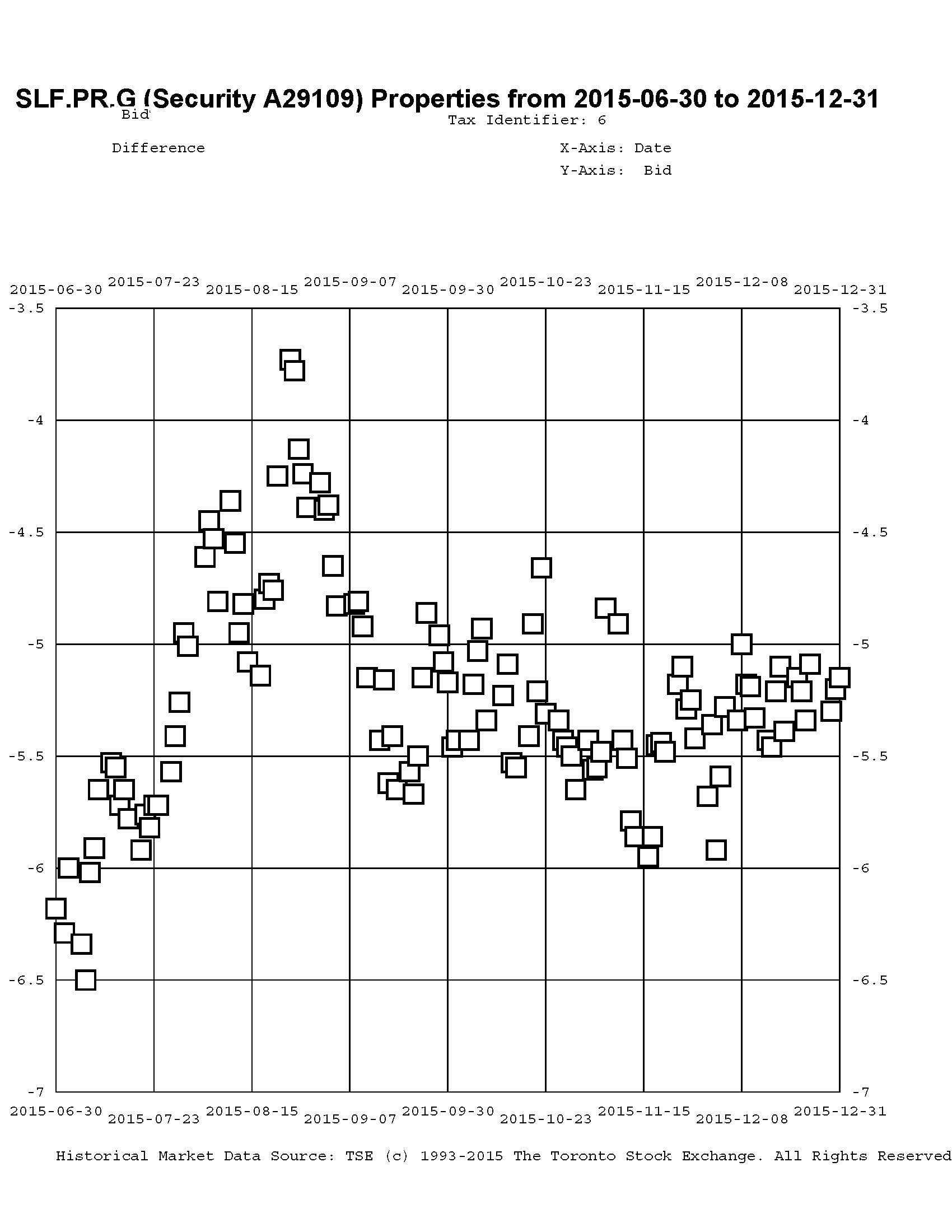

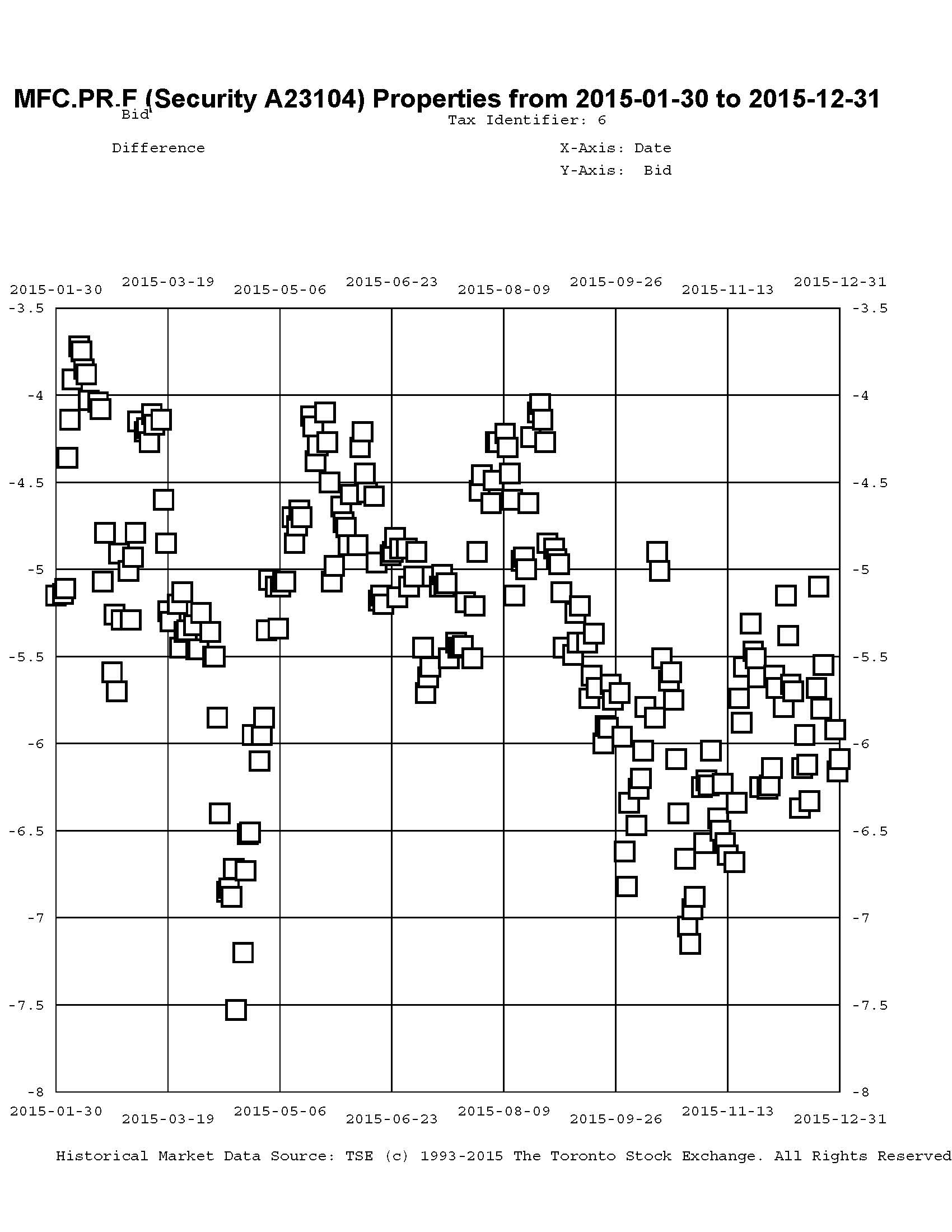

Click for Big

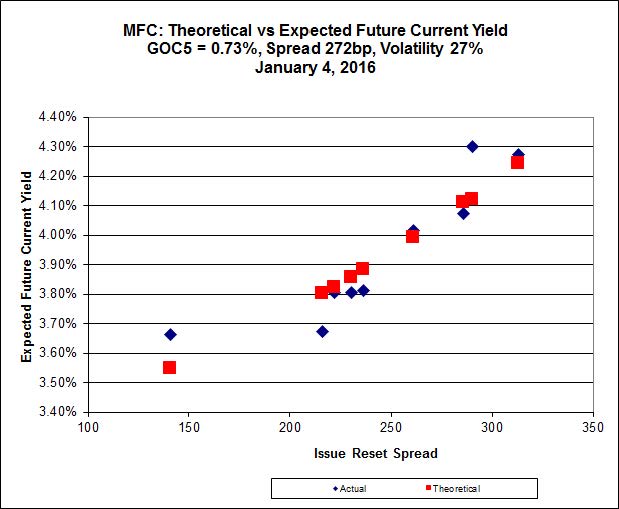

Click for BigMost expensive is MFC.PR.L, resetting at +216bp on 2019-6-19, bid at 19.67 to be 0.66 rich, while MFC.PR.G, resetting at +290bp on 2016-12-19, is bid at 21.11 to be 0.92 0cheap.

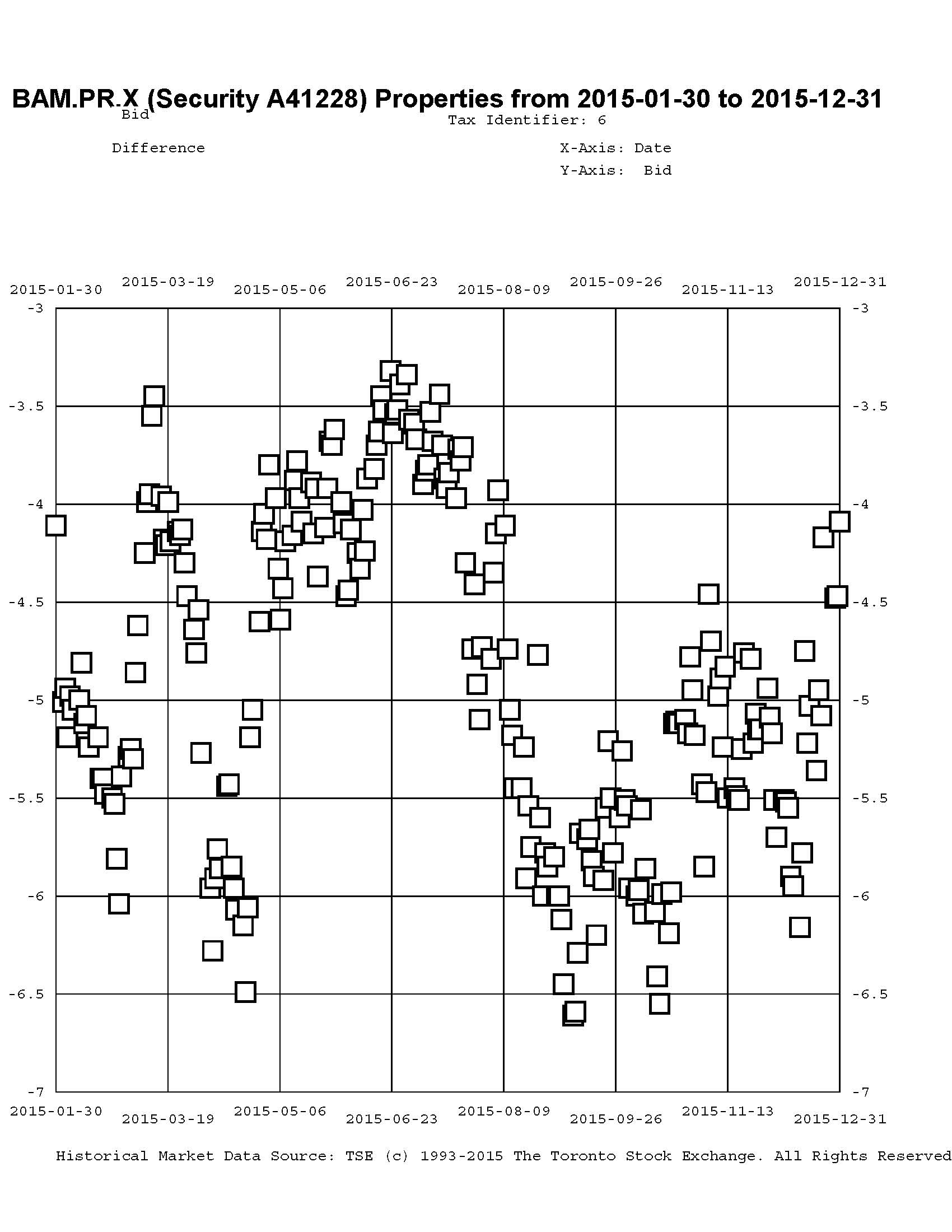

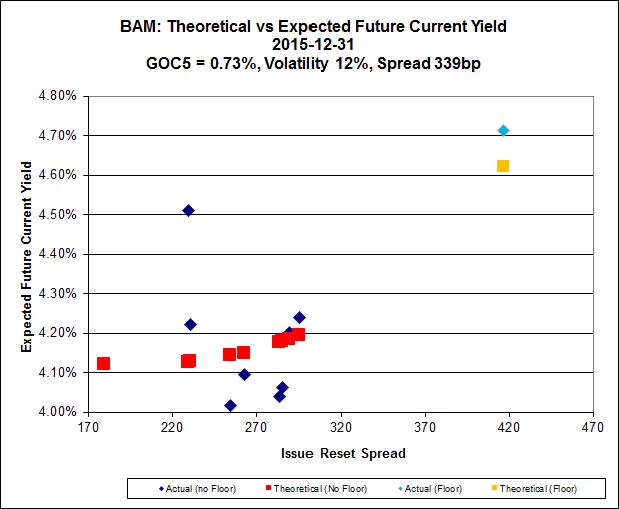

Click for Big

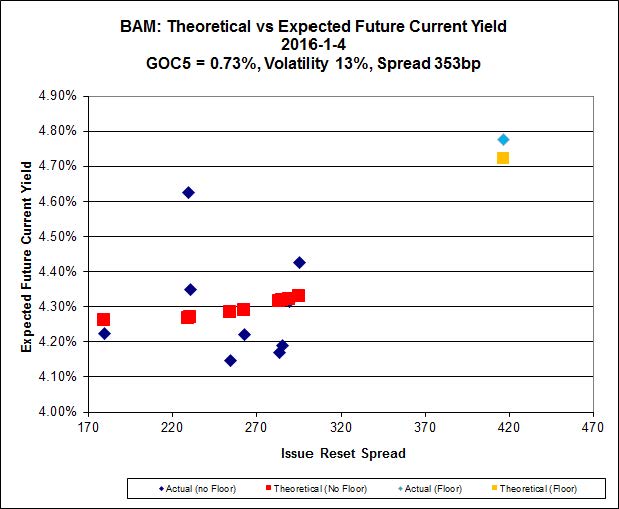

Click for BigThe cheapest issue relative to its peers is BAM.PR.R, resetting at +230bp on 2016-6-30, bid at 16.38 to be $1.37 cheap. BAM.PF.G, resetting at +284bp on 2020-6-30 is bid at 21.40 and appears to be $0.71 rich.

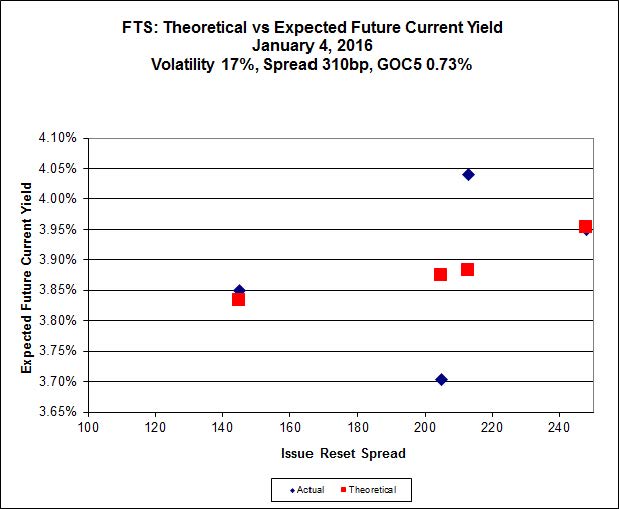

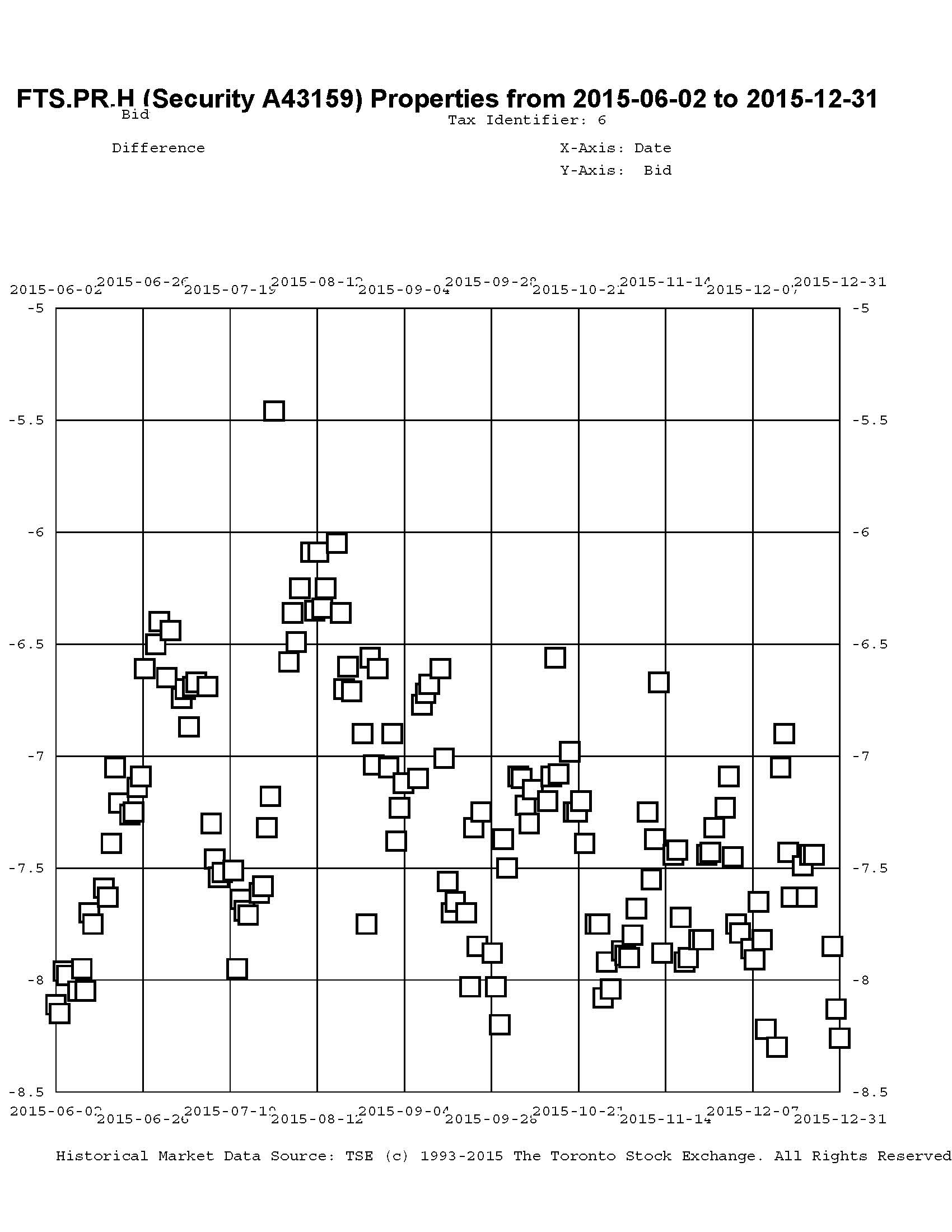

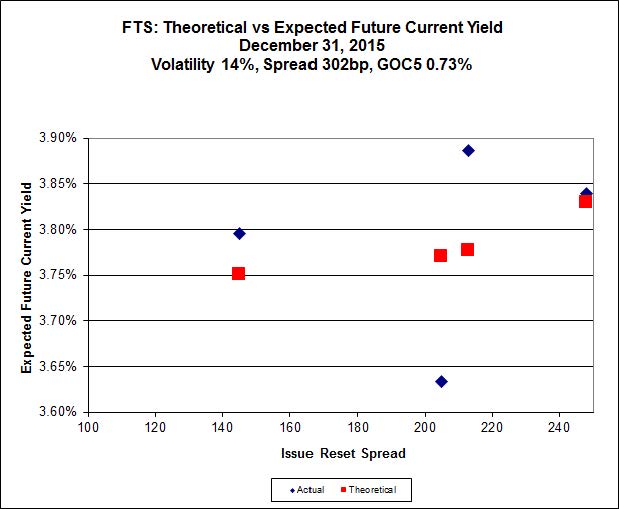

Click for Big

Click for BigFTS.PR.K, with a spread of +205bp, and bid at 18.77, looks $0.83 expensive and resets 2019-3-1. FTS.PR.G, with a spread of +213bp and resetting 2018-9-1, is bid at 17.70 and is $0.72 cheap.

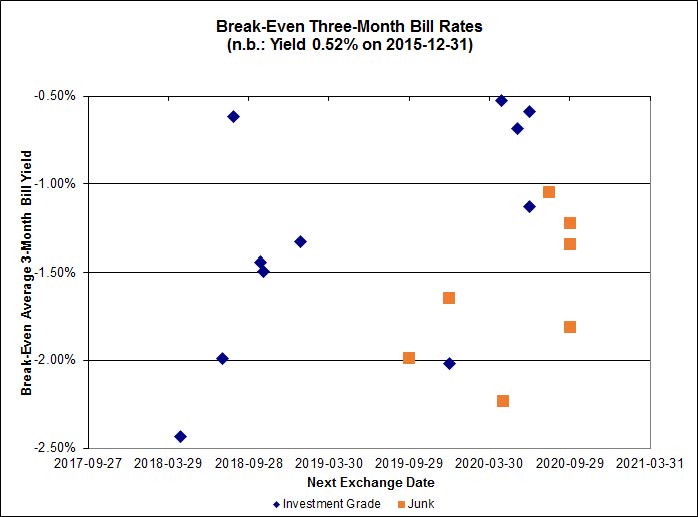

Click for Big

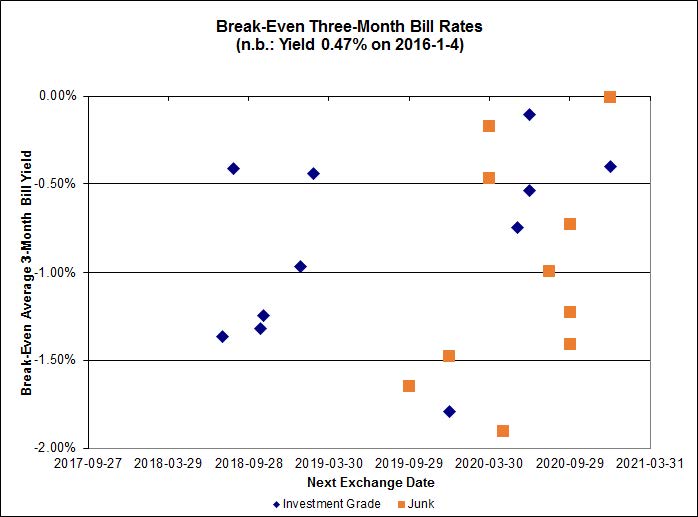

Click for BigInvestment-grade pairs predict an average three-month bill yield over the next five-odd years of -0.89%, with one outliers above 0.00%, and one below -2.00%. Note the scale of the y-axis has changed. There is one junk outlier above 0.00%.

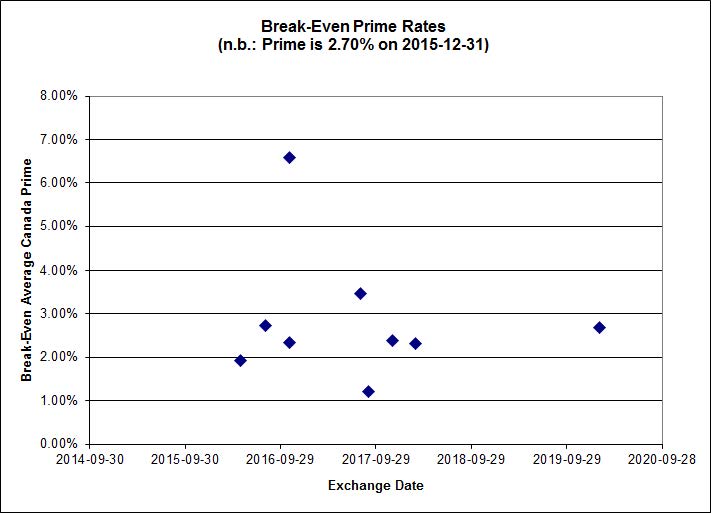

Click for Big

Click for BigShall we just say that this exhibits a high level of confidence in the continued rapacity of Canadian banks?

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

4.77 % |

5.79 % |

29,266 |

16.92 |

1 |

-1.9310 % |

1,630.4 |

| FixedFloater |

6.82 % |

6.05 % |

36,225 |

16.14 |

1 |

-0.2151 % |

2,859.5 |

| Floater |

4.19 % |

4.38 % |

78,915 |

16.69 |

4 |

-0.3538 % |

1,821.9 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.1132 % |

2,746.4 |

| SplitShare |

4.81 % |

5.78 % |

80,711 |

1.82 |

6 |

-0.1132 % |

3,213.8 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.1132 % |

2,507.5 |

| Perpetual-Premium |

5.79 % |

3.20 % |

91,891 |

0.09 |

6 |

-0.4462 % |

2,524.1 |

| Perpetual-Discount |

5.63 % |

5.68 % |

102,372 |

14.36 |

34 |

-0.4139 % |

2,556.9 |

| FixedReset |

5.07 % |

4.40 % |

255,333 |

14.78 |

81 |

-2.9709 % |

2,032.2 |

| Deemed-Retractible |

5.21 % |

5.17 % |

125,066 |

5.30 |

34 |

-0.5584 % |

2,585.1 |

| FloatingReset |

2.82 % |

4.27 % |

65,184 |

5.62 |

13 |

-1.3557 % |

2,129.8 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| VNR.PR.A |

FixedReset |

-7.28 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.47

Evaluated at bid price : 18.47

Bid-YTW : 4.99 % |

| MFC.PR.G |

FixedReset |

-6.55 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.11

Bid-YTW : 6.00 % |

| BMO.PR.Q |

FixedReset |

-6.44 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.21

Bid-YTW : 5.97 % |

| MFC.PR.H |

FixedReset |

-6.11 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.59

Bid-YTW : 5.36 % |

| GWO.PR.O |

FloatingReset |

-5.95 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 12.32

Bid-YTW : 10.63 % |

| BAM.PR.X |

FixedReset |

-5.90 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 14.98

Evaluated at bid price : 14.98

Bid-YTW : 4.47 % |

| SLF.PR.H |

FixedReset |

-5.61 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.85

Bid-YTW : 7.37 % |

| CU.PR.C |

FixedReset |

-5.45 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.07

Evaluated at bid price : 19.07

Bid-YTW : 4.21 % |

| TRP.PR.B |

FixedReset |

-5.25 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 11.56

Evaluated at bid price : 11.56

Bid-YTW : 4.41 % |

| MFC.PR.J |

FixedReset |

-5.24 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.80

Bid-YTW : 5.98 % |

| IFC.PR.A |

FixedReset |

-5.16 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 15.80

Bid-YTW : 8.94 % |

| MFC.PR.N |

FixedReset |

-5.01 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.90

Bid-YTW : 6.48 % |

| MFC.PR.K |

FixedReset |

-4.95 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.39

Bid-YTW : 6.60 % |

| SLF.PR.G |

FixedReset |

-4.87 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.65

Bid-YTW : 9.01 % |

| HSE.PR.E |

FixedReset |

-4.85 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.44

Evaluated at bid price : 18.44

Bid-YTW : 5.93 % |

| MFC.PR.I |

FixedReset |

-4.84 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.03

Bid-YTW : 5.47 % |

| HSE.PR.C |

FixedReset |

-4.82 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 17.58

Evaluated at bid price : 17.58

Bid-YTW : 5.72 % |

| HSE.PR.G |

FixedReset |

-4.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.50

Evaluated at bid price : 18.50

Bid-YTW : 5.90 % |

| BIP.PR.A |

FixedReset |

-4.68 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.55

Evaluated at bid price : 19.55

Bid-YTW : 5.58 % |

| SLF.PR.I |

FixedReset |

-4.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.41

Bid-YTW : 6.24 % |

| CM.PR.P |

FixedReset |

-4.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.92

Evaluated at bid price : 18.92

Bid-YTW : 4.13 % |

| MFC.PR.M |

FixedReset |

-4.30 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.27

Bid-YTW : 6.29 % |

| NA.PR.W |

FixedReset |

-4.22 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.39

Evaluated at bid price : 18.39

Bid-YTW : 4.28 % |

| BAM.PR.Z |

FixedReset |

-4.18 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.85

Evaluated at bid price : 20.85

Bid-YTW : 4.57 % |

| IFC.PR.C |

FixedReset |

-4.08 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.00

Bid-YTW : 6.41 % |

| FTS.PR.G |

FixedReset |

-3.80 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 17.70

Evaluated at bid price : 17.70

Bid-YTW : 4.26 % |

| RY.PR.K |

FloatingReset |

-3.79 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.61

Bid-YTW : 4.20 % |

| IAG.PR.G |

FixedReset |

-3.69 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.40

Bid-YTW : 5.78 % |

| MFC.PR.L |

FixedReset |

-3.67 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 19.67

Bid-YTW : 6.51 % |

| PWF.PR.T |

FixedReset |

-3.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 22.36

Evaluated at bid price : 22.89

Bid-YTW : 3.56 % |

| BMO.PR.S |

FixedReset |

-3.61 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.47

Evaluated at bid price : 19.47

Bid-YTW : 4.17 % |

| CM.PR.O |

FixedReset |

-3.58 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.39

Evaluated at bid price : 19.39

Bid-YTW : 4.13 % |

| TRP.PR.C |

FixedReset |

-3.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 12.26

Evaluated at bid price : 12.26

Bid-YTW : 4.61 % |

| BNS.PR.Z |

FixedReset |

-3.40 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.20

Bid-YTW : 5.90 % |

| TRP.PR.G |

FixedReset |

-3.38 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.00

Evaluated at bid price : 20.00

Bid-YTW : 4.68 % |

| BNS.PR.Y |

FixedReset |

-3.32 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.10

Bid-YTW : 5.63 % |

| BMO.PR.T |

FixedReset |

-3.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.05

Evaluated at bid price : 19.05

Bid-YTW : 4.16 % |

| BMO.PR.Y |

FixedReset |

-3.26 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.80

Evaluated at bid price : 20.80

Bid-YTW : 4.27 % |

| BAM.PF.G |

FixedReset |

-3.17 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.40

Evaluated at bid price : 21.40

Bid-YTW : 4.43 % |

| BAM.PF.E |

FixedReset |

-3.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.78

Evaluated at bid price : 19.78

Bid-YTW : 4.47 % |

| RY.PR.H |

FixedReset |

-3.06 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 4.19 % |

| BAM.PF.F |

FixedReset |

-3.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.43

Evaluated at bid price : 21.43

Bid-YTW : 4.40 % |

| BAM.PF.B |

FixedReset |

-2.97 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.90

Evaluated at bid price : 19.90

Bid-YTW : 4.40 % |

| BAM.PR.T |

FixedReset |

-2.94 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 17.47

Evaluated at bid price : 17.47

Bid-YTW : 4.47 % |

| RY.PR.Z |

FixedReset |

-2.87 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.95

Evaluated at bid price : 18.95

Bid-YTW : 4.15 % |

| TRP.PR.A |

FixedReset |

-2.79 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 16.00

Evaluated at bid price : 16.00

Bid-YTW : 4.34 % |

| FTS.PR.M |

FixedReset |

-2.78 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.32

Evaluated at bid price : 20.32

Bid-YTW : 4.20 % |

| BMO.PR.W |

FixedReset |

-2.72 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.98

Evaluated at bid price : 18.98

Bid-YTW : 4.14 % |

| HSE.PR.A |

FixedReset |

-2.67 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 12.75

Evaluated at bid price : 12.75

Bid-YTW : 4.82 % |

| BAM.PF.A |

FixedReset |

-2.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.03

Evaluated at bid price : 21.03

Bid-YTW : 4.47 % |

| TD.PF.A |

FixedReset |

-2.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.32

Evaluated at bid price : 19.32

Bid-YTW : 4.13 % |

| TD.PF.C |

FixedReset |

-2.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.95

Evaluated at bid price : 18.95

Bid-YTW : 4.20 % |

| MFC.PR.F |

FixedReset |

-2.60 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 14.60

Bid-YTW : 9.09 % |

| BAM.PR.R |

FixedReset |

-2.50 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 16.38

Evaluated at bid price : 16.38

Bid-YTW : 4.68 % |

| TD.PF.B |

FixedReset |

-2.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.15

Evaluated at bid price : 19.15

Bid-YTW : 4.16 % |

| GWO.PR.N |

FixedReset |

-2.43 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.65

Bid-YTW : 9.82 % |

| TRP.PR.D |

FixedReset |

-2.38 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.45

Evaluated at bid price : 18.45

Bid-YTW : 4.40 % |

| CIU.PR.C |

FixedReset |

-2.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 12.40

Evaluated at bid price : 12.40

Bid-YTW : 4.28 % |

| CM.PR.Q |

FixedReset |

-2.32 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.20

Evaluated at bid price : 20.20

Bid-YTW : 4.37 % |

| SLF.PR.A |

Deemed-Retractible |

-2.24 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.41

Bid-YTW : 6.96 % |

| BMO.PR.M |

FixedReset |

-2.20 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.00

Bid-YTW : 3.64 % |

| MFC.PR.C |

Deemed-Retractible |

-2.18 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.62

Bid-YTW : 7.24 % |

| TD.PF.D |

FixedReset |

-2.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.61

Evaluated at bid price : 20.61

Bid-YTW : 4.34 % |

| SLF.PR.J |

FloatingReset |

-2.00 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.72

Bid-YTW : 9.39 % |

| FTS.PR.I |

FloatingReset |

-1.96 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 12.50

Evaluated at bid price : 12.50

Bid-YTW : 3.87 % |

| MFC.PR.B |

Deemed-Retractible |

-1.95 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.13

Bid-YTW : 7.06 % |

| BAM.PR.E |

Ratchet |

-1.93 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 25.00

Evaluated at bid price : 14.22

Bid-YTW : 5.79 % |

| BNS.PR.A |

FloatingReset |

-1.93 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.41

Bid-YTW : 4.37 % |

| RY.PR.I |

FixedReset |

-1.92 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.04

Bid-YTW : 3.91 % |

| CU.PR.G |

Perpetual-Discount |

-1.89 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.26

Evaluated at bid price : 20.26

Bid-YTW : 5.63 % |

| FTS.PR.K |

FixedReset |

-1.88 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.77

Evaluated at bid price : 18.77

Bid-YTW : 3.98 % |

| TRP.PR.F |

FloatingReset |

-1.83 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 13.40

Evaluated at bid price : 13.40

Bid-YTW : 4.49 % |

| BMO.PR.R |

FloatingReset |

-1.77 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 22.70

Bid-YTW : 3.83 % |

| RY.PR.J |

FixedReset |

-1.69 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.34

Evaluated at bid price : 20.34

Bid-YTW : 4.33 % |

| CU.PR.F |

Perpetual-Discount |

-1.64 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.35

Evaluated at bid price : 20.35

Bid-YTW : 5.60 % |

| BAM.PF.C |

Perpetual-Discount |

-1.62 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.07

Evaluated at bid price : 20.07

Bid-YTW : 6.09 % |

| SLF.PR.C |

Deemed-Retractible |

-1.59 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.36

Bid-YTW : 7.33 % |

| BNS.PR.P |

FixedReset |

-1.57 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.47

Bid-YTW : 3.35 % |

| CU.PR.E |

Perpetual-Discount |

-1.53 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.64

Evaluated at bid price : 21.91

Bid-YTW : 5.65 % |

| POW.PR.D |

Perpetual-Discount |

-1.46 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.98

Evaluated at bid price : 22.21

Bid-YTW : 5.64 % |

| TD.PF.E |

FixedReset |

-1.40 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.53

Evaluated at bid price : 21.84

Bid-YTW : 4.17 % |

| FTS.PR.H |

FixedReset |

-1.39 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 14.16

Evaluated at bid price : 14.16

Bid-YTW : 3.99 % |

| SLF.PR.B |

Deemed-Retractible |

-1.37 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 21.60

Bid-YTW : 6.89 % |

| SLF.PR.D |

Deemed-Retractible |

-1.36 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.27

Bid-YTW : 7.40 % |

| BAM.PF.H |

FixedReset |

-1.35 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2020-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.65

Bid-YTW : 4.45 % |

| CU.PR.D |

Perpetual-Discount |

-1.30 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 21.66

Evaluated at bid price : 21.94

Bid-YTW : 5.64 % |

| TD.PR.S |

FixedReset |

-1.22 % |

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 24.20

Bid-YTW : 3.49 % |

| CIU.PR.A |

Perpetual-Discount |

-1.16 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.50

Evaluated at bid price : 20.50

Bid-YTW : 5.69 % |

| NA.PR.S |

FixedReset |

-1.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 4.31 % |

| IGM.PR.B |

Perpetual-Premium |

-1.07 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2018-12-31

Maturity Price : 25.00

Evaluated at bid price : 25.03

Bid-YTW : 5.74 % |

| RY.PR.M |

FixedReset |

-1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.20

Evaluated at bid price : 20.20

Bid-YTW : 4.26 % |

| ENB.PR.A |

Perpetual-Discount |

1.04 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 22.98

Evaluated at bid price : 23.25

Bid-YTW : 5.98 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| RY.PR.Q |

FixedReset |

190,141 |

Recent new issue.

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2021-05-24

Maturity Price : 25.00

Evaluated at bid price : 25.66

Bid-YTW : 5.02 % |

| NA.PR.S |

FixedReset |

137,370 |

TD crossed 130,000 at 19.00.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.00

Evaluated at bid price : 19.00

Bid-YTW : 4.31 % |

| GWO.PR.N |

FixedReset |

56,825 |

Scotia crossed 45,000 at 13.90.

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 13.65

Bid-YTW : 9.82 % |

| FTS.PR.M |

FixedReset |

52,750 |

Desjardins crossed 50,000 at 20.45.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 20.32

Evaluated at bid price : 20.32

Bid-YTW : 4.20 % |

| BIP.PR.B |

FixedReset |

34,721 |

Recent new issue.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 22.78

Evaluated at bid price : 24.00

Bid-YTW : 5.73 % |

| CM.PR.O |

FixedReset |

32,000 |

RBC crossed 25,000 at 19.62.

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 19.39

Evaluated at bid price : 19.39

Bid-YTW : 4.13 % |

| There were 11 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| Issue |

Index |

Quote Data and Yield Notes |

| VNR.PR.A |

FixedReset |

Quote: 18.47 – 20.00

Spot Rate : 1.5300

Average : 0.8870

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 18.47

Evaluated at bid price : 18.47

Bid-YTW : 4.99 % |

| BMO.PR.Q |

FixedReset |

Quote: 20.21 – 21.27

Spot Rate : 1.0600

Average : 0.6874

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2022-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.21

Bid-YTW : 5.97 % |

| SLF.PR.I |

FixedReset |

Quote: 20.41 – 21.20

Spot Rate : 0.7900

Average : 0.5261

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.41

Bid-YTW : 6.24 % |

| MFC.PR.J |

FixedReset |

Quote: 20.80 – 21.50

Spot Rate : 0.7000

Average : 0.4445

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 20.80

Bid-YTW : 5.98 % |

| SLF.PR.H |

FixedReset |

Quote: 17.85 – 18.56

Spot Rate : 0.7100

Average : 0.4601

YTW SCENARIO

Maturity Type : Hard Maturity

Maturity Date : 2025-01-31

Maturity Price : 25.00

Evaluated at bid price : 17.85

Bid-YTW : 7.37 % |

| PWF.PR.T |

FixedReset |

Quote: 22.89 – 23.95

Spot Rate : 1.0600

Average : 0.8240

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2046-01-04

Maturity Price : 22.36

Evaluated at bid price : 22.89

Bid-YTW : 3.56 % |