My attention was drawn to a piece by David Berman of the G&M, in which he touted the virtues of ZEB, BMO Equal Weight Banks Index ETF. I took issue with one rather careless line in the analysis, but was fascinated by one of the reader comments:

I own bank stocks and have done so for many years with great results.

But recently a friend introduced me to BK which is an ETF doing covered calls on the Canadian banks. Pays 15% annual dividends distributed monthly. Trying to figure out the downside on this.

Any opinions are appreciated.

My interest was piqued because I recently contributed to a FWF thread titled Covered Call ETF’s – Why? in which the pro-CC forces did battle with battalions of the anti-CC stripe. Also because, as we all know, BK is a SplitShare Corporation that, like most (all?) of the others, regularly touts its covered call programme:

. To generate additional returns above the dividend income earned on the portfolio, The Company engages in a selective covered call writing program.

So I responded:

BK is the Capital Units of a SplitShare Corporation and therefore has special risks all of its own. For starters, it’s leveraged. The capital units will stop paying dividends if the Whole Unit NAV falls below $15, which is another wrinkle often missed.

Hardly a thesis, but there’s enough there to tell the questioner where to begin asking questions about this wonderful investment that pays 15% annual dividends due in part to the magical powers of Covered Calls.

And that got me wondering: just what is the performance of BK/BK.PR.A Whole Units vs. ZEB? We shouldn’t really use the S&P/TSX Capped Financial Index (TTFS) as a comparator, because that includes insurers. While I have no doubt that there are lots of people who meticulously decompose TTFS into appropriate components, or have access to such data, I’m not one of them!

There’s performance data, of a sort, in the 2024 BK Annual Report and the ZEB Web Page (where you can show Annualized Performance as of 2024-11-30 after a bit of fiddling).

| Issue |

One

Year |

Three

Year |

Five

Year |

Ten

Year |

| ZEB |

+39.76% |

+9.68% |

+11.92% |

+9.89% |

BK

Whole

Units |

+34.31% |

+12.14% |

+11.96% |

+9.21% |

So ZEB has done a little better over the ten year period than the BK Whole Units, but given the volatility of the relative returns as imperfectly reflected in these data, nothing to really write home about.

Now, zealots of the Covered Call faith will be quick to dismiss such heterodox notions and point out that the banks have been on fire for the past ten years. And the only coherent defence of their religion I have ever seen cheerfully admits that a covered call strategy will underperform in good times (because occasionally you have positions called away and replaced at higher prices; or you have to buy back your options before this happens, again at higher prices) but that this is compensated for by corresponding outperformance in bad times. This may not achieve much, net, over a cycle but it does reduce your volatility for those who care about such things. So we’ll wait for some banking bad times and see what happens.

That coherent defence of Covered Callism? It was some time ago I read it, but I think it was on the CBOE website. Those of you with a prediliction for archaelogical librarianism might wish to find it and post a link in the comments, because I got stuck!

Update, 2026-02-07 : OK, so I found some information which may or may not actually be what I remember, but is certainly consistent with it: see the links referenced on the index dashboard for the Cboe S&P 500 BuyWrite Index (“BXM”).

I just hope that earnest inquirer in the Globe comments sees my response and does some checking, because there’s no way 15% is sustainable. As DBRS said in their most recent confirmation of BK.PR.A:

Without giving consideration to capital appreciation potential or any source of income other than the dividends earned by the Portfolio, the Preferred Share distributions together with the current distributions on the Class A Shares will create a projected grind on the NAV of the Portfolio of approximately 9.3% per year over the next 5 years.

… and while it might be tempting to think there is a huge population of option buyers out there, eager to overpay for call options so they can underwrite excess performance for sleazy CC salesmen, I’m not convinced that call option buyers are that dumb.

See the sections Sequence of Returns Risk and The effect of Cash Income on Sequence of Returns in my discussion of SplitShare credit quality to learn more about cash grind.

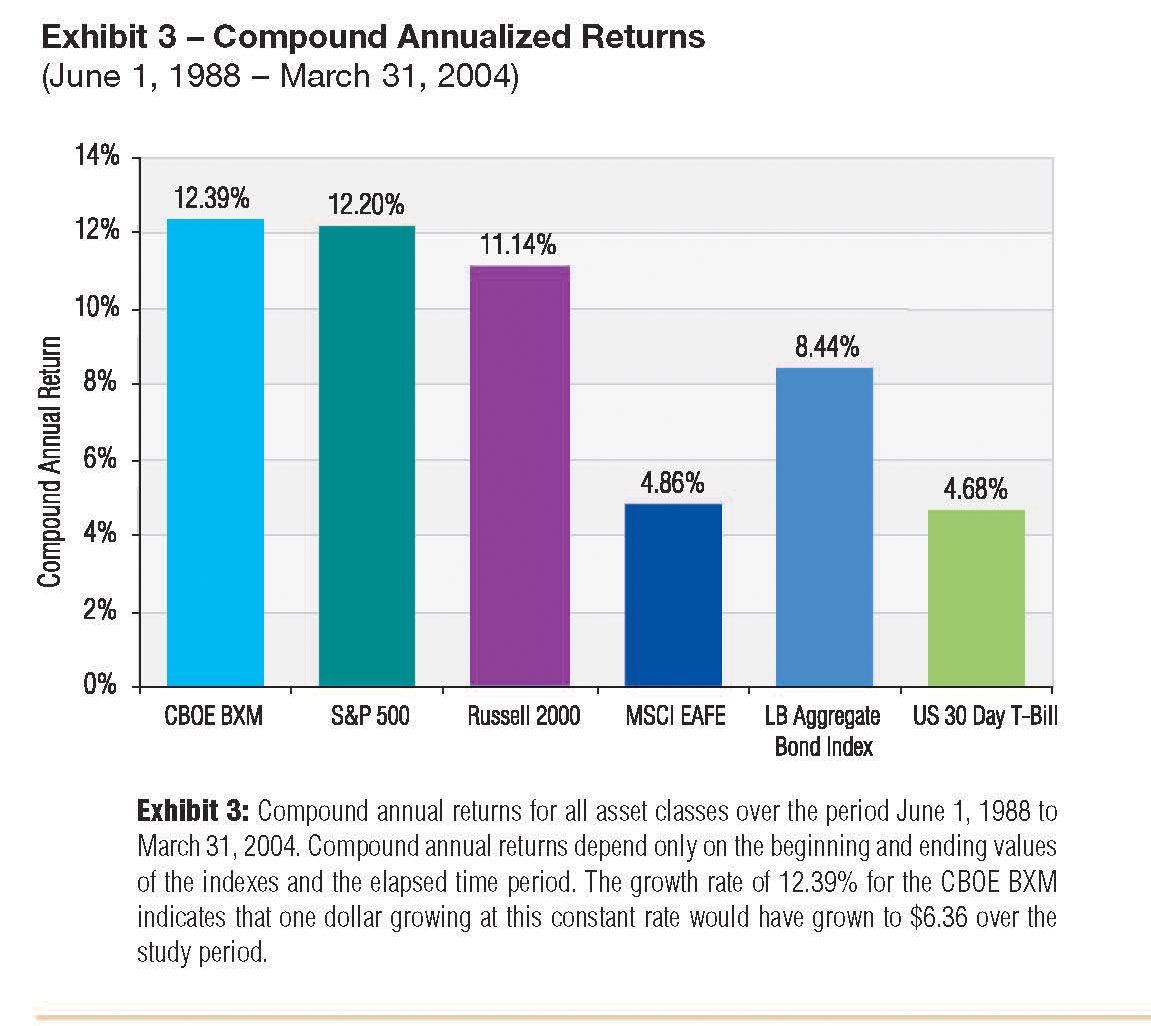

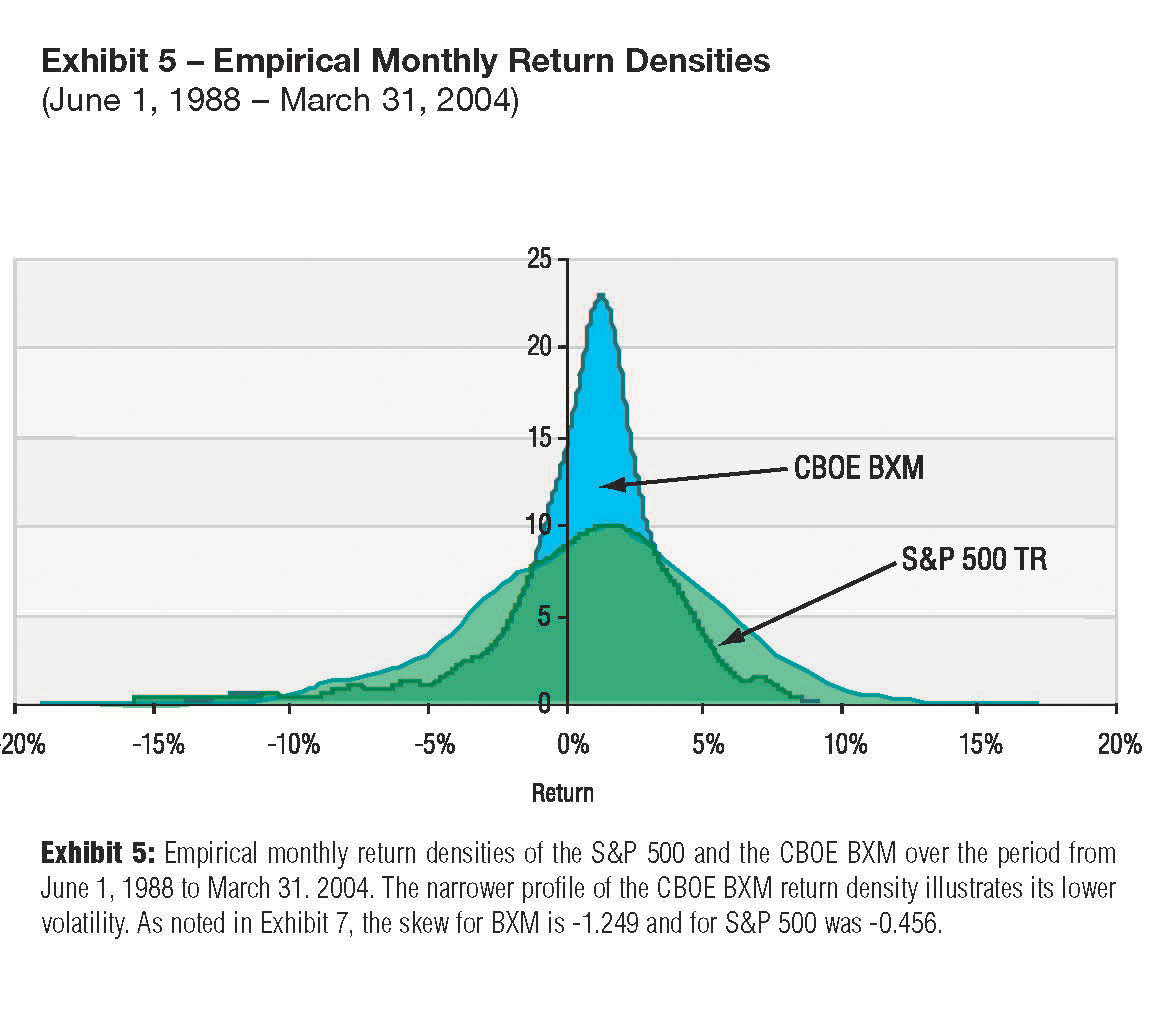

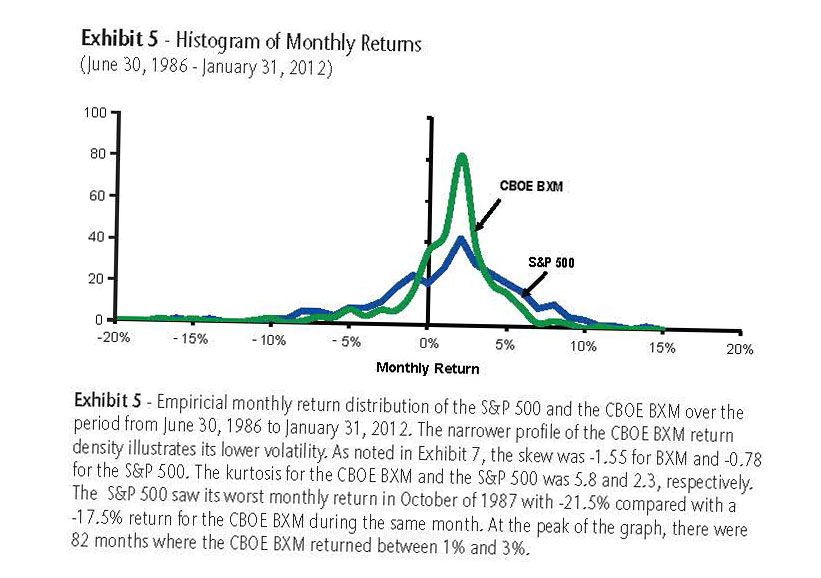

Update, 2026-02-08: So I continued to be interested in this questions and looked more closely at the data provided by the CBOE for its BXM product, the Cboe S&P 500 BuyWrite Index. The early study by Ibbottson was fascinating, with two very interesting pictures:

As indicated on these charts, the period examined was 1988-06-01 to 2004-03-31 … this is old data, but interesting nonetheless.

CBOE also publishes a fact-sheet (I’m not sure how often it’s produced), which is on-line at LINK. I have also stored this report (dated 2025-12-31) here on PrefBlog so future generations of researchers can verify that I’ve copied the numbers correctly.

The fact-sheet doesn’t reproduce the pretty pictures provided by Ibbottson, but they do present the data in a table. This may be compared with the Ibbottson data; I’ve also found a report on the CBOE site from Hewitt EnnisKrupp which I’ve tucked away HERE. The Hewitt EnnisKrupp report came with another pretty picture that matched the ideal look for the covered call concept:

| Data Source |

Period |

BXM

Annualized

Return |

S&P 500

Annualized

Return |

BXM

Annualized

Volatility |

S&P 500

Annualized

Volatility |

| Ibbottson |

1988-06-01

2004-03-31 |

12.39% |

12.20% |

10.99% |

16.50% |

| Hewitt EnnisKrupp |

1986-06-30

2012-01-31 |

+9.2% |

+9.2% |

11.4% |

15.9% |

| CBOE |

1986-06-20

2025-12-31 |

8.5% |

11.1% |

10.7% |

15.2% |

Fascinating, eh? It’s unfortunate that the starting points of the analyses are different, particularly since the fact-sheet includes the crash of ’87 and Ibbottson doesn’t, but nonetheless very interesting, particularly since the Ibbottson study was as of March 2004, when the democratization of investing (via discount brokerages and ETFs) was in its infancy whereas the data samples nowadays include the gamification of investing and negligible trading costs.

It looks like:

- The buy-write strategy, as exemplified by the S&P 500 and BXM, is no longer as attractive as it used to be from a total return perspective; the buy-write strategy is, in fact, markedly inferior in this respect to simply buying the damn index

- The buy-write strategy seems to have gotten somewhat worse at reducing volatility

It would be very interesting to get the raw data together and rip this thing apart until a good understanding of these apparent changes has been achieved. Of particular interest, I think, would be looking at the effect of fiddling with the index construction: it rolls the one-month call at a strike-price that is closest to, but above, the index value at the time of the roll. Why not a longer term? Why not a portfolio of short calls, laddering the term somehow to reduce transaction sizes and get some term premium, maybe varying the strike prices (and making adjustment trades throughout the term of the ladder, maybe, to get the strike prices of the various components within some kind of tolerance of the ideal)? Why not a more out-of the-money call? And why not more realistic pricing of the expected cost of the roll than simply assuming VWAP, since you can’t really expect to get VWAP consistently if you’re constrained to sell. Decisions, decisions…

But retail investors shouldn’t hold their breaths waiting for a fund vendor to assemble and analyze these data. The project has probably been done by research departments at the big investors of their own money, such as insurance companies and pension plans that directly manage their own funds; and there’s probably a few institutional investment firms that have done it; but retail investors? Sorry guys, you’re stuck with the Other People’s Money department of the banks and sell-side; facts don’t matter, nobody cares, let’s have lunch and pretend we know stuff.

I did find one fund that tracks BXM, Invesco S&P 500 BuyWrite ETF. It does a pretty good job of tracking the BXM index, but the 25Q4 fact-sheet (copy stored by PrefBlog HERE) confirms the recent collapse of returns relative to the underlying S&P 500:

| Performance of |

1-Year |

3-Year |

5-Year |

10-Year |

| ETF – NAV |

+8.47% |

+13.07% |

+8.87% |

+6.74% |

| S&P 500 |

+17.88% |

+23.01% |

+14.42% |

+14.82% |

… and the website also informs us that this ETF has about 340-million under management. The call buyers are feasting … if we assume that the fund has had 340-million under management throughout the last ten years, and observe that the underperformance apparently caused by the option-writing overlay (I am ASSUMING that the tracking error for the S&P 500 holding is negligible, since that’s so easy to do nowadays) is 8% annually, that comes to … um … 27-million annually of client money vapourized by this single fund alone.

PS: Another fund is the Global-X S&P 500 Covered Call ETF that doesn’t track BXM as well, but claims $3.17 billion AUM.

PPS: There’s a study by Wilshire on the CBOE site, which I have tucked away HERE that – finally! – provides annual data for the period 2001-2018.

HIMIPref™ Preferred Indices

These values reflect the December 2008 revision of the HIMIPref™ Indices

Values are provisional and are finalized monthly |

| Index |

Mean

Current

Yield

(at bid) |

Median

YTW |

Median

Average

Trading

Value |

Median

Mod Dur

(YTW) |

Issues |

Day’s Perf. |

Index Value |

| Ratchet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0747 % |

2,478.2 |

| FixedFloater |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

0.0747 % |

4,699.1 |

| Floater |

5.81 % |

6.06 % |

57,680 |

13.78 |

3 |

0.0747 % |

2,708.1 |

| OpRet |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0629 % |

3,669.0 |

| SplitShare |

4.76 % |

4.58 % |

86,321 |

3.04 |

5 |

-0.0629 % |

4,381.6 |

| Interest-Bearing |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0629 % |

3,418.7 |

| Perpetual-Premium |

5.67 % |

5.57 % |

565,856 |

6.78 |

7 |

-0.0906 % |

3,078.2 |

| Perpetual-Discount |

5.56 % |

5.62 % |

51,479 |

14.44 |

27 |

0.1388 % |

3,406.2 |

| FixedReset Disc |

5.94 % |

6.00 % |

113,182 |

13.75 |

28 |

-0.0953 % |

3,173.9 |

| Insurance Straight |

5.46 % |

5.55 % |

65,787 |

14.51 |

22 |

0.0217 % |

3,330.2 |

| FloatingReset |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0953 % |

3,775.7 |

| FixedReset Prem |

5.97 % |

4.33 % |

84,902 |

2.53 |

20 |

0.0691 % |

2,657.5 |

| FixedReset Bank Non |

0.00 % |

0.00 % |

0 |

0.00 |

0 |

-0.0953 % |

3,244.3 |

| FixedReset Ins Non |

5.28 % |

5.49 % |

77,138 |

14.46 |

14 |

0.0859 % |

3,133.2 |

| Performance Highlights |

| Issue |

Index |

Change |

Notes |

| ENB.PR.N |

FixedReset Disc |

-1.81 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.17

Evaluated at bid price : 24.37

Bid-YTW : 6.02 % |

| GWO.PR.H |

Insurance Straight |

-1.36 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 21.51

Evaluated at bid price : 21.77

Bid-YTW : 5.63 % |

| PWF.PF.A |

Perpetual-Discount |

-1.09 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 20.05

Evaluated at bid price : 20.05

Bid-YTW : 5.66 % |

| CU.PR.G |

Perpetual-Discount |

1.03 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 20.68

Evaluated at bid price : 20.68

Bid-YTW : 5.45 % |

| FFH.PR.K |

FixedReset Prem |

1.14 % |

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2027-03-31

Maturity Price : 25.00

Evaluated at bid price : 25.65

Bid-YTW : 3.21 % |

| IFC.PR.A |

FixedReset Ins Non |

1.15 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 21.60

Evaluated at bid price : 22.00

Bid-YTW : 5.37 % |

| CU.PR.D |

Perpetual-Discount |

1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 22.05

Evaluated at bid price : 22.28

Bid-YTW : 5.50 % |

| MFC.PR.F |

FixedReset Ins Non |

1.23 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 18.88

Evaluated at bid price : 18.88

Bid-YTW : 5.76 % |

| IFC.PR.K |

Insurance Straight |

2.49 % |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.39

Evaluated at bid price : 23.85

Bid-YTW : 5.55 % |

| Volume Highlights |

| Issue |

Index |

Shares

Traded |

Notes |

| FTS.PR.M |

FixedReset Disc |

215,493 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.13

Evaluated at bid price : 24.62

Bid-YTW : 5.55 % |

| SLF.PR.H |

FixedReset Ins Non |

102,000 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 21.95

Evaluated at bid price : 22.50

Bid-YTW : 5.60 % |

| ENB.PR.Y |

FixedReset Disc |

88,096 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 21.51

Evaluated at bid price : 21.51

Bid-YTW : 6.31 % |

| BN.PF.F |

FixedReset Disc |

70,647 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.20

Evaluated at bid price : 24.75

Bid-YTW : 5.87 % |

| MFC.PR.Q |

FixedReset Ins Non |

64,228 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.61

Evaluated at bid price : 25.32

Bid-YTW : 5.49 % |

| FTS.PR.K |

FixedReset Disc |

57,340 |

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 22.79

Evaluated at bid price : 23.65

Bid-YTW : 5.43 % |

| There were 15 other index-included issues trading in excess of 10,000 shares. |

| Wide Spread Highlights |

| See TMX DataLinx: ‘Last’ != ‘Close’ and the posts linked therein for an idea of why these quotes are so horrible. |

| Issue |

Index |

Quote Data and Yield Notes |

| ENB.PR.N |

FixedReset Disc |

Quote: 24.37 – 25.03

Spot Rate : 0.6600

Average : 0.4291

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.17

Evaluated at bid price : 24.37

Bid-YTW : 6.02 % |

| GWO.PR.M |

Insurance Straight |

Quote: 25.33 – 25.92

Spot Rate : 0.5900

Average : 0.3962

YTW SCENARIO

Maturity Type : Call

Maturity Date : 2026-03-08

Maturity Price : 25.00

Evaluated at bid price : 25.33

Bid-YTW : -3.06 % |

| POW.PR.B |

Perpetual-Discount |

Quote: 24.00 – 24.50

Spot Rate : 0.5000

Average : 0.3267

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.69

Evaluated at bid price : 24.00

Bid-YTW : 5.62 % |

| GWO.PR.H |

Insurance Straight |

Quote: 21.77 – 22.30

Spot Rate : 0.5300

Average : 0.3734

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 21.51

Evaluated at bid price : 21.77

Bid-YTW : 5.63 % |

| BN.PF.A |

FixedReset Prem |

Quote: 25.65 – 26.11

Spot Rate : 0.4600

Average : 0.3083

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 23.65

Evaluated at bid price : 25.65

Bid-YTW : 5.84 % |

| PWF.PR.E |

Perpetual-Discount |

Quote: 24.30 – 24.88

Spot Rate : 0.5800

Average : 0.4631

YTW SCENARIO

Maturity Type : Limit Maturity

Maturity Date : 2056-02-06

Maturity Price : 24.05

Evaluated at bid price : 24.30

Bid-YTW : 5.69 % |